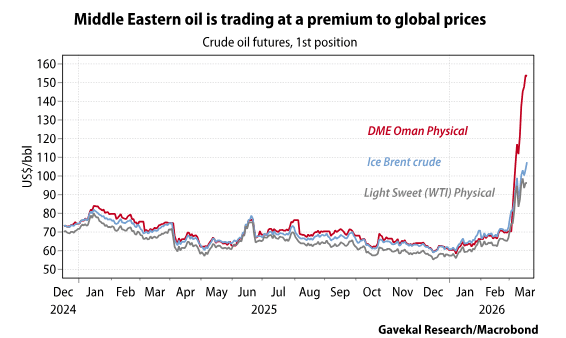

Most of the financial reporting on the Strait of Hormuz closure has focused on oil. There are obvious reasons for this, starting with the fact that economic activity, as we never tire of saying, is simply “energy transformed”. Looking back through post-World War II history, one can find many examples of oil price spikes derailing equity bull markets and/or economic expansions. It is therefore understandable that financial market participants concentrate disproportionately on oil, especially as prices have, over the past few trading sessions, started to show major dislocations. Middle Eastern benchmarks such as Dubai and Oman are now trading above US$150 a barrel, while Brent and WTI remain around US$100/bbl, an unprecedented divergence.

That said, oil may not be the biggest single issue emerging from the Strait of Hormuz closure. First, oil may still find ways out of the Middle East through alternative routes. The dollar amounts involved are large enough that it can make sense for boat captains to pay Islamic Revolutionary Guard Corps commanders to guarantee safe passage for the odd vessel (something that is already happening). At the same time, around 7mn barrels can still be transported by pipeline to Saudi Arabia’s west coast, provided the pipeline itself is not targeted. Unfortunately, it cannot be much more given that the Saudi port on the Red Sea is already operating close to full capacity. Otherwise, oil can also be loaded onto trucks and transported through Iraq and into Turkey, from where it can be exported onward.

But essentially, if the IRGC is letting Iran’s own oil through—the war has to be funded—and allowing vessels bound for China, India and Pakistan to pass, then the overall oil situation may work itself out. If the remaining flows can move via the Red Sea, provided the Houthis do not start blocking this route, or by truck and pipeline to Turkey, an enormous catastrophe may yet be avoided.

Admittedly, there are a lot of “ifs” in that paragraph, and the above Band-Aids may provide near-term relief but do not constitute an agreeable long-term solution. More importantly, the bigger supply chain dislocations linked to the Iran war may not be oil, but natural gas. Qatar alone accounts for roughly a fifth of global exports, and shipments since the war started have drawn to a standstill.

Sulfuric acid is another key pinch point. Sulfuric acid is necessary for the processing of many metals, not least copper, and roughly half of annual seaborne supply transits through the Strait of Hormuz. Fertilizer flows are also at risk, with roughly a third of global supply transiting through the strait. In short, the consequences of the closure go far beyond the oil market.

With that in mind, and assuming that a near-term solution is not brokered, which given the breakdown in the Iranian leadership seems unlikely, it probably makes sense to establish a list of the more obvious winners and losers from the unfolding conflict.

Likely winners from a continuation of the war

Non-Middle Eastern oil producers. That one seems fairly obvious, but producing oil in Brazil, Colombia, Australia, Canada, the US and China now looks like a better business than it did a few weeks ago, in both relative and absolute terms.

Fertilizer producers with access to cheap hydrocarbons. Again, fairly obvious. The share prices of companies such as Nutrien and CF Industries have gone parabolic since the start of the conflict. This makes sense. The longer the strait stays closed, the stronger these companies’ pricing power.

Coal producers. With Europe, South Korea, Taiwan and Japan no longer supplied with cheap natural gas, the default response will likely be to turn back to coal. This should support seaborne prices. In recent years these have been depressed by the China slowdown and rising Mongolian production (which has led China to buy less coal from Australia and Indonesia).

