“Oh, and I hear all the time that this isn’t anything to what we were seeing at the peak of the tech bubble in 2000. Sure – knock yourself out with that one.”

– David Rosenberg, Sept 4th, 2020

“Today’s concurrent bubbles in equities and bonds is of epic proportions. We are witnessing single stock behavior on par with the most excessive extremes of 1999 and 2000, and in many cases, it is worse.”

– Jones Trading’s Mike O’Rourke, The Closing Print, September 30th, 2020

“When the capital development of a country becomes the by-product of a casino, the job is likely to be ill-done.”

– John Maynard Keynes

*Note: The featured image for today's article is of The Monte Carlo Casino, officially named Casino de Monte-Carlo, which houses a world-famous casino, Le Grand Théâtre de Monte Carlo, a key theme in today's missive.

______________________________________________________________________________________________________

If it’s October it must be time for the World Series, that signature event for America’s once-upon-a-time favorite pastime, right? Undoubtedly, millions of baseball fans simply have to be waiting in breathless anticipation for the 117th anniversary of the Fall classic (or 136th if you use the alternative starting year of 1884, as do some baseball pundits). Actually, this year take the “Un” off of “undoubtedly”.

Maybe it’s watching NL and AL teams playing before cardboard fans that’s taken the thrill out of this Autumn’s playoffs. Or maybe it’s the shortened season that makes it all feel kind of strange and pointless. As with so many things these days, major league baseball just doesn’t seem normal – other than that the Seattle Mariners will once again be nowhere to be found in the post-season. Thank you, M’s, for that little bit of constancy in this totally foreign world we find ourselves in today!

Fortunately, for millions of mostly younger folks there is a new game in town that has superseded the World Series in popularity and has even become a worthy rival to the NFL (which seems much more like the real deal, at least to this admittedly inexpert observer). Moreover, it affords a gambling opportunity that far eclipses betting on baseball, football, and, perhaps, fantasy teams (I know that last one is highly debatable). What pray tell is this utterly captivating alternative option? Yes, that’s it: the option market (ok, purists would say the options market).

Considering that listed options contracts began trading in 1973, they are not exactly a new invention. Bespoke options actually go back as far as ancient Greece, but they didn’t really attract much of a following until they became highly liquid thanks to the CBOE (Chicago Board Options Exchange) nearly 50 years ago. But, frankly, these derivatives rarely attracted broad retail investor interest. More typically, they were used by large institutions to hedge their underlying stock or market index positions. Lately, though, it’s been, shall I say, a very different ball game.

