“At the edge of chaos, unexpected outcomes occur.”

-MICHAEL CRICHTON, American author and filmmaker

“It’s not the Fed’s job to stop people from losing money.”

-Incoming Fed chairman JAY POWELL

“When you start using the market as a casino, that’s a huge mistake.”

-CARL ICAHN in a CNBC interview last week

First, please accept my apologies for a slightly delayed edition of our annual Unexpected Outcomes Evergreen Virtual Advisor. However, as most regular EVA readers know, we have run several forecast-oriented issues to kick-off the new year, particularly our Evergreen Roundtable on January 12. Additionally, we’ve published two forward-looking pieces from Gavekal’s Anatole Kaletsky (The Big Questions for 2018 and The 5 Big Bond Market Questions for 2018) and last week’s Quarterly Webinar EVA also included a number of “anticipations”.

Yet, I feel like we should stay true to the concept of outlining a number of items which aren’t so much forecasts as they are plausible surprises. In other words, developments that, should they happen, would constitute a wrong-footing of consensus views.

Before we get to this year’s Unexpected Outcomes, let’s do a quick review of last year’s results. For those that just want the bottom-line, my best attempt at objective scoring is to give myself a 7 ½ out of 10, or a 75% “hit” rate. Considering that these were all contrarian postulations, that’s not bad and probably better than I’ll do in the future. As usual, one crucial point I missed—and the majority got right—was with the US stock market which, as we all know, had another outstanding year. In my defense, though, I did speculate that the long-lagging international markets might surprise almost everyone by outperforming the S&P 500, which did in fact happen.

France was my particular favorite based on what I thought would be successful reforms by Emmanuel Macron. My view was that Mr. Macron’s stunning landslide in the French presidential election in 2016 would give him the momentum and political capital to implement a series of acutely needed reforms in that long-sclerotic economy. This was a very non-consensus viewpoint but, thus far, it does appear to be playing out as I hoped.

Perhaps my best against-the-crowd call was related to oil. In January of last year, the consensus had become extremely bullish even as inventories were overflowing. This led me to believe that a correction was highly probable and that if and when it happened, it would cause sentiment to turn very negative on oil, setting the stage for a rally in the second half of the year. Because this expectation had a double element to it—and also turned out to be dead-on—I gave myself an extra half-point credit. (Self-grading does have its advantages!)

Enough on last year—it’s time to move on to what surprises may be in store for 2018.

1. The Fed. Last year, I was right to think J. Yellen & Co. would catch the markets off-guard by hiking rates as much as they said they would at the start of 2017, something it hadn’t done once throughout this expansion. Presently, judging by the futures market’s pricing of the fed funds rate, there is an underestimation of our central bank’s resolve to restore interest rates to anything in the same zip code as normal, particularly for what is considered to be a healthy economy.

My take is that the market is once more underestimating the Fed, especially given that it is under new management these days. This is another deviation I have with the prevailing group-think. Jay Powell, who has just taken the baton from Janet Yellen, is widely perceived to be her clone. But I disagree.

Based on a series of statements he has made lately—along with revelations of the misgivings he had at the time about the Fed’s ill-advised QE3—I believe he is much less committed to avoiding market turbulence than was Ms. Yellen. In my opinion, the Fed will hike rates at least four times this year and—for extra credit—I’d even speculate that a ½% bump at a future meeting is a distinct possibility —something that would really throw the forecasting community for a loop.

One caveat: should the stock market’s recent weakness morph into an actual bear market, all bets are off. One senior Fed-head recently said that if the market fell hard, and stayed low, the Fed would likely stand down and I think he’s telling it straight. But, please realize, he’s saying that it would take a severe and lasting decline to shift the Fed’s tightening stance.

Also, please be aware that this is the first time in history the Fed is engaged in a double-tightening: raising rates at the same time it is shrinking its balance sheet (by letting its massive trove of treasury and mortgage securities contract). Despite the market turmoil over the last couple of weeks, the Fed is dropping no hints it will deviate from this double-tightening. My belief is Jay Powell and his colleagues will issue further warnings that they will continue to raise the cost of money and simultaneously suck excess liquidity out of the system. Those that ignore them will be doing so at great risk to their portfolios.

