“But we are restricted from investing in that wider range of assets…it could be useful (at a later date) to be able to intervene directly in assets where the prices have a more direct link to spending.”

-JANET YELLEN, responding earlier this week as to whether the Fed had the authority to purchase stocks and corporate bonds.

Unless you are a first time EVA reader, you are surely aware that Evergreen Gavekal is skeptical that the current US stock market has much left in the tank. This week, we decided to use a roundtable-type format featuring our senior investment team contributors. In this issue, we examine 10 different investment scenarios that could meaningfully impact the future direction of the stock market. The tone is less what could go wrong and more an attempt to address some of the popular ideas we’ve heard that might produce a credible extension to the current bull market. You will notice that the opinions below are far from unanimous and, as such, they give readers a glimpse into the different ways our team’s philosophy is formed. Start to finish, this week’s edition is about a 15-minute read, but for our readers who prefer a more abbreviated version this format easily allows readers to skip around to topics (or authors) on which (or whom) they wish to focus.

Jeff Dicks: The base case, in my view, is that the six-quarter earnings recession comes to an end by the first-half of next year. The key to this thesis is that February did in fact mark the cycle low in energy prices. This would imply that the bulk of energy-related write-downs are in the rearview mirror. Therefore, energy earnings in 2017 will see a significant uplift given an easy comparison to a 2016 plagued with impairments. However, I am hesitant to say this will prove bullish for stocks in general. The rest of the economy has seen significant margin contraction given rising wages as well as a dollar that remains 20% above 2014 levels. Additionally, if we are right and energy prices continue to normalize higher, it’s likely to weigh on consumer spending. As a result, corporate earnings will get a boost from energy, but overall profit growth will miss expectations due to margin pressure, and weaker growth from the rest of the economy.

Source: A. Gary Shilling's Insight

Source: A. Gary Shilling's Insight

Jeff Eulberg: The second quarter of 2016 marked the sixth consecutive quarter of lower S&P 500 earnings than the previous year. Ominously, Goldman Sachs noted that this has never happened outside of a recession. Over the last two years, markets weathered this earnings sink-hole by placing the blame squarely on the shoulders of the energy sector and a strong US dollar. And, now that energy prices have stabilized and the dollar is no longer soaring, the bulls believe we're on the verge of an earnings recovery. While I do believe that energy prices have seen near-term lows, I’m not as convinced as other members of our team that the dollar has seen its short-term highs, especially if we see a risk-off period caused by a myriad of potential issues. Further, based on where current energy prices stand, I expect losses in that sector to abate, but soaring earnings growth from it will be a challenge as bankers remain hesitant to lend with the memories of sleepless nights in 2014/2015 all too vivid. So with financing restricted, it will be hard to generate much growth.

Tyler Hay: The real earnings disaster has occurred in the energy sector. To the extent oil prices remain above $40 per barrel I’d expect a bounce back in earnings. I really see a tale of two economies. First, there are those companies who can leverage technology to make themselves more efficient and ultimately more profitable. On the other hand, there are companies facing stiffer regulation, foreign competition, and higher employment costs. I think these two effects sort of net each other out and so my overall outlook for profits is essentially neutral.

David Hay: For nearly two years, stock market investors have looked past what has clearly been a full-blown earnings recession. The downside from this reality has been dismissed for the reasons cited above. These are valid points and it’s certainly plausible that the drag from these two factors (the dollar and oil) will ease going forward. The main risk I see to this sunny view is that it is looking more and more like a US recession could be in the cards for 2017.

Jeff D: If the Fed, or other central banks, gives up on ZIRP or NIRP I believe that could lead to a nasty correction in global asset prices. In the US, when the Fed announced its first rate hike last year we saw a spike in volatility and a quick 13% drop in the S&P 500. And, that was based off a measly 25bp rate hike. In response, the Fed significantly talked down the pace of future tightening, which helped to stabilize the market. If we get into an environment where global central banks actually normalize rates the drop we witnessed last year will likely be significantly magnified. However, considering that most developed economies are still committed to full-fledged easing, a radical shift like this seems unlikely.

Jeff E: An increasing number of central bankers appear to be losing faith in the almighty zero (or even negative) interest rate policy. While bringing rates in the US to zero may have been necessary during the Great Recession, now seven years out, and only 50 bps away from the zero-bound, growth remains tepid. While normalizing interest rates may be the right policy in the long run, a sustained move higher in interest rates will undoubtedly bring about lower asset prices. However, rest assured, it would take a maverick central banker to institute such a policy and I don’t see anyone resembling Paul Volcker being mentioned for the job.

