"History has not dealt kindly with the aftermath of protracted periods of low risk premiums."

-Former Fed Chairman ALAN GREENSPAN (low risk premiums equate to high market prices)

At the end of 2017, we initiated a new EVA series titled “Bubble Watch” where we went as far as to postulate that we’re in the midst of the Biggest Bubble Ever (BBE). It was in that EVA that we pointed to cryptocurrency-mania (e.g., Bitcoin) as a prime illustration of the euphoria intoxicating those attempting to turn a quick buck (the quintessential case of “speculating” rather than “investing”). Since the publication of that EVA, cryptocurrencies have plummeted back down to earth. Equity markets, on the other hand, have sputtered, but have not come off the rails by any means.

More recently, we published the first chapter of a new book I’m penning titled: “Bubble 3.0: How Central Banks Created the Next Financial Crisis.” It was in this missive that we outlined our position that the bubble presently building is strongly linked to years of coordinated global central bank efforts to pump money into the system while suppressing interest rates. This week, we will present the second chapter of that book, taking a closer look at how we got to our present predicament. This EVA will run in two parts; the second part being published next week.

BUBBLE 3.0: HOW DID WE GET HERE? (PART I)

Another logical starting point in the anatomy of Bubble 3.0 is to reflect back on how we arrived at our present situation of unprecedented central bank meddling involvement with financial markets. It’s also important to consider the uniqueness—and latent danger—in the reality that most developed country governments have utterly trashed their balance sheets over the last 10 years—despite a sputtering but long-lasting economic expansion. After a decade of extreme monetary measures, the likes of which the world has never seen, and sovereign debt levels at all-time highs, the solution set for policymakers to react to the next financial crisis and/or recession is perilously limited.

However, for now, let’s zero-in on what central banks have done in the last decade. (Ironically, zero is an apt word since that’s what short-term interest rates fell down to—or even lower—and stayed there for years; but more on that in a bit.) If I had been so imprudent as to have speculated back in 2007 that, over the upcoming decade, the Fed would resort to three separate rounds of “quantitative easing”—the antiseptically technical term our central bank conjured up to obscure that it was, in fact, printing money*—my readers would have reasonably concluded I had lost it totally. (This is a suspicion I know many have right now, as they read the start of this book.)

It would further have strained my credibility to the laughing point if I had said the Fed would be joined in their radical mission by most other “rich” world central banks. As mentioned in the introduction to Chapter 1, in the April 27, 2018 EVA, the most remarkable of these efforts might be what the tiny—yet, symbolically important—Swiss National Bank has done in recent years. Their tactics are also significant in that they reveal a mostly covert reason why central banks have been engaged in long-running emergency monetary policies that really should only be activated, and maintained, in the midst of a global depression and/or severe financial crisis.

The Swiss National Bank (SNB) certainly didn’t have the high responsibility level of its far larger peers like the Fed or the European Central Bank (ECB). Nor was it trying to prevent a collapse of its national banking system. And its tiny but resilient economy was in no danger of doing a reprise of the Great Depression, unlike the US and the rest of Europe during the bleak and terrifying days of 2009.

Instead, it had one objective: to prevent the Swiss franc from rising to astronomical heights as the ECB--under Mario “whatever it takes” Draghi--slashed interest rates to zero, and then below, putting significant downward pressure on the euro. Consequently, to keep the lid on the Swiss franc, in order to protect its impressive list of multinational exporters from being priced out of global markets, the SNB resorted to its own shockingly loose monetary policies.

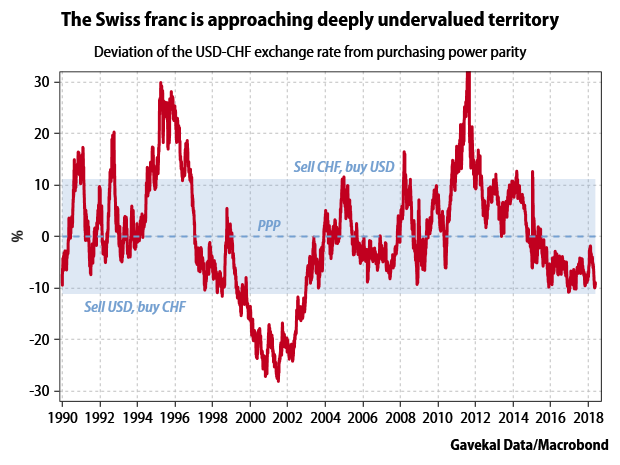

This included fabricating $50 billion from its own digital printing presses and using that sum to buy US stocks. As a result, the SNB has become one of the largest holders of iconic US growth stocks such as Amazon, Facebook and Google. Per the below chart, you can see that the SNB managed to suppress its currency quite effectively, as it also forced interest rates down to -.75% notwithstanding an economy growing slowly but steadily (also, Switzerland avoided the double-dip recession the rest of Europe suffered after the financial crisis). In fact, despite huge trade surpluses, the Swiss franc (or Swissie, as it is affectionately known) is now undervalued, a condition it rarely attains.