2. The Bond Market. This was another one of our better surmises from last year as we correctly saw yields on the 10-year T-note staying in a range of 2% to 2.7%, even as the Fed tightened. We also accurately felt that would flatten the yield curve. Recently, though, as regular EVA readers know, we shifted our views, believing that the crucial 2.65% upper bound that has persisted for many years was likely to be broken to the upside.

This, of course, occurred in January with the rate on the T-note touching 2.9% and it played a starring role in the stock market’s recent reversal. Consequently, the formerly extreme bullishness on treasuries has flipped into pessimism, as almost always happens when an asset class falls on hard times.

Yet, at this point, the negativity is not at peak levels but it may be quickly heading that way. My best guess is that treasuries will stabilize for a time just under the super-critical 3% yield threshold. This has held since the “taper tantrum” bond rout of mid-2013 that lasted until early 2014. Should 3% get taken out, the next stop appears to be around 3.75%. Few observers seem to feel that we could see rates vault that high, but I believe it is much more than a long shot. (It was also highly unusual for bond yields to have stayed close to their highs even when stocks were getting pounded last week.) In fact, I’d say another treasury rate spike is a likelihood for some of the reasons covered below. If I’m right, this is nearly certain to be a huge factor in Unexpected Outcome #3.

3. The US Stock Market. First, let me once again say that millions of investors should be paying me to keep calling for a market pull-back. This ultimate “unexpected outcome” of mine has worked wonders for extending the longevity of what is quickly closing in on the 1990s as the longest bull market ever.

Lately, as I outlined in last week’s quarterly webinar, I’ve been noting a number of parallels with 1987, the year that some of us old fogeys remember as having a bit of market hiccup (like 30% down over five trading days!). Undoubtedly, that possibility seemed ludicrous a couple of weeks ago as the market kept relentlessly making new highs. After the air pocket stocks hit at the end of January, it suddenly seems less absurd.

However, it’s reasonable to say that such an event is still viewed as highly unlikely by most Wall Street strategists and, of course, the constant cheerleaders on CNBC. At this point, we are probably due to see more big rallies and sharp sell-offs as the market attempts to find its footing at this level. As long as 3% on the 10-year holds, that should be doable. But if my suspicion that 3% is taken out later this year, and a rapid rise to the upper 3s occurs, then a replay of October 1987, becomes a very real possibility.

