Click here to download PDF and print.

“The psychological effect of stock market activities on business is, I think, overemphasized…I do not think that the fall in security prices will itself cause any great curtailment in consumption.”

- E. H. H. Simmons, president of the NY Stock Exchange, January 26th, 1930.

THE EVERGREEN EXCHANGE

Worth Wray, Tyler Hay, David Hay

What a difference a month makes! Realizing that the suddenly vulnerable US stock market is top of mind for most investors, three of our team-members are going to explore several possible scenarios in this month’s edition of the Evergreen Exchange. We are attempting this with full admission that we are looking through a glass darkly as all investment professionals are these days. We also concede there are definitely more than three possible paths for stocks to take in the coming quarters. As noted repeatedly in prior EVAs, there truly is no precedent or playbook for how this era of extreme central bank manipulation of asset prices will end. But we are convinced that when it does, it is likely to be messy—possibly very, very messy. Yet, times of chaos, uncertainty, and fear typically bring exceptional opportunities for cash-heavy investors with a willingness to buy into the panic.

While we are taking different tacks and coming to varying conclusions about the longer-term outlook, you might notice that all three of us believe an oversold rally is a near certainty (and we felt that way even before this week’s bounce happened). We also suspect it will be relatively brief. In our view, a more durable recovery will not occur until prices decline meaningfully and valuations return to more reasonable levels.

Now, without further ado, let’s check out the three scenarios.

___________________________________________________________________________________________________________________

DON’T PANIC... JUST YET

Scenario #1: Correction likely overdone as global investors overreacted to previously under-appreciated China risks and herding behavior took over. A rally here is an opportunity to get defensive. New highs are possible as inflows from abroad drive P/E multiples higher, but beware shocks from abroad.

As my colleagues and I have continued to warn in recent weeks, anxiety from China and fragile emerging markets is starting to spill over into major developed markets around the world. While the direct economic linkages are admittedly limited—especially in the United States, where exports account for a modest 13% of GDP—what we have seen in recent days is proof that our interconnected and dangerously leveraged global financial system is subject to extreme herding behavior. All it takes is a break in the prevailing mindset to trigger a global rush for the exits.