Tyler: At some point the Fed will give up on ZIRP. The canaries in the coalmine are really Europe and Japan. They’ve been pushing the limits on ZIRP and even venturing into negative-rate territory. I’m hopeful the Fed will be able to learn by observing the follies of other failed experiments instead of having to try it for themselves. Certainly, a return to a more normal rate environment would provide room to cut rates should the economy require greater accommodation. The good news is the Fed is the only central bank seeming to move this direction. The bad news is the pace at which they are moving—which makes a glacier look fast.

Dave: There is a growing chorus of former senior Fed officials who are loudly asserting that eradicating interest rates—as well as fabricating trillions of dollars to buy government bonds—is backfiring. Even some current Fed-heads are expressing concerns. Should the Fed return to a set of policies that restores a reasonable cost of capital, economic activity should benefit in the long-term. The problem is the short-term. Such a radical policy shift may tip an already fragile US economy into recession, causing a financial market panic that amplifies the downturn, as was the case in 2008. As noted in many prior EVAs, the Fed has printed itself into a very tight corner.

Jeff D: Since 1950 there have been 10 official US recessions, which on average have spanned roughly one year. This means the U.S. tends to go into recession every five-and-a-half years. Accordingly, it’s fair to say we are overdue given we are over seven years removed from the 2008 financial crisis. With GDP growth running at 1.0% for the first half of the year, it’s also reasonable to say the economy is dangerously close to contraction territory. My concern is we are beginning to see the service side of the economy roll over, and big-ticket purchases from consumers, like auto sales, are beginning to lose steam. The kicker could very well be a continued normalization in energy prices. If consumers, who have faced higher healthcare and housing costs, also get pinched from higher gas prices it could be what tips the economy into recession.

Jeff E: With current U.S. GDP expectations at just over 1% for 2016, and expectations from most observers for 2017 in the low 2% range, obviously the smallest hiccup could send the US back into recession. Over the summer and into the fall, economic data has continued to deteriorate in the US, and the odds of a recession over the next 24 months have risen markedly in my eyes. While I’ll admit, by keeping assets prices elevated, the world’s central banks have avoided the tipping point for now, and this may very well continue. But as the economy continues to face new headwinds, the central banks are running out of weapons to combat the inevitable decline in asset prices.

Tyler: I’m skeptical about the predictive power of these economic indicators. If any of them really worked, we wouldn’t need to always be guessing which one to follow. I continue to think the U.S. economy is just in a slow “melt up” phase. I don’t anticipate strong GDP numbers like the 3-5% we saw in the 1990s but for now I expect the 1-2% type we’ve seen since the Great Recession to continue. I am certainly not calling for a recession unless some sort of exogenous shock hits the economy.

Dave: One of the best arguments I’ve heard for why the economy can avoid a contraction near-term is that the post-financial crisis recovery and expansion have been so lethargic. The theory is that we haven’t experienced the typical excesses that force the Fed to repeatedly tighten monetary policy, inverting the yield curve (short rates go above long rates), producing the classic recession scenario. It’s hard to argue that there haven’t been the pervasive signs of over-investment in the real economy (the energy patch being a notable exception and inventories another). However, it’s my belief where things have been over-cooked is in the financial markets. Any violent down-move in these is almost certain to feed back into the economy itself. Further, an economy that is growing at a rate so close to “stall speed”, as America’s is (and, frankly, as is most of the “rich world”), can easily slip into negative growth (aka, a recession), as both Jeffs have noted.

Jeff D: If central banks go “all-in” with accommodative policy I do think it would send asset prices higher. However, I question whether this is a likely scenario. In the US, the Fed is attempting to tighten financial conditions, as opposed to easing them. Internationally, it’s probably more likely; however, we have recently seen the Bank of Japan (BOJ) and the European Central Bank (ECB) miss expectations on further easing. Furthermore, negative interest rate policy (NIRP) appears to be doing more harm than good, particularly for banks and insurance companies. Additionally, with the MSCI World Index nearing its all-time high another “Big Easy” by overseas central banks doesn’t seem like a scenario that would unfold near-term. That said, I do think if we get a global recession this could very well be the next step central bankers take. If so, it would likely be after a fairly vicious decline, which makes the odds currently low, in my opinion, for an all-in at the present time.