*At least thus far, the major central banks have refrained from actually printing currency as Germany’s Weimar Republic infamously did in the 1920s; rather, they have created digital reserves out of nothing but their computers. Those reserves have then been transferred to the banking system, typically in return for government bonds.

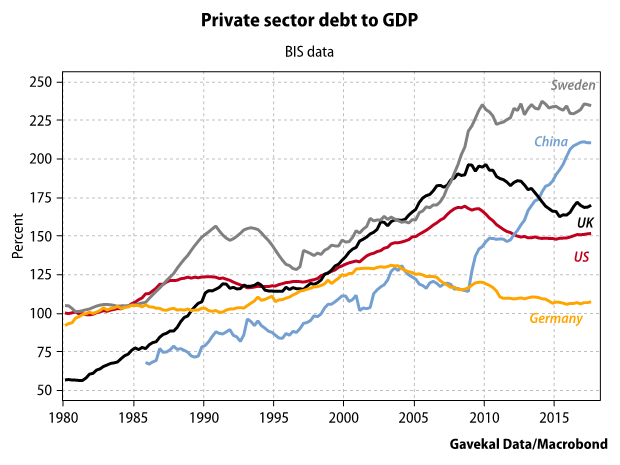

This same phenomenon has been unfolding in another smallish European nation that also possesses its own currency: Sweden. Commendably, the Swedish central bank has not whipped up tens of billions to speculate in US stocks but it has crushed interest rates into the negative zone (meaning borrowers are paid to take out loans, a condition that, once again, would likely have gotten me committed to an institution where the sportscoats “button” in the back had I suggested it as a possibility 10 years ago).

Even as the Swedish economy has been growing at a healthy clip of 2.8% per year since 2012, its central bank (the Sveriges Riksbank, for you financial nerds) has maintained rates, once again, at levels that should be reserved for disaster conditions. Why? To paraphrase Bill Clinton’s former chief strategist, James Carville, “it’s the currency, stupid!”.

Source: Bloomberg, Evergreen Gavekal (2015-2018)

Source: Bloomberg, Evergreen Gavekal (2015-2018)

Like the SNB, the Swedish central bank was worried its exporters would be crippled if its currency was allowed to soar against a euro that the ECB was trying so hard to depreciate. As with the SNB, it succeeded but, in what I expect to be THE question of the next decade, at what cost? (Much more on this to follow in a future chapter tentatively titled “What Price Prosperity?”)

