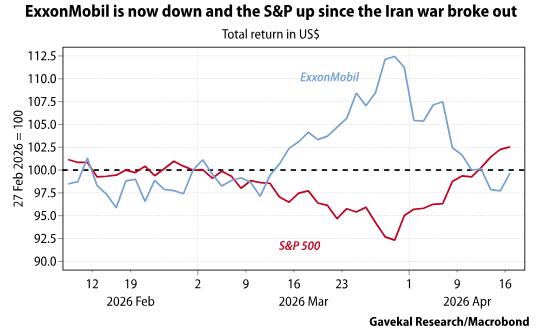

The S&P 500 index has now risen for 12 consecutive days (March 31-April 16, 2026). The 11% gain recorded since its recent March 30 low is in the 99th percentile for 12-day returns. In short, it has been quite a rally. Perhaps most impressive is that the S&P 500 is now back above its February 27 level, when the Iran war started. Since that day, the index is up a couple of percent, while ExxonMobil, the largest US oil company, is down by roughly the same amount.

At first glance, this seems massively counterintuitive. After all, over the same period, 30-year treasury yields have risen 25bp, WTI crude is up by roughly US$25 a barrel, gasoline prices have risen by US$1 a gallon and crack spreads have soared. So how can equity markets brush off all this bad news? Is this a traditional case of “climbing the wall of worry”? Are markets too complacent?

The aim of the following piece is to examine the possible explanations for the impressive equity rebound, while acknowledging that we are very much scratching our heads as to why equity markets seem so sanguine in the face of what appear to be meaningful supply chain dislocations across key inputs, whether oil, natural gas, fertilizer, sulfuric acid or urea.

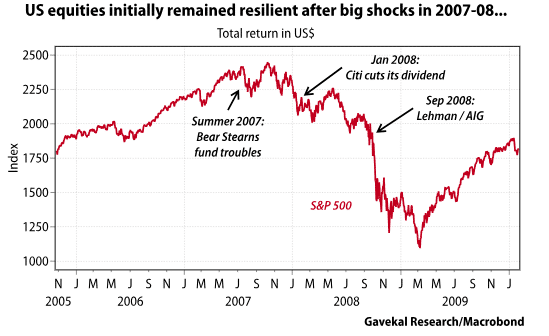

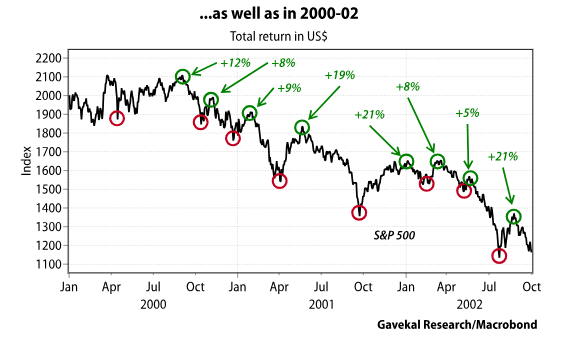

Option 1: The strongest equity market rebounds tend to occur in bear markets. This is what makes investing during bear markets so challenging, even for bears. Take 2007 as an example. In June 2007, Bear Stearns was forced to bail out two of its funds with exposure to US mortgage debt and then in August credit markets froze after BNP Paribas stopped withdrawals from two similar funds. The S&P 500 index quickly shed -10% but then bounced back and went on to make new highs. It then moved sideways through the summer of 2007, even as news of mortgage issuers, such as Countrywide, running into trouble continued to build. By January 2008, Citibank, HSBC and UBS were taking large write-offs and slashing dividends. In March, Bear Stearns failed and by the fall of 2008, the wheels had come off the wagon. In other words, the mortgage crisis arguably started in earnest with Bear Stearns’ fund troubles, yet throughout this period the market experienced a number of meaningful rallies. A similar pattern was seen in the 2000-02 bear market.

Embracing option 1 essentially involves saying that recent market signals should be ignored. To be clear, sometimes that is the right thing to do. But it is seldom comfortable. When the market moves against one’s assumptions, one should at least be willing to question them. Which brings us to the other options below.