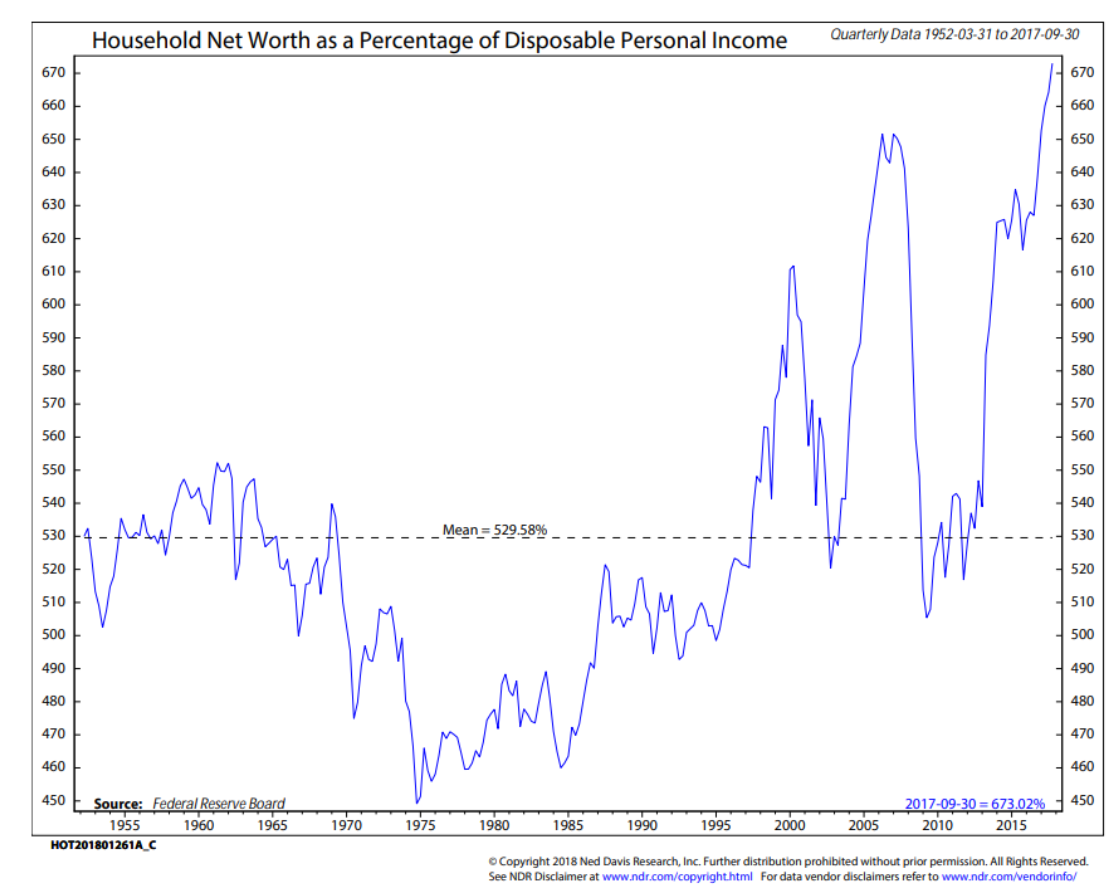

The good news is that 1987 was actually a positive year for stocks because they had risen so much before the crash happened. This year, the rally that kicked-off 2018 also created a cushion and I wouldn’t discount another rally that restores much of what was lost towards the end of January—or even more. But here’s the dilemma for stocks: the further they rise, the more likely the Fed is to be aggressive on the rate hike front. As I noted last week, people forget that the crash of ’87 happened despite a popular tax reform the prior year, strong earnings, and a roaring economy. Consequently, a nasty shocker for stocks this year could be a sudden cliff-dive that makes what we saw earlier this month look mild. Per the following chart from Ned Davis Research, you have to be wearing a pair of super strong bubble goggles not to think it’s a very high cliff indeed.

4. Inflation. For years, Evergreen has downplayed the risk of a rapid rise in the CPI, even when the Fed was creating money by the trillions through its QEs 1, 2 and 3. But there is the scent of higher prices in the air these days—and not just for stocks. Ironically, this is just what the Fed and other central banks have yearned for years. But, perhaps it’s another example of “be careful what you wish for because you are going to get it good and hard”.

The fact that inflation has consistently undershot the 2% level—that, for some reason, central banks all want to see—is why they have collectively kept fabricating money by the trillions. This has been true even as the leader of the pack—the Fed—long ago shut down its digital printing presses. As previously noted in these pages, the first half of 2017 saw the greatest amount of QE in the post-financial crisis era.

Therefore, as central banks have frantically attempted to push inflation to their desired 2%, they have created enormous asset price inflation. They have used the CPI shortfall to justify their pedal-to-the-metal policies even in the midst of what is popularly known as a global synchronized recovery. In the US, an economy that is running at pretty much full tilt is now getting a major jolt of highly stimulative deficit spending due to the new tax bill. Thus, the usual late cycle flare-up in inflation is likely on the horizon and, per the Wall Street Journal headlines below, it is perhaps even closer than that.

As a result, the Fed may be even more motivated to clamp down, with the bond market also likely to be on high alert with regard to inflation. Ergo, it’s possible we will see a “triple tightening” between the Fed shrinking its balance sheet and hiking rates at the same time that the bond market cracks, pushing rates well above 3%. If so, we doubt inflation will prove very durable. In what could take the irony to a whole new level, by obsessing so much about attaining 2% inflation—and creating vast asset bubbles in the process—the central banks may get a very surprising bout of deflation once the myriad speculative manias end in tears. As a matter of fact, one of those already has.