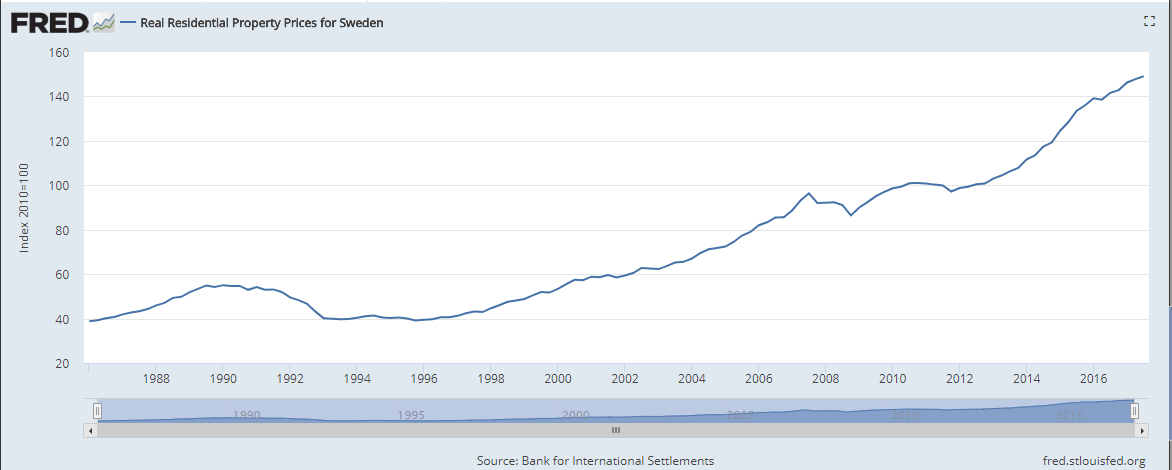

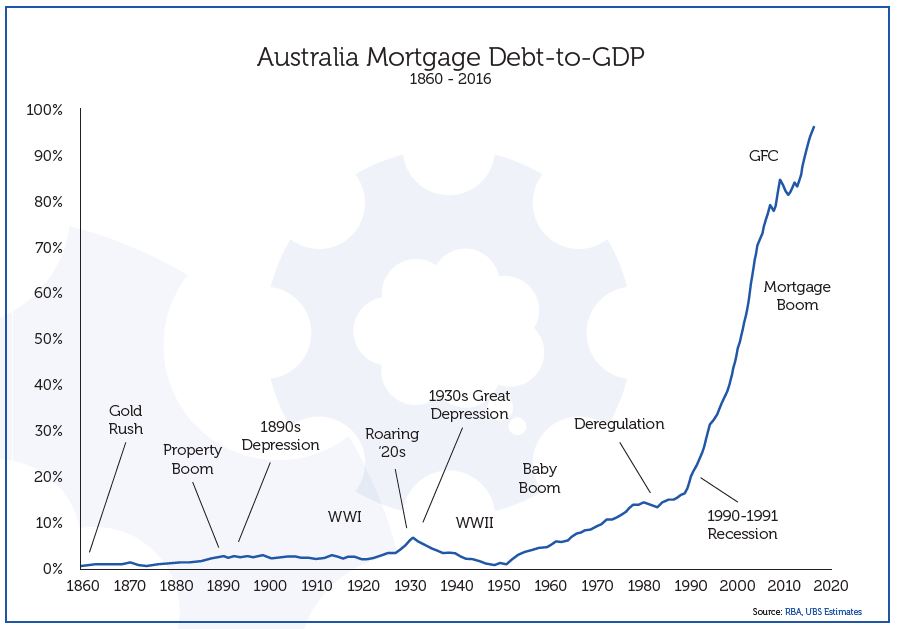

Despite the fact that Sweden was nearly bankrupted by a massive housing boom-cum-bust in the early 1990s, its recent experiment with zero to negative interest rates during a robust economic phase has created a housing bubble that puts the earlier one to shame.

As a result of this latest housing mania, Sweden’s financial vulnerability is more acute than it was even leading up to the early 1990s bust.

The early 1990s housing bust was so severe that it caused the Swedish government to nationalize all of its banks, at a cost of about 4% of GDP. In the process, it guaranteed and protected all deposits in return for complete ownership of its banking system. (In a sneak preview of what happened in the US with the Troubled Asset Relief Program—TARP—Sweden’s policymakers took equity positions in their banks; eventually, it sold these stakes for an amount that repaid half of its outlays. As many readers know, the US Treasury realized a substantial gain on its TARP investments, validating one of the wildest forecasts this newsletter has ever made, back in 2009.)