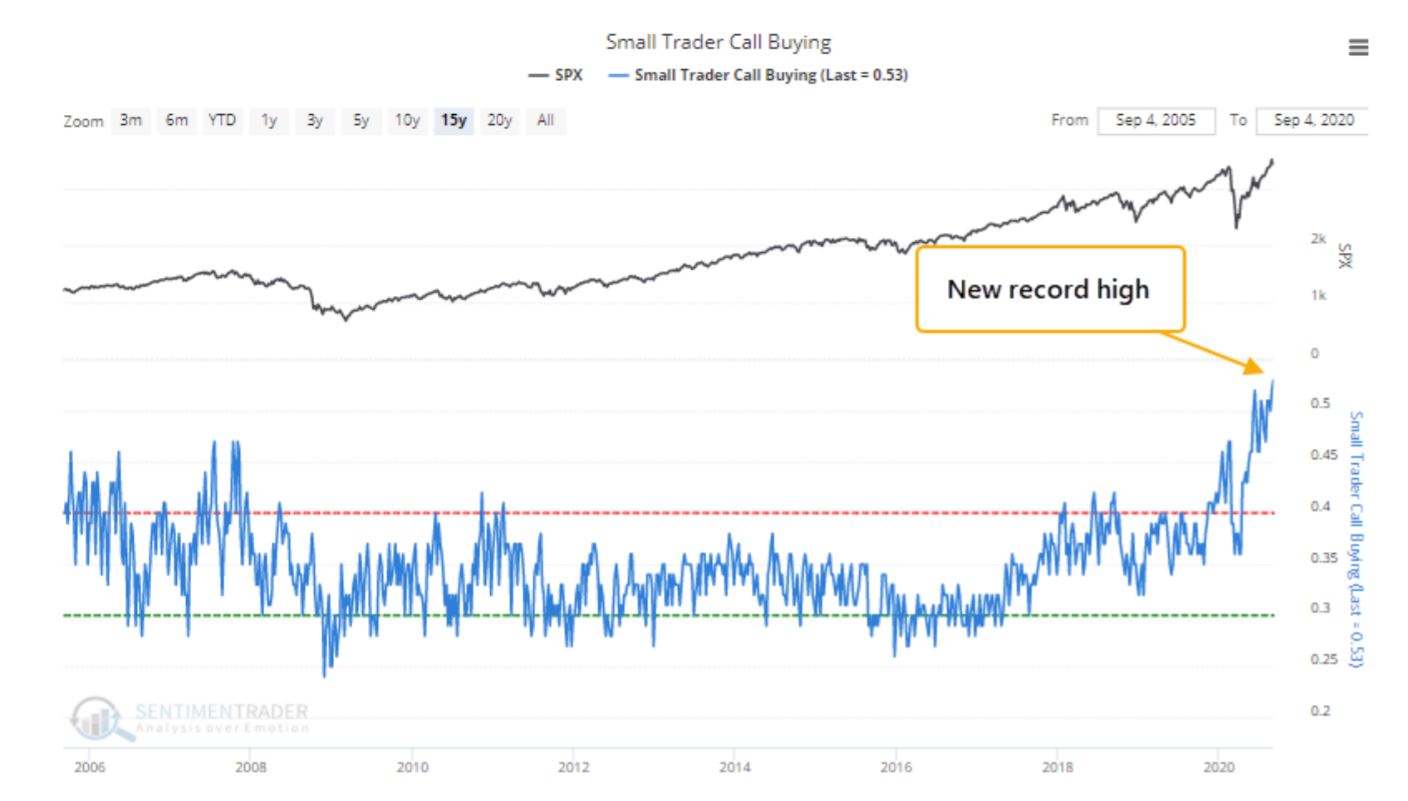

As Barron’s Andrew Bary and Avi Salzman noted in the September 14th issue, quoting Sundial Capital Research’s president, Jason Goepfert: “There has been a huge ramp-up in speculative trading”, calling it “a retail option-trading frenzy. These small traders have become the biggest part of the options market.”

Source: SentimenTrader, Jason Goepfert

Mr. Goepfert proved his point by stating that since mid-July 60% of opening call options (i.e, purchases) involved contracts of 10 or less. These small trades are clearly the province of the retail speculator. And, unquestionably, speculation it is and, as it turns out, in one of its wildest forms.

Before getting to that aspect, let me provide a very brief primer for those too prudent to be familiar with options. First, these are not the stock options that companies lavishly award to their senior executives. Those are often the path to vast wealth, unlike the speculative CBOE variety that more often than not impoverish those amateurs who dare to dally in them.

The two types of listed options are calls and puts. The underlying contracts involve 100 shares, known in olden days as round lots. The purchase and/or sale price is called the premium. This amount entitles the buyer to either acquire or dispose of the underlying shares for a specified length of time, typically less than a year, at a fixed price.

A call gives the holder that right to buy the underlying stock (or index, for that matter) at, say, $50 for the remaining term of the contract ($50, in this case, is known as the strike price in options lingo). An example would be a stock trading at $45 with a $50 strike price where the buyer might pay $2 per share, or $200. Consequently, this option buyer would control an underlying security worth $4,500 ($45 times 100 shares) for that small sum of two C-notes (aka, Benies).

This sounds great but, again, this isn’t a permanent right. As noted above, it only exists for the length of the contract. Let’s assume that is six months in this instance. Therefore, even if the stock rises by $5 over that timeframe, or about 11%, the option holder loses his or her entire investment. (Option prices can certainly be less than in my example; the market values the options of more volatile stocks at higher prices than those that are more placid.) If the stock stays flat or falls, it’s also obviously a total wipeout for the options punter.

This is an even a worse set of odds than described by former Ohio State football head coach Woody Hayes (who was no fan of the air game). In a famous quip, he said that with a forward pass only three things can happen and two of them are bad (incomplete or intercepted). In the case of options, it’s three out of four: down, flat, and up a bit are all bad (per the above example). Only up significantly is a winner. (It is possible to buy options where the underlying stock is trading at or above the strike, or exercise, price but those are more expensive, reducing the upside leverage.)

