“The Fed won’t admit this, but it looks and smells an awful lot like the monetary authority is financing the fiscal authority.”

–Mark Cabana, Strategist at Bank of America Merrill Lynch

“Monetary Policy has released a pernicious attack on prudence and financial discipline by those who save.”

–Bob Rodriguez, Former CEO of First Pacific Advisors

______________________________________________________________________________________________________

THE COST OF BEING NORMAL

By Jonathan Fulcher

Throughout 2015 and all the way into 2018 the Fed was a bit obsessed with being “normal”. They wanted a “normal” interest rate (justifying rate hikes) and they wanted a “normal” balance sheet (justifying a reduction in that balance sheet). Being “normal” seemed like a noble goal, and it basically stood for the unwinding of unconventional policy that was only ever supposed to provide temporary support. They were even somewhat successful in implementing rate hikes and a very transparent program to reduce the size of their bloated balance sheet.

Unfortunately, that quest for “normalization” appears to have come full circle and now looks to be in full reversal. The reversal began with ending Quantitative Tightening (the reduction of the amount of securities held on their balance sheet, or QT), then cutting interest rates, then intervening into financial markets due to liquidity issues, and finally will lead us back to square one…balance sheet expansion. Being normal isn’t all its cracked up to be anyway…

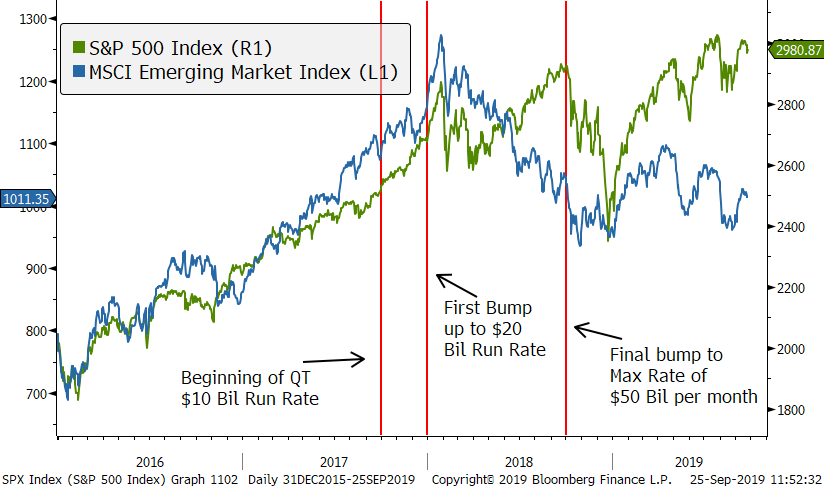

It may be helpful to look back at the very beginning of Quantitative Tightening, which officially began in October of 2017 when the dollar amount of assets on the Fed’s balance sheet stood at nearly $4.5 Trillion. The tightening started slowly at first, with just a $10 billion reduction per month for the first three months; but the program then called for an additional $10 billion (for a total of $20 billion per month) starting one quarter later in January of 2018. This was upped again each quarter until the monthly runoff hit $50 billion. This final run rate became reality starting in the 4th quarter of 2018. But what effect has this had on financial markets? Here is where it gets truly interesting.

The following graph is probably quite familiar, as many commentators have equated the expanded balance sheet at the Fed (and the subsequent excess liquidity and easy money) to a rise in the US Stock Market. As soon as the end of QE3 halted the expansion of the Fed’s balance sheet, the S&P 500 also stopped expanding. Correlation does not necessarily mean causation and ultimately the market was able to break out of its malaise due to some timely stimulus from China and a renewed spurt of global growth that took hold in 2016.

Source: Bloomberg, Evergreen Gavekal

Once that growth found stable footing, the Fed began their quest. Normalization was the goal and raising interest rates was only the beginning. Following the first interest rate rise in over a decade, the Fed announced QT in 2017 and, in what seemed like a major win, the market shrugged it off (unlike, say, the Taper Tantrum reaction back in the summer of 2013). At the beginning, it seemed this whole QT thing would be no big deal and plus, the entire market was being re-rated due to the forthcoming tax law change that reduced corporate tax rates, and the global economy was only beginning to enter a synchronized global expansion (or so it was believed). This led to an almighty blow-off in January of 2018 when expectations ran hot, just as the additional installment of QT began to bite.