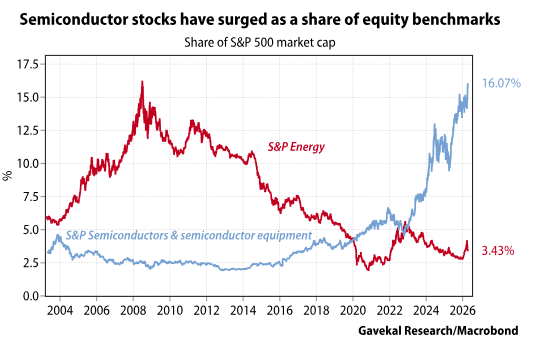

Option 2: The Persian Gulf is not the story. Artificial intelligence is. The rally off the late March lows has been led first and foremost by semiconductor stocks. Since the March 30 low, the PHLX semiconductor index is up 25%. Names such as Samsung Electronics, SK Hynix and Taiwan Semiconductor Manufacturing Company have surged, to the point where Taiwan now has a larger market capitalization than the UK, creating challenges for investors benchmarked to Asian or emerging market MSCI indexes as these stocks become an ever larger share of benchmarks. Even in the US, as the semiconductor index reaches new all-time highs, semiconductor stocks account for 16% of the S&P 500, compared with 3.4% for energy.

Interestingly, while semiconductor stocks have soared (up 31% YTD for the PHLX semiconductor index), software stocks (down -21.5% YTD for the S&P North American expanded technology software index) continue to make new lows. Which brings us to the main challenges to the view that semiconductor stocks can continue to rise in a vacuum. Specifically:

Option 3: Hopes that oil prices will remain contained because China is now a moderating force in the market. A contributing factor to the 2008 crisis was the spike in oil prices from US$100/bbl to US$150/bbl. That surge was largely driven by the Gansu-Sichuan earthquake in the run-up to the Beijing Olympics. Ahead of the games, Chinese factories were operating at full capacity, knowing production would be curtailed during the Olympics to ensure clear skies. Then, in May, disaster struck, with tens of thousands of casualties in the deadliest earthquake since 1976. The Chinese government mobilized rapidly, taking control of the rail system to transport rescuers and supplies to the affected regions. As a result, coal shipments were disrupted, and factories that had been running at full tilt were forced to rely on diesel generators. Oil and gasoline prices duly surged. Today, the situation is almost the mirror image. Rather than being a forced buyer of energy, China is sitting on record inventories and benefits from a much more advanced electricity grid. So perhaps the market is brushing off concerns over the Persian Gulf because the world can absorb US$100/bbl oil, and because China is unlikely to bid prices up to levels that would derail the global economy.

The underlying notion behind this explanation is that the supply shock from a closure of the Strait of Hormuz will prove manageable. China would draw down the excess inventories it has built up, Russia would ramp up production, Saudi Arabia would divert exports through the Red Sea and Iraq through Turkey. This is not to say that all will be well. Smaller, poorer and more marginal economies will still struggle. In this world, being Sri Lanka, the Philippines or Kenya is not a good position. But the larger players should be able to muddle through, which, for financial markets, is what ultimately matters.

As it turns out, this theory is likely to be tested in the coming weeks. The Strait closed six weeks ago, and in the weeks that followed, ships that had departed the Gulf before February 27 were still being unloaded. By now, however, all vessels that left before the war have reached their destinations. And even if the Strait was to reopen tomorrow, no new shipments would arrive for at least another month. The coming weeks will therefore be the real test of whether financial markets have been too complacent about supply chain dislocations.

