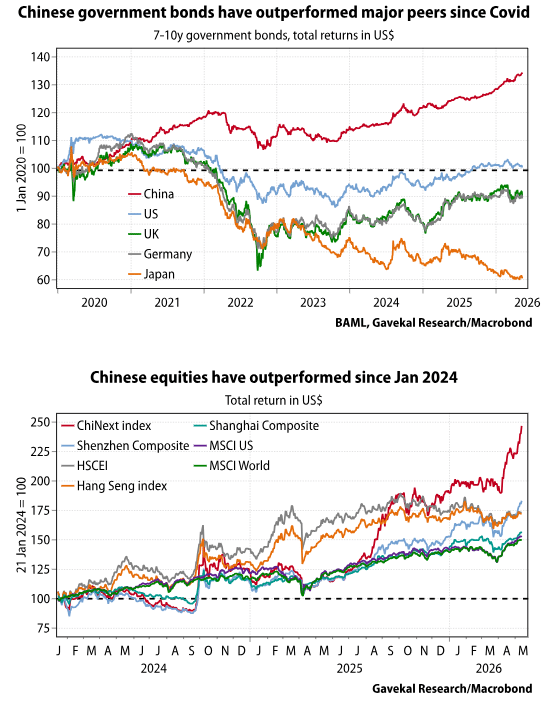

Our contention in January 2024 was that the Chinese government’s intervention in the stock market was a watershed moment. Up until then, Beijing had seemed far more focused on ensuring the outperformance of the Chinese government bond market, which we had interpreted as a guarantee of CGB outperformance. That said, the policy shift toward equity markets has thus far not been detrimental to total returns on Chinese government bonds.

So, in January 2024 the Chinese government stepped into equity markets and actively bought a cross section of Chinese equities. Since then, Chinese equity market performance has been quite disparate. The Shanghai Composite index has essentially performed in line with US and global equities.

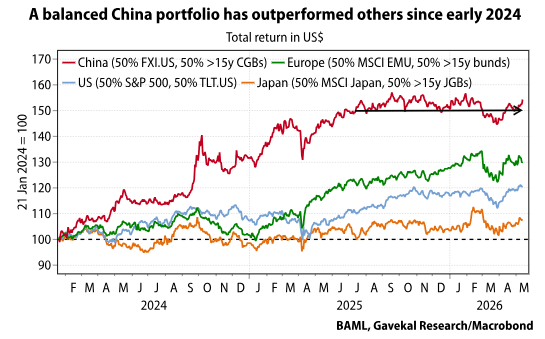

This joint performance of Chinese equity and bond markets is helping mend the damage caused by the real estate bust on corporate, and individual, balance sheets. Nonetheless returns have essentially plateaued over the past 12 months. This is disappointing.

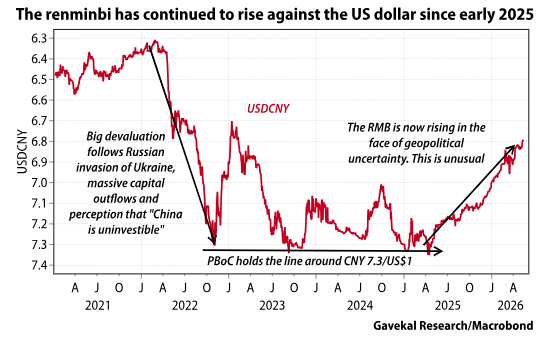

One positive tailwind for both Chinese bonds and equities is the unfolding shift in China’s exchange rate policy. Since early 2025, the renminbi has risen against the US dollar, and most other major currencies, almost every month. This is an interesting development, especially in the face of the Iran war. In the past, the default mode for renminbi management was to freeze the value of the currency at times of global uncertainty. But not today. Instead, the renminbi continues to grind higher.

