Introduction

Bears and bulls sit on both sides of virtually every debate. Bitcoin is no different and, in fact, might be the modern-day posterchild for pontificators and investors waging an age-old argument around intrinsic “value.” The headline captured below underscores this point, questioning if the emerging asset is disruptively valuable or a passing fad that’s practically worthless.

Since 2017, this newsletter has published several opinions on the subject of bitcoin, presenting different viewpoints on whether this “digital gold” is a goldmine or a sinkhole. This week, we are presenting an extremely bullish outlook on the digital currency from an intelligent, true bitcoin believer, Pedro Noronha. Pedro is a friend of Evergreen’s and is the founder and managing partner of Noster Capital LLP. Interestingly, despite his current bullish stance, he started out bearish back in 2017 and shorted the digital coin at that time, which was around the same time when we first put out our negative view of the asset.

Similar to Pedro, we have softened our stance over time, but have held firm to the belief that the inevitable blow-up of stablecoins and exchanges is more than likely to create another crash in the world’s first cryptocurrency. We also believe, as we’ve often written, that perhaps the biggest drawbacks of Bitcoin, et al, is their extreme volatility. When combined with the intense media coverage they attract, particularly when they are zooming up or down, the average speculator investor in them has a hard time resisting the urge to buy into meteoric rallies and then bail out during the inevitable terrifying plunges. However, the fact that Bitcoin has crashed repeatedly and come roaring back time-after-time indicates an inherent demand that is unlike any other bubble we've ever seen.

Which begs the question, will the next major crash be a buying opportunity for investors that have remained on the sidelines up to this point? While we continue to have concerns about the space overall, we do believe BTC will be a survivor (and perhaps even a thriver) in the crazily cryptic world of cryptos.

Why Investors Cannot Ignore Bitcoin Any More by Pedro de Noronha

All good investors and those who understand how markets work know that a market exists at the intersection of supply and demand. For Bitcoin, the price is a function of a network effect directly affected by its finite supply and growing demand. In this context - known as digital scarcity - Bitcoin can be seen (at the bare minimum) as the 21st century version of gold, known as the oldest and, to date, the soundest store of value.

Yet, Bitcoin has several superior characteristics to gold that makes it a much better store of value across both space and time:

Another major advantage of Bitcoin is that it invented for the first time in history absolute digital scarcity, the much-needed antidote to the irresponsible printing of paper money by Central Banks since 2009.

Fiat debasement in a degree never seen before in modern times has created a growing demand for scarcity, proving the need for an efficient and secure transfer of value across time and space with minimum leakage. Add to that a network that incentivizes participants to ensure the continued well-functioning of the network and you have Bitcoin, the soundest “Store of Value” asset ever created, available to everyone, from the wealthier cohort that own a significantly larger share of global wealth to the bottom who in many instances were first adopters of this technology that truly serves everyone.

After several years of work on Bitcoin, we believe that - worst case scenario - it will likely continue to grow as the alternative asset allocation to gold given its superior attributes, especially in the context of the continued growth of the digital world. Best case scenario, we are at the beginning of a new technological revolution, the biggest since the advent of the internet. And neither of these scenarios are currently being priced in by the market, which is why we are so bullish on this new asset class.

Right now, we could compare Bitcoin to the internet in the mid 1990’s, when few predicted how revolutionary that new technology was. We believe the same applies here, but this time Bitcoin is already the most widely held asset in human history to date and growing at twice the rate that the internet was when it was the same age.

We first heard about Bitcoin in 2013, around the time the man behind the ‘black market’ Silk Road website was arrested by the FBI. At the time we paid little attention to it as it was a tiny, fringe movement, and although we felt a certain kind of attraction to the idea of an asset beyond the existing financial system, and independent from government control, there was no practical way for us to get involved.

Fast forward to 2017 and the CME launched Bitcoin futures. Having studied bubbles for over two decades, we knew that the introduction of futures on Bitcoin had a very high likelihood of popping the bubble. This led us to short Bitcoin on the day that its futures were launched in December 2017, and over the next year rode the price down from just below $20,000 to around $5,000.

Our bearishness on the asset, and the fact that we held the position for over a year, forced us to continually try to understand what Bitcoin was, and what its potential could be, to stress test our short position on such a high volatility asset.