5. Crypto-currencies. In my section of our Evergreen Roundtable, the asset class I least favored was Bitcoin and its many sketchy off-shoots. It was just in mid-December that Bitcoin hit $20,000, causing a rabid enthusiasm among millions of retail investors unrivaled since the fascination with dotcom stocks in the late 1990s. The hysteria for the cryptos also caused Evergreen to write a scathing EVA about them on December 22nd.

Most uncharacteristically for me, I hit the peak almost to the day instead of my usual premature bubble recognition syndrome. You may have seen that last week Bitcoin touched $6,000, a decline of 70% from its zenith in just two months, before rebounding to around $10,000 today. As I commented back in December, the main significance of what was the biggest bubble in human history—exceeding even the mythic tulip bulb frenzy in the 1600s—was that it revealed the ambient conditions, namely of outlandish risk tolerance and outright greed.

After experiencing a 70% decline, it’s safe to say this bubble has popped, notwithstanding the recent bounce. This is most definitely not to say there can’t be another rousing rally or two that will probably serve to lure back in some of the suckers players who still have a little money—or, if you will, a bit of coin—that hasn’t been vaporized…yet.

Again, the bigger significance in my mind is the flow-through to more legitimate asset classes. Back in early 2000, the dotcom stocks imploded even as the overall market continued to rise. But the “dot.bombs” were definitely the canaries in the coal mine that indicated the great 1990s stock bubble was on borrowed time. These days, the canaries are dropping like flies in a polar express—including one that has been an incredible profit machine for years.

6. Volatility. It would be bad form to use a dramatic change in volatility as an unexpected outcome had it not been for my comments in the Evergreen Roundtable that the unprecedented short position in volatility was a “huge risk”. (For all of you who don’t understand what shorting volatility is, be thankful you don’t. These were essentially bets that market fluctuations would continue to look like the EKG of a cadaver—which they did until a few weeks ago.)

For years, shorting the “VIX”, as the volatility index is popularly known, has been a printing press worthy of a central bank. Some readers may remember the EVA we did on this last September when we highlighted the good fortune of a former Target middle manager who had parlayed $500,000 into $13 million by shorting the VIX (at last report, said individual had seen his nest egg shrink down to $3 million and, based on subsequent events, possibly much less).

Shorting volatility was also a very popular trade among institutional investors, primarily hedge funds. The utter collapse of exchange traded funds that specialize in shorting the VIX—like down 95% in a few days—virtually assures astronomical losses for the “professionals” who have been playing this financial version of Russian roulette. In my mind, the collapse of this so-called strategy is another graphic indication that the Bubble-mania we’ve been engulfed in for years is rapidly approaching its sell-by date. In fact, I would argue the date investors need to sell-by was a few weeks in the rearview mirror.

It’s my suspicion that even more volatility lies ahead, despite the fact the market is now treating what happened earlier this month as just a bad dream—and definitely not the end of the dream-like conditions that have persisted for so long.

7. Foreign Markets. To expect outperformance by foreign markets vs the mighty S&P 500 certainly isn’t as radical as it was a year ago. However, according to our partners at Gavekal, institutions remain underweight both Japan and China. The former continues to be one of our favorite markets, a stance we articulated a number of times in EVAs during 2017. China is more of an enigma to us, but we defer to Team Gavekal who views it as one of its preferred markets.

