"ETF data for small-caps will create some adversity if flows were to turn meaningfully negative… the pickup in volatility may have a more adverse effect on highly exposed ETF firms."

-CIRRUS RESEARCH, an independent research firm that analyzes small-, mid- and micro-cap stocks

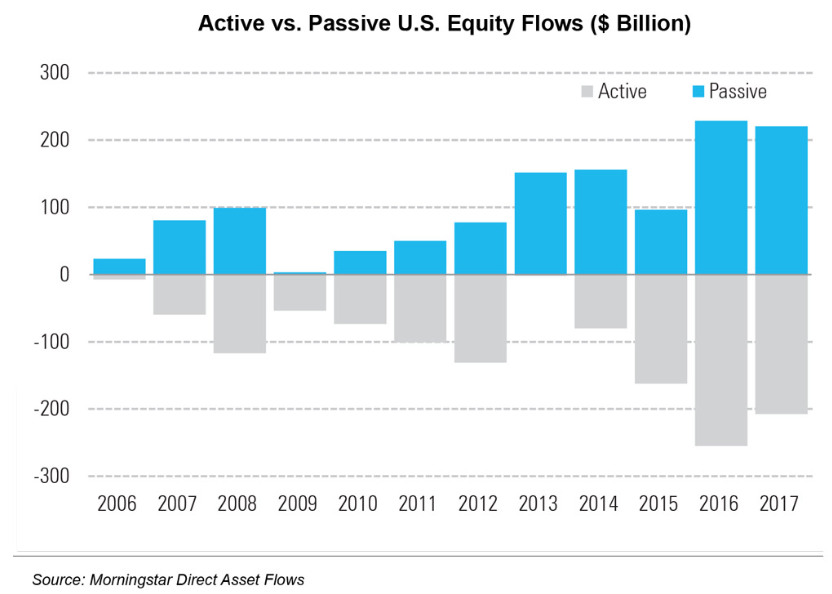

It’s been nearly a year since our newsletter last touched on the passive investing phenomenon. And yet, despite its absence from these pages, direct asset flows into passive vehicles have continued to outdo their active counterparts at a dizzying pace. As shown in the chart below, which comes from Morningstar’s annual fund flow report, it wasn’t even close in 2017.

While we will address this broader topic and its long-term implications for the market in a future letter, the purpose of this week’s EVA is to focus on a much more microscopic area of the investment world: small cap stocks. For regular readers, it should come as no surprise that Evergreen has been unapologetically bearish on the asset class – and for, what we believe to be, good reason. The following charts show just how overvalued the Russell 2000 – an index of small cap stocks – is on a historical basis in terms of Enterprise Value/EBITDA and Price/Sales ratios.

Source: Bloomberg, Evergreen Gavekal (as of 5/9/2018)

Source: Bloomberg, Evergreen Gavekal (as of 5/9/2018)

This week, we present a like-minded view that small caps are currently in “no-go” territory from our guest author, Eric Cinnamond. Eric is an investment manager who built his career investing in the space – originally, and ironically, for another Evergreen (that is, Evergreen Funds in Purchase, New York). What’s particularly telling about Eric’s outlook is that he is completely divested from any small cap positions. That’s right: zero, zip, zilch investment in small caps… from a small cap manager. In fact, Eric even shut down his small cap fund and returned money to investors because of the lack of worthwhile opportunities.

As the pages below reiterate, return expectations should be tempered in the small cap space for the foreseeable future. Passive ownership has propped up valuations and there are dangers in extrapolating cash flows and earnings during the late stages of an economic up-cycle. The next bear market will likely shine a light on the concentration of passive ownership, the risks associated with this, and the need for the return of the “small cap police.”

Eric Cinnamond, CFA, was most recently a Vice President and Portfolio Manager at River Road Asset Management, LLC. Prior to this, Eric was a Vice President and Lead Portfolio Manager of the small-cap strategy at Intrepid Capital Management Inc. which he joined in 1998. Previous to that he held similar roles at Evergreen Asset Management, Aston Funds – ASTON/River Road Independent Value Fund, and the asset management arm of Wachovia Corporation, formerly First Union National Bank. Eric has been a top returning small cap manager throughout his career, solidly beating the Russell 2000 even with an average of 40% allocation to cash. Please visit Eric’s blog to read more: www.ericcinnamond.com.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

THE SMALL CAP POLICE

By Eric Cinnamond

Today I was going to write about passive investing, but there was just too much for one post.

In 1996, I joined the Evergreen Funds in Purchase, NY and started working solely on small cap stocks. It was a great experience and I pinched myself every day heading into work. I was only 25 years old and was working on a 4-5-star small cap fund. In 1996-1997 small cap businesses were performing very well as the profit cycle was peaking. It was tough to make mistakes as rising profits were elevating the small cap market to record highs. I thought I was the next Warren Buffett, but in reality I was just in the right place at the right time. Nevertheless, I learned a lot during the mid-90s and look back on those years as a time when the foundation of the absolute return strategy I developed was formed.