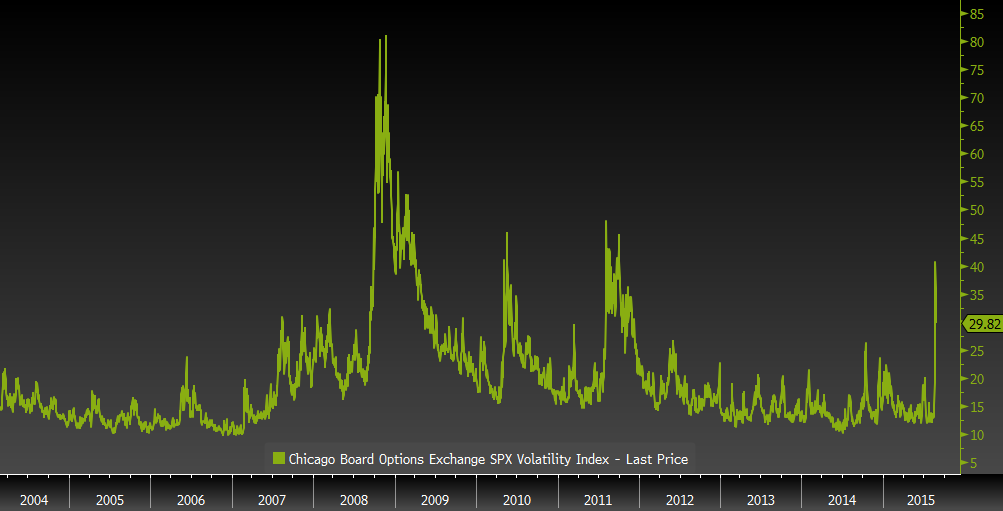

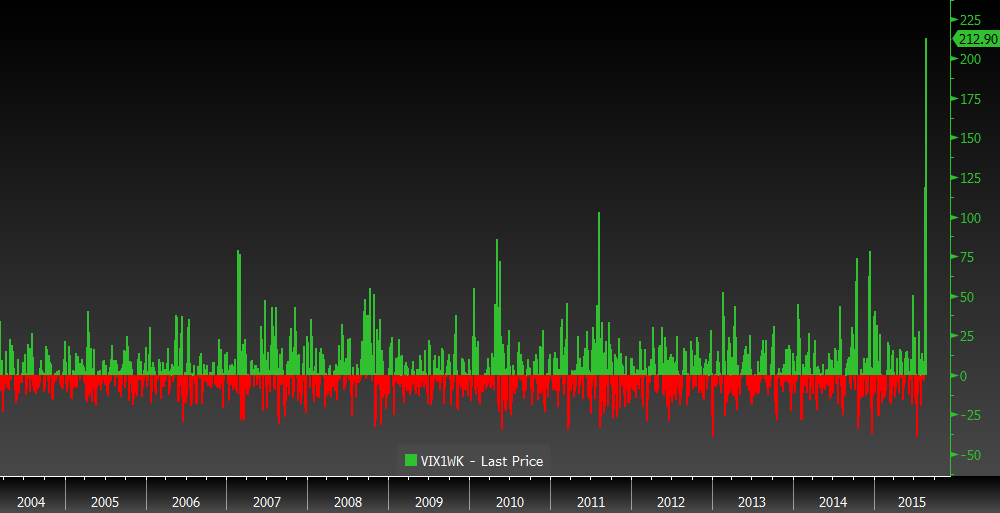

As you can see in the charts below, US equity volatility, as measured by the VIX Index, jumped from 12 to 47 on Monday morning as a number of high-quality stocks and relatively high-volume ETFs sold off in classic flash-crash fashion. We saw credit spreads blow out, commodities and emerging market currencies slide to new lows, and equities drop in an outright panic. While a number of traders had speculated that Monday could be a rough day for global markets, no one could have guessed that the week-over-week change in the VIX would explode to levels unseen even during extreme events like the Lehman shock or the Euro crisis. This is what a mild panic looks like in a market dominated by high-frequency trading, ETFs, and systematic allocation models.

FIGURE 1: US EQUITY VOLATILITY (VIX INDEX) Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

FIGURE 2: US EQUITY (VIX INDEX) ONE-WEEK CHANGE Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

Through Thursday (8/27), the S&P 500 has fallen 6.5% from its May 2015 peak, which begs a critical question for US investors: Are we on the edge of the great unraveling? Is this sell-off the beginning of a vicious bear market? Or are we just experiencing a long-overdue correction—the first in four years—in an otherwise durable rally?

In my mind, a major break seems a bit premature. And the sudden shift in market sentiment appears to be overdone. I won’t go so far as to call this correction a long-term buying opportunity, but I also wouldn’t abandon the safety of a defensively-positioned, diversified portfolio to make an all-in bet on cash or US Treasuries. Unless the US economy suddenly slides into recession, this bull market can run a while longer and valuations can stretch even further against a backdrop of weakening global growth… which would raise the uncomfortable odds of a major deflationary accident in the medium term.

Consider, for a moment, why global financial markets are melting down. While emerging markets like Brazil, Russia, Turkey, South Africa, Malaysia, and Indonesia (among many others) have been deteriorating for several years, and capital outflows have certainly accelerated in anticipation of a Fed rate hike over the past several months, the US dollar has not fared favorably in the past week. In fact, we saw both the euro and the Japanese yen surge against the dollar on Monday morning as markets took the turmoil as a sign the Fed would be forced to delay a hike. More on that in a minute, but suffice to say that the US dollar is not driving this correction. China is… or rather the market’s over-reaction to recent events in China.

Let me be clear. China is not collapsing, but Beijing’s credibility is. Last month’s confidence-killing intervention in its domestic equity market, coupled with growing capital outflows, the clumsy move to a more market-oriented exchange rate, and the recent drop in China’s manufacturing Purchasing Managers Index (PMI), has led to a sharp break in a broadly-accepted narrative. The world is suddenly realizing that Chinese economic growth is slowing more dramatically than the official numbers suggest and Beijing may be losing control. But while the simultaneous un-anchoring of what had been one of the world’s most stable currencies—and widespread questioning of what had been one of the world’s most credible governments—is understandably having a big impact on sentiment, the direct economic impacts are not so sudden.