Source: Bloomberg, Evergreen Gavekal

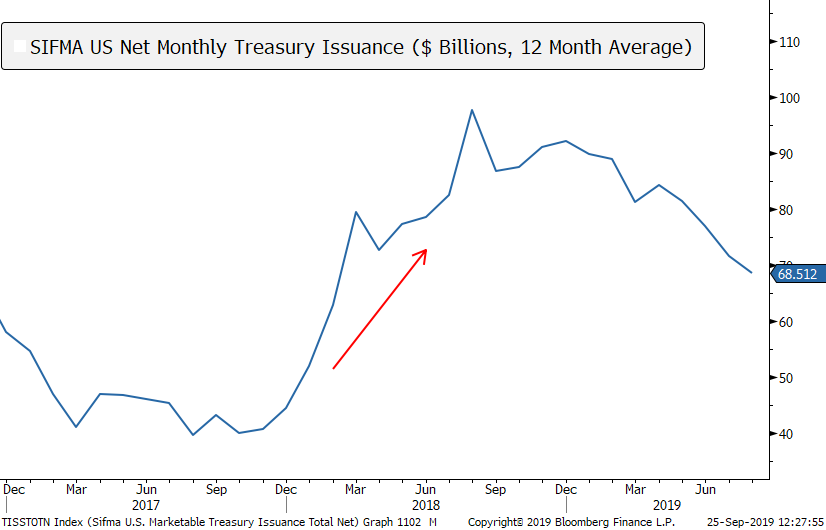

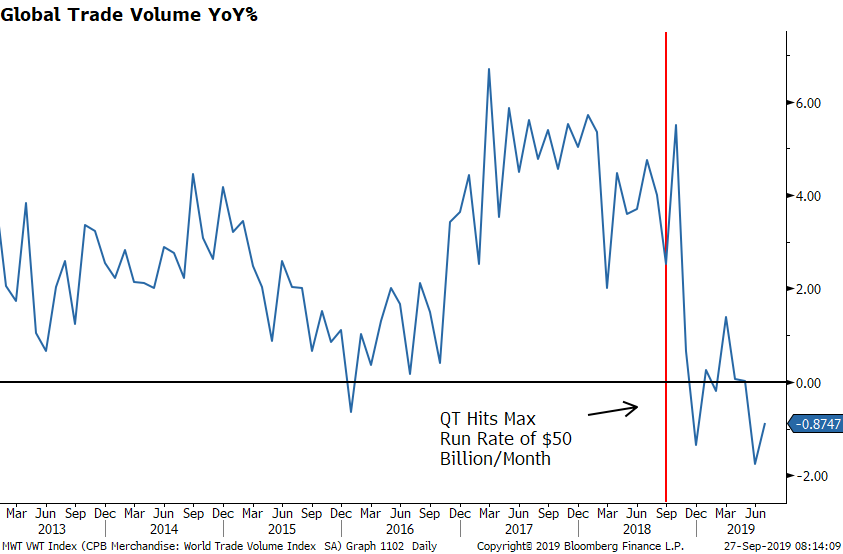

Financial markets had become accustomed to liquidity (make that addicted) and the Fed was finally taking away the punch bowl. Effectively, they were decreasing liquidity within the US Dollar system and the first market to really feel the heat was Emerging Markets, which have yet to recover. In fact, in June of 2018 the Governor of the Reserve Bank of India, Urjit Patel, made headlines with an article in the Financial Times imploring the Fed to readjust their normalization plan as liquidity conditions outside the US were in turmoil. Argentina and Turkey became shining examples of the exact trouble Mr. Patel highlighted and put the consequences of tightening liquidity on full display. He was also early to identify the other culprit, US Treasury Debt Issuance.

Source: Bloomberg, Evergreen Gavekal

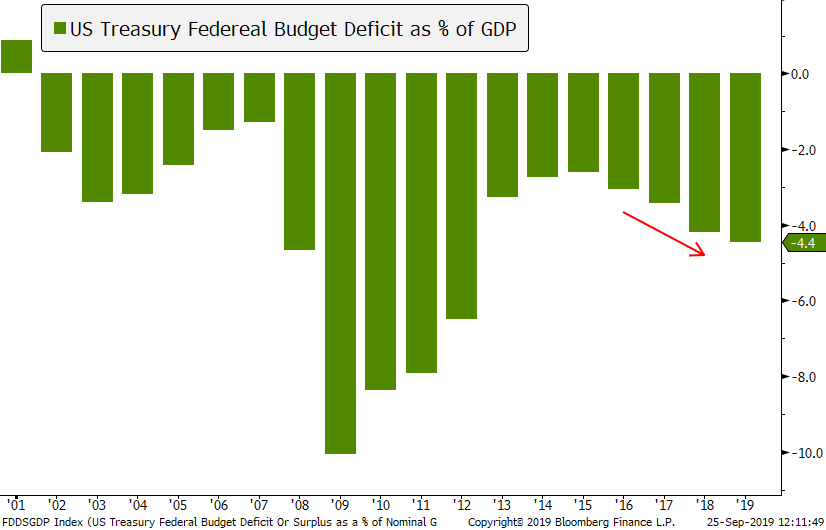

Along with the tax law change from late 2017 (which lowered tax revenue for the Treasury), the US government also saw an explosion in spending, and this shortfall needed financing.