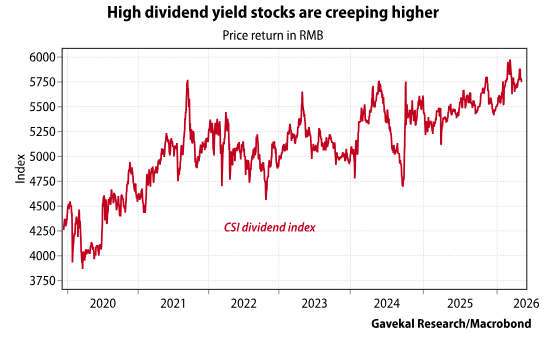

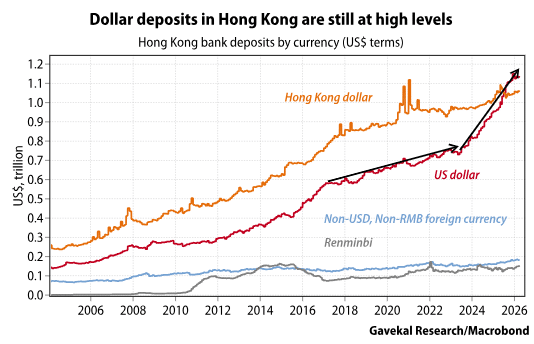

This shift in the renminbi trend, combined with the drop in US short rates, led us to believe that Chinese savings would stop being funneled into US dollar bank deposits, and would instead have no alternative but to look for domestic yield. In reality, this has yet to happen. Sure, high-dividend-yield-paying stocks have continued to do well, but they have not done so at an accelerating pace.

For now, it seems that Chinese money may have stopped flowing into US dollar deposits. At the same time, money previously deployed in US dollars has yet to leave. At least, that is what US dollar bank deposits in Hong Kong would seem to indicate.

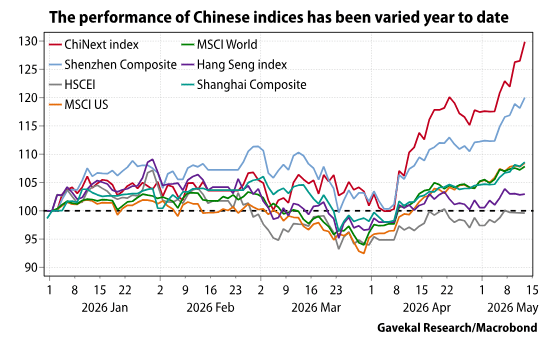

All of which brings us to the year-to-date performance of Chinese equities and the impressive divergences across the various Chinese equity markets (see chart below). Since the start of the year, the higher-yielding H-share index and Hang Seng index have underperformed, while ChiNext, China’s “growth market,” which de facto offers very little yield, has been on fire. The Shenzhen Composite index, which is also a low-yielding index, has performed handsomely as well. Finally, Shanghai’s performance has essentially tracked that of global and US equities.

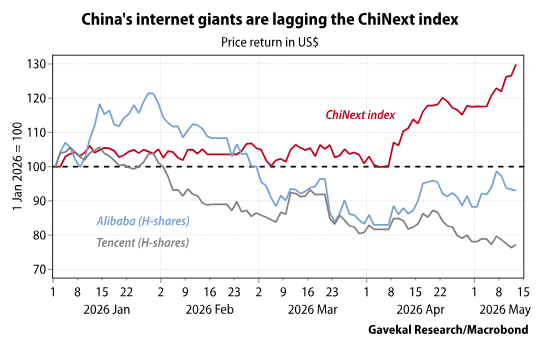

Behind the divergent performances of Chinese indices lies a phenomenon investors in Western equity markets will recognize. Essentially, anything linked to the rollout of artificial intelligence capital spending and semiconductors has ripped higher. Meanwhile, the rest has broadly languished. And, as it turns out, tech hardware companies make up a bigger share of the ChiNext and Shenzhen indices than of the Shanghai or Hong Kong benchmarks. The relative performance of Alibaba and Tencent to ChiNext is a good example. It suddenly feels as if China’s big tech companies are becoming a funding source for the newer, more exciting, more AI-related, names.

This Chinese divergence between hardware names on the one hand and software/web platform names on the other is eerily reminiscent of what has been unfolding in US markets. With one key difference: in the US, hardware names are a bigger part of the main indices (semiconductor names are now 18% of the S&P 500), so the outperformance of hardware is having a bigger impact on broader benchmarks.

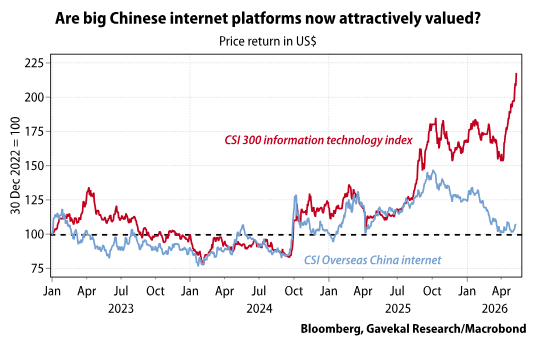

The underperformance of Alibaba, and especially of Tencent, possibly adds a further “psychological” element to recent Chinese equity market performance in that, for most foreign investors, BABA and Tencent essentially “are” the Chinese equity market. Or at the very least, these two companies are the usual proxies through which foreign investors tend to judge the progress, or lack thereof, of Chinese equity markets. This might not be fair, but there it is anyway! Foreign investors will only rarely talk about the impressive performance of Cambricon, CATL, Wasion and other hardware names. Instead, because Tencent and Alibaba have struggled this year, the default assumption seems to be that the Chinese equity bull market is over.

