Sometimes warnings do more harm than good. Back during the rock and roll phase of the late, great tech boom, various observers, including your humble EVA-author, repeatedly warned of a judgment day. Yet the NASDAQ just kept rolling. The innumerable premature warnings only seemed to embolden those entranced by tech’s seemingly endless ascent.

In the last year or so, much verbiage and energy has been expended, once again including yours truly, warning of the dangers of the housing market, particularly with regard to mortgage lending. As with tech, home prices managed to defy gravity much longer than would seem possible. Such is the nature of very powerful surges in price inflation and the credit expansion that facilitates them.

And, as was also the case with tech, the apparently misguided “buyer beware” advice appeared to confirm to the housing bulls that the little boys and girls crying wolf just didn’t get it. They seemed to forget that eventually with tech the wolf really was in the neighborhood.

Now that housing has clearly entered one of its swiftest and sharpest recessions, it would seem an odd time for me to focus on this area once again. After all, it would appear my concerns that it was destined to end in tears have been borne out.

The reality is the stock market has recently been acting like the clouds are parting. Additionally, there seems to be little focus on how housing and the very Byzantine world of derivatives might intersect in a disturbing way.

First of all, has the eye of the hurricane truly passed for housing? Based on 20 to 30% rallies over the last couple of months in the stock prices of the home builders, the market certainly seems to think that is the case. Also Alan Greenspan has been quoted as saying the worst is over for housing (no surprise on the Maestro’s part: he was blamed for the tech bubble and he doesn’t want another major meltdown to blemish his legacy).

I beg to differ. The recent home building stock recovery reminds me of several of the vigorous NASDAQ rallies that occurred back in 2000 and 2001 in the midst of that staggering 75% decline. (Yes, for those who have mercifully forgotten, the NASDAQ really did surrender threequarters of its total value from intoxicating peak to nauseating trough.)