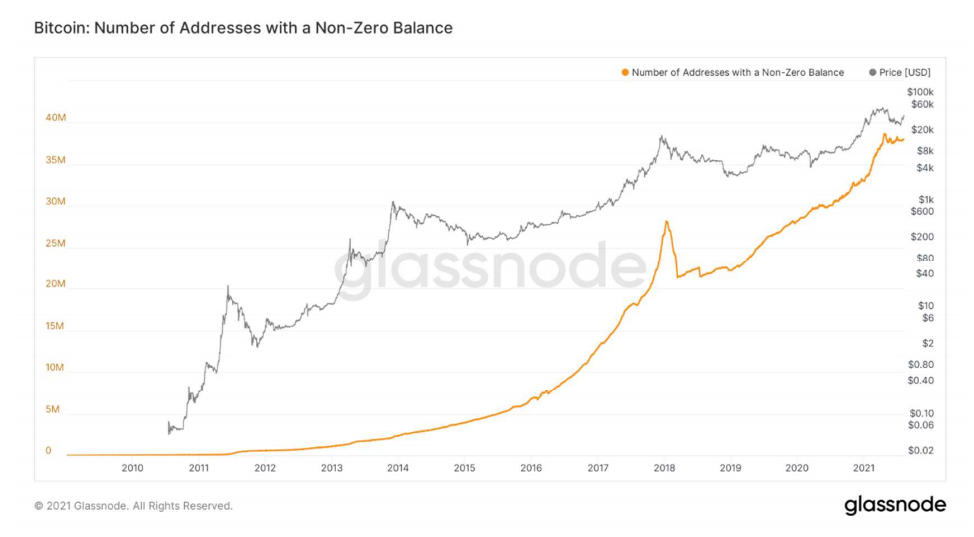

The more work we did, the more we learned. We witnessed that, whilst the price of the asset frequently went through cycles of peaks and troughs, the network itself kept on growing unequivocally since inception. Today – after only 12 years – Bitcoin is held by 114 million different people, making it the most widely held asset in history, and adding, on average, ca. 2 million new owners per week. This is not a fringe movement anymore.

We were welcomed to this universe of developers, entrepreneurs, economists, and former macro investors that were not only dedicating their time to this space, but also betting with increasing conviction on this new asset class. This includes some of the world’s largest investment banks, Hedge Funds, Public Corporations, Insurance Companies Sovereign and Pension funds, Ultra High Net Worth and High Net Worth individuals, private investors, and regular individuals. This all meant that, in late 2018, aware of the power of the network and that the digital world is without a doubt fertile ground for natural monopolies born from network effects, we closed our short position and quickly began building a long-term focused long position on Bitcoin (institutional and corporate players who are just now about to start a similar strategy). We understood (as they too are starting to realize as well) that Bitcoin is the most asymmetric risk/reward opportunity seen in our careers.

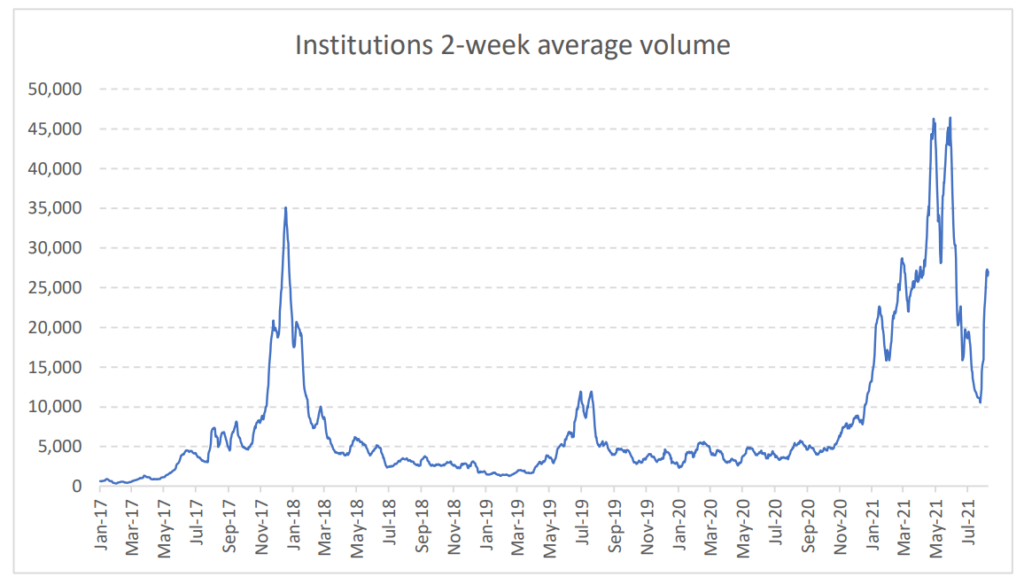

Whilst 6% of US households already have exposure to Bitcoin, the true case of validation of this past year has been seeing daily institutional traded volume growing 5x since late 2020 to $25 billion (peaked at $45 billion earlier this year) as can be seen on the chart above. We at Noster Capital are adamant that price gyrations are not based on a price target but rather based on the growth of the network ecosystem.

