“The Internet is the first thing that humanity has built that humanity doesn’t understand.”

-ERIC SCHMIDT, former CEO and Executive Chairman of Alphabet Inc. (Google)

On December 14th, 2017 the Federal Communications Commission (FCC) ruled in favor of overturning Obama-era net neutrality regulations by a vote of 3-2. While not necessarily underreported, the ruling was, in many ways, overshadowed in the financial media by two parallel events: tax reform and the Bitcoin bubble. Case in point, we have used these pages to share our view on both of these topics over the past several weeks, while completely ignoring the FCC’s landmark decision.

And yet, despite its importance, it’s easy to see why the net neutrality repeal took a back seat: it’s not a get-rich-quick scheme (à la Bitcoin), nor does it have an immediate bottom-line impact on nearly every American’s net worth (à la tax reform). But to brush the reversal aside and let the other two acts take center stage is a short-sighted approach to dealing with a momentous decision that will affect almost every American.

And, make no mistake, it will impact almost every American.

For those who are showing up late to the show or need a quick refresher on what net neutrality is, it’s basically a set of rules passed in 2015 under the Obama administration intended to protect consumers as more Americans take to the internet for communications. It also ensures media companies can sell their goods, services, and distribute information without restrictions from internet service providers (ISPs).

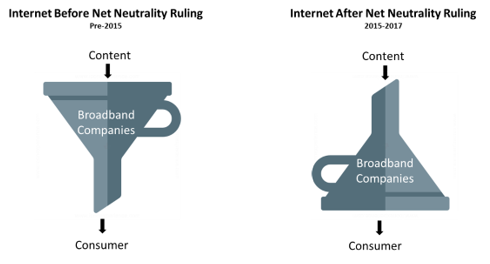

In perhaps the most simplistic terms I can think of to describe it, the purpose of these rules is to allow information to flow freely and without bias from content providers to consumers (see my crude depiction below illustrating how content could be filtered by broadband companies prior to the net neutrality ruling, and how the pipeline between content and consumers widened after the 2015 ruling).

This 2015 ruling was, in most regards, a win for consumers. So, it should come as no surprise that, leading up to the most recent December 14th, 2017 vote, the masses littered the internet with propaganda aimed at keeping these rules intact and swaying the newly appointed FCC-Chairman, Ajit Pai, away from what was an almost certain reversal (we’ll return to Ajit Pai in a minute, but for now, enjoy a few of my favorite internet memes poking fun at the very serious debate).

However, this internet-fueled campaign was in vain as Pai gathered the necessary support from a Republican-majority board to continue on his path towards destroying the rules his predecessor put in place.

At the risk of (and suggestion to avoid) getting too political, the main point here is that up until last January, Tom Wheeler, a Democrat, sat at the head of the FCC. He fought for net neutrality with support from the Obama administration under the premise that it was good for the majority of Americans. When Trump was elected, he replaced Wheeler with Pai, a Republican intent on repealing and retracting those laws and shifting the balance of power to a select few corporations.

In theory, the idea that internet service providers shouldn’t abuse their market power is hard to contest. However, where the debate gets sticky is putting these rules down on paper and determining a fixed set of standards to regulate the internet.

In a classic free market debate, the blue-blooded policy-makers are, generally, for more regulation while the red-blooded are, generally, for less oversight. This trickles into the debate around net neutrality as one side argues that the government should have no hand in dictating how internet service providers can operate, while the other side argues the opposite.

Now, no one has ever accused Evergreen of being anti-free enterprise, and we don’t want the finger-pointing to start now. But, what’s alarming about the repeal of net neutrality is the implications for American consumers and small businesses. But, before getting in to that, let’s take a look at where things have been in order to understand where they’re going.

Relegated to the Slow Lane

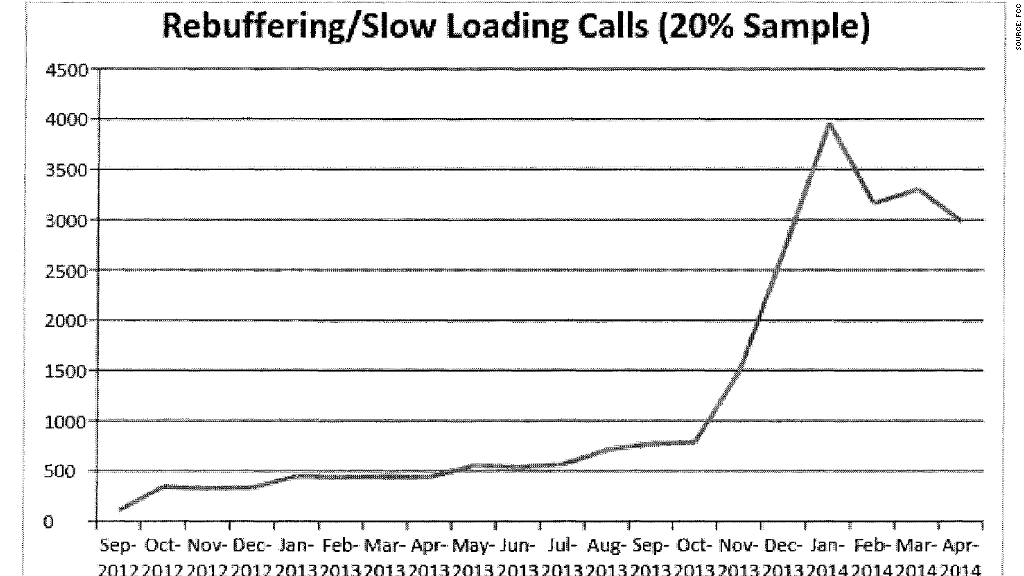

In February 2014, Netflix reluctantly paid Comcast to gain direct access to its network. The reason for doing so was that Comcast had been intentionally reducing speeds for consumers trying to access the streaming-service (which led to an ungodly rise in customer service complaints between September 2012 and January 2014, as shown below).

