“We have nothing to fear but the notion that there is nothing to fear.”

-ED YARDENI, Noted economist and stock market strategist

“The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs.”

-WARREN BUFFETT

“It’s the swings of psychology that get people into the biggest trouble, especially since investors’ emotions invariably swing in the wrong direction at the wrong time.”

-HOWARD MARKS, Co-founder of money management giant, Oaktree

POINTS TO PONDER

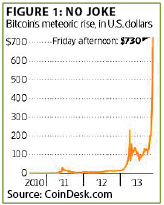

1. Although Fed officials seem unable to identify signs of speculative excess, units in the virtual currency bitcoin are up 5300% thus far in 2013. (See Figure 1)

2. Investors taking comfort in upbeat market forecasts by leading Wall Street strategists for 2014 should be aware that since 2000 this group collectively has never called for a down year, missing the four that occurred. Also, their average annual return forecast was 10%, versus the 3.3% that has actually been realized over the past 13 years.

3. Prior EVAs have noted how expensive the US stock market is on a price-to-sales basis. Societe Generale’s Albert Edwards observes that, based on this metric, the median stock is at an all-time high. Consequently, current valuations using this approach (which is not impacted by peaks and troughs in the earnings cycle) have exceeded even the dizzying heights seen in 2000.

4. Those who are positioning for an eventual sizable correction in US stocks may want to be aware of both the large premium for small companies compared to blue chip shares and also their performance in recent market plunges. Per the chart below, small- (and mid-)cap stocks were also richly valued, on a relative basis, prior to the 2008 bear market and the deep correction in 2011. Both of those episodes saw their excess P/Es largely eliminated. (See Figure 2)

5. The stock market has, at least for now, ignored the sharp rise by longer term interest rates since last June. Housing, however, is definitely feeling the pain. (See Figure 3)

6. America’s remarkable energy renaissance continues to defy skeptics. Texas’ venerable Permian Basin was viewed not long ago as in a state of perpetual decline. Yet, production has leaped from 850,000 barrels per day (bpd) in 2008 to 1.3 million currently. Estimates are that by 2018 it will be churning out 1.9 million bpd, roughly two-thirds of Iraq’s total national output.

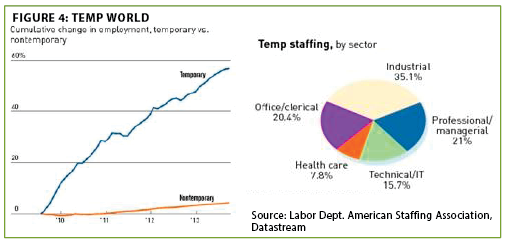

7. Typically, a surge in temporary worker hiring portends a coming acceleration in full-time job growth. As is the case with so many economic relationships during this “expansion,” the normal scenario isn’t playing out. The multi-year gap between temporary and non-temporary growth implies permanent changes, possibly caused by new factors such as Obamacare. Today’s jobs report, however, does to be solid and almost blemish-free. (See Figure 4)

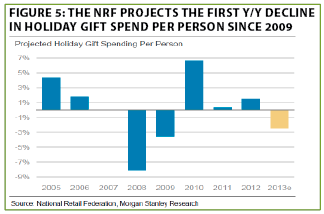

8. In yet another indication of the lackluster nature of the US economy, the National Retail Federation is forecasting the first year-over-year contraction in holiday sales since 2009. However, some of this weakness is due to Thanksgiving having fallen so late in November. It also appears consumers are spending more on big-ticket items like autos and home improvements versus consumer staples. (See Figure 5)

9. Each year since 2009 was supposed to be the break-out year for global growth, returning economic expansion to its normal trend line. Unfortunately, 2013 is turning out to be another year of underachievement. Moreover, the OECD (Organization for Economic Cooperation and Development) just reduced its 2014 forecast to 3.6% growth from 4% in May (note that this includes the effect from faster-growing emerging markets; developed nations are projected to grow at a rate just above “stall speed”).

