Each December, as most of us prepare to celebrate the holiday season, Wall Street luminaries deliver their outlooks for the year ahead. Typically, they “predict” where markets will finish in the coming year and detail key risks that could lie ahead. Respected Chief Economist at Deutsche Bank, Torsten Slok, prepared a list for 2020 market risks that can be found here.

His list is thoughtful and encapsulates a lot of the same concerns that many market experts were also weighing at the time, so this is by no means an attempt to discredit him. Notably, the emergence of Covid-19 was absent from his list, which would go on to have the greatest market impact in over a decade. In early 2020, the Covid-19 pandemic would take grip of the world, sending markets into a panic seemingly overnight as the S&P 500 fell 34% from February 19th to March 23rd. Also absent from his list was mention of the drastic increase in inflation that we are experiencing in today’s economy.

I am quite sure that if we were able to review every single economist’s list of risks from that time, very few would have Covid-19 listed as a possibility. Perhaps, some of the more germophobic pundits may have included health pandemics, but they probably included it as a matter of personal fear rather than an impending outbreak.

As the news of the pandemic broke, hysteria and fear ensued, bringing the market to its knees in an instant. Reflecting back, it’s hard to put into words the level of uncertainty humanity was facing. Few people on earth had lived through such a pandemic. Some warned it was the second coming of the Spanish flu, while others dismissed it entirely. No one knew how deadly it would be, how it was transmitted, where it came from, if it could be treated, who it targeted, etc. The questions were endless, and the answers were few. As a result, we found ourselves living through a time so surreal and bizarre that it felt as if it couldn’t really be happening.

I don’t care how smart you are, how well you speak or write, how successful your past returns have been, how much market research you do; to my knowledge, there is no way to predict the future. Yet, there’s often a belief that good investors know more about the future than lessor ones. (Maybe it’s because we want to believe that the future can be predicted.) The events of the Covid pandemic only reminded us of what a fool’s errand attempting to predict the future is. It was an event no one saw in advance. Almost as equally unexpected as the pandemic itself was the market’s rapid recovery. Therefore, if the future remains unknowable, and the markets’ reaction to these events is unpredictable, then we should conclude that investing isn’t predicting what may come next but adapting to what is occurring.

During the March lows of 2020, we found ourselves actively redeploying client assets as we considered new realties. Fortunately, many of the experiences we’ve gained over the years have helped us craft a methodical approach for periods of market instability. As we’ve said many times in past writing, market volatility can be quite helpful for investors who have the tools to navigate it. Many investors have been programmed into thinking that passive investing is superior to active investing. I’ve often used the analogy that passive investing is like cruise control; it’s wonderful when the highway is free of obstacles. In turbulent times, a more attractive approach tends to gain favor, only to wane as the seas calm and investors lose sight of the last storm.

Active management is a concept often misunderstood by casual investors. Generally, people tend to think that active management means doing stock-specific research and deciding whether to buy Nike versus Adidas (as an example). This is generally referred to as security selection. In truth, security selection is not the most important aspect in active management. Let’s use the last few years as a framework for thinking about the key active decisions one could have taken in managing a portfolio. In the height of the Covid panic, did it matter whether you held Nike or Adidas? No, they both were collapsing along with the market as a whole. A far more impactful action to navigate the Covid market meltdown was to rotate out of safer assets that had held up better than the overall market (i.e., bonds). By swapping safe assets that held up admirably during the storm and buying stocks at depressed levels, you would have earned a handsome return. Fortunately, for many of our clients, we were able to do exactly that during the market pandemonium caused by Covid.

Another broad portfolio shift that’s been even more critical of late has been adapting to the increasing presence of inflation, particularly as it relates to bond holdings. Bonds are debt that typically pay a fixed interest rate over a set period of time. Let’s say you own bonds in a quality company that reliably pays you 3% for ten years. While 3% isn’t the most exciting return on your money, one might conclude that at least you aren’t in cash earning nothing and/or losing purchasing power. However, lately, the problem with owning bonds that yield 3% is that inflation has been running around 7%. Therefore, each year this rate of inflation continues, your bond holdings are “losing” 4% because you’re not keeping up with rising prices. Making matters worse, as inflation rises, interest rates follow suit which decreases the value of bond holdings. It’s also important to note that the length of the bond matters immensely. Very short-term bonds see more minimal impact whereas longer term bonds will incur substantial declines.