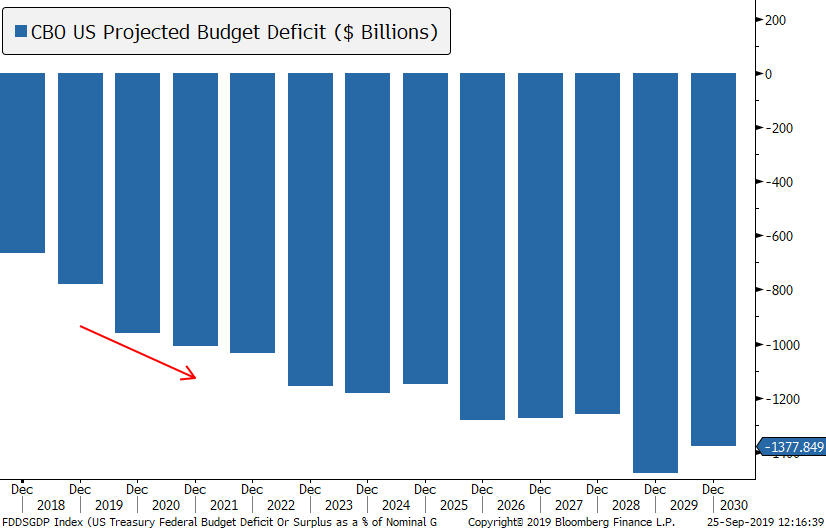

The answer turned out to be an increase in the US deficit and increase in the issuance of US treasuries. This added “demand” for capital, alongside the market’s largest buyer actively reducing their “supply” of capital, served to affect a “double whammy for global markets” as Mr. Patel put it. As you can see from the Congressional Budget Office (CBO) projected deficit chart above, this issuance is not expected to go away anytime soon. In fact, including the estimate for this month’s issuance, the Treasury expects to have borrowed an additional $433 billion from the market in Q3 2019. That’s an annual pace of well over $1.5 Trillion!

Ultimately, that last jump into the final tranche of QT at the end of September 2018 (which occurred alongside yet another interest rate increase) combined with the surge in issuance from the US Treasury hit some sort of threshold.

It took a few months to fully realize the damage, and the Fed even raised rates once more in December of 2018 in what is now largely seen as a bit of a mistake from which Powell began backtracking almost immediately. By March of this year, the Fed announced a grand plan to halt Quantitative Tightening sooner than many in the market had originally anticipated (slated for September 2019), and with a much larger ending amount of T-bonds on the balance sheet (which was a quick reversal given investors were told the balance sheet reduction was on “auto pilot” as recently as December). Still, the Fed has insisted that the real US economy has been functioning just fine, even firing on all cylinders. In fact, according to the NFIB Small Business Economic Trends Survey for August of 2019, just 4% of business owners reported that they did not have access to cheap and abundant capital, right about at the historic low. Life seems to be good for a small business in the US.