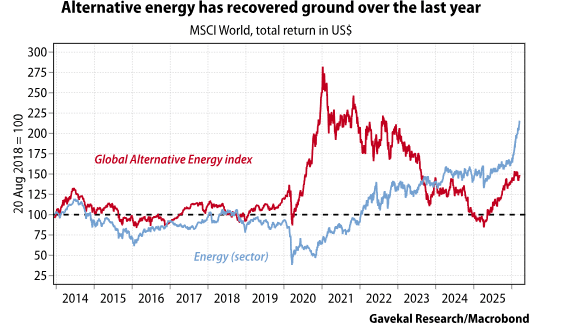

Alternative energy. The sector has been a dog. The “crocodile mouth” we highlighted in the summer of 2020 has now well and truly closed. The sector is either loathed or ignored. Still, it has been quietly building momentum since bottoming a year ago (see chart below). More importantly, with rising geopolitical uncertainty, government subsidies are likely to start flowing toward wind and solar again, not out of a desire to be green, but to achieve energy independence.

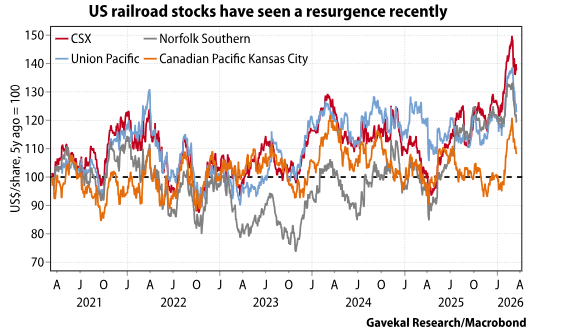

Railroads. If, as seems likely, the near-term energy squeeze intensifies and the Band-Aid solution is greater use of coal, then this should benefit railroads tasked with moving that coal around. As it stands, railroad stocks have spent most of the past five years consolidating, though they have come alive over the past 12 months.

Commodity producers in general. Following the removal of Nicolás Maduro in Venezuela, the argument we made was that a more uncertain US foreign policy would encourage countries to move away from stockpiling US treasuries and gold, and instead begin stockpiling whichever commodities they import. Needless to say, the Iran war only amplifies this shift from “just in time” to “just in case”.

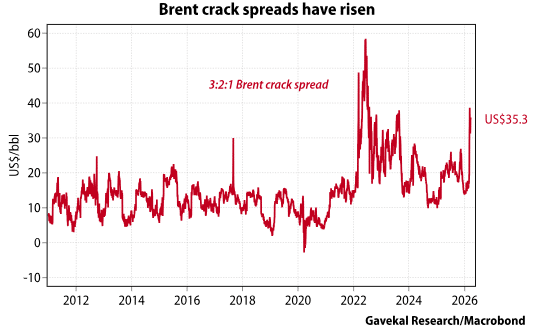

Refiners. Russia and Ukraine were already targeting each other’s refineries. If Middle Eastern countries now follow suit, then crack spreads are likely to remain elevated for the foreseeable future.

Banks. This one is more uncertain and, for now, the market is not pointing in that direction. However, if everyone, from nations to companies, now needs to stockpile more of everything, then someone will have to fund this inventory build. As it turns out, financing inventories is a fairly straightforward and lucrative business for banks. Still, it has to be said that, since the war started, bank share prices have been disappointing, and we seem to be rapidly approaching an important test of the 200-day moving average.

Likely Losers from a Continuation of the War

Obviously, the biggest losers in any conflict are the people caught on the wrong end of missiles, bombs and bullets. In this case, that means the 90mn Iranians, 10mn Israelis and 60mn residents of the six Gulf Cooperation Council countries. These are the people enduring property destruction, the loss of friends and family, and deep uncertainty about the future. The human toll is real. That is 160mn people caught in a terrible crossfire, roughly equivalent to the combined population of Germany, Benelux, France and the United Kingdom in 1940. Beyond the human toll, other likely victims include:

Government bonds. Wars are inflationary. They typically lead to wider budget deficits, capital destruction and unproductive spending. This is why our friend Luke Gromen likes to say that “if truth is the first casualty in war, bonds are usually a close second.”