Jeff E: “Don’t fight the Fed” has been the rallying cry to live by for the last seven years. However, after reviewing recent comments from many Fed officials, witnessing a hawkish tone from the ECB, and seeing the recent results from Japan’s latest quantitative easing (QE) experiment, one has to ask two very important questions. First, are the Fed Governors still prepared to give the markets a helping hand should assets prices stumble? Next, and more importantly, if the central banks do provide greater forms of monetary easing will the market continue to believe that’s all that matters? Fed Governors Eric Rosengran, Esther George, John Williams, and others, have all recently cited the strong employment numbers and a slight uptick in inflation as a reason to raise interest rates (albeit gradually). The ECB last month surprised by presenting a hawkish tone and failing to prepare the market for a QE extension in Europe. Further, the Bank of Japan recently expanded its QE program only to see Japanese government bonds sell off and the yen strengthen. While I believe this could be a reason that we see a blow-off top, I’m fine missing it because the inevitable crash to reality will be far more painful.

Tyler: I fully expect this to happen in the next crisis. However, the depth and scale of the crisis will dictate whether it’s all central banks or done more regionally. If there’s a globally-coordinated response by central banks, it’s my opinion that it will mean the world’s economy is in deep financial trouble. If on the other hand, it’s a more regional crisis, like a European Union breakup, we could still see extraordinary measures from the ECB but it might not mean the world is in crisis. While many have debated the efficacy of interest rate “experimenting” on the economy itself, no one has argued it hasn’t been good for US equity prices.

Dave: In my mind, this is one of the most persuasive bullish arguments even though it would be nearly certain to intensify a future day of reckoning. My young friend Vincent Delaurd has eloquently outlined this case, including in our September 16th EVA (click here to view). This is why Evergreen has not positioned its clients totally in cash and other no-risk securities. The next point is also valid, in my view, and another reason why we aren’t in the proverbial investment bomb shelter, surrounded by canned goods and shot-gun shells.

Jeff D: History shows the longer you go without a bear market the higher the odds you get one in the near future. There have been twenty-five bear markets going back to 1929 with each of these lasting, on average, ten months. This means you typically experience a bear market every 3 years. Given it has been well over 7 years since our last 20% drawdown (and 5 years since there was a near 20% slide), it’s safe to say we are overdue. Time alone, though, doesn’t necessarily mean a downturn is lurking. However, when you have profit margins rolling over, and extremely sluggish GDP growth, bear markets tend to occur. For instance, three out of the last four times the S&P 500’s operating profit margin declined by 2%, as it has lately, a bear market ensued over the next year. Additionally, the last two times we had back-to-back sub-3% nominal GDP prints, like we did in Q1 and Q2, we experienced a bear market. So, just because we have had certain dislocations in the market that doesn’t signify we are out of the woods. In fact, based on the length of the bull market, falling corporate profit margins, and sub-3% nominal GDP, it’s likely coming much sooner than most investors anticipate.

Jeff E: Since 2009, the S&P 500 has declined more than 5% ten separate times with the longest period between market highs being 157 days. Going all the way back to the Great Depression, the only period longer than our most recent expansion without experiencing a bear market (commonly defined as a 20% correction) was from 1987-2000. In this latest bull market, whenever asset prices started to head towards bear market territory the saving grace for risk assets, like stocks, has primarily been monetary policy. While many bulls can casually brush off an arguably arbitrary 20% bear market milepost, I do believe the winds are changing and its unlikely that central bankers will have the ammo to thwart off many more corrections. Today, with waning enthusiasm for experimental monetary policy and valuations near historic peaks, I have a strong conviction that in the near future one of these mini-panics will turn into a long overdue bear market.

Tyler: The idea that a series of corrections has helped the market blow off steam along the way isn’t the key, in my mind. What I see is a very resilient market. We’ve seen the Greek Crisis, Taper Tantrum, Flash Crash, Brexit, US downgrade, all transpire without the market falling more than 12%. Further, the longest it took the market to rebound from any of the above events was 63 days. Eventually, we will have a bear market but I think it will take a very serious event to cause it.