A number of China watchers—myself included—have been warning for years that economic growth was slowing dramatically under a weight of bad debt incurred in the wake of the Global Financial Crisis. We shouted from the rooftops that China’s growth was far too reliant on credit-fueled, malinvestments in “old economy” sectors (like real estate, infrastructure, mining, and low-value-added manufacturing). We said that the Middle Kingdom faced an epic crisis or long-term stagnation if it failed to quickly transition to a more sustainable growth model driven by “new economy” sectors (like retail, services, technology, and high-value-added manufacturing). We even warned that an avoidable crisis in China could send a shock wave through the global financial system and that the inevitable investment slowdown would be enough to destabilize commodity-oriented economies around the world.

That said, it’s important to note that we are not seeing an economic crisis in China today. The world is waking up to the under-appreciated risks in the People’s Republic because its equity market is collapsing. And while a crashing equity market dramatically increases the odds that China will find itself stuck in the middle-income trap, as Beijing is forced to backstop bad debts (rather than offloading bad assets and deleveraging troubled firms through equity issuance to foreign buyers, as Beijing had hoped), it signals very little about the real economy in the short term. As Capital Economics’ Julian Evans-Pritchard recently noted, “The 40% decline in the Chinese stock market since June has nothing to do with any deterioration in the economy, just as the 58% surge in the first half of this year didn’t reflect a genuine improvement in economic fundamentals either.”

So, what if markets realize that rumors of China’s imminent collapse are greatly exaggerated over the next few weeks while US economic data continues to improve? What if the stellar August consumer confidence data (released this week) foreshadows a solid employment report next week? And what if, despite the naysayers, the Federal Reserve does decide to follow through with a rate hike in the coming months? Recent softness in the US dollar, continued tightening in the US labor market, a desperate policy need to get off the zero bound, and the risks to the Fed’s credibility in the event of inaction, collectively provide sufficient justification for a 0.25% lift-off—despite the fall in oversupplied commodity markets, the slide in inflation expectations, and weakness in global growth.

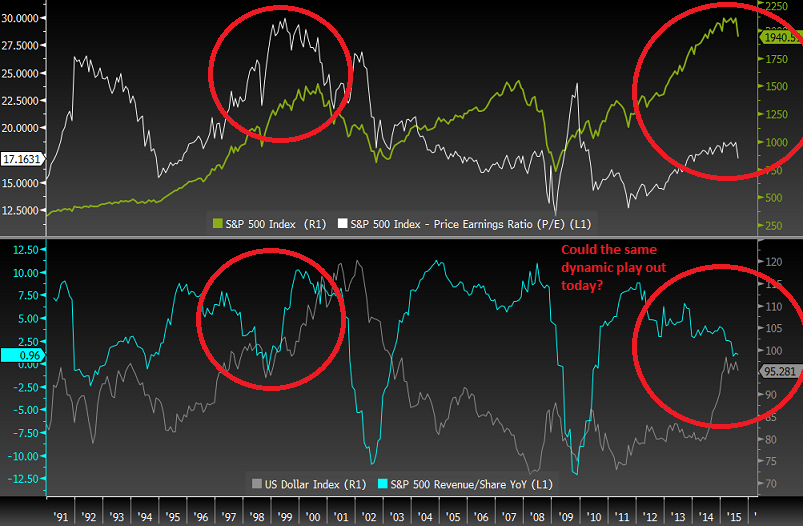

Aside from the bloodbath that a Fed hike would likely trigger in fragile emerging economies and dollar-denominated commodity markets, a rate hike could initially lift the US equity market somewhere in the neighborhood of 10%. And while a strong US dollar could certainly erode the 33% of S&P 500 earnings that come from abroad, the capital inflows behind it could also drive the equity market higher through multiple expansion. We saw that dynamic before in the late 1990s and it’s not out of the question this time around; however the risk of exogenous shocks are much higher (dare I say, probable) and could easily shift incoming flows from growth-oriented equities to the safe haven of US Treasuries.

