“Oil changed the world in the 1900s. It drove cars, it drove the whole chemical industry…I look at data as the new oil.”

–BRIAN KRZANICH, Former CEO of Intel

One of the reasons for the proliferation of technological innovation within the United States over the last several decades is due to its “lighter touch” on regulation when compared to global counterparts. Even when comparing the tech industry to other industries within the United States, the technology sector is the least regulated industry with just 27,000 federal laws verses 128,000 for the financial sector and 215,000 for manufacturing.

Source: BofAML Global Investment Strategy

Source: BofAML Global Investment Strategy

But, as one of the most hotly debated topics of 2018 - and there were a lot of those this year - the power and influence of the tech industry came under a microscope, epitomized by Mark Zuckerberg’s very public testimony before Congress on Facebook’s consumer data scandal. The question that policy makers and the general public face today is how much regulation is necessary to protect the data and privacy of consumers, while allowing US-based tech firms the latitude to continue to innovate and maintain global leadership in the sector.

Despite the increased scrutiny on this topic in Washington over the past couple of years, neither Congress nor the Trump administration have acted on momentum to implement reform in the tech industry at the federal level… yet.

A fiery mid-term election season just wrapped up, and with its conclusion came a shift in the balance of power within the legislative branch of government. What’s particularly intriguing about this cycle’s result is the impact it could have on the future of tech regulation in America.

Lessons from Europe and California

On May 25, 2018, Europe’s General Data Protection Regulation (GDPR) went into effect. Basically, the law requires businesses operating (either physically or virtually) in the European Union (EU) to ensure its processing of personal data be designed and built with safeguards to protect that data. It requires that businesses use the highest-possible privacy settings by default, so that data is not available publicly without explicit, informed consent, and cannot be used to identify a subject without additional information stored separately.

The impact of this law on businesses operating in Europe has been significant and has disrupted the balance between regulation and innovation, making it harder for start-ups and established businesses to launch or grow. Having consulted for a large software company that partners with many companies doing business in the EU, I can attest to this disruption first-hand. Forbes recently brought the wide-ranging implications of this new law to light, reporting:

“The head of a small company that does online consulting and training for Microsoft’s SQL Server wrote regretfully about how all of GDPR’s hoops are “just not worth the hassle.” The owners of the Chicago Tribune and the Los Angeles Times decided to deny European readers access to the papers’ websites. Others that either temporarily or permanently blocked European visitors due to GDPR include A&E Networks, History.com news-link aggregator Instapaper, and, ironically, Unroll.Me, a service that helps users unsubscribe from unwanted emails.”

And the wave of regulation that began in Europe with GDPR has crossed the pond and made its way West. In the United States, California, which has been a cradle for innovation and has minted more tech billionaires than anywhere else in the world, passed a measure last summer called the California Consumer Privacy Act (which has been nicknamed the “American GDPR”).

In a similar vein to its European counterpart, the California Consumer Privacy Act grants a consumer “the right to request a business to disclose the categories and specific pieces of personal information that it collects about the consumer, the categories of sources from which that information is collected, the business purposes for collecting or selling the information, and the categories of 3rd parties with which the information is shared.”

Unfortunately for California – and more specifically the Valley – the progressively unfavorable environment for enterprises is beginning to take a toll, as more people and companies are now leaving Silicon Valley than arriving. And, on a national level, efforts from the Federal Trade Commission (FTC) to hold a series of hearings on Competition and Consumer Protection in the 21st century have been underway since September, examining whether changes in tech might require adjustments to consumer protection laws.

What’s particularly concerning – at least for US tech firms – is that if policies similar to GDPR or the California Consumer Privacy Act are enacted at the federal level, companies and talent could make a similar exodus out of the United States to more regulatory-friendly countries.