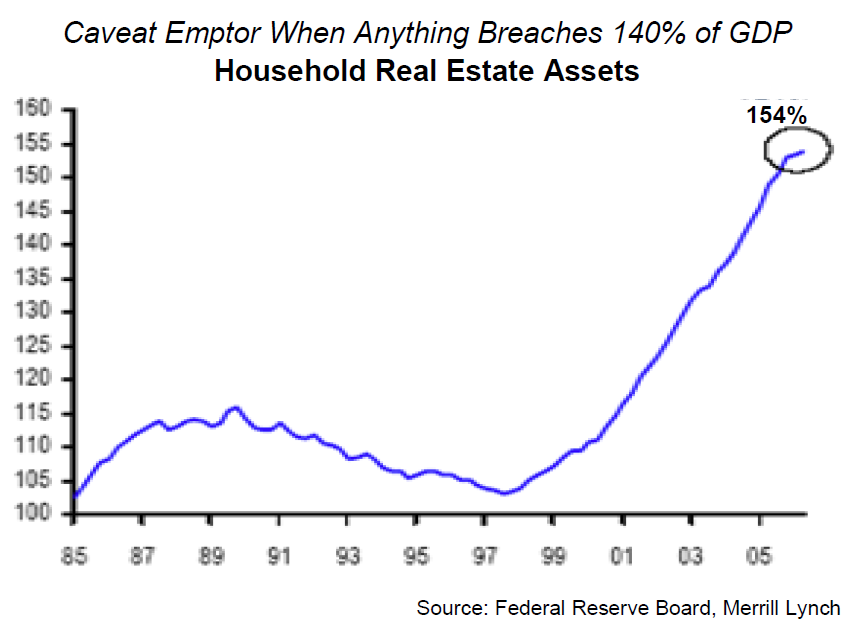

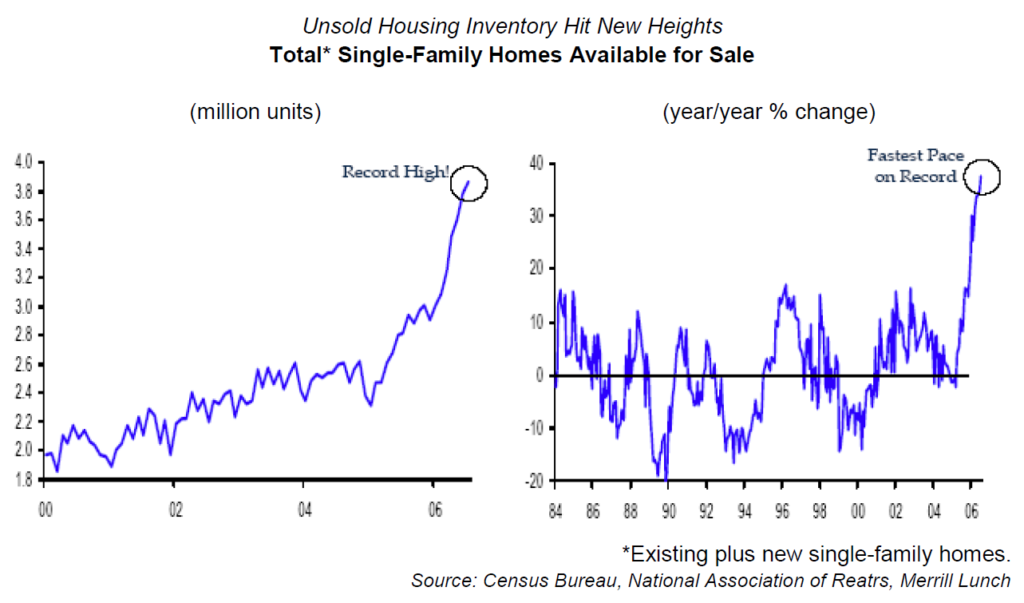

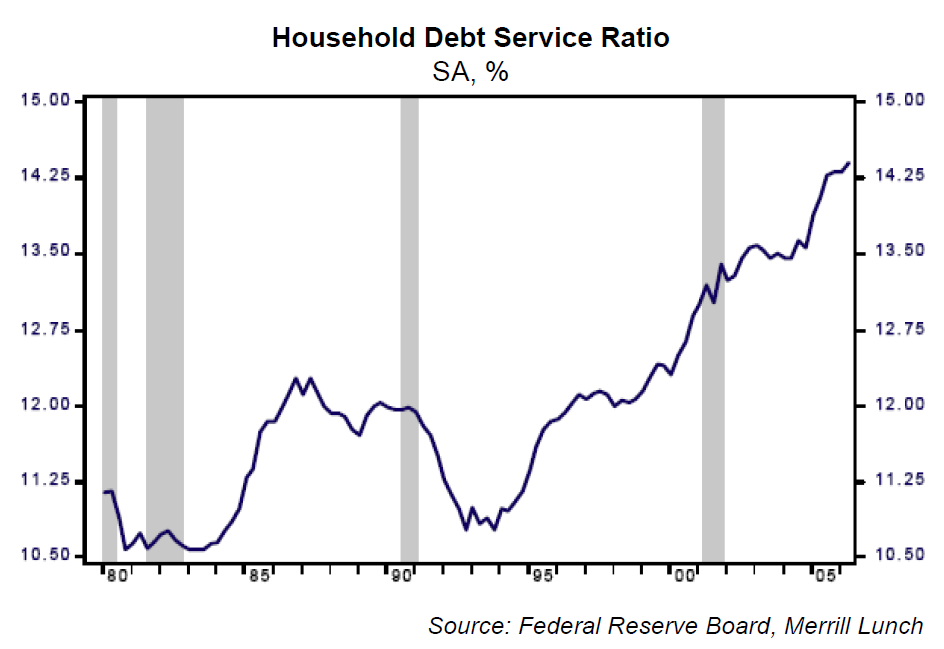

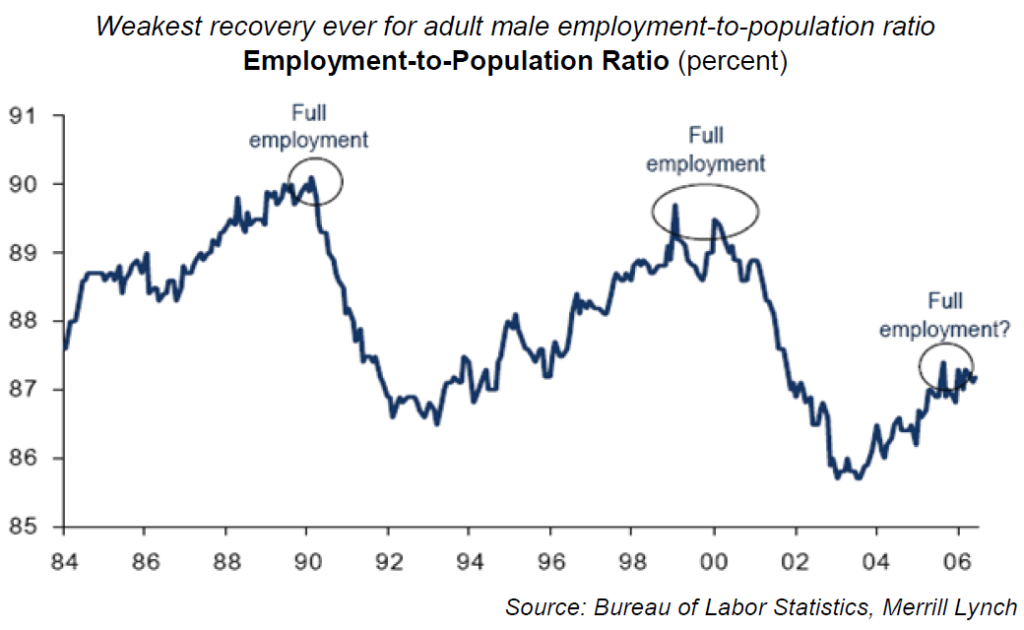

My belief that housing will not revive quickly is based on several things:

Ok, I’ll quit beating a dead house, sorry, horse. My emphatic point is that those who think this is going to be a short and relatively painless correction for housing are likely to be very disappointed or embarrassed or both.

Now what does this have to do with derivatives? Plenty! Unbeknownst to the average citizen, hedge funds have been among the most avid purchasers of mortgage debt. In fact, they are potentially the largest holder of such obligations though their clandestine nature makes it impossible to know for sure. What is clear is that several prominent hedge funds have demonstrated an amazing ability to vaporize almost overnight.

So far there has been virtually no “systemic” damage from the mostly energy-related funds that have collapsed in recent months (including the Amaranth fund, the largest hedge fund failure ever, as discussed in the October EVA). The overall financial system and the capital markets have been able to absorb these blow-ups with admirable resilience.

However, I doubt these essentially painless melt-downs (unless you are an unlucky investor in them) will continue if the mortgage debt situation becomes as nasty as I believe it will. My rationale is based on the fact that mortgage-backed debt is so ubiquitous and, in a growing number of instances, highly suspect due to the “miraculous” legerdemain described below.

Thanks to the alchemy of Wall Street, even low quality (sub-prime) mortgages can be magically transformed into high grade paper. This is accomplished through a process known as “tranching.”

Basically, a large collection of mortgages are put into a pool and then sliced up into pieces called tranches, usually four, with the most senior (i.e., the portion that gets paid first) typically AAA-rated. Thus, low quality underlying collateral can be sliced and diced so that some investors wind up with a very safe investment – or so it is assumed (more on that later).

The most junior tranche (i.e., the segment that gets paid last) is, of course, the riskiest and has the highest return. In a strong housing market, hedge funds have made massive profits on these, employing leverage to further embellish their already gaudy returns.

Even loans that defaulted weren’t a problem over the last few years because the house could be repossessed and sold for, at worst, break-even. And, of course, any homeowner with a functioning cerebral cortex was also aware of the rising market value so they would sell before the lender lowered the boom. It’s another example of a rising tide lifting all boats, even those that aren’t seaworthy.