FIGURE 3: DOLLAR UP, REVENUES DOWN, STOCKS RISE IN LATE 1990s AS FOREIGN CAPITAL RUSHES IN Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

With all this in mind, I wouldn’t bet aggressively on higher equity prices at this point… just as I wouldn’t bet on an outright equity collapse this week or this month. When the same capital inflow dynamic that could drive multiples higher for a brief period could also destabilize the global financial system, it pays to be cautious. A 10% bounce—or even a 20% surge—in US equities could present the opportunity for respectable short-term trading gains (or to strategically shift your portfolio holdings around for the next phase of the cycle), but current valuations still point to disappointing long-term investment returns and the risk of an outright crash. I think I can speak for all of my colleagues at Evergreen GaveKal when I say that a temporary reflation would present an opportunity to become even more defensive.

___________________________________________________________________________________________________________________

FEELING QE-EASY.

Scenario #2: Watch the Fed, use recent volatility as wake up call: lost confidence is the end game.

On Monday, the Dow Jones Industrial Average closed down 588 points, making it the 7th largest point loss in the market’s history. During Tuesday’s trading session, the market was actually 13% off its high from May 19th. For many, the extreme volatility we’ve seen of late has likely brought back flashes of the swings we saw during the financial crisis of 2008-2009. Now, if any of this caught you off guard, it probably means you are not a subscriber to this newsletter or haven’t been reading it very closely—neither of which I would fault you for.

I’ve been asked to outline what I think are the implications of the market’s recent turbulence and how I see events unfolding from here. However, I can’t begin to do so without starting with the Federal Reserve. Personally, I believe Fed chair Janet Yellen knows we are at a fundamental crossroads that’s been a long time coming. On one side of the debate are those who believe the US economy and financial markets can sustain a rate hike. After all, the data is decent (especially in the wake of the recent second quarter GDP reading of 3.7%), markets have had plenty of time to digest a hike and, lastly, if they don’t hike soon there will be no room to cut if we enter into another crisis. On the other hand, Jeff Gundlach, Larry Summers, and others have cautioned that the economy isn’t strong enough to sustain an increase in interest rates, especially given the rise of the US dollar. If the Fed plans to raise rates at their September meeting—as most investors expect—one has to wonder if the recent market gyrations are enough to change the Fed’s course. Personally, I don’t think it really matters whether or not they raise rates in September. I think those who are fixated on this question are missing the point. Instead of wondering about the trajectory, timeline, and token language surrounding the “pending” hike in interest rates, investors should be preparing for the opposite: another new round and form of quantitative easing (QE).

You see, even if they start to hike rates, it’s inconceivable that they get very far into their campaign before they have to reverse course. Unfortunately, the Fed has missed its chance to raise rates while markets were calm. Now they are behind schedule and any attempt to accelerate the tightening cycle will likely knock the economy flat on its back.

The Fed is stuck with a losing hand and is trying to keep a really good poker face. When they are forced to show their cards, the markets will panic, forcing the Fed to scramble for a new way to inject life into the markets. It’s at that point investors will run for the exits. Since the financial crisis, we have been brainwashed to believe that the central banks have a handle on economic growth and financial markets. The central banks cannot and do not steer financial markets anymore than FEMA controls natural disasters. Instead, they provide relief in times of crisis when they have the tools.

I’m afraid the next crisis won’t be one of a financial nature but, rather, a crisis of confidence when investors stop believing the Fed is in control. Will it be QE 4,5,6 before markets realize that continual need for central bank intervention isn’t a support for markets, but a sign of economic fragility? With the Fed out of chips, I think the onus will then fall on the Federal government to boost spending. It’s bad form for a Republican Congress to oversee a massive spending bill. So, instead of a spending bill, it might be called an infrastructure investment bill. Regardless, of partisan views, it’s long overdue. Both parties have spent years bickering in traditional D.C. form as our infrastructure has continued to decay. Want proof? Every four years, the American Society of Civil Engineers releases a report card for America’s infrastructure. It reflects grades the Kardashian girls probably earned in high school.