The fund I worked on was called the Evergreen Small Cap Equity Income Fund. It was a very interesting fund – a small cap fund with a yield requirement. Imagine how well that strategy would be performing today given the panic for risk and yield! In any event, the yield was meant to help reduce downside and obviously produce income. It turned out to be a great risk-adjusted return strategy and was listed by Barron’s in their top 100 funds rankings in 1997 and 1998. In addition to helping us generate attractive risk-adjusted returns, focusing on stocks with dividends forced me to follow and analyze more mature businesses that generated free cash flow. This concept has followed me even today as the majority of the small cap businesses on my 300-name possible buy list are in fact mature businesses that generate abundant free cash flow over a profit cycle.

Another reason I’ve gravitated towards mature businesses is I believe they can be valued with a higher degree of confidence versus young and unproven businesses. If there is a long operating history to analyze, I can better determine how the business will perform throughout an industry and economic cycle. The more cycles the better. Also, the longer the history the better understanding one can have of the company’s normalized free cash flow. Extrapolating peak cash flows (what many investors are doing now in my opinion) is a very dangerous game. Conversely, extrapolating trough cash flows can lead to tremendous cost in the form of lost opportunities. Lastly, mature companies often are higher quality businesses. If a company has survived for decades and has flourished through multiple economic booms and busts, there is typically something high quality about the business.

So, what does all of this have to do with passive investing? Absolutely nothing. What I want to discuss, but was sidetracked, is how the top holders of many of the mature companies I follow has changed considerably since the mid-90s. At that time, I remember the top holders of high quality small cap companies were often large buy-side mutual funds such as Royce, Heartland, and Gabelli. Can you guess what the top holders of most small cap stocks are today? You guessed it, passive index funds such as Vanguard, Blackrock, and Dimensional Funds.

In my opinion, high quality small caps are the most expensive I’ve ever seen them. For the first time since 1993 I don’t own one stock – I am completely out of the market. Looking through my possible buy list there is very little I would consider to be a good investment or that will generate adequate absolute returns relative to risk assumed. In effect, by recently recommending returning capital to clients, I was recommending going 100% cash. And that’s where I am today.

When I look at some of the stocks I owned over that past 20 years that were trading at 10-15x earnings at the time of purchase and that are now trading at 20-35x earnings, I ask myself, “Who in the world is buying these things?” When I pull up the top holders to discover the culprits, I often see the most popular index funds and ETFs.

Mature small cap businesses that are growing 2-3% organically should not trade at aggressive growth-like valuations. The math simply doesn’t work for slow to no growth companies. Investors are getting a 3-4% earnings yield on earnings that are in many cases being generated off peak margins. As noted previously, extrapolating peak cash flows is a very dangerous game, but extrapolating peak cash flows AND requiring a meager low single digit earnings yield is, frankly, irresponsible (especially if you’re doing this with other peoples’ money). A rational investor or banker wouldn’t lend to these businesses long-term at 3%, but equity holders are supposed to be satisfied with these type of cap rates on uncertain perpetual cash flows?

Why are valuations of mature high quality small cap stocks so expensive? ZIRP, NIRP, and global QE* along with the investment philosophy of the day T.I.N.A. (there is no alternative) are obviously to blame; however, I believe the shift to indexing and passive investing is also responsible. Index funds do not care about earnings yields, risk premiums, margins of safety, cash flows, and on and on. When an index fund receives an inflow, it buys the stocks in the index regardless of fundamentals and price. I believe this sort of price indifference is one of the main reasons valuation multiples have expanded significantly this market cycle. I haven’t done the comparison, but if you pulled up a chart of index and ETF inflows I wouldn’t be surprised to see a high correlation to a chart of rising valuation multiples (especially price to sales and CAPE).

When I started this industry, small caps were policed by the largest holders, which were often disciplined buy-side managers. These “small cap police” helped keep law and order in the price and valuations of the small cap stocks they owned or followed. Unlike index funds, the buy-side funds were price sensitive. Mature and boring small cap businesses would seldom trade at today’s valuations because the top holders were expected to sell and take profits if valuations increased to levels that couldn’t be justified with rational assumptions. While overvaluation and investors’ willingness to overpay (the #1 investment crime!) are present in every cycle, the major holders were at least cognizant of companies’ worth and were not indifferent to price. Where are the small cap police today? They’re no longer as important and are dropping off the list of top holders.

So, without the small cap police what do we have? We have a market that is more price insensitive and dependent of flows. What happens when all of the index funds (the top holders) have outflows during the next bear market? Who will they sell to? They can’t sell to each other as they’ll all be selling at the same time to meet redemptions. Furthermore, since they’re fully invested they don’t have cash buffers and will have to liquidate holdings immediately, or that day. Just as they’re price insensitive on the upside, they’ll also be price insensitive on the downside.

I suspect most of the indexers who believe markets are efficient have never tried to liquidate a multi-million-dollar small cap position in a market with few bids. I’ve seen it. It’s sloppy, illiquid, and very inefficient. I believe the great passive investing unwind could be one of next attractive buying opportunities for disciplined absolute return investors. I’m ready and looking forward to owning small cap stocks again.

*ZIRP stands for Zero Interest Rate Policy. NIRP stands for negative interest rate policy. QE stands for Quantitative Easing.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.