Puts allow a holder to sell at a fixed price for a specified length of time. In this case, the strike price for a put on a $45 stock might be at $40. If $2 is again the premium, or cost, the stock needs to fall below $40 at the expiration date for the holder to recoup any of their outlay. But let’s assume that the put was on a certain alleged hydrogen-powered truck company where disclosures suddenly emerge of possibly fraudulent activities and the price crashes to $20 almost overnight. The lucky, or foresighted, put buyer would have an asset worth $2,000 (100 shares times $20), or ten times their investment.

Ok, got all of that? Probably not, unless you’re a seasoned investor or professional trader. Frankly, I don’t think a lot of the newbies playing the options game fully understand even the basics. Underscoring this point, a 20-year old options trader took his own life in a tragic twist earlier in the year after seeing a negative balance of $730,000 in his Robinhood account.

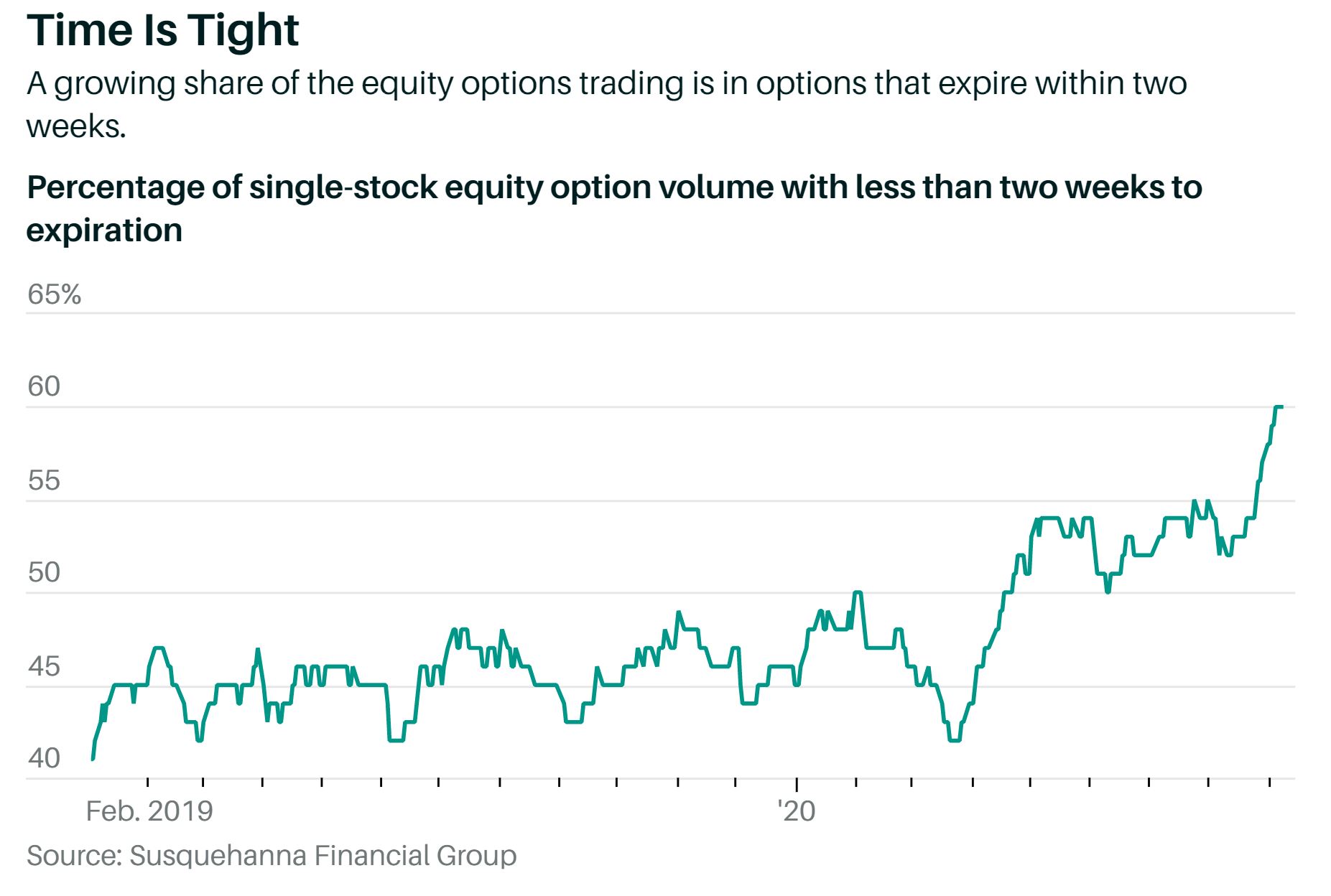

What’s ever more undeniable, is that options traders are extremely unconcerned about the rapid passage of time. The percentage of single-stock (i.e., not on an index) volume on options that expire in less than two weeks has soared to 60%.