Dave: This one isn’t a theory, it’s a fact. Almost every corner of the investment world has experienced a pull-back—or even an actual bear episode—in recent years. The exceptions have been the S&P 500 (of course!) and government bonds, although the S&P has briefly dipped more than 10% a couple of times over the last 13 months. And even treasuries were taken to the woodshed during the “taper tantrum” in 2013’s second half. For energy and gold miners, the damage at one point was truly epic. The normally defensive mid-stream energy sector (MLPs) crashed by 60% from their mid-2014 peak to their early 2016 trough. Gold miners were smashed even harder, down 80% from high (in 2011) to low. There’s also no question that the reason Evergreen clients are enjoying such a lucrative 2016, despite huge holdings of cash and other defensive securities, is that we bought into the utter carnage in energy and gold. This rolling correction process might continue, leaving the overall market flattish, but gradually purging speculative excesses. If so, that would be, to me, the best case outcome.

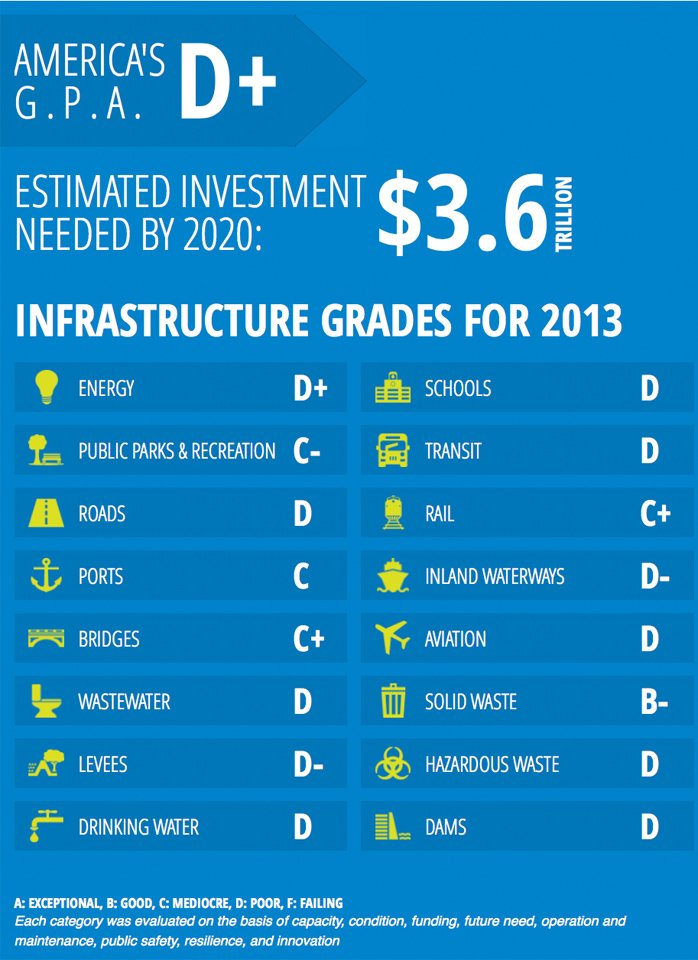

Jeff D: The American Society of Civil Engineers recently graded our infrastructure in the U.S. and sadly our nation scored a D+. So, clearly America needs a significant rebuild, but does this make economic sense? The Centre for Spatial Economics recently ran a study on the economic benefits for infrastructure spending in Canada. They found that the discounted value of GDP from a dollar of infrastructure spend was between $2.46 and $3.83. The study also highlighted the economy would add jobs, increase productivity, and improve living standards. I believe the same would be true in the US. However, with our nation’s debt-to-GDP now exceeding 100% it is a risk to add more to our mounting debt load. Considering the economic benefits, and the fact that we desperately need the upgrade, I think it’s worth that risk.

Source: The American Society of Civil Engineers

Source: The American Society of Civil Engineers

Jeff E: During this campaign season, infrastructure spending has been one of a few topics which Republicans and Democrats alike can get behind. While infrastructure packages have been proposed by both candidates, this does not mean that Congress is going to rubber stamp either proposal on Inauguration Day. Trump is not beloved by his party and the type of deficit spending he is proposing throughout his offered programs sends chills up the spines of Tea Party loyalists. If Hillary was to win, the Democratic Party is all too familiar with the challenges of getting legislation through the current House of Representatives. Further, in order for this to be bullish for the US economy, the funds would also have to be spent wisely, and looking at past records of government spending this is far from a foregone conclusion. If an infrastructure bill was to pass through Congress, a handful of individual companies may benefit, but I have my doubts about it being the saving grace for the overall US economy.

