_____________________________________________________________________________________________________

By Dan Wang and Yanmei Xie of Gavekal Research and Gavekal Dragonomics. Published on March 3rd, 2022.

Not long before Russia invaded Ukraine, Xi Jinping and Vladimir Putin met in Beijing and declared the friendship between their countries had “no limits”. Russia is likely finding out now that this “future oriented strategic partnership” is in fact limited. While China shares Russia’s disdain for the US-led international system, its material assistance to Russia under Western sanctions will be meager. In recent days, officials in Beijing have inched away from their earlier pro-Russia statements and taken on a more neutral tone. As sanctions threaten to reduce Russia to an economically isolated pariah, China will not ride to its rescue.

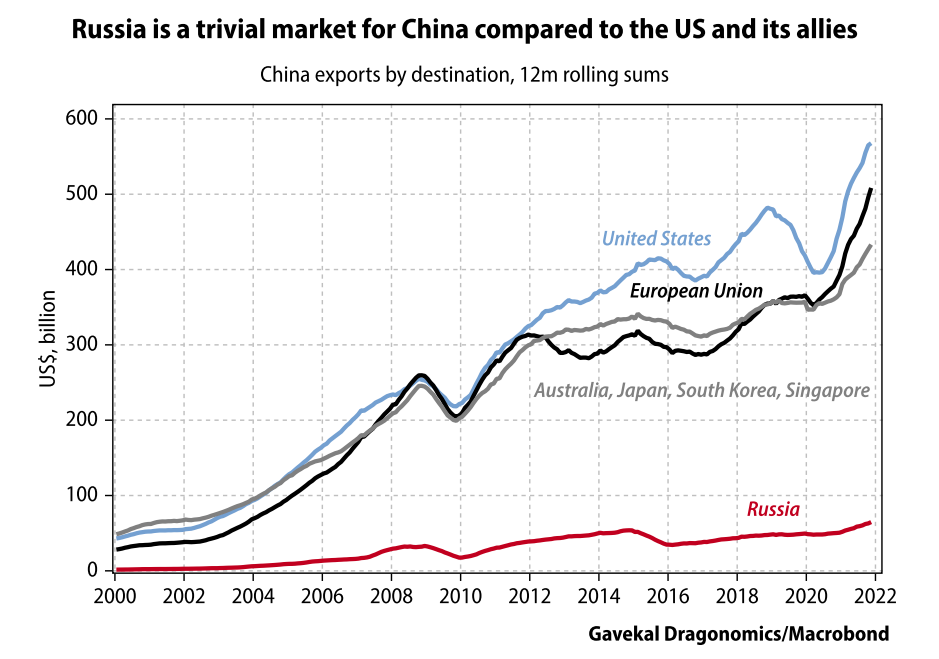

The calculation for China is simple: its commercial ties with the US, European Union and their allies in Asia are much more important than those with Russia. China exported about US$68bn of goods to Russia in 2021; its exports to the US and EU together are well over US$1trn. Even though China’s government probably wishes to assist Russia, it cannot shield its companies from the potentially crippling punishments for violating sanctions. Officials are likely to follow their past practice of implicitly advising companies to obey sanctions by alerting them to risks. Beijing will not bust sanctions and risk losing access to markets in the developed world, which is united against Russia.

The US, UK and EU, along with Japan, South Korea, Australia, Singapore and other countries, have jointly imposed a battery of financial sanctions against Russia. They include freezing the assets of Russia’s central bank, banning transactions with major Russian commercial banks, disconnecting selected Russian banks from the Swift financial messaging system, and restricting transactions in Russian debt and equity. The combined effect is to significantly limit Russia’s ability to conduct international transactions.

Chinese diplomats have criticized the sanctions, and top banking regulator Guo Shuqing said Wednesday that China will not join in the financial sanctions but will instead “continue to maintain normal economic, trade and financial exchanges with relevant parties.” Such a statement, however, does not mean Chinese banks will defy the sanctions. On the contrary, large state-owned Chinese banks reportedly have already begun limiting transactions with Russia. Such moves are consistent with their historical pattern of complying with US sanctions against North Korea, Iran and even Hong Kong at the same time as the Chinese government vehemently denounced those sanctions.