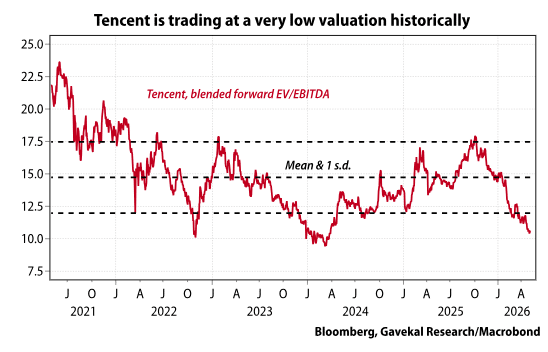

This focus on Tencent and Alibaba probably makes sense to the extent that both companies are now trading close to their valuation lows. Tencent is currently trading at roughly 10.5x EV/EBITDA and 12x cash flows. This valuation is roughly a third, or one-and-a-half standard deviations, below Tencent’s average of the past decade.

The same is roughly true for Alibaba (though the valuation discounts relative to BABA’s own history do not seem quite as extreme) and most of the other tech platform names, including Baidu, Meituan, JD and Pinduoduo. So with valuations for the tech names (that foreign investors have historically loved to own) now back to their lows (see chart below), foreign investors feel entitled to question the notion that China is in a bull market. After all, in a bull market, multiples should expand, not contract!

So having formed a nice base, are the major Chinese internet platforms now a buy? Or will they remain dead money? In an environment in which the excitement seems to be all about AI, all the time, the initial gut reaction has to be that the big tech platforms will remain dead money. However, this may be too simplistic. To begin with, some of the large tech platforms, including Alibaba and Baidu, do offer AI solutions of their own and, at some point, these may get the market excited. Second, the market may have been all about AI over the past six months, but who is to say whether this AI excitement will continue over the medium to long term? Finally, and perhaps most importantly, the fact that the valuations of the big tech platforms are back to their lows may well put pressure on the Chinese government, and on the management of these businesses, to do more to organize a meaningful rally. This could come through the encouragement of buy-backs, an increase in dividend payouts, or a less restrictive regulatory environment.

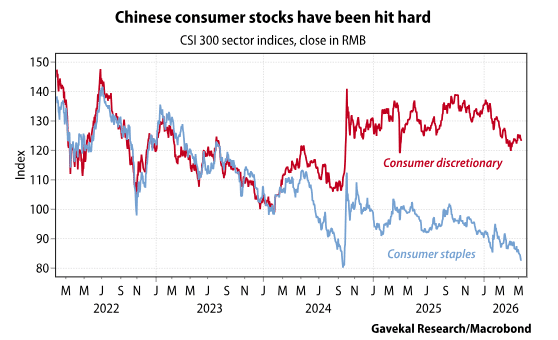

Aside from the tech platforms, other underperformers in Chinese equity markets have been consumer-related names. Both discretionary and staples have been massive disappointments (see chart below). The staples index, weighed down by the spirits sub-sector and the underperformance of names like Kweichow Moutai—itself a primary victim of the anti-corruption drive, is again flirting with decade lows. Meanwhile, consumer discretionary stocks have essentially flatlined over the past 18 months.

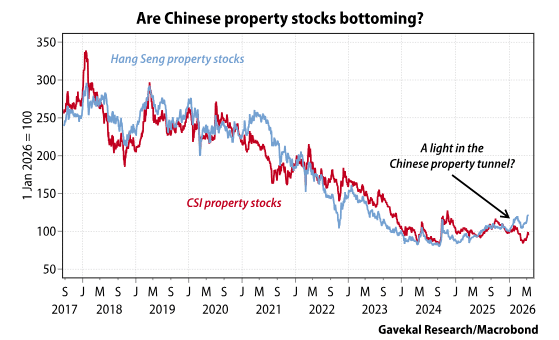

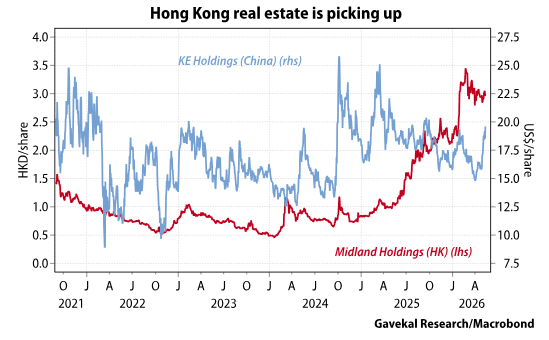

The same is true of Chinese real estate stocks. With underlying real estate prices and transaction volumes falling, real estate stocks have unsurprisingly been dogs with fleas. However, in tier-one cities, real estate prices now seem to be stabilizing and transactions have lately been picking up. Will that prove enough to trigger a rebound in the very beaten-up shares of Chinese property developers? Interestingly, so far this year, the shares of Hong Kong-listed property developers have gained 20% while their Chinese counterparts have shed -3.5%, though these suddenly seem to be coming alive.