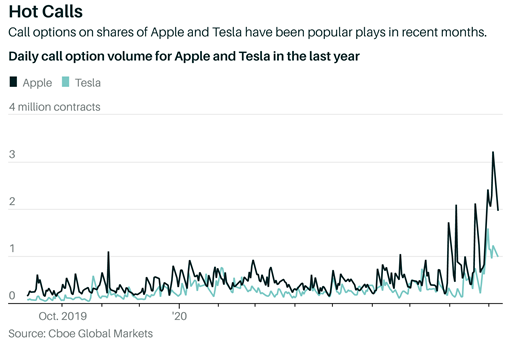

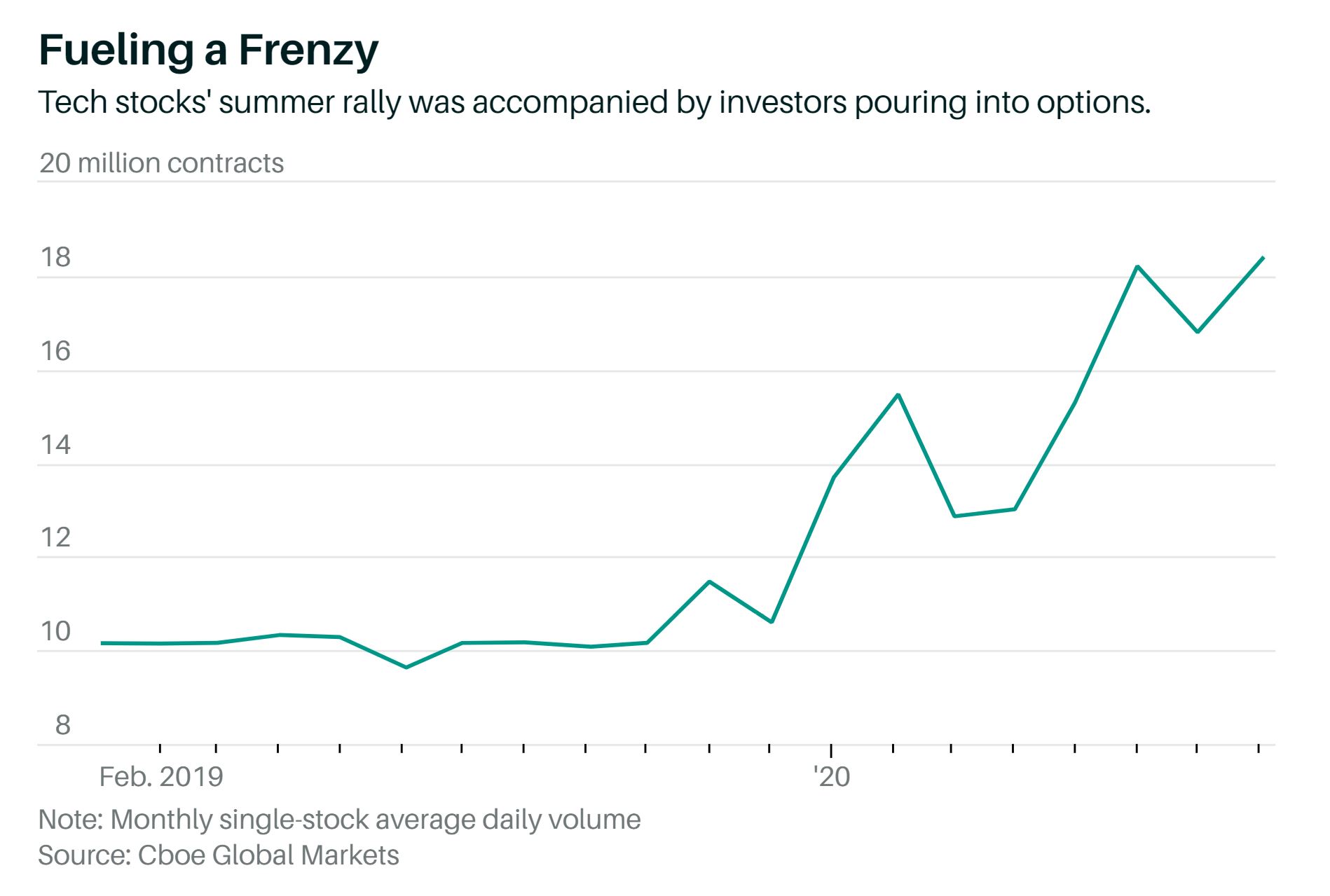

Two weeks is an absurdly short timeframe even in our current instant-gratification world. The odds are heavily stacked against this type of speculation. One might think few would be willing to make such a dangerous gambit. Yet, in the feverish month of August, when stocks like Apple and Tesla announced four-for-one and five-for-one splits, causing their prices to soar despite the reality that this action creates absolutely zero real value, option activity exploded. Single-stock option volume was the highest ever, 18.4 million contracts per day. This was up about 80% from 2019, as the aforementioned Barron’s article pointed out. Much of this frenetic activity was in those two high-profile, greed-stoking names.

Another, undoubtedly, is that the Robinhood and Davey Day Trader* (DDT) types are among the main forces behind this latest mania (adding to a very long list we’ve seen in recent years). However, it’s now been disclosed that a huge whale was swimming alongside the millions of minnows (and the Robinhooders/DDTers do truly number in the millions). My bestie and partner Louis Gave began telling our research team in early September that the Japanese tech leviathan Softbank (an early investor in China’s even more massive Alibaba) was likely the whale, which is exactly what was disclosed shortly thereafter. Softbank’s option punt amounted to around $4 billion.