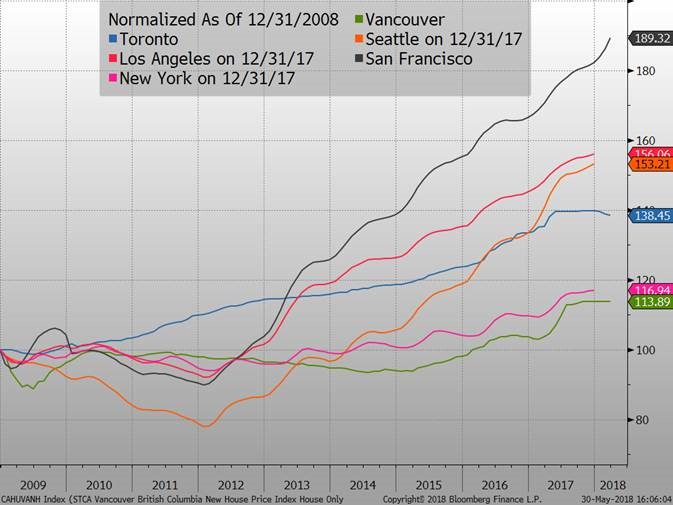

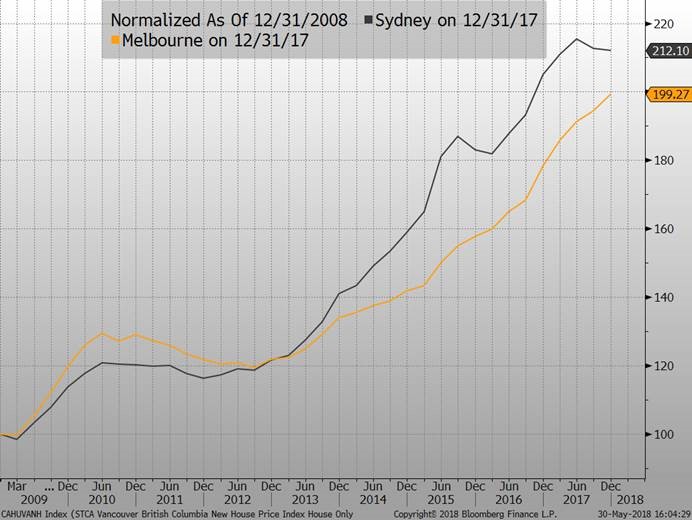

Key to the central thesis of this book, Sweden is far from alone. In most of the major metropolitan areas of the planet’s leading economies, housing prices have done moon-shots. If the last housing bubble soared into the stratosphere, this one has made it all the way to the ionosphere--if not the exosphere.

Source: Bloomberg, Evergreen Gavekal (as of May 30, 2018)

Source: Bloomberg, Evergreen Gavekal (as of May 30, 2018)

As far as the last chart on home prices in Sydney and Melbourne, please check out the gem below from my close friend Grant Williams. If that doesn’t scream “bubble to the max”, you may want to have your hearing checked!

But let’s return to the US and how our earlier housing bubble came onto being. Though some no doubt challenge the linkage (often those who continually deny the existence of bubbles in the first place), the evidence is strong that the speculative frenzy around tech stocks in the late 1990s initiated the chain reaction that would ultimately lead to the now-infamous housing explosion and implosion.

With the passage of nearly 20 years, memories are quickly fading of how traumatic that cycle truly was. Arguably, it began with the initial public offering (IPO) of Netscape in 1995. The spectacular success of the search-engine pioneer’s public debut began what would become, over the ensuing five years, the most intoxicating run of new issues in the history of the financial markets.

The seemingly insatiable appetite for IPOs from 1996 until early 2000 (with a brief hiatus caused by the 1998 Asian Crisis), set off an extraordinary sequence. As Wall Street was increasingly bestowing breathtakingly lofty valuations upon companies that were going public—in some cases, with little more than a business plan—tech entrepreneurs and venture capital investors were incentivized to an unprecedented degree to create and fund start-ups. This allure, combined with the legitimate break-through nature of the internet, proved an irresistible temptation for investors. And, of course, Wall Street underwriters, always in search of big fees, were only too happy to satisfy these cravings.

As more companies went public and saw their prices rise vertiginously, venture capital (VC) investors were emboldened like never before. Private placement memorandums (PPMs) and executive summaries—the essential documents of raising capital for start-ups—began circulating in Silicon Valley and Seattle, the dual hot-beds of tech innovation, like illicit drugs at a Hollywood party.

Unquestionably, most of these failed without making it to the going-public stage (and the bulk of those would eventually flame out during the great tech bust). But enough made it to the NASDAQ to pour napalm on the speculative flames of entrepreneurs and investors alike. The term internet millionaire—and, often, billionaire—entered the popular lexicon.

Before long, the most intense stock market boom in 70 years—since the giddiest years of the Roaring Twenties—was working its way to a feverish crescendo. While the majority of the companies that would become associated with the tech bubble—such as Netscape, Cisco, VMware, and EMC--hailed from California’s Bay Area, the most dominant of all, as it would turn out, came from the greater Seattle area.

It is with great embarrassment that I will now relay a story that has become the stuff of legends in my family. In November of 1995 one of my close friends called me about investing in an internet start-up. Over the years prior to this, I had invested repeatedly side-by-side with this individual, typically on a no-questions-asked basis. We were, at that stage, almost virtual partners.

Right before Thanksgiving of that year, as I was rushing to get out of town with my young family for a ski trip, he had called to tell me of a presentation by a 30-something tech innovator that had blown him away. When I asked what they did, he told me their uncomplicated business plan. Unlike with most tech companies I’d heard about, which were doing things I could only dimly understand, this one was so simple and obvious that I remarked: “But can’t anyone do that?”

After listening to him some more, I took my criticism to the next level by invoking Warren Buffett: “Where’s their moat?”. In other words, I couldn’t figure out their competitive advantage. It seemed to me that their much larger and well-established competitors could easily replicate what they were attempting and rapidly drive them out of business. My friend agreed with me but at the end of our conversation, when I said that I would think about the deal on my trip, he ended with this: “I get your points but the CEO is really, REALLY smart.” He added that he was investing $50,000—a sizable sum back then to put into something as risky as this venture.