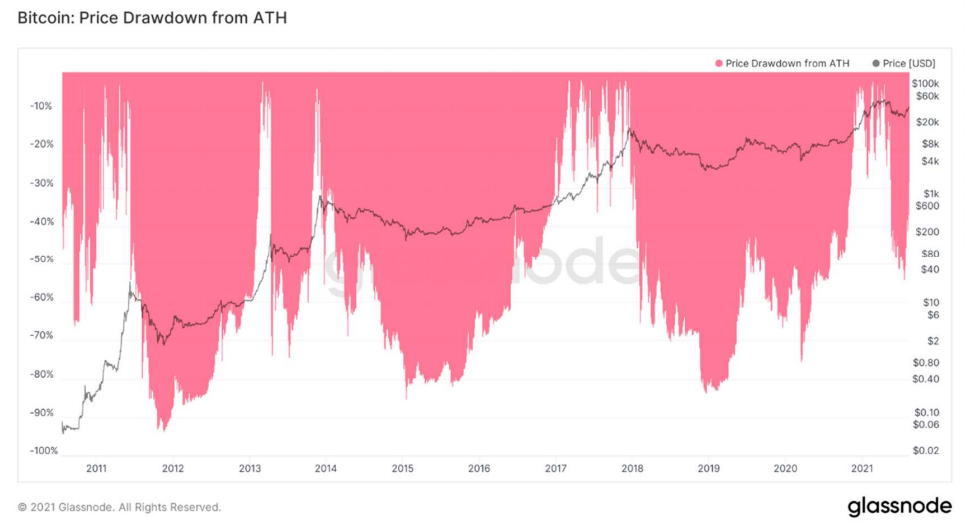

Bitcoin has returned 132% CAGR in the last 10 years. Despite that, it has entered a bear market approximately 20 times, and it has gone through three full bull and bear market cycles excluding this current cycle. Unaware of any other asset class that has been through such extreme price fluctuations and survived, it is way too simplistic to discount Bitcoin as a “bubble”, one-trick-pony or boom-and-bust such as the sometimes comparisons to the Tulip Mania, South Sea or Mississippi bubbles made my mainstream media and other outlets.

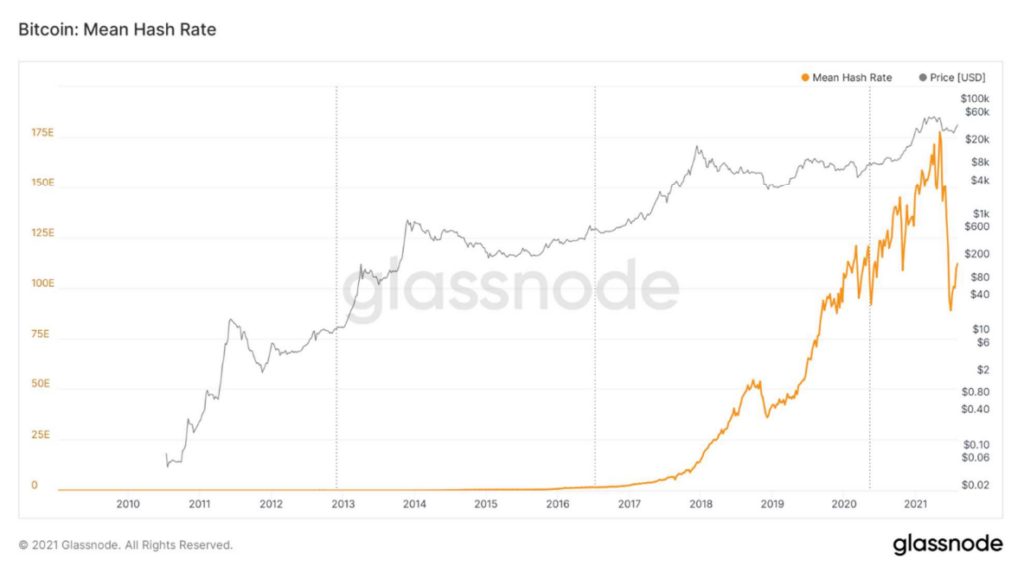

Visuals such as the below make it easy to see how adoption continues to move exponentially higher regardless of several 80%+ drops in price, where holders have held firm rather than jump off the Bitcoin train.