The Hong Kong real estate market started to bottom a year ago, with rental yields and transaction numbers picking up. One of the signs that the Hong Kong real estate market was bottoming was the sharp re-valuation of the biggest listed Hong Kong real estate broker, Midland Holdings. In that regard, the fact that KE Holdings, one of the larger listed Chinese real estate brokers, is no longer collapsing is perhaps encouraging.

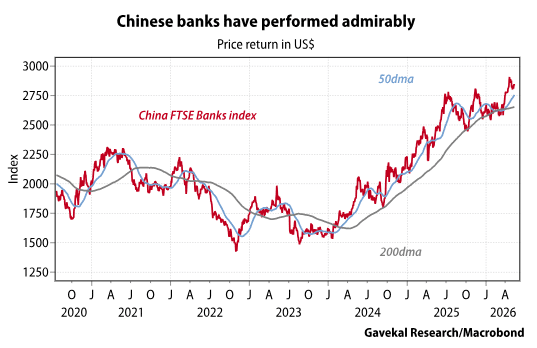

Aside from tech, the positive side of the ledger has also been dominated by banks. For most managers, this is a double-edged sword. On the one hand, the outperformance of bank stocks, especially as interest rates fall, is a rather bullish sign for the economy and the broader markets (see chart below). At the very least, it is far better than a shocking underperformance of banks, for this tends to set off alarm bells! On the other hand, most active managers tend to be structurally underweight banks since Chinese banks, through the cycle, end up being instruments of Chinese policy. The mantra on Chinese banks tends to be that one can rent them, but never own them.

Today, the big question surrounding the banks is whether the anti-involution campaign launched by Xi Jinping roughly a year ago will prove to be a net positive. Conceptually, the anti-involution campaign should mean that banks no longer have to lend good money after bad to the champions of every local authority, which sounds great. On the flip side, the anti-involution campaign should also mean that companies unable to raise their prices and generate genuine margins will go out of business. That would leave banks with yet more bad loans to clean up at a time when balance sheets are still digesting the impact of the real estate bust.

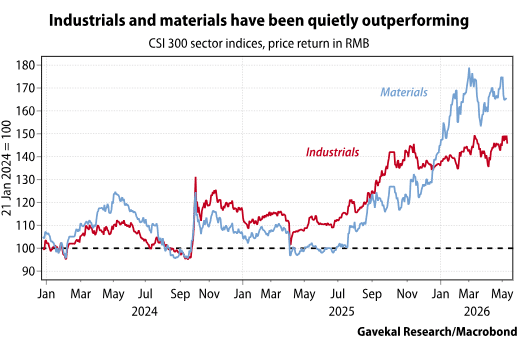

Finally, aside from the tech hardware stocks and the banks, the other shining lights in Chinese equity markets have been the materials and industrial sectors. To a large extent, these have been the sectors that have benefited the most from the policy shift toward making the Chinese economy more resilient and less dependent on foreign inputs.

It is also in these sectors that we are increasingly seeing the emergence of genuinely world-class companies. Indeed, for years it seemed that the main job of Chinese companies was to produce inferior products at lower prices than those produced in Japan, South Korea, the US or Europe. Needless to say, it is hard to get investors fired up about paying big valuation premiums for companies that produce lower-quality goods, especially if the process also involves destroying everyone’s margins.

Just as importantly, materials and industrials should also be the two sectors that benefit the most from the anti-involution campaign, assuming the Chinese government means what it says and says what it means when it comes to industrial overcapacity.

Investors are having to digest a number of very important shifts right now. Specifically:

So what do all of these shifts mean for the various segments of the Chinese equity market?

In conclusion, the Chinese equity landscape is constantly evolving. And as things stand, the market continues to offer a number of attractive opportunities. Momentum investors can focus on AI, tech hardware, industrials and materials. Carry investors can look to high-dividend-yielding stocks and banks. Meanwhile, mean-reversion investors may find value in internet names, real estate stocks and consumer names.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.