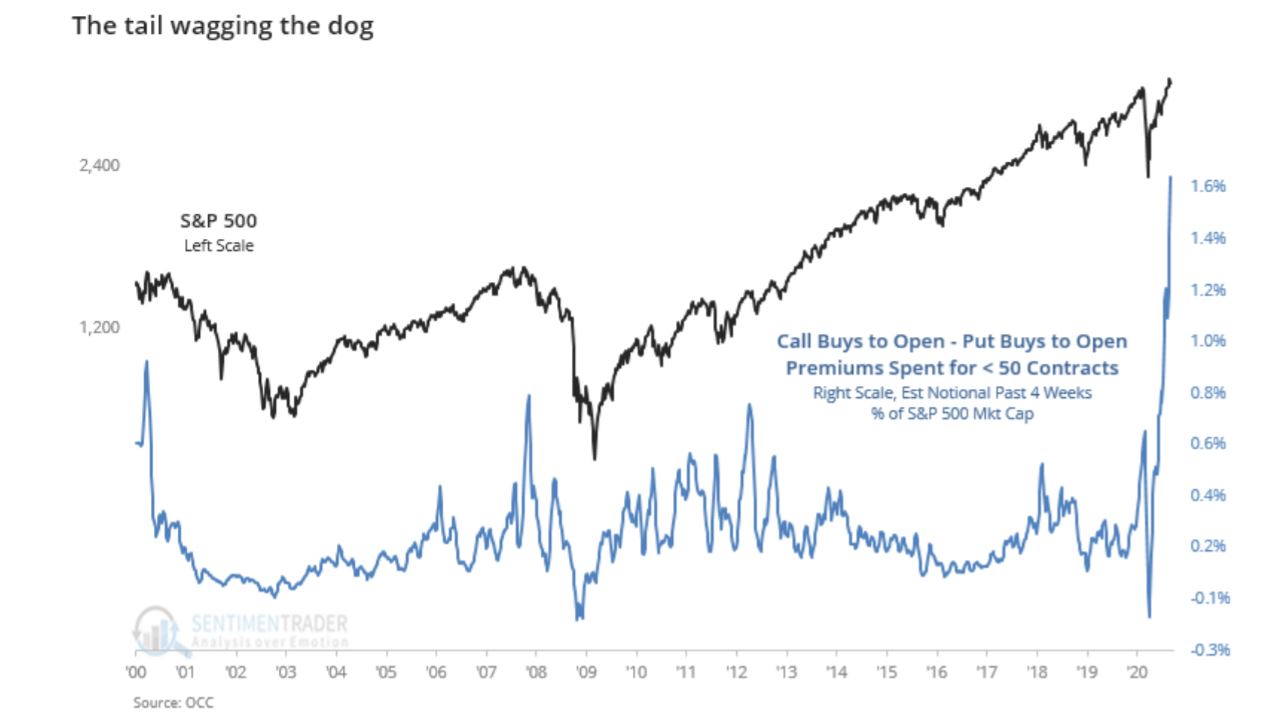

Maybe that doesn’t sound like much, but it concentrated this in just eight go-go growth stocks like Tesla and Apple. Further, remember that options contracts are highly leveraged plays on the underlying stocks. Thus, Softbank’s $4 billion spend translated into controlling some $50 billion worth of shares. This was in addition to the estimated nearly $500 billion of notional, or underlying, market value related to the feeding frenzy by retail speculators in option contracts, amounting to 1.7% of the S&P 500’s total capitalization. Additionally, this unfolded over just four weeks. As you can see below, the correlation with this astounding options volume surge and the August market leap was very tight.

Source: SentimenTrader, Jason Goepfert

Notice, too, that call option buying totally overwhelmed that of put buying. Thus, these speculators were wildly bullish (puts are bearish bets, as noted above). And this is a key part of the further amplification of the powerful upside pressure.