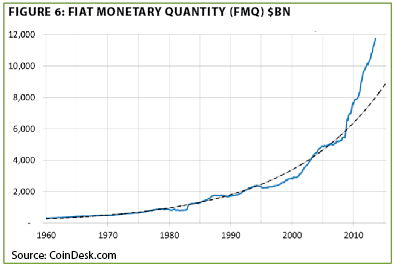

10. Since the bursting of the tech bubble, the US has created trillions of dollars of “fiat” money (i.e., backed merely by the US government’s promise to pay). Thus, it is hard to believe gold will continue to be so intensely out of favor. Additionally, like many other lagging asset classes in 2013, bullion currently may be experiencing acute tax-loss selling. (See Figure 6)

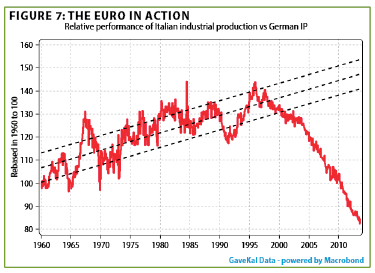

11. For years, GaveKal’s Charles Gave has been warning that the structure of the euro—too cheap for Germany and too expensive for Southern Europe—would crush industry in countries like Italy. Based on the evidence of the last decade, this certainly appears to have been an accurate prediction. (See Figure 7)

12. It looks as though Spain’s brutal two-year recession came to an end in the third quarter. Despite this good news, the risk of a European debt trap continues to escalate. The 17 members of the euro zone reported that debt as a percentage of GDP hit 93.4% in Q2, up from 90% a year earlier. Additionally, it appears that both the French and Italian economies are contracting again, raising the probability that their debt will continue to grow faster than GDP.

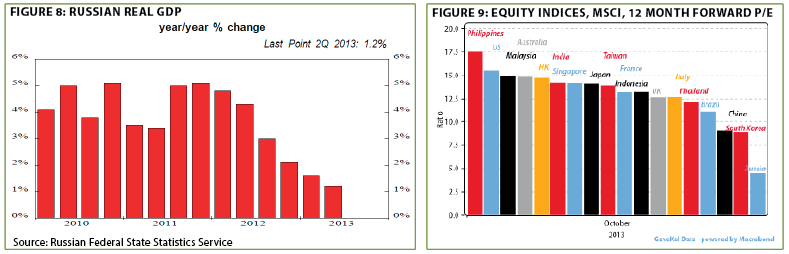

13. Russia is a member of the once-deified BRICs (Brazil, Russia, India, China). Like most of the other countries with which it shares that acronym, growth is heading in the wrong direction. However, the former USSR’s stock market is exceedingly inexpensive. (See Figures 8 and 9)

14. In another example of how comfortable investors currently are with high risk, the ultra-aggressive frontier markets, based in countries such as Pakistan and Nigeria, are outperforming those of lower risk nations such as China and Thailand by nearly 20% this year.

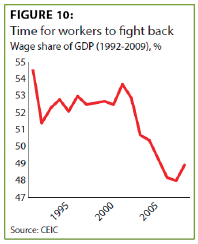

15. It’s not just US workers who have seen their share of the economic pie shrink. The same phenomenon has been true in China, though the latest data are showing some signs of improvement. (See Figure 10)

The every-which-way-but-down market. It was one of those strange thoughts I admittedly have more frequently than most people. In the middle of a conversation about the US stock market’s Teflon-like ability to effortlessly shed any concerns, a future Wall Street Journal headline suddenly hit me: “China Invades Japan; Dow Soars on Expectations of More Fed Easing.”

And although this mental flash was obviously just a figment of my often overactive imagination, it does at least lightly jingle the truth bell. From a statistical standpoint, it is stating the obvious to note the boa constrictor-tight correlation between the Fed’s money printing (more technically, reserve creation) and rising stocks. Yet, as esteemed money manager and PhD John Hussman observes, this may be due more to psychology than reality. His logic revolves around the fact that the Fed’s frantic easing in the wake of the bursting of both of the tech and housing bubbles did not prevent two of the worst bear markets in history.

Regardless, psychology is perhaps the single most powerful influence when it comes to the direction of asset prices. And, for the time being, the guiding belief among millions of investors, large and small, is that as long as the Fed is rivaling New Orleans as the Big Easy, stocks are going higher—almost irrespective of whatever calamity might occur.