Falling tides, naturally, are a very different matter. Until recently, loss experience with mortgage loans has been stellar. It takes someone with a lot of gray hair –or no hair– to remember the last time residential mortgage defaults escalated sharply. The statistical models being used for these mortgage pools, or Collateralized Debt Obligations (CDOs) as they are known, are reportedly based on the experience of the recent boom times.

This is where it gets interesting. For those of you who have never read Jim Grant, you have missed, and are missing, something special. Not only do his newsletters contain provocative insights into the financial markets they are also written with a remarkable flourish. He also pens a regular column in Forbes with similar wit and skill. Overall, he’s made some very astute calls though he is often premature in his warnings (there’s that premature warning thing again).

In a recent issue called Inside the Mortgage Machine he delved into this “alchemical process”, in his words, that Wall Street and the hedge fund community use to convert dodgy underlying loans into investment grade –even AAA– debt (CDOs).

Without going into the complex details, here’s the essence of what Grant is saying: low quality underlying collateral combined with copious amounts of leverage is extremely dangerous. Even a relatively small price correction in housing prices can have an exceedingly negative effect on these mortgage pools (aka CDOs). This is especially true for hedge funds which are, as usual, leveraging up in the desperate pursuit of high returns to justify their exorbitant fees.

Jim quotes Paul Singer of Elliot Associates who notes that the proliferation of “affordability products” such as interest-only, piggy-back, no-document, and option ARM loans has turned many homeowners into renters. They merely possess an option to buy. In my view, many of these pseudo-owners, woefully bereft of equity and often facing much higher monthly payments, are likely to simply say: “return to lender – the keys are in the mail.”

Grant further quotes Singer as he outlines a scenario where those hedge funds caught holding these securities, using borrowed money, experience massive losses even with a fairly minor decline in home prices. Certainly, his view may be excessively bleak but I do think there is going to be a very serious shake-out for leveraged investors playing this lethal game. And it has the potential to spill-over into the rest of the financial system as did Long-Term Capital’s collapse back in 1998.

It’s important to emphasize here that Singer is referring to the sub-prime or low-quality mortgage market; high-quality mortgages, which are a much greater portion of the collateralized mortgage market, will by definition perform far better. Yet, even here, I worry that so many of the assumptions being made were based upon incredibly favorable conditions which are now yesterday’s news.

This is where things could become contagious to the overall financial grid. Hedge funds have grown exponentially over the last decade; they are clearly one of the major market-moving factors out there. They are also an incredibly lucrative source of commissions, as well as interest income, both for Wall Street and the mega-banks like Citigroup, J.P. Morgan and B of A.

When the hedge folks put on their complex derivative trades, as with such things as CDOs, they post collateral with their broker or bank in case the market moves against them. In normal times the assets they put up provide a safe buffer for their lender. If the collateral shrinks and becomes too skinny to satisfy their broker or bank, they receive a margin call just like anybody else who leverages up to play the investment game. Again, no problem.

But what happens if the markets move very violently, creating an avalanche of margin calls that overwhelms the Wall Street back offices that process them? Realize, dear reader, that many of the investments made by hedge funds are not in things like IBM where there is a known market value and tremendous liquidity. Quite often the valuation process is more art than science and the asset in question is extremely illiquid. This might mean, during fast market conditions, the lender has no idea of how adequate the margin deposit truly is.

John Mauldin, in one of his newsletters written during the chaotic conditions of this past spring, reported that the margin departments of many major financial institutions were seriously swamped. He relayed that countless trades had not been settled, or properly accounted for, often over days or even weeks. Fortuitously, the markets recovered and settled down allowing Wall Street’s computers and margin clerks the chance to catch up.

However, that episode was but a minor earthquake – kind of like the tremor that hit Hawaii recently, not the Big Kahuna. If things really got ugly in the world of mortgage-backed CDOs, it could cause a very, very serious stress test for our financial markets and their leading participants.

This is not to postulate a doomsday scenario but rather to raise the possibility of another Long Term Capital occurrence and the temporary market panic that triggered. Unlike the perpetual gloom and doom set, I have no doubt that our financial ecosystem can withstand the fallout from a housing-to-mortgage debt catharsis. But that doesn’t mean we won’t experience some pretty serious tremors.