Tyler: I think this is very likely. There is an old quote that says “the US will always do the right thing after they have exhausted all other options.” We are there. Democrats and Republicans alike agree that our infrastructure is out of date. Bridges are collapsing. Water systems are failing. Traffic is out of control. In addition, it will create jobs in areas where we need them most. Better infrastructure is good for everyone and allows us to be a competitive nation. I really think this is one of the most likely ways we can extend this bull market another 4-7 years. That said, it’s in the hands of Washington politics and it seems that even on areas of agreement it takes far too long to get anything done.

Dave: For years, I’ve been advocating that the US should implement a “domestic Marshall Plan” (see August 2012 EVA). Partially due to the ineffectiveness of the Obama administration’s not-so-shovel-ready 2009 initiative, there has been no political will to attempt a new and improved version. If either leading presidential candidate can be believed (a tremendous leap of faith, I realize), it’s not a question of whether an infrastructure spend is coming, but rather of how large it will be. In addition to the size question, there is even the greater uncertainty as to whether it will be poorly-designed and riddled with political pork, as was the 2009 version. There is a lot of risk in attempting this and my preference is for private-public partnerships prioritized by the greatest societal benefits, and funded, as much as possible, by user fees. But I agree with Jeff Dicks that it’s a risk we need to take.

Jeff D: This to me is probably the most reasonable item on this list for why we could see one final surge this cycle for stocks. Evergreen spends considerable time looking for contrarian indicators. Currently, when analyzing mutual fund flows, speculative ETF positioning (inverse/leverage equity ETFs), and short-term trading sentiment, we see bearish readings in many cases. In fact, Ned Davis Research tracks returns when these readings get as pessimistic as they are today. They have found, on average, returns have annualized over 27% when any of these readings are at such bearish levels. Thus, at least on a near-term basis, we should expect a bit of a rally in the stock market until positioning becomes less bearish.

Jeff E: By driving down interest rates the central banks of the world have pushed savers into assets that they previously would have avoided. Therefore, due to the large amount of assets not trading with traditional market forces, focusing on historic levels that have caused past recessions may be a losing game. In this bull market, investors are not choosing to chase a new fad or trend like we saw in technology at the turn of the century or real estate investments in the middle of the last decade. Pessimism is understandably higher now because many investors are uncomfortable with the level of risk they’re forced to hold in their portfolio, but they remain heavily exposed to stocks.

Tyler: It’s debatable in my mind that people are pessimistic about this bull market. Seems to me that markets going up for seven years shows someone must be buying the optimistic side! What I see, though, more than optimism or pessimism, is complacency. I see investors who’ve forgotten that stocks don’t always go up. I see investors who think bonds are boring and drags on their portfolio. I see investors who think cash is the enemy. Eventually, I think that will change. I don’t believe that the basic tenents of good portfolio management have changed because we’ve been in a prolonged bull market.