One of the mistakes I made a year ago when I felt stocks were fully priced and likely to just tread water in 2013 was not being more vocal about an upside overshoot. By May, I started to entertain this possibility when I wrote these words: “What lies ahead, no one knows. However, I believe that one of two paths is likely: Either the Fed stays on its present path and we get 1987 revisited—with a bull becoming a bubble, followed by the big pop—or it tries to gracefully exit stage left, triggering a more immediate but much less painful ‘adjustment’. “

Since then, the market is up another 8% and although it would be a stretch to call this gradual ascent over six months anything approaching the hockey stick-like finale typical of a rampaging bull market, there are some disquieting elements. As previously noted, there are plenty of signs of speculative fervor run amok: the new nifty-fifty (Netflix, LinkedIn, Twitter, et al.), the biotech index at 170 times earnings, bitcoins engulfed in far more than a bit of a bubble, and the growing number of business plans masquerading as companies going public at astronomical valuations despite an absence of profits. (In fact, 60% of IPOs are losing money, a level not seen since 2000.)

Additionally, there are clear signs of recklessness returning to the credit markets to a degree strongly resembling the anything-goes lending attitude prevalent in 2007. Suffice it to say, pretty much anything, and everything, did go—as in down the tubes—shortly thereafter.

Yet, as all experienced investors are aware, markets can overshoot on both the up- and downside, often most dramatically. On this point, I read Jeremy Grantham’s latest comments with great interest. As avid EVA readers (all three of you) are aware, Mr. Grantham and the firm he co-founded, GMO, have one of the best, if not THE best, records of forecasting long-term returns for the major asset classes. However, despite his reputation for being a bit bearishly inclined and his firm’s long-range forecast of negative after-inflation returns from US stocks over the next seven years, he believes a further 20% to 30% spike by the S&P 500 is entirely possible.

For a moment, let’s just assume this “up-losion” plays out, as it easily could. That would be a wonderful thing, at least for investors who decide to jump in with both feet now, right? As they say in France, about almost everything, especially the appalling notion of a longer work week, au contraire!

When good is bad. Perhaps it’s just my oh-so-contrarian genetic disposition but I can’t imagine a worse scenario than US stocks going vertical from here. Such a surge would almost certainly accelerate what are already near record inflows into stocks (admittedly, after years of outflows). Retail investors are increasingly growing very restive about not having enough invested in US stocks, often even if they are holding an “age appropriate” level. Another upside bolt is likely to prove irresistible to the millions who still hold trillions in cash.

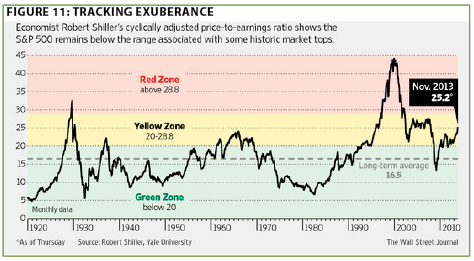

And, as those bulling stocks love to point out, valuations are not as egregiously elevated as they were in 2007, much less where they topped out in 2000. While this is technically true, given subsequent performance, it is also not especially comforting. Even the keeper of the cyclically adjusted P/E (CAPE), recent Nobel Prize recipient Robert Shiller, conceded in a Wall Street Journal interview last week that the overall market is not in the extreme danger zone yet, though it is clearly well above its long-term average. He did state, however, that another 20% rise would push equities decidedly into the bubbleshpere.

Of course, if that should happen, there will be even more pundits opining as to why those prices are rational, just as they did in 1999 and 2007. Meanwhile, those who have been warning of overvaluation, like a certain newsletter scribe in Bellevue, Washington, will become even more discredited and disdained.

Given the swelling throng of folks of a cautious persuasion conceding the likelihood of an “up-losion,” it’s possible the top isn’t that far away (even one erstwhile mega-bear, who hated stocks at the bottom in 2009, sees single-digit returns next year). I realize that when I bring up the idea of a pending peak, there are many who think: “Quit being such a killjoy! There’s nothing wrong with a runaway bull market. Nobody wants to see this thing end!” Unfortunately, history tells us that, when it involves stocks, too much good is definitely bad.

As I’ve observed previously, bubbles are like dying stars known in astronomy as red giants. They swell far beyond their original dimensions, but this immense growth is an unstable illusion of vapor and gases. Eventually they implode, becoming the dreaded black hole that sucks in anything within its gravitational field. Whatever goes into that abyss never comes out, much like the money invested in highly speculative securities during the terminal stages of an upside mania.