The basic incentive for Chinese financial institutions to comply is the same as for their Western counterparts: self-preservation. The US Treasury Department has the legal authority through the Countering America’s Adversaries Through Sanctions Act to inflict secondary sanctions on non-US companies or individuals that “knowingly facilitate significant transactions” with blacklisted Russian entities. The US has repeatedly applied such secondary sanctions under other laws to enforce previous sanctions against North Korea, Iran, Russia or Venezuela. Losing access to the US financial system and the ability to conduct transactions with US counterparts is too big a risk for most Chinese banks. “I don’t think you will see many large Chinese multinational banks that will keep an open door to the most heavily sanctioned sectors of Russia’s economy,” said Nick Turner, a sanctions specialist at Washington-based law firm Steptoe & Johnson.

The tough financial sanctions on Russia have led to calls in China to increase the use of renminbi rather than US dollars in trade, and to widen the use of its home-grown Cross-Border Interbank Payment System (CIPS) rather than the Swift network. While it is true that it would be technically easy for trading companies to shift the invoicing currency for goods, or for banks to install new software, these measures would not fundamentally reduce China’s vulnerability to US sanctions. Chinese companies transacting with banned Russian banks still risk secondary sanctions no matter which settlement system or currency they use. Only institutions that have no need to transact with the US can actually ignore the risk of sanctions, and such institutions are few and insignificant (such as Bank of Dandong which deals with North Korea, and Bank of Kunlun which deals with Iran).

Technological decoupling

In addition to financial sanctions, the US has imposed strict export controls on Russia that have also been matched by its allies. As with the devastating chip embargo on China’s tech giant Huawei, the US is asserting jurisdiction over all products made with US software or tools, and requiring an export license to supply such products to strategic Russian industries, including the defense, aviation and maritime sectors (see The Sanctions Sledgehammer). These sanctions will deny Russia access to critical technology products such as semiconductors, encryption security, lasers, sensors and navigation, with the goal of degrading the industrial and military base over time. The result is that companies from Boeing to Apple are assuming they can no longer sell to Russia.

Although China is also chafing under similar but more targeted export controls, it is unlikely to offer substantial technological help to Russia. Again, the reason is simple: Chinese companies have much more to lose than to gain by violating sanctions. For most Chinese companies, Russia is just too small of a market for the business to be worth the risk of getting cut off from developed markets or being sanctioned itself. From the US, Europe and Japan, China needs access in particular to semiconductor materials and equipment, as well as various types of high-end capital goods such as jet engines. Even the Chinese companies already suffering from US restrictions would have more to lose. Although Huawei and SMIC are both already on the entity list, they are still able to receive some US technologies with the permission of the Department of Commerce. If they violate US law, then they risk being added to either the denied persons list (maintained by Commerce) or the Special Designated Nationals list (maintained by Treasury), which would result in much harsher restrictions. Given the risk that existing US sanctions could escalate further, Chinese firms have good reason to stay well behaved.

Energy balancing act

Energy transactions so far have been exempted from the sanctions, due to Europe’s heavy reliance on Russian natural gas and oil. Should the West decide to impose an energy embargo, fear of secondary sanctions would again compel China’s state-owned oil and gas majors, which control the vast majority of the nation’s energy import infrastructure, to comply. Independent importers may snatch up cheap Russian supply, but their volume will be limited by capacity constraints and import quotas.

Equally, if Russia deliberately cut down its natural-gas exports to squeeze Europe, China may be able to absorb some additional Russian supply at the margin, but not enough to offset the financial losses. China received roughly 10bn cubic meters of natural gas from Russia last year via the Power of Siberia pipeline, which began delivery late 2019 and is the sole natural gas route between the two countries. That pipeline could theoretically carry as much as 38bn cubic meters per year—a fraction of sales to Europe, estimated to be about 175bn cubic meters in 2021. Furthermore, the pipeline is not connected to the fields that supply Europe, which makes it difficult in the short term for Russia to reroute to China natural gas previously intended for the West.

The existing structure of global trade and the logic of self-preservation mean that, despite the political alliance that Xi and Putin celebrated not long ago, China in practice will offer Russia little more than rhetorical solidarity with its sanctions woes.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.