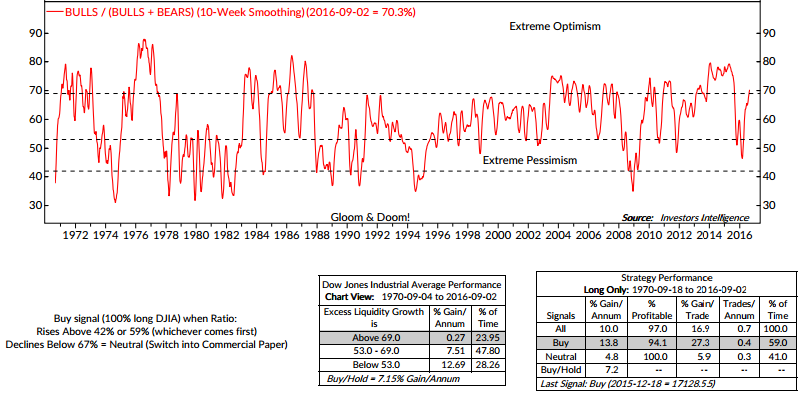

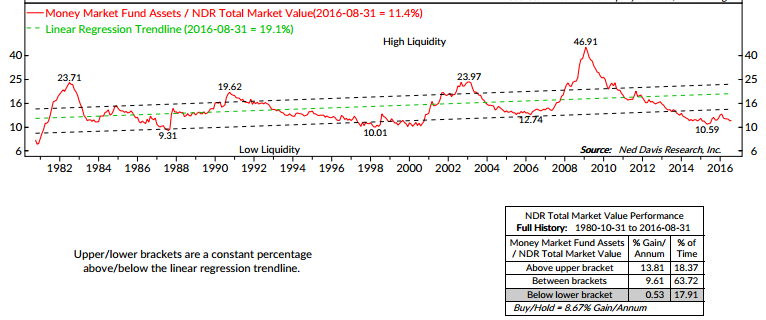

Dave: This one reminds me of the old saying: Lies, damned lies, and statistics. As indicated in last week’s EVA, my belief is that there are a lot of heavily invested bears—or at least Nervous Nellies—out there, as well as a plethora of conflicting sentiment measures. The two charts below, once again from Ned Davis Research, would argue against the belief that investors are positioned in a highly defensive manner (so even their stats are sending conflicting signals!). It is fair to say, I believe, that the market’s recent mild pullback has raised anxiety levels a bit but we certainly are light years away from mass hysteria. I’d rate this one neutral, at best.

Source: Ned Davis Research

Jeff D: One of the most compelling valuation metrics going for stocks is the “Fed Model”. This compares the earnings yield of the S&P 500 (earnings divided by price) with long-term government bond rates. The component with the higher yield, according to the Fed, is more attractive. Currently, the earnings yield is roughly 5% on the S&P 500 ($106 in trailing earnings / $2146 price) compared with a 1.55% yield on the 10-year treasury. Therefore, according to the model, stocks are cheap relative to bonds. The problem is the Fed, by manipulating interest rates, has rendered the valuation metric pretty much useless. For instance, in order for stocks to be just fairly valued relative to bonds, the S&P 500 would need trade at over 7,000 ($106 divided by .0155, or 1.55%). My point is that it is extremely likely the “Fed Model” will fail to give a warning sign ahead of the next bear market for stocks. Furthermore, we have had full blown bear markets in both Japan and Europe, which have negative rates on their 10-year bonds. So, while TINA has no doubt lifted equity markets, I think it would be foolish to say TINA is here for good due to the fact that government bond yields are at record low levels and likely to surge at some point (perhaps during the next global recession when central banks might resort to so-called “helicopter money”).

Jeff E: Again, by driving down interest rates the central banks of the world have pushed savers into assets that they likely would have avoided previously. As long as the markets believe that the Fed can control interest rates, risk assets will benefit as returns on conservative investments evaporate. However, as mentioned above, I do believe that we’re close to the market losing faith in the central bank’s ability to control interest rates. Unfortunately, when this happens, I think there will be some very surprised retired people who didn’t realize how much risk they’ve been incurring.

Tyler: This is true, I think. The US market has been a bright spot in a global economy that has been slow. I do think more and more investors have adopted the idea that with bond yields so low, one might as well buy stocks. As I mentioned above, I do think this will eventually reverse.

Dave: It’s hard to dispute the notion that the lack of attractive alternatives to US stocks has been one of the strongest drivers of this long bull market. Frankly, given a Fed that is so afraid of moving even timidly toward more normal interest rates, I don’t see that ending soon. But what could change much sooner are investor attitudes. If those shift to preferring a return of their money—versus a return on their money—then the TINA support can end very quickly. However, until there is some kind of major shock that scares the bejeezus out of the investing community, TINA will likely keep stocks well bid.

Jeff D: This one seems reasonable as well. However, I think it’s more likely money will flow from European to US bonds as opposed to stocks. European BBB-rated corporate bonds barely yield 1.5% relative to US BBB-rated corporate’s at a more reasonable 3.3%. Additionally, 1.6% on a 10-year US treasury actually looks decent when compared to a German 10-year yielding -0.11%. If Europe does enter a crisis it is reasonable to believe money could flow out of there to America. Despite that, I think it’s more likely US stocks get a significant haircut, as well, should it be a severe panic.

Jeff E: Without question, the top fear amongst the majority of Evergreen Gavekal clients that I speak with is the current Presidential election in the US. While I completely understand the depressing state of affairs of having to choose between two of the most disliked candidates in history, I’ve long believed that the political climate in Europe is far more frightening. As nationalist parties continue to rise in the post-Brexit polls, European political positioning will continue to add volatility to global markets in the second half of this decade. Thus, with already anemic growth throughout the developed world, I find it impossible to believe an unravelling in the world’s second largest economy (collectively) could be positive for risk assets anywhere. I do believe that US debt securities and gold will benefit, but those counting on further equity appreciation will likely end up feeling short-changed.