Countries dependent on Saudi and UAE largesse. Egypt obviously comes to mind, as do Pakistan and Lebanon. These are countries that, in the not-so-distant past, received direct handouts or investments from the United Arab Emirates and Saudi Arabia to keep their economies on track. However, charity begins at home, and the days of large external checks may be put on hold for a while.

Farmers, especially in Europe. Yes, wheat, corn and soybean prices are moving higher, but so are fertilizer costs and diesel prices. Unfortunately, diesel and fertilizer are likely to rise far more in Europe than in the Americas or Russia. Western European farmers will likely get squeezed, which means that by next autumn tractors will likely be blockading the Champs-Élysées and the M25.

Luxury goods. The Middle East has long been an important market for luxury goods manufacturers, so the fact that tourists are no longer flocking to Dubai’s malls is not great news. Combine this with the squeeze on disposable incomes from higher energy and food prices, and renewed yen weakness, with Japan another key market, and it is hard to be too enthusiastic about the sector’s prospects.

Airlines/tourism. Airlines are already canceling less profitable routes because of soaring jet fuel costs. At the same time, rising food and energy prices will likely squeeze lower-end consumers, who may respond by cutting out that holiday to Majorca, Las Vegas or Phuket...

Drilling and oil service companies. Normally, soaring oil prices are good news for oil service firms. But today’s move reflects a supply shock rather than stronger demand. As such, energy companies are likely to keep capital spending in check, should the situation in Iran improve and oil prices retreat.

Gold. Arguably, gold should perform well in periods of rising geopolitical tension. Yet, interestingly, it has gone nowhere in recent weeks. This may reflect concerns that Middle Eastern countries could sell part of the gold accumulated in recent years to meet rising expenditures. Alternatively, countries may now recycle excess reserves directly into the commodities they need, such as oil, fertilizer and copper, rather than into the yellow metal.

Utilities. As the price of natural gas, coal and oil shoots higher, the question is whether utilities will be able to pass these cost increases on to end consumers, or whether political pressure will force them to absorb the hit to margins.

Semiconductors. The sector has had an amazing run, but the level of uncertainty has now jumped a notch. First, there are concerns around access to helium. Second, and more importantly, there are growing doubts about the construction of the massive data centers that were supposed to come online in Saudi Arabia, the UAE and Qatar...

Weapons manufacturers. It has been a recurrent theme of our research. Recent conflicts seen in Armenia, Ethiopia, Ukraine and Yemen have highlighted just how much warfare has changed. Simply put, the math of sending US$1mn interceptors against US$30,000 drones does not work. Nor does the math of deploying aircraft carriers that cost billions of dollars but must now remain hundreds of miles away from combat zones to avoid drone attacks. As Joseph Stalin reportedly said, “In warfare, quantity has a quality all its own.” Put differently, owning hundreds of thousands of cheap drones may make more sense than relying on a small number of very expensive, highly efficient fighter jets.

Legacy currencies. This war helps neither Japan, which is stuck with a much higher energy bill when inflation is already too high, nor Europe, which faces the same challenge alongside the loss of key markets, nor the US, where there is a risk that Saudi Arabia, the UAE and Qatar start repatriating funds by selling assets to meet short-term needs. One can thus make cogent bearish arguments for the yen, the euro and the US dollar. The simpler conclusion may be to seek refuge in other currencies. That could mean a stable renminbi, which the Chinese leadership seems keen to push higher, or undervalued commodity currencies such as the Australian dollar or Canadian dollar, which should benefit from higher materials prices. Alternatively, investors may look to high-yielding currencies such as the Brazilian real or South African rand.

Conclusion

The above lists are not exhaustive, and the situation remains fluid. Still, assuming the war drags on, reducing exposure to the “losers” and increasing weightings in the “winners” makes sense. All the while remembering that, as money managers, we are not paid to forecast (especially not political developments in the Middle East) but to adapt.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.