Calls can also be sold, not just bought. This can be done for extreme speculation (called “naked” call selling) or quite conservatively for the much better known “covered call writing”. In the latter case, the holder of, say, Microsoft, who may be thinking of selling part of his or her position, might sell some calls to generate cash. Should the share price rise above the strike price—hypothetically, $200 – causing the number of shares of Microsoft represented by the quantity of contracts sold to be “called away”, the investor is not unhappy. They have pocketed the call premium plus, generally, some appreciation above where the stock was trading when they sold the calls (perhaps $190 in this case).

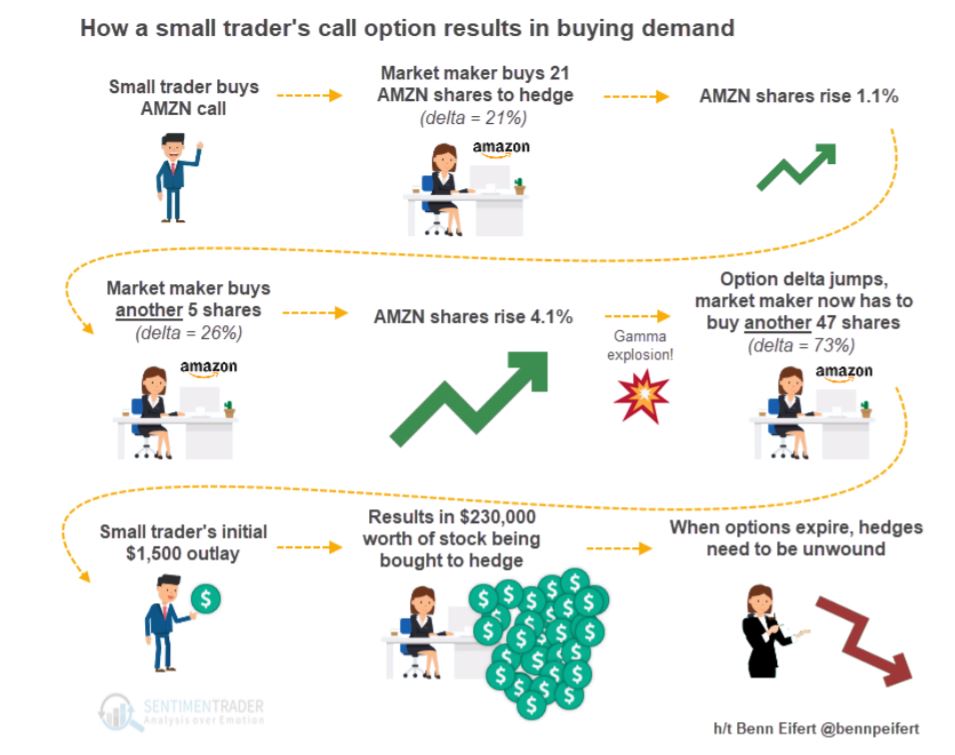

Generally, there is a decent balance between buyers and sellers of calls. However, that was decidedly not the case in August of this year. Because there were far more buyers of calls than sellers, as noted above, the firms that make markets in these options (for a fee or spread, of course) had a problem. As buying swamped selling, they were forced to buy the underlying shares to hedge their position risks. If you think this put unusual upside pressure on stocks like Tesla and Apple, you are spot-on.