What Goes Up, Must Come Down

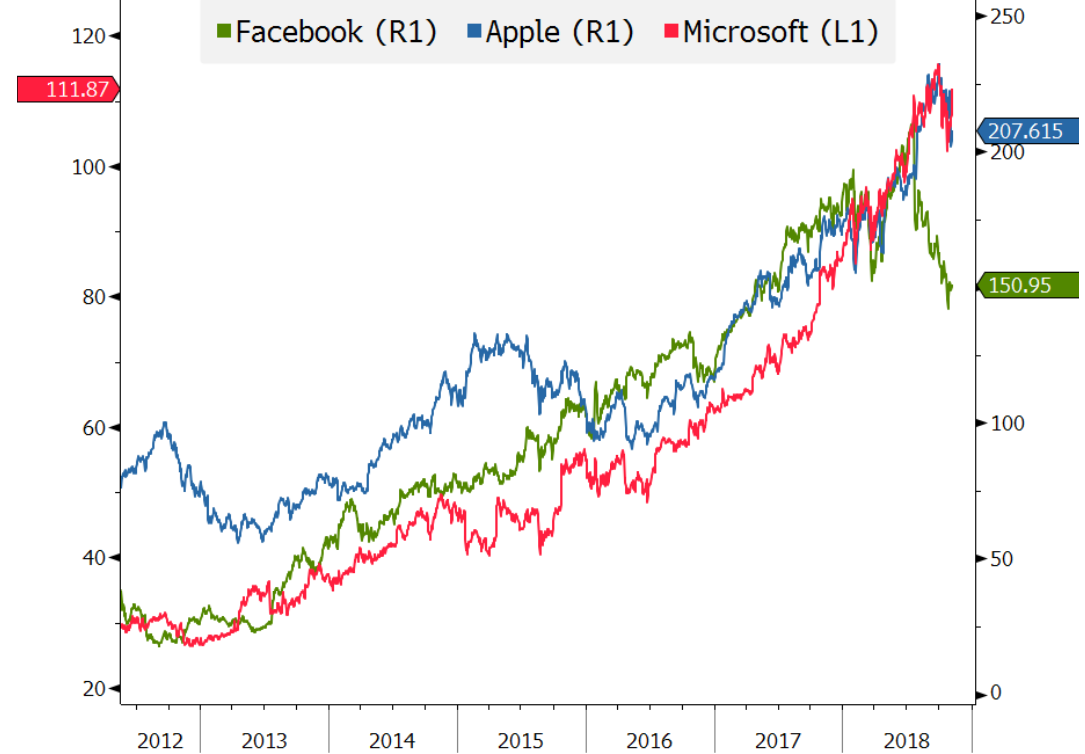

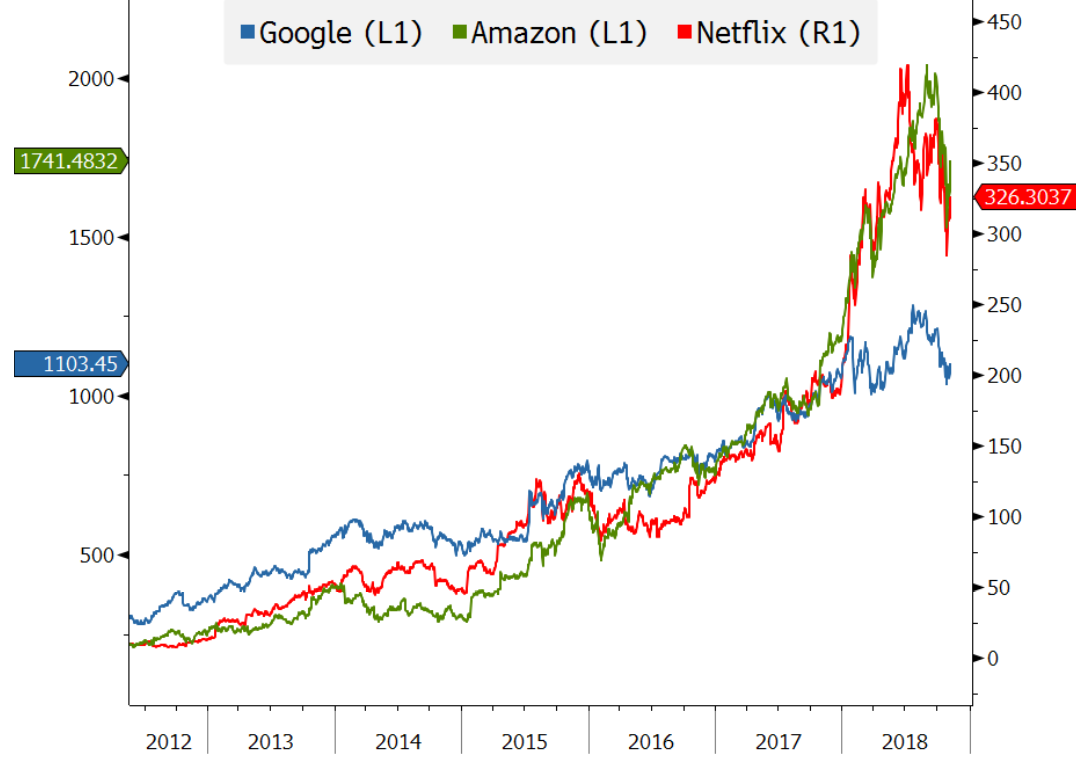

For those that have been fortunate enough to ride the tech-wave over the past several years, it’s been quite a spectacular ride. FAANGM stocks (Facebook, Apple, Amazon, Netflix, Google and Microsoft) have led an impressive charge, generating a 760.7% total return since May 17, 2012 (Facebook’s IPO date).