Now, my pal had heard a lot of pitches in his career and he was the furthest thing from a pushover to a dreamer with a sexy story so his words stuck with me—to this day. But between Thanksgiving and the usual year-end craziness of being a portfolio manager, plus all of the upcoming Holiday activities, I forgot about our call for a month or two. In the new year, early 1996, I thought about it periodically and fleetingly, but figured that, given the astronomical odds they faced, they’d be coming back for more money—and probably at a lower offering price (known in the venture capital, or VC, game as a “down-round”).

To say that I made a miscalculation was a massive understatement. In May of 1996, my friend called me again asking me if I remembered our chat six months earlier. The sharp pain in my gut told me I knew what was coming—or so I thought. What he was about to tell me rendered my apprehension reaction a shadow of what it should have been—the tiny company he’d invested in mere months earlier had already attracted a multi-million dollar “up-round” (i.e., they paid a higher, not lower, price) from one of Silicon Valley’s most prestigious VC firms, Kleiner Perkins. But the worst news, at least for me, was coming: Wall Street was already interested in taking this entity public. Less than a year earlier it had been headquartered in the garage of a 1950s era house in a Seattle suburb, not far from where I lived. Now it was poised to realize the oft-dreamed of, and rarely attained, mega-payday (at least for early-stage investors) of an IPO.

In case you haven’t figured out which Seattle-based internet star I’m referring to, it’s the one that, when it comes to its increasingly besieged competitors, plays by jungle rules...as in Amazon jungle rules. Yes, I whiffed on the chance to be a first-round investor in the mighty AMZN. It was no big deal--it only cost me about a billion.

As the 1990s wound down, the tech sector wound up to a dizzyingly frenetic pace. While Netscape and Amazon were in the vanguard, scores of other internet companies followed close behind. Conditions had become feverish enough, as early as 1996, for then-Fed chairman Alan Greenspan to famously warn of “irrational exuberance” in the stock market. As stock prices continued to rip higher over the next three years, the man known at the time as “The Maestro” for his deft handling of monetary policy and the economy had his first major brush with fallibility. However, rather than maintaining the courage of his convictions and becoming increasingly vocal about the escalating mania, he began to equivocate. Statements such as the following from his August, 1999, speech in Jackson Hole, as the tech bubble was in full inflation mode, reflected his new-found ambivalence. “To anticipate a bubble about to burst requires the forecast of a plunge in the prices of assets previously set by the judgments of millions of investors, many of whom are highly knowledgeable about the prospects for the specific companies that make up our broad stock price indexes.” With those words, the Maestro made it clear he didn’t understand how the allure of overnight profits could distort the judgment of even professional investors (the highly knowledgeable). By the time the tech tide went out, institutional portfolios were bloated with internet and other “new economy” stocks. In fact, even 50% of the S&P 500 was in tech and telecom issues on the eve of the big meltdown, graphically illustrating that the “judgement of millions of investors” wasn’t so judicious.

Much more seriously, despite the growing obviousness that the behavior of the NASDAQ was becoming eerily similar to the market action leading up to the 1929 crash, Mr. Greenspan failed to do what prior Fed chairmen had done during earlier frothy markets. Individuals like William McChesney Martin--who coined the pitch-perfect adage that the Fed needed to remove the punch bowl just when the party was warming up—had proactively intervened to prevent past bull markets from morphing into bubbles by raising margin requirements. Yet, not once did the Greenspan Fed do so, even as the NASDAQ proceeded to nearly quadruple AFTER the Maestro had warned of irrational exuberance.

In fairness, Mr. Greenspan, like many (including this author), was concerned about the potential for severely negative repercussions due to the Y2K computer conversion looming soon. This, combined with the late ‘90s Asian crisis that slammed markets globally—and triggered a particularly deep correction in many tech stocks—caused the Fed to actually cut rates in the fall of 1998. It also flooded the system with money during 1999 due to Y2K concerns, despite a booming US economy and a tech bubble that was distending to gargantuan proportions.

Yet, despite the Y2K issue, the Fed’s decision to relax monetary policy at a time of robust economic conditions and hyperventilating markets, clearly injected rocket fuel into the financial system. Its actions during the Asian crisis also reinforced the belief by market participants that the Fed’s new unspoken third mandate (along with maintaining low inflation and high employment, two conflicting goals that were already challenging enough) was asymmetrical. In English, this meant that investors now believed the Fed would step in during periods of market turbulence to support asset prices but would stand aside when they were rising--no matter how rapidly and excessively. Basically, with his 1999 Jackson Hole speech, Mr. Greenspan codified the Fed’s “see no bubble” policy. It was a mindset that would come back to haunt the Fed—and the planet at large—less than 10 years later.

(To be continued next week…)

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.