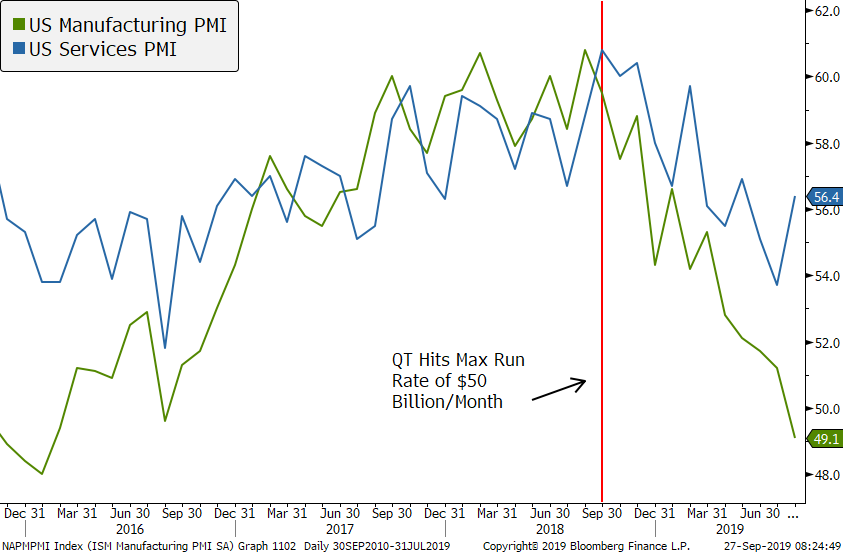

Finally, at the end of July, the Fed surprised the market with news that Quantitative Tightening would end effective immediately, which seemed an odd announcement given the program was already set to end just two months later. This was paired with the first interest rate cut since December of 2008, which bodes the question: if the small business community is doing just fine, what is going on? Maybe Mr. Powell is finally listening to the likes of Mr. Patel, or maybe he is reading the tea leaves (like those in the charts below) and is attempting to head off further deterioration. His comments on “mid-cycle adjustment” would suggest the latter. Politics may have played a part (yikes, we hope not) and it certainly seems he felt pressure from financial markets to do its bidding. Regardless, something clearly broke during that final push into full blown QT.

Source: Bloomberg, Evergreen Gavekal

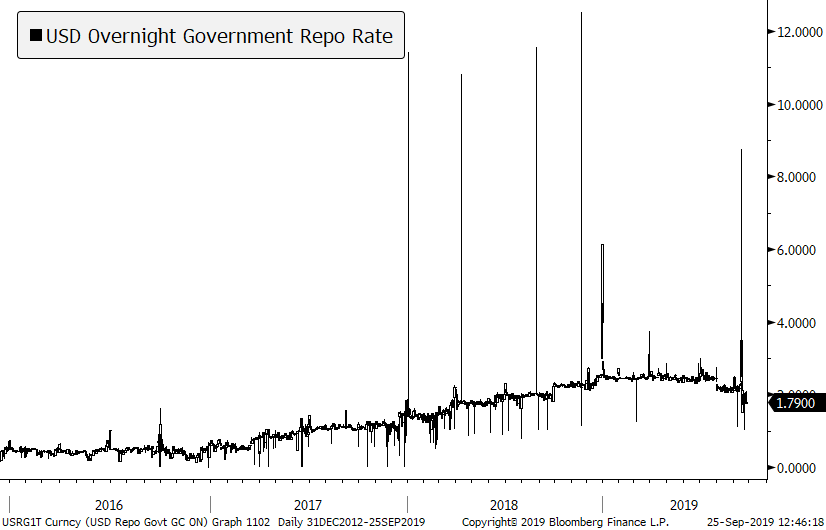

A potential answer came to us early last week as the Repurchase Agreement (Repo) market suddenly became headline news for the first time since 2008. The Repo market is an overnight lending market where large pools of money earn an overnight interest rate by lending their cash to those who need it. It’s basically the plumbing for financial markets and the rate tends to follow the Fed Funds rate. However, this time it got a bit out of control.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

But what is really fascinating, is that this is not the first time. In fact, this has occurred at least 5 other times in the past year-and-a-half which is, coincidentally, the same time frame we’ve been discussing (i.e. the “QT Era”).

You might ask yourself: Has this happened prior to that? No, not really. So, maybe we should have seen this coming? Well…sort of. The difference this time is that the issue didn’t immediately go away and forced the Fed to actually step in over the course of multiple days and provide a direct injection of liquidity to the Repo market.

To vastly oversimplify, it appears that this Repo turmoil was caused by a lack of liquidity, fueled by an unfortunately timed corporate tax payment (the first liquidity drain) paired with a big week for treasury issuance (the second liquidity drain). Basically, lots of securities entered the system demanding capital and the capital simply wasn’t there. In official terms, the level of excess reserves in the banking system have been deemed too low and that is a direct result of the Fed’s tightening program.