Before the ground starts to tremble, you better be sure your investments have a solid foundation as in top-quality stocks and bonds. Even if we avoid a serious quake, and we get the much yearned for soft-landing, they should still perform very well – especially compared to a number of things which might act like there isn’t much soft about any kind of landing.

While I am willing to be extremely blunt, perhaps foolishly so, that housing and, especially, mortgage lending industry are in for a protracted struggle, I am very ambivalent about the economy overall.

For those of you who just read our hard-copy quarterly, Strategist, this will seem a trifle redundant. Accordingly, please accept my apologies. But I truly do feel the $14 trillion dollar question (roughly the total market value of U.S. stocks) is whether we have a recession or not.

Looking through my lens, this is beyond the ability of mere mortals to discern at this time. Yes, I realize there are myriad commentators willing to offer iron-clad assurances either way but I am not among them and, frankly, I don’t think they have any more of a clue than I do.

What I do know is that the stock market is clearly convinced the horizon is bright and cloudless. Because that conviction is so fervent, there is likely an opportunity to profit – or at least be protected– if it is mistaken.

Why might the stock market’s insouciance be perhaps misplaced? In the interest of brevity, I thought I would follow a similar pattern to my tale of woe with housing in the previous section. Accordingly:

Naturally there are a number of positives as well, most notably the considerable plunge in energy prices. J.P. Morgan recently put out a piece estimating that this will save consumers roughly $65 billion annually. That’s a significant boon to the economy though one could also fairly note that energy costs are still far higher than they were three years ago. Back then we would have shuddered at the thought of oil prices near $60.

Additionally, corporate profits continue to be bountiful and the balance sheets of Fortune 500 type companies are the strongest they’ve been in some forty years. They certainly have the wherewithal to continue spending on new capital equipment, research and development, as well as hiring the workers they need.

Finally, the hysteria we witnessed back in the spring about inflation has died down and consumer expectations in this regard have also moderated. That’s a clear psychological positive.

Thus, it’s reasonable to assert we have a very mixed set of economic conditions allowing “experts” to credibly argue for a recession, a slow-down or a reacceleration. However, while I can buy the first two outcomes, the third seems to me highly improbable. And if it were to occur it would force the Fed to raise rates further from here, greatly escalating the odds of even a harder landing later in 2007 (this, by the way, is the Bear Stearns outlook).

So, as the old saying goes, all roads lead to Rome; in this case, inevitably a slowdown – be it hard or soft. Accordingly, it’s worth considering what does well in a decelerating economic environment. Bonds obviously come to mind.

In the last EVA we actually shifted to a neutral stance on bonds after the significant decline in yields from roughly 5¼% in early summer down to 4.55% in late September. This seemed to us too much, too soon and we were also distressed to see the speculative contingent so optimistic.

However, in October the bond market sold off hard, moving yields back up to 4.8%. At that point we extended our maturities somewhat. Subsequently, the third quarter GDP number came out softer than expected and bonds have once again rallied. This causes us to temper our enthusiasm though we still feel high-quality bonds are a buy on any sell off.

Basically with bonds, if the stock market is wrong and we do encounter even a mild recession next year, you get some excellent insurance. This particularly makes sense as a counter-balance for stock investments requiring good economic times such as energy and other cyclical shares.

In stock land, we still believe the consistent growth, best of breed companies are ideally positioned to benefit from any type of landing (though even these do much better under the milder scenario). They are, at long last, showing signs of leading rather than lagging the overall market. They have a whole lot of catching up to do.

A few months back there were widespread fears the economic outlook was darkening. Now, the stock market perceives a cloudless sky for as far as the eye can see. The last ninety days have shown how quickly sentiments can shift. It just might be another reversal lies ahead as the realization grows that housing matters very much to the US consumer and the US consumer continues to have a profound impact on the global economy.

Having some protection from this potentiality seems to me a most prudent course of action even if –and, perhaps especially, if– most investors couldn’t disagree more.