Source: CNN

Source: CNN

In fact, in a petition filed to the FCC in August 2014, Netflix stated that, “For many subscribers, the bit rate was so poor that Netflix streaming video service became unusable. Some [subscribers] canceled their Netflix subscription on the spot, citing the unacceptable quality of Netflix’s video streams and Netflix’s inability to do anything to change the situation.”

But the ISP-inflicted pain didn’t end there. After its February agreement with Comcast, Netflix entered into comparable agreements with AT&T, Verizon, and Time Warner Cable to avoid a similar fate.

The trickle-down was that Netflix was forced to raise their streaming plan prices for new customers from $7.99/month to $9.99/month in May 2014.

Not only did existing Netflix subscribers experience unbearable poor streaming quality for a period of time, but new customers that were not grandfathered in under the legacy pricing model had to a pay premium rate.

Yikes.

This example typifies the power struggle that existed between internet service providers, content providers and consumers prior to 2015. As a result of net neutrality rules, such blatant commercial strong-arming became illegal, and allowed content providers and consumers to take a deep breath and operate in a “free and fair” internet universe – at least for a couple of years.

However, with the recent repeal of net neutrality, many are concerned that ISPs will again be able to play traffic cop, giving preferential treatment to certain content providers while punishing others.

Shifting the Balance of Power

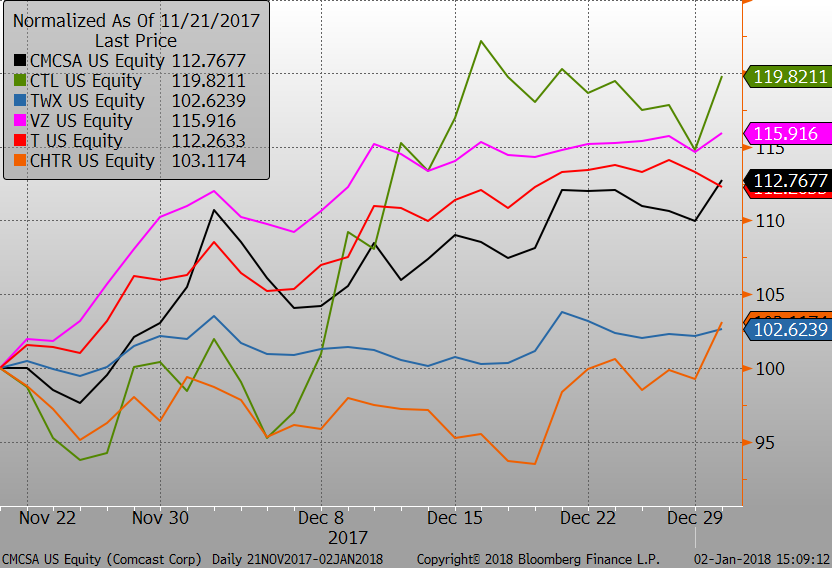

The clear and obvious winners from December’s ruling are internet service providers (companies such as Comcast, AT&T, Charter, Verizon, Time Warner Cable, CenturyLink). Since Pai announced that the FCC would move to vote on net neutrality repeal on November 21, 2017, many of these stocks have performed decently well.

Source: Evergreen Gavekal, Bloomberg; Comcast (CMCSA), CTL (CenturyLink), TWX (Time Warner), VZ (Verizon), T (AT&T), CHTR (Charter Communications)

Source: Evergreen Gavekal, Bloomberg; Comcast (CMCSA), CTL (CenturyLink), TWX (Time Warner), VZ (Verizon), T (AT&T), CHTR (Charter Communications)

Not-as-obvious winners from net neutrality repeal are large content providers including Netflix, Google, Facebook, and Amazon (yes, the very same companies that will be paying more to ensure their customers have fair access to content). While some of these companies, like Netflix and Google, opposed the repeal, the reality is that theses behemoths have the money and leverage to negotiate advantageous deals that will allow their customers to ride the internet autobahn at faster speeds than shallow-pocket competitors.

Conversely, small businesses and start-ups will be most negatively impacted by the repeal. The main reason is that these companies will face increased costs associated with ensuring their traffic reaches consumers at reasonable speeds. Tech startups such as Etsy, Airbnb, and Foursquare all opposed the repeal, fearing larger competitors would be able to pay for preferential treatment to operate in internet fast lanes.

A Daily Dose of Salt

As Evergreen’s CIO, David Hay, likes to say: it’s shaker grain of salt time. The repeal that was announced on December 14th just reached its final form yesterday. Shortly, the rules will be entered into the federal register, at which point they will both come into effect and come under almost certain legal opposition. The next steps will likely be hearings, lawsuits, attempts by states to establish their own rules, and attempts by Congress to keep net neutrality alive. If successful, these attempts could change the course of the repeal.

Whatever your stance – or depth of knowledge – is on net neutrality, the undeniable reality is that this is a very important topic worth keeping at the top of your newsfeed. The implications for internet service providers, large content providers, small businesses, start-ups, and consumers are significant and should not be ignored because, make no mistake...

The ultimate outcome will impact almost every American.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.