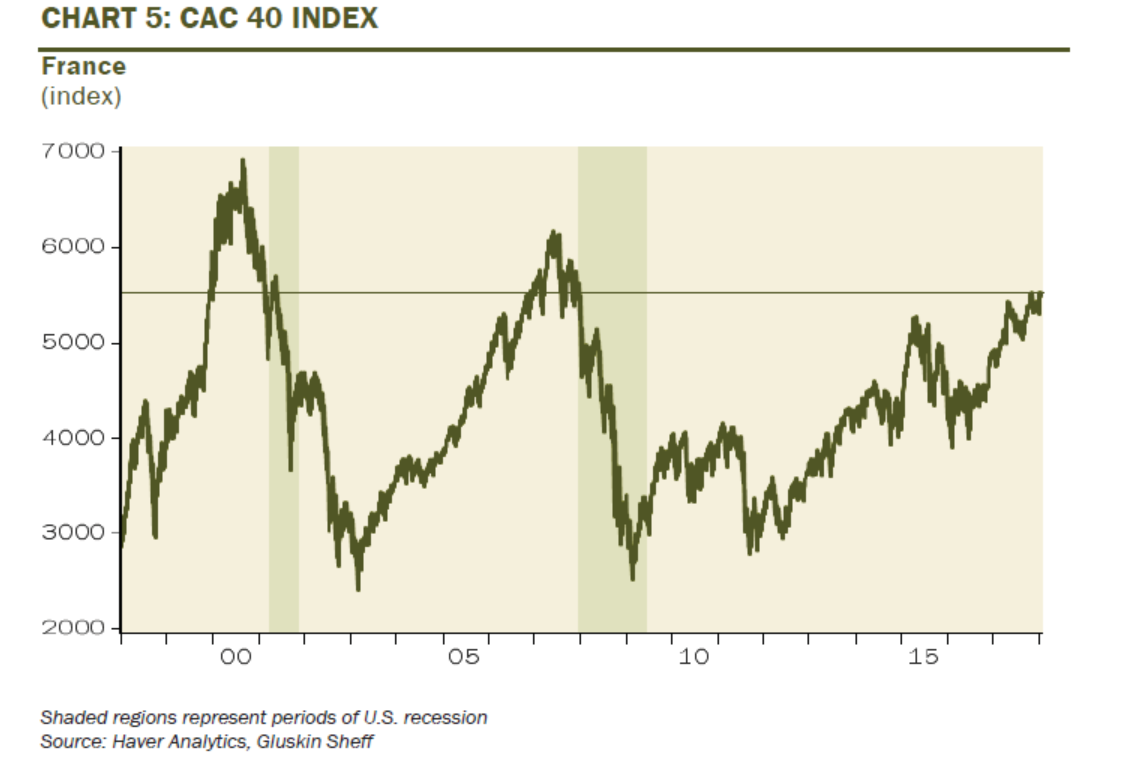

Similarly, how many people have you heard bragging about their French stocks lately? Suffice to say, France remains deeply out-of-favor and yet the CAC40 (their equivalent of the Dow) recently achieved an impressive breakout. But, per the following chart, note that it is still well below its 2000 apex.

If I am right that there is another shakeout coming for US stocks, it’s a lock that foreign markets will get hit, too, as they have recently. Should that be the case, investors will likely be well-advised to do the “buy the dip” routine overseas rather than at home. And that’s not at all what most folks are expecting to do.

8. US Politics. Leftward ho! The combination of a still strong stock market and generally upbeat economic news is leading many to assume that the populism seen during the 2016 election (evidenced by both the election of Mr. Trump and the Bernie Sanders phenomenon) is a thing of the past.

Unlike any president before him, Mr. Trump has benchmarked his presidency to the S&P 500. That’s great when the bull is running but when it suddenly stops—and, particularly, should an ursine animal take its place—then the folly of that strategy will be fully exposed. Thus, the surprise I’m proposing might be a leftward lurch by the US electorate should the stock market crater and overall confidence do the same. Maybe this can be avoided before the mid-term elections, but it seems highly improbable we can make it all the way to 2020 and the next presidential election without a full-fledged bear market and recession. Regardless, a rough time for the GOP come November would clearly catch the stock market off-guard.

9. Energy. No other major sector of the market has been as beat up over the last three years as has energy. In fact, since the prior market peak in 2007, energy is the lone sector that has actually posted a negative total return.

The mood swings toward crude are borderline manic depressive, maybe sans the borderline. Accordingly, paying attention to extreme bullish and bearish sentiment readings—and doing the opposite—has definitely proven to be rewarding.

Up until recently, the intense negativity seen last summer had flipped into euphoria—just in time for the latest price swoon. In that regard, this year is looking a lot like the start of 2017 with one very material difference: the oil market is much, much tighter from a supply standpoint.