FAANGM STOCKS - TOTAL RETURN

Source: Bloomberg, Evergreen Gavekal (as of 11/7/18)

Source: Bloomberg, Evergreen Gavekal (as of 11/7/18)

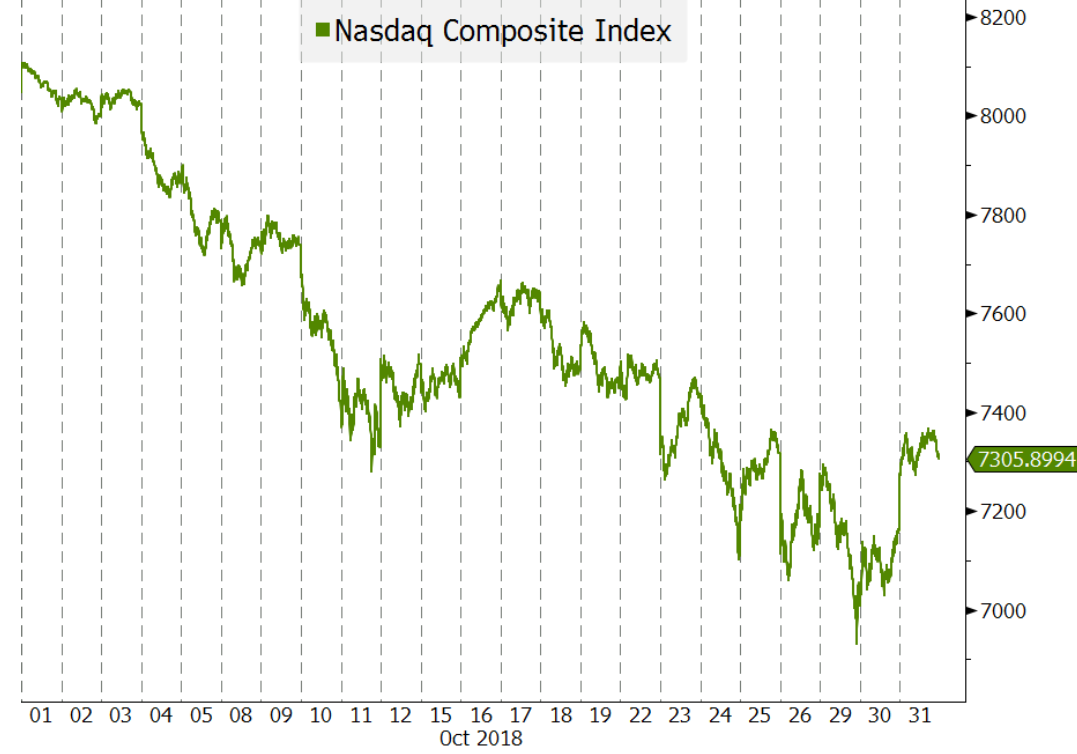

Although, recently, tech stocks were briefly humbled, as the Nasdaq closed down -9.16% in the month of October.

NASDAQ PERFORMANCE OCTOBER 2018

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

While increasingly lofty valuations reminiscent of the dotcom bubble fueled October’s back-to-earth moment, the prospect of an increased regulatory environment could bode even more troublesome for tech stocks in the not-too-distant future.

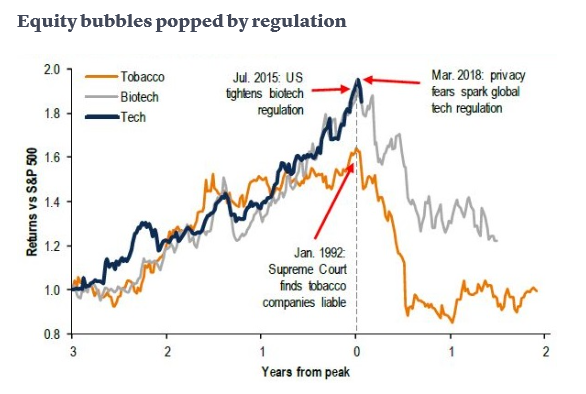

When comparing the potential impact of tech regulation to regulatory moments in other industries, Michael Hartnett, chief investment strategist at Bank of America, recently said, “Tobacco (1992), financial (2010), and biotech (2015) industries illustrate how waves of regulation can lead to investment underperformance.” And, as the chart below shows, the ride down can happen fairly quickly once regulations take hold.

Source: BofAML Global Investment Strategy

Source: BofAML Global Investment Strategy

The Bottom Line

If the federal government broadly increases regulations in the tech industry, the “self-policing” environment that US tech firms have grown accustomed to for decades could end abruptly. Mixed with sky-high valuations, increased regulatory pressures would bode poorly for an industry that has outperformed just about everything over the last 6 years.

The extent that regulations impact innovation, stock performance or US leadership in the sector likely depends on the degree to which the laws disrupt business. While the magnitude of policies such as the GDPR and California Consumer Privacy Act are unlikely at a federal level under the watch of this administration, the undeniable fact is that pressure has and will continue to mount to ensure consumer data is safeguarded. What might be good for the data-consuming citizenry (isn’t that almost all of us?) could be anything but for those who are heavily exposed to the one market segment that has kept rising as nearly every other sector has been pounded. The cold, hard reality is that all good things come to an end eventually. Caveat tech emptor.

Michael Johnston

Tech Contributor

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE *

* Some EVA readers have questioned why Evergreen has as many ‘Likes’ as it does in light of our concerns about severe overvaluation in most US stocks and growing evidence that Bubble 3.0 is deflating. Consequently, it’s important to point out that Evergreen has most of its clients at about one-half of their equity target.

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.