There was another force at work that has to do with how much the options were rising versus the underlying stock (gamma and delta for options geeks) but that’s too esoteric to go into here other than to run the below schematic, again borrowing from Mr. Goepfert’s excellent missive on this phenomenon. However, suffice to say that it further stoked the speculative fires as buying beget buying…and buying and buying and buying.

Source: SentimenTrader, Jason Goepfert

All of the foregoing might give you the uncomfortable feeling that the US stock market has turned into a veritable casino. If you are right, per the opening quote from John Maynard Keynes, that implies problems for America’s long-term economic well-being. Because I would argue this casino-like behavior has been operative in many asset classes for years--producing a series of bubbles that swell and then burst--it might be a key reason why economic and financial conditions have become increasingly fragile. And, in fact, sudden market plunges have become more frequent in recent years.

Le Grand Casino de Amerique is reflected by much more than merely options market madness. Presently, there are 530 US stocks trading at over 10 times their underlying sales per share. This is the threshold that is widely considered to be a full-blown (sorry) bubble and is nearly the same percentage of total stocks at this nosebleed level that was seen in 2000, during the peak of dot.com insanity. The reality is that there is a plethora of what I’ve been calling COPS out there--Crazy Over-Priced Stocks. Accordingly, David Rosenberg’s quote from the top of page one is eminently defensible.

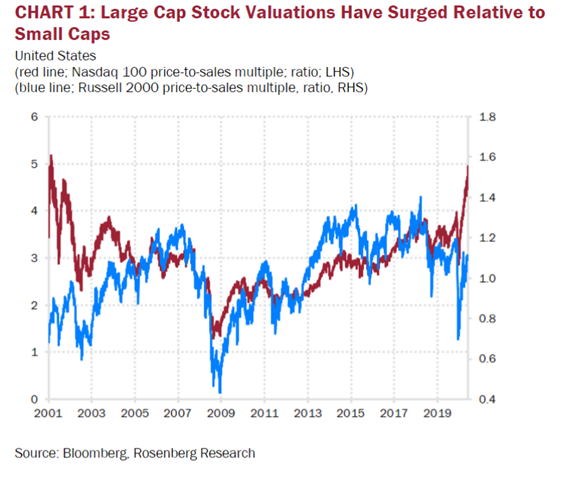

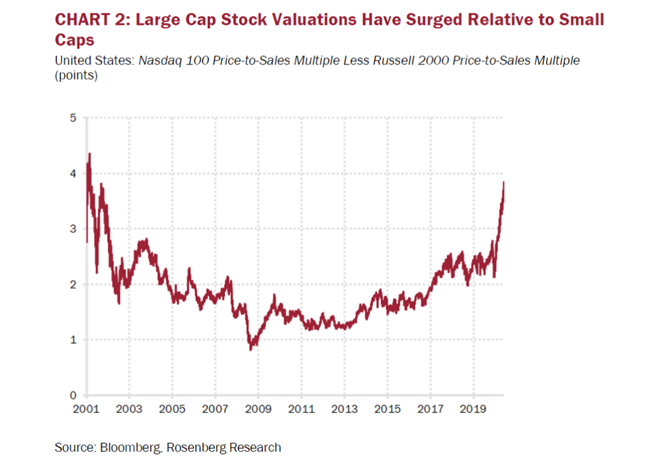

Need more? 60% of the Nasdaq is represented by merely 12 stocks and you can probably guess which they are. The Nasdaq 100 has now overtaken the value of the entire European stock market. The “Naz” 100 now trades at roughly 5 times sales, the highest ever (and showing how extreme 10 times sales truly is). Today’s de facto tech weighting, including issues like Google, Facebook and Amazon, which are officially designated in other sectors, is 38% of the S&P 500, greater than the 33% seen in 2000.