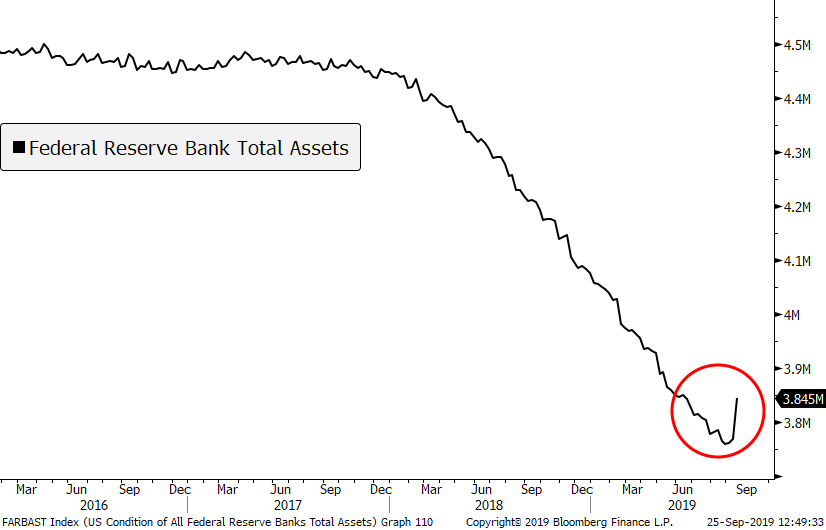

And here is the rub. Our system has now grown up around the Fed’s unconventional “temporary” policies and we are unable to back away from them. The Fed halted the roll off of the balance sheet because the system can’t handle a further liquidity drain. In fact, Chairman Powell slipped in the words “return to organic growth” when discussing the balance sheet at last week’s announcement. But the crazy part is…they’ve already begun.

Source: Bloomberg, Evergreen Gavekal

In just one week, the Fed has undone 3 months of monetary shrinkage. This clearly paves the way for balance sheet expansion from here. Do we expect QE-lite or even QE4? Maybe more toward the “lite” version in the near term but on this topic, a former senior Fed official whom our team spoke to last week stated that it would be no problem for the Fed’s balance sheet to expand to $7 trillion. Now that’s some financial intervention!

It has always been assumed that the Fed would step back in with their balance sheet and now there is a clear path towards that outcome, and markets may even approve. The problem is, between the tightening and the ongoing issues regarding trade wars and general uncertainty, they may have already broken this expansion cycle. Those data points above continue to deteriorate while Europe finds itself even further along the road to contraction. The surprising bit in all this is that the US Stock Market remains within spitting distance of an all-time high…

There are a couple of questions with fuzzy answers that come out of this exercise.

1. Are interest rates an effective tool for the Fed these days?

It is difficult to say yes given they essentially lost control of the overnight interest rate in the Repo Market last week. That and there really isn’t a business with even a faint pulse that is unable get a hold of cheap capital these days despite a rising or falling Fed Funds Rate (though that may be a different story if those rates were in the 5% range).

2. Is the new “normal” monetary tool going to be the Fed’s Balance Sheet?

My guess is this has become more important than many realize. We now have a Fed that will act to provide increased liquidity (larger balance sheet) at any sign of stress and a Treasury that is issuing ever larger quantities to fund fiscal spending, which is causing the very liquidity squeeze that the Fed is responding to. That’s a nasty circle that looks eerily like Modern Monetary Theory (MMT). If the Executive Branch of the US Government was looking for a way to force the hand of the Fed, it appears they have figured it out.

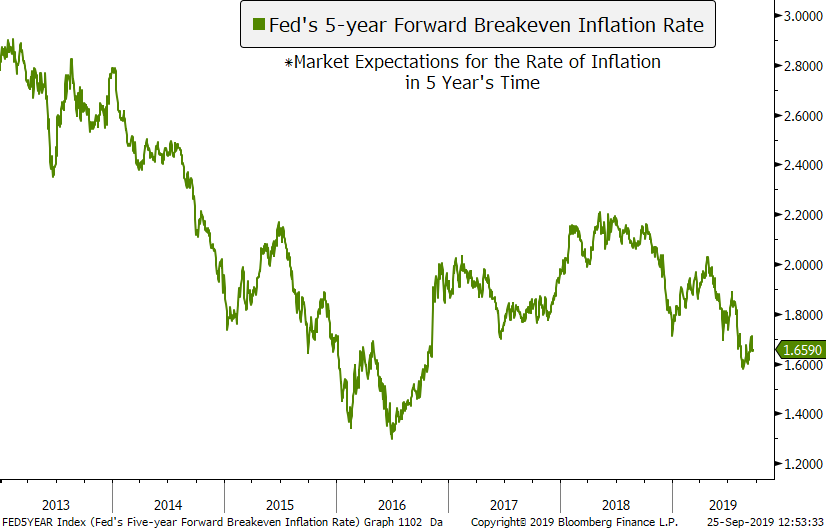

One final thought given that conclusion. The fears over past balance sheet expansion circled around worries about inflation spiraling out of control. That never occurred as those excess reserves simply sat on banks’ balance sheets at the Federal Reserve and were never circulated. So, what happens if those excess reserves are effectively spent by the Treasury/US Government? The market is certainly not expecting that outcome…

Source: Bloomberg, Evergreen Gavekal

Jonathan Fulcher

Senior Analyst

To contact Jonathan, email:

jfulcher@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.