Tyler: I agree with Jeff and Jeff.

Dave: This is something I can buy—up to a point. For example, if a European bank or two goes under, that might push even more money into the US (as noted in prior EVAs, the Swiss National Bank already owns $60 billion of US stocks!). But if the big Italian vote, now pushed back until early December, goes against the establishment party (polls indicate a very close race), and the eurozone banking situation devolves into a full-blown panic, that would likely create some serious selling pressure, even in US stocks.

Jeff D: To me, if you look at the US election, it’s a non-event if Hillary takes the Oval Office. If you compare Hillary vs. Barack on issues such as defense, the economy, or even individual rights, there is not a huge difference between the two. This probably means investors will assume it is more of the same for the next four years. I think the base case is you will see brief rallies each time Hillary takes the lead. However, if Hillary wins, it’s likely to be ho-hum for the market. At that point, the market will focus back on the Fed, global monetary policy, and economic growth—or the lack thereof. As a side note, there are murmurs from several extremely bright minds that Donald Trump will win the presidency, despite his generally panned performance in the first debate. I know I am not going out on a limb here, but I personally think the odds of this occurring are slim-to-none.

Jeff E: In spite of Trump's handful of rallies in the polls, my belief that Hillary will end up winning this election has not wavered much. However, the populist uprising seen during the Brexit election certainly gave me reason to pause. Was Brexit the start of a populist trend globally? I don’t believe so. If you study the electoral map, Trump is still fighting an uphill battle and will need to improve dramatically from his lackluster showing on Monday night. However, as I mentioned above, I do believe that Brexit is the first of many populist uprisings in Europe. I expect Hillary will win, but I’m not sure it means that the global economy will steer clear of all the political landmines out there.

Tyler: If Hillary wins I expect markets to yawn. If Donald wins I think this could create a high level of uncertainty, something markets do not like. Ultimately, though, I believe the market would realize that The Donald faces challenges within his own party. Therefore, the worry that a Republican mandate could give him excessive power to push his agenda seems overblown to me. While the US election effect on markets has been a popular conversation at cocktail parties, I don’t think it will matter nearly as much as people are expecting.

Dave: It’s almost a cliché to say markets are more comfortable with Ms. Clinton than with Mr. Trump but sometimes clichés are true. Therefore, I do believe that if she wins markets will rally—for awhile. After a few jubilant sessions, however, I suspect the reality of “more of the same”—meaning continued sluggish growth at best and a possible 2017 recession at worst—will weigh on investors’ minds

Obviously, there are many other potential positives that could prevent this aged bear from making its maker in the near future. These would include the potential for corporate tax reform and the simple reality that stocks tend to rally between November and May. But, we’ve tried to give the bull case our best shot. We’ve learned that this beast was truly born to run..and run…and run.

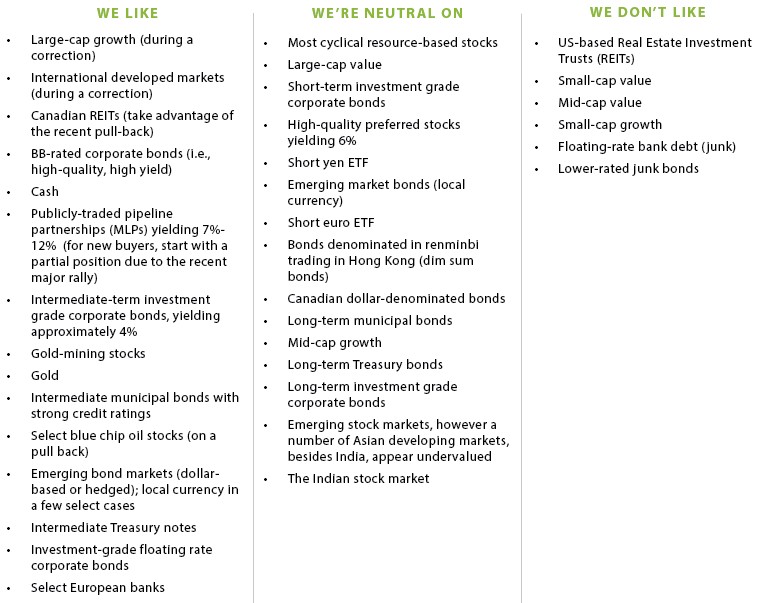

OUR CURRENT LIKES AND DISLIKES

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.