FIGURE 4: US INFRASTRUCTURE OVERALL RATING Source: American Society of Civil Engineers

Source: American Society of Civil Engineers

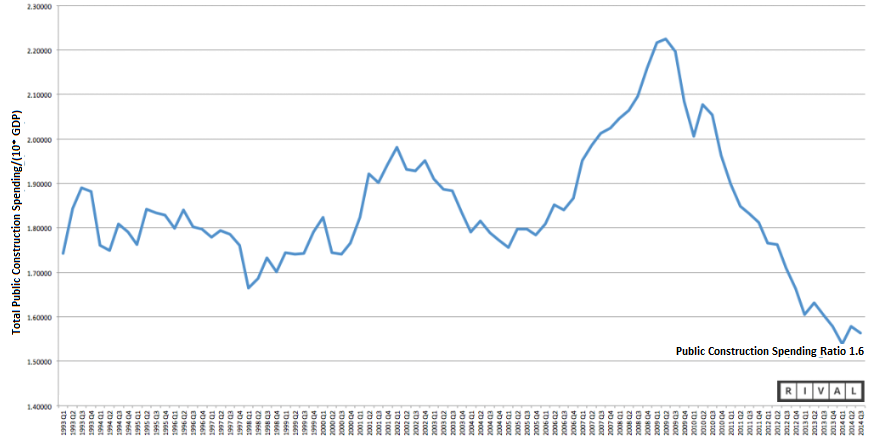

Clearly, we’ve been deferring a lot of spending on this front.

FIGURE 5: PUBLIC CONSTRUCTION SPENDING TO GDP RATIO Source: FRED

Source: FRED

Let me admit that I’m not the first person to make the economic case for an infrastructure spend. Our CIO, David Hay, and other lonely voices have been calling for this for years. However, what I haven’t heard many people conclude is that it will occur because the Fed is out of QE ideas. Certainly, we can all agree that Congress isn’t very productive unless the country is in the midst of a crisis. I don’t know how many more pep talks and QE experiments will take place before confidence is lost and lawmakers are forced into action. It’s estimated that we need $3.2 trillion of investment to modernize our infrastructure, which will mean more debt. For those of you shaking your heads because you think we are already in over our heads, I’d say it’s better than the alternative. The current QEs we’ve witnessed have done little for the real economy and a lot for the financial markets. This type of investment would be very much the opposite. The effects of a massive infrastructure would benefit Main Street more than Wall Street, something many may find refreshing.

Last week was a sneak preview for investors. Despite the precipitous decline, we anticipate that markets will rally at least partially back from what looked like extremely oversold levels (as they have already begun to do). Unlike Worth and Dave, I don’t have a strong sense of where stocks are headed after this week’s recovery. Rather, I think it’s more important for clients to reassess their risk levels and to study the interaction between the markets and the Fed.

If the pain of last week was too severe, your portfolio likely has too much risk. The decline of 13% was a heads-up for what’s ahead if the economy turns south while the Fed’s gun remains unloaded. But whether the Fed does raise rates or not isn’t the critical piece of the puzzle. Instead, watch how the market responds. If the Fed acts and the market responds favorably, you know that the belief is still alive that we are in a period of central bank omnipotence and your portfolio is likely safe. Instead, be on guard for the moment when the market doesn’t take the bait and those who’ve been saying, “Don’t fight the Fed” start to say “Let’s indict the Fed.”

___________________________________________________________________________________________________________________

THEY DON’T CALL IT FALL FOR NOTHING.

Scenario #3: Short-term rally (more than we’ve seen thus far), but market fails to make new highs; second down-leg into Sept/Oct bottoming close to 1600; Fed launches QE 4, triggering a powerful recovery; a deeper decline below 1600 in 2016; a new bull market begins in 2017.

Why is it that it’s not just leaves that fall during autumn, but stocks so often do, too? It’s a pattern stretching back to at least the 1920s and it does overlap with the storied “Sell in May and Go Away” axiom, a notion that has been derided because it didn’t work very well in recent years. You may have noticed, however, that following it would have been a good idea in 2015, at least so far. (In fact, it worked reasonably well last year, too, if one was a buyer during the 2014 autumnal swoon.)

The positive aspect of this seasonal tendency is that stocks often bottom in October and rally furiously thereafter. It may come as quite a shock to EVA readers that I actually believe this is fairly probable this year as well. But, just so I don’t completely throw you off, my suspicion is that the typical October lift-off will occur from a much lower level than where stocks are trading this week, despite the correction we’ve already seen.

Regular EVA readers know that I have felt the odds of a market crash or “crashette” were unusually high for the last year or so. We