From 2009 to May 2021 the hash rate, which is the amount of computing power dedicated to the network, which directly translates into the level of security of the network itself, grew like a hockey stick with the recent drop due to China’s ban on Bitcoin mining operations, something we see as a medium and long term positive.

The NYSE trades $50bn-$75bn and the NASDAQ trades $100bn-$120bn per day. Currently trading at approximately $40 billion a day – Bitcoin is significantly past the stage where it can be considered a retail passion project of a few “out of the box” characters.

Price Cycles

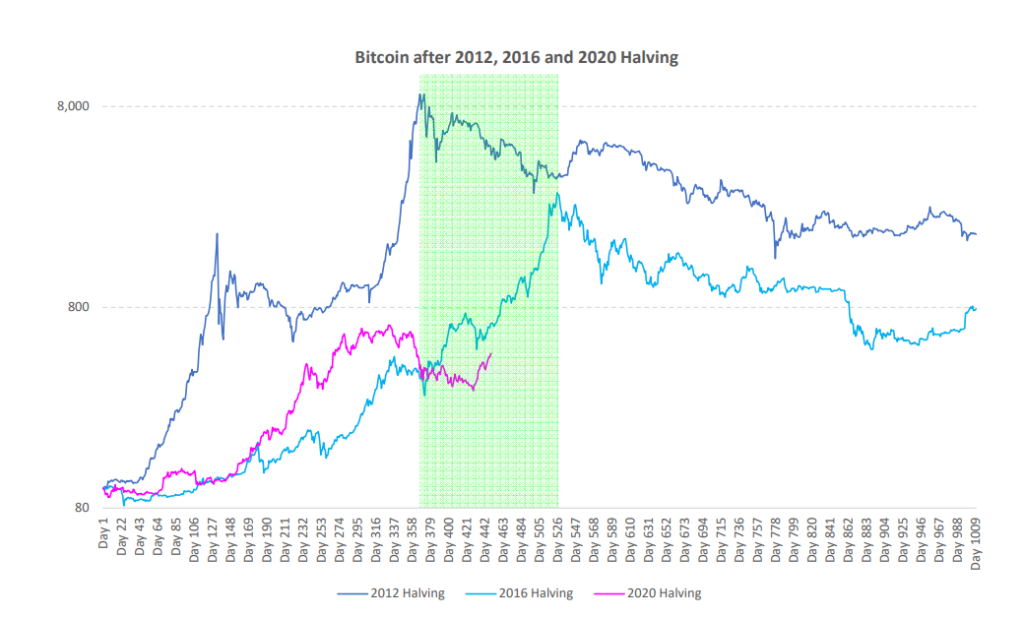

Bitcoin’s protocol implies that every 210,000 blocks (broadly, every four years), the amount of new supply that reaches the market halves. This implies that the natural inflation rate of Bitcoin is naturally cut in half every four years, with that number being currently at under 2%. The next halving cycle in 2024 will make Bitcoin's inflation rate lower than golds.

Based on a 12-year history and three halvings, we have a comprehensive idea of its market cycles sees exponential rises in price after each halving event. Last seen in May 2020, we seem to continue to be broadly in trend, implying significant upside to Bitcoin prices in the next 3 to 6 months as depicted on the green box below.

Bitcoin’s ESG concerns

Bitcoin is based on “proof of work” mechanism that requires large amounts of computing power to ensure the security of the network. The larger the network becomes, the higher the amount of computing power needed to keep it secure, the more electricity is required to run it. In order to support the protocol that makes any “hack” or fraudulent transaction virtually impossible, electricity must be consumed – that’s the trade-off.