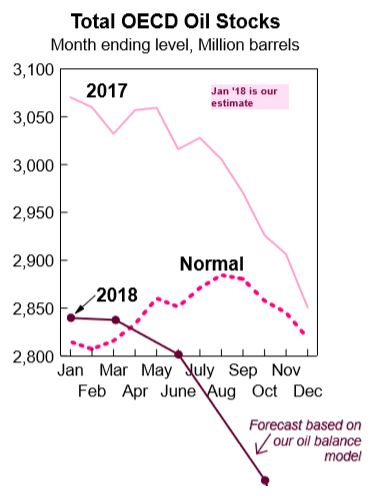

In fact, at a time of year when there is typically an inventory build, we are seeing the opposite. Per the following chart, you can see the magnitude of the swing not only versus 2017 but also relative to normal seasonal trends.

As I mentioned in the Evergreen Roundtable EVA, a correction was to be expected after hedge funds and other short-term players became wide-eyed bulls. Fast-money types are already running for cover, but I continue to believe that the energy sector will materially outperform the S&P 500 over the next few years. This includes master limited partnerships (MLPs) which have also dipped but relatively mildly, especially considering that bond yields are up while oil prices and stocks are down—a nasty triple-whammy. The bottom-line: rather than fleeing from energy when it corrects, as the herd is doing once again, I anticipate another rally that will once more baffle the consensus.

10. Debt Crisis. One of the most harmful long-term aspects of central banks’ money for nothing policies (or less than nothing, in many cases) is what it has done to the always shaky fiscal discipline of governments around the world. The US is a classic case in point. At this late stage of an economic expansion, deficits should be falling. Instead, they are rising. The US deficit as a percent of GDP has risen for three years in a row, the first time this has ever happened outside of a recession. And the red ink is poised to surge much more this year...and as far as the eye can see.

Presently, this doesn’t worry the cheery consensus at all, which seems convinced that the sharp market decline of the last few weeks was just a fleeting fleeing by a handful of Nervous Nellies. But with the Federal deficit poised to soar to close to $1 trillion this year, at the same time the Fed will be reducing its treasury holdings at a $600 billion annualized clip by mid-year, the potential for a train wreck is far from trivial. Thus, the net amount of additional funding needed to be provided by the market is over $1 trillion. The risk of a financing seizure is especially acute with both the Fed and the bond market raising rates.

Two-thirds of US debt matures within five years. Presently, the interest carry on this is a mere 1.78%, per my good friend and venerable money manager, John Goode. As a result, the Federal government is highly exposed to rising rates, as are so many consumers and businesses with floating interest costs, particularly with the Fed committed to another series of hikes this year.

As noted in earlier EVAs, globally it’s a similar story as the planet at large has feasted at the banquet table of free money. 2007 was considered to be the pinnacle of debt-driven insanity yet global debt levels are up from 280% of GDP back then to nearly 320% now. In dollar terms, about $70 trillion of additional indebtedness has been accumulated over the past 12 years.

But, because of the rapid deterioration of the US fiscal position—largely, but not totally, due to the new tax law—America is likely to experience the first crisis of confidence, at least among leading countries. Projections are for a $1.2 trillion deficit next year, 5.4% of GDP, which is truly horrifying considering this assumes decent growth. Imagine what the shortfall will look like in the next recession. (By the way, unfunded liabilities like Medicare and Social Security bring the actual national debt up to $75 trillion, four times GDP.)

Again, Wall Street and the many bull-market-forever believers are not the least fazed by these daunting numbers. Therefore, my final potential curveball for this year is that debt emerges as the four-letter word that comes back to haunt the complacent consensus.

To wrap up this Unexpected Outcomes EVA, the overarching surprise might be that 2018 turns out to be a very different year than 2017, in no small part because this is likely to be a very different Fed. It will probably take some time, but the realization should eventually sink in that J. Powell is no J. Yellen. When investors discover that the legendary “Fed Put”—the level at which our central bank will ride to the market’s rescue, with printing presses blazing—is much lower than they believe, there is likely to be serious yellin’ and screamin’ and, eventually, cryin’.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.