The five biggest companies in the S&P trade at an average P/E ratio of 44 vs not much below the 50 seen in 2000. Eight stocks make up 28% of the index, a higher concentration than 20 years ago. As was the case then, large cap growth stocks (the Naz 100) have soared to an extreme valuation premium over small cap stocks (the latter are now down roughly 12% for the year, taking an average of the Russell 2000 and S&P 600 small company indexes).

Of course, in the growth vs value race, it’s a similar story. Growth issues were up 26% year-to-date through September 30th versus a decline of 11% for value. This divergence has been occurring for nearly 15 years despite the fact that value has historically beaten growth in 92% of prior decades, leading to an average annual outperformance of 3.2% per year. Further, although the S&P was up 5.5% at the end of September, only one in three stocks were higher for the year, yet another de ja vu 2000 all over again occurrence (most stocks entered a bear market in 1998 back then).

As far as the frothiness meter goes, the CNN Fear and Greed index hit the extreme avarice level of 78% a few weeks back. Meanwhile, the Citigroup Panic/Euphoria reached three times the euphoric threshold around the same time.

Now here comes a “fortunately”: notwithstanding the multitude of COPS in circulation presently, there is also a long list of CUPS—Crazy Under-Priced Stocks. Many of them are fine companies, truly industry leaders, not just the “cigar butt” type, in Warren Buffett’s pejorative words. Of course, they tend to be in out-of-favor sectors, those of the “Virus Victim” nature. However, some of these—such as Deere, Caterpillar and Paccar—have suddenly sprung to life and in some cases have made new all-time highs. This perhaps signals better times ahead for the other, still beaten-down, Virus Victims.

In my sequencing of the main bubbles of the last twenty-five years, the great tech mania was Bubble 1.0 and its bursting lead to Bubble 2.0, the infamous housing boom and bust. The latter almost destroyed the global financial system and led to the extreme monetary policies (zero and/or negative interest rates along with tens of trillions of central bank fabricated digital money) that have persisted ever since. As many EVA readers are aware, I wrote a virtual book on what I believe is Bubble 3.0. Clearly, David Rosenberg is with me on that but many, perhaps most, pundits disagree with us.

Let me politely beg to differ: I think they’re nuts. Perhaps the capstone of Bubble 3.0 will be the mid-September IPO of Snowflake (ticker: SNOW), another thermonuclear hot cloud software company. Despite a shockingly outrageous offering price of $120, SNOW almost instantly traded to $245, producing a market value of $88 billion. Its total sales are just a tad lower, like $617 million. Consequently, SNOW is trading for over 100 times revenues! If that’s not a shrieking bubble siren then I don’t know what even more alarming proof the see-no-mania crowd needs.

To wrap up this EVA, please allow me to quote Professor Peter Atwater from his recent brief, but most trenchant, missive, “The Coming Age of Screwtiny”. To wit:

“You see, what is ahead will be the third major betrayal in twenty years. After the dot.com debacle and the housing crisis, the crowd won’t take kindly to yet another bubble burst.

And today’s bubble is different. This time it isn’t tech or real estate*; it’s illusion. Deception has transcended the financial markets. It’s cultural and it is everywhere. From ‘influencers’ to blitzscaled start-ups, the past decade has been a Gold Rush in fakery.

The problem with it all is that other than on a magician’s stage, illusion is predatory. It is deception with intent to gain advantage and defraud. It is a zero-sum game in which the side show barkers and con men win at the expense of the crowd. And win they have. The wealth amassed by those at the center of the act has been unprecedented.

For now, with the crowd still making money, the illusion is enticing. The ten-headed lady is incredible, and the Sirens’ Song of today’s P.T. Barnum is promising an eleven-headed woman tomorrow. Step right up!”

In other words, Le Grand Casino is also Le Grand Illusion**. Or perhaps it’s Le Grand Delusion. Regardless, all those day traders now singing “Take Me Out to the Call Game” will soon simply be taken. And they’re going to want their revenge. The founders of the Robinhood trading platform and Davy Day Trader might want to get while the getting’s good.

*I’d respectfully add the word “just” in front of “tech or real estate”

**One of the greatest films ever made, in 1937, by Jean Renoir, son of Auguste Renoir.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.