As usual, many asset classes are not “enjoying” extreme popularity and the resulting bubble-like pricing. US high-quality stocks are one example. They have badly lagged riskier issues for years (except in 2008) and look decent from a valuation standpoint. Yet, as we found out in 2000 to 2002 and 2008 to early 2009, when a bull turns into a bear, even most blue chips with reasonable valuations get thumped. The old saying is that when they raid the house of ill repute, everyone gets nabbed, even the piano player. But clearly, the most pain is likely to be suffered by the over-popular and, in some cases, over-leveraged areas.

On the latter score, if there’s an asset class that I believe will soon have its come-uppance—or, should I say, come-downance—the carry trade involving low-quality credits is close to the top of my list. When taper talk first surfaced in late May, the carry trade (borrowing short to invest longer term) in high-quality debt was clobbered. But it appears as though there was very little flushing of the carry trade with junk-type credits.

As Woody Brock pointed out in last week’s guest EVA, there has been a lot of game-playing going on with financial institutions stretching for yield. Even some at the Fed, typically oblivious to such things, at least until they blow up, are worried about the systemic risks posed by these low-grade carry trades and the “collateral transformation” that is apparently becoming widespread. (This attempt to magically convert low-quality debt into high-quality is ominously reminiscent of the alchemy of turning sub-prime mortgages into AAA-rated securities, circa 2005 and 2006).

Accordingly, there are several areas to clearly avoid right now, many of which are, unsurprisingly, the most popular. But let’s take a look, as we wrap up this week’s EVA, at where the risk/reward ratios look favorable.

Closed-end fun. In this week’s Barron’s, Jeff Gundlach, the pretender to the throne of King of Bonds Bill Gross, was interviewed. He was quoted to the effect that most investors are terrified of interest rate risk and, as a result, that’s where the opportunities lie. This is similar to a point I’ve been making in our internal research meetings that the consensus hates interest rate risk but loves credit risk. This broad conviction, combined with the lowest grade issues trading so rich, leads me to believe that the proper positioning for 2014 is the other way around.

While I have been far too cautious on the US stock market this year—assuming a rally and then a sharp decline, ending roughly flat—my worries about bonds from late 2012 have been vindicated. As in the stock market, high quality has badly lagged with longer term treasuries deeply in the red while the trashiest corners of the bond market have posted solid returns.

Consequently, closed-end funds that invest in higher rated yield securities have been pummeled. This pasting appears to be getting magnified by year-end tax selling since these are heavily owned by retail investors (who are also famously intolerant of losers, regardless of the income stream). True to our contrarian nature, we are stepping up our buying pace after nibbling a bit in this area during the summer swoon. We are capturing yields of 6% to 8% with such securities, and most of these are down 20% to 30% from where they were trading in mid-spring.

Interestingly, Jeff Gundlach also told Barron’s that he sees considerable value in dollar-denominated emerging market debt, which most US investors are seriously hating right now. Several closed-end funds that invest in this niche are selling at double-digit discounts to fair market value (aka net asset value) and the underlying debt is mostly investment-grade. Thus, it is possible to get better than junk bond returns without taking the credit risk. To us this is a no-brainer, allowing us to upgrade credit quality, including with investment grade US corporate and municipal bonds, essentially swapping credit risk for some interest rate risk. (As a related aside, AAA-rated five-year corporate debt in China is yielding 6.25% and in a currency that looks a lot stronger to the Evergreen team than the greenback.)

In my mind, depressed closed-end income funds, and their juicy yields, are likely to work regardless of whether the market goes parabolic or experiences a surprising (to the crowd) near-term correction. Should the “up-losion” scenario play out, these yield vehicles could fall further but, once the dying star turns into a black hole, their safety and cash flow should trigger a powerful rally. And, if a seasonally atypical correction occurs in the months ahead, they should begin outperforming sooner, though less impressively.

To reprise what I believe is an important point I made months ago (I do stumble on a few of those), the key in a bull market is not what you make, it’s what you keep. Past precedent is very clear that investors who try to keep up with a market that enters its going-postal phase won’t keep very much.

Far better to go where the action isn’t, lock down dependable cash flows in what is almost certain to continue to be a yield-starved world, and be prepared for the day when J.P. Morgan’s wise words are affirmed once again: Stocks will fluctuate. And careless investors, such as the individual pictured below, will painfully discover that the gyrations won’t always be to the upside.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.