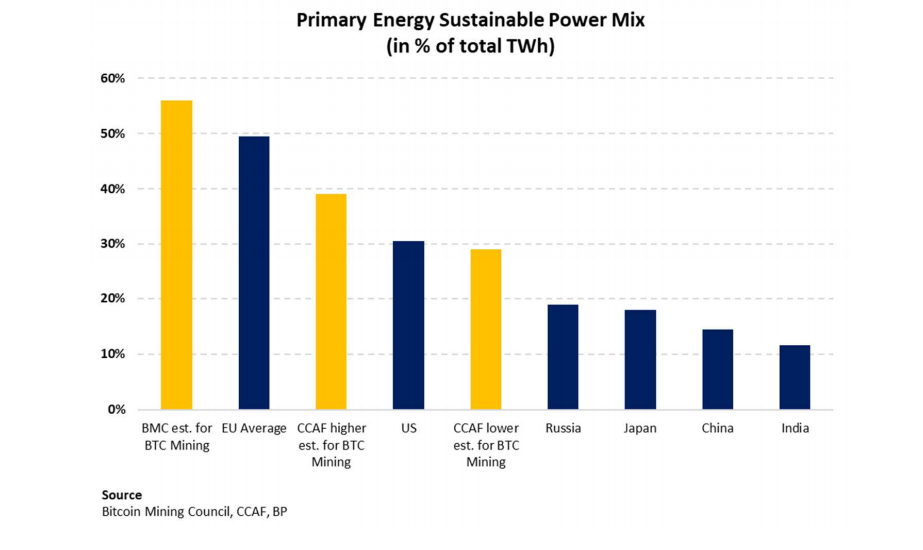

In a world increasingly concerned with ‘ESG’ principles, this electricity consumption has been the source of much controversy. Research by the CCAF at Cambridge University suggests that 29% to 39% of mining’s total energy consumption comes from renewable sources, whereas the recently formed Bitcoin Mining Council estimates this number to be 56%.

As with all other industries, Bitcoin mining will continue on trend to shift to greener energy either as miners are incentivized or pushed to do so by regulation, or by finding opportunities in using stranded energy in remote locations - that is because mining infrastructure can be set up in remote locations that have large electricity generation potential (i.e. hydro, geothermal or solar energy) that can be difficult to deliver or distribute to grids or direct to end-users.

We are already seeing plenty of examples of this happening from Iceland and soon El Salvador (which just legalized Bitcoin as legal tender, on par with the USD) to Bitcoin mining facilities in oil fields in Texas where methane gas flared to the atmosphere is now being used to mine for Bitcoin (this replaces methane emissions with carbon dioxide), which reduces its environmental damage by 97.5%.

The team at Noster Capital fundamentally believes that ESG worries are overstated and significantly misinformed as we consistently see scenarios that incentivize miners to innovate and adjust their energy mix profile. Will the day soon come when we can have the interesting argument about Bitcoin getting its share of carbon budgets? We believe that Bitcoin could become the ultimate ESG asset.

Regulatory action is a mid-term positive, and long-term proof of validation

Often leading people to strongly negative conclusions about Bitcoin is the misinformed idea that regulatory entities tend to take a hostile stance towards cryptocurrencies, leading to a logical high level of uncertainty about future regulation.

Since 2021, Bitcoin has experienced some level of regulatory scrutiny. Regulation has and is gradually maturing, with the FinCEN, IRS, CFTC and SEC all coming together to try and form a harmonized regulatory framework for this new asset class. A process has taken some time mainly due to:

We expect the regulatory framework to continue to tighten going forward. However, we see this regulatory action as a mid-term positive as a serious and well-reasoned framework that clears out bad actors could pave the way for institutional players increased adoption rates, driving demand significantly higher whilst supply remains mathematically capped, supporting the supply and demand unbalanced reality of the Bitcoin market.

What you’ll hear people say about Bitcoin

Conclusion

We see bitcoin as one of the most important financial developments of the last 20 years, and - consequently - an incredibly important social development. To be a participant in today’s financial markets one should have a certain understanding of bitcoin, its base layer technology and opportunity.

We believe that bitcoin is an incredibly attractive investment opportunity by itself, given its unique characteristics: the way it allows for value to be stored throughout time and across space, the magnitude of inflows it will likely see in the coming years as fears of inflation pick-up, the overall infrastructure developments around the asset, which will continue to make capital allocation easier, safer and more efficient, and the daily growth in adoption regardless of price fluctuations or negative media. With equities at all-time highs and valuations being fully detached from any fundamental drivers, and Governments and Corporations issuing bonds that are not compensating investors with high enough yields whilst being debased, Bitcoin is the solution to many of the modern investor’s capital allocation problems.

Pedro de Noronha

pedro@nostercapital.com

Twitter: @NosterCapital

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.