As it became more apparent that inflation was setting in, as a firm, we began rotating into investments that offered more protection from inflation. Since bonds typically make up a significant portion of most investors’ overall portfolio, avoiding losses is far more impactful than whether you choose, as an example, to own Nike or Adidas. In addition, as I will describe below, recognizing that the inflationary environment was escalating after decades of calm prices was only half the battle. The additional step required was to understand what investments offered the ability to avoid the negative impacts of inflation. Said more basically, it’s great to notice there’s a fire in the building, but if you don’t know how to find the exit, it doesn’t do you much good.

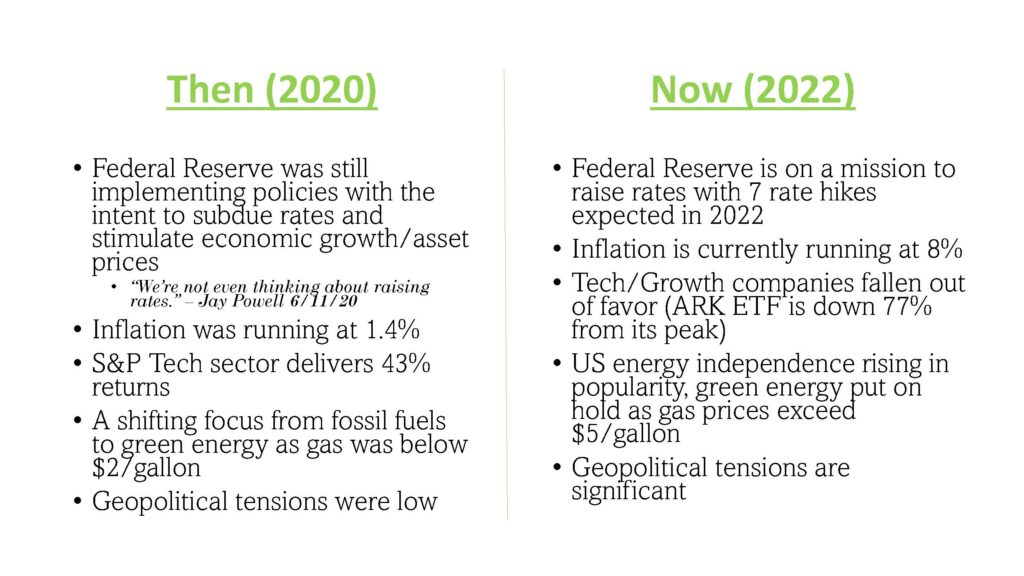

Today, we find ourselves in a situation that is anything but smooth sailing. The Federal Reserve is faced with inflation levels we haven’t experienced in decades. The plan was a set of measured rates hikes that were supposed to start cooling prices without triggering a recession. This already delicate task was massively complicated by Russia's invasion of Ukraine, further fanning the flames of inflation. In a best-case scenario, the situation in Ukraine will de-escalate, and we’ll go back to the more singular challenge of inflation. However, a range of less optimistic outcomes remains an ominous possibility. As we did during the height of the pandemic, we as a firm must again adapt to certain new realities. I’ve highlighted some of the most critical challenges we are facing today:

Given these new realities, we are actively taking steps to mitigate risks and capitalize on opportunities. Said another way, if we are forced to play with this set of cards, what’s the best way to do it? This is a question we find ourselves asking constantly at Evergreen woven deeply into our investing fabric. We will leave predicting the future - which none of us control - to the fortune-tellers, while we focus on how we adapt our investments to the current environment - which is something we do control.

Here's a simple summary of the process we practice that has helped us navigate past crises with success:

I titled this piece “Stranger Than Fiction” because future events that will unfold go beyond what anyone can imagine. After all, so many of the events that have led to periods of market instability seemed inconceivable until they occurred. Who would have thought the tech bubble in the 1990s would have formed? The valuation for many companies defied anything a mathematical formula taught by any discipline within finance could explain. The seemingly brilliant financial models built during the housing crisis seem comically flawed with the benefit of hindsight. The emergence of a global pandemic that came out of nowhere reshaped our daily lives in ways only found in movies or books. The sights in Ukraine as the largest European conflict since WWII wasn’t "supposed" to happen in the modern world. If nothing else, periods of instability should remind us just how unstable the world can be. Smart investors will not simply hope that nothing unpredictable occurs in the future. Nor will they think that they or someone else can predict such instances. Fortunately, many of our clients have been through enough of these periods with us to know you don’t have to predict the future to protect and grow assets. After all, even if we knew the future and told you what it would hold, I’m not sure anyone would believe it.

Tyler Hay

Chief Executive Officer

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.