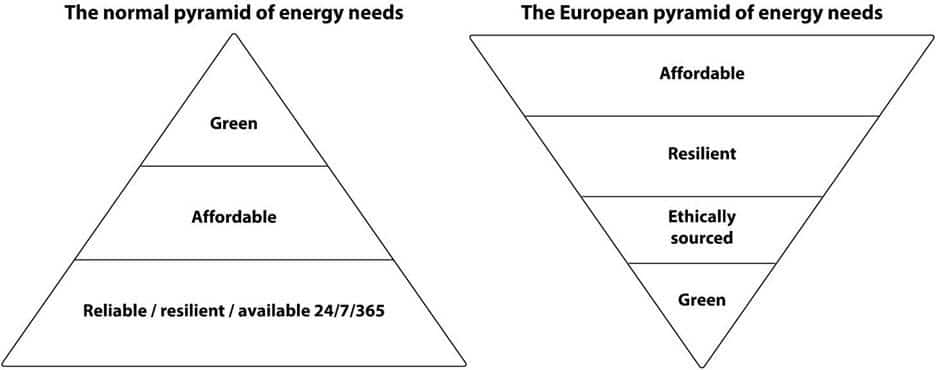

Option 4: Acknowledgment that every country will now have to review its energy policies. Numerous countries have in recent years adopted “upside-down” energy policies.

The Ukraine and Iran wars have now served as wake-up calls. Just as France embraced nuclear energy after the 1973 Arab oil embargo, countries are now likely to push for more electric vehicles, solar, wind, nuclear, geothermal and even coal, effectively moving toward the kind of energy strategy China has pursued over the past decade for national security reasons. To the extent that this entails greater investment in productive infrastructure, it could prove to be a positive development.

Still, grids take years to upgrade and power plants years to build. In the short term, these new energy imperatives are likely to lead to a relaxation of tariffs on Chinese solar panels, batteries, windmills, turbines and electric vehicles, alongside a rebuilding of inventories of oil, natural gas and coal. Lower tariffs on Chinese goods would be a positive deflationary shock, while inventory rebuilding would represent a negative inflationary shock.

Over the long term, smarter energy policies are undeniably positive. So perhaps markets are looking through the painful short term, namely higher costs of capital as infrastructure spending and budget deficits increase, toward a more prosperous future driven by more stable and cheaper energy costs?

Option 5: The US dollar quandary. Foreign investors today own roughly US$9.5trn of US treasuries and an additional US$3.5trn of US corporate debt. This debt is held for many reasons, but the principal one is that US debt has been the cornerstone of the post-World War II financial system. Foreigners save in US dollars on the premise that, in a crisis, the US Navy can deliver weapons, food, energy or whatever else may be needed. But is this still the case? The world is changing rapidly. Warfare has become asymmetric. The US is no longer seen as a benign hegemon, and its navy no longer fully controls global sea lanes. In a conflict, is it better to have a single US$150mn F-35 or US$150mn worth of US$500 Chinese drones and US$80,000 ballistic missiles? Rather than accumulating US dollars, does it now make more sense to stockpile commodities?

Assuming that the Iran war is the moment when investors are forced to recognize that the world has changed dramatically, the obvious question is whether they will continue to hold trillions in US debt, or whether that capital begins to shift into real assets, whether commodities or equities. In that spirit, perhaps the simplest explanation for the recent equity rally is that, following the initial shock and sell-off, investors are gradually repositioning portfolios for a world in which the need to hold US dollar-denominated debt is diminishing.

The counterargument is that, if this were the case, one would expect precious metals to be making new highs and stocks such as ExxonMobil to be performing particularly well. However, as noted above, market performance has been highly concentrated in AI-related names.

Conclusion

The market seems to have returned to where it was before the Iran war began, namely strong enthusiasm around AI and limited concern for anything else. Against this backdrop, readers will typically fall into one of two camps. The first argues that AI will change the world and nothing else really matters. The other, of which we are fully paid-up members, holds that rising energy costs will at some point puncture the AI narrative, just as they did during the 2008 equity market bubble. Importantly, we should know in the coming weeks which of these views is more likely to prevail. Our bearish stance rests on the premise that current supply chain dislocations are significant and will begin to surface more clearly in the near term. If that proves not to be the case, then the market will have been right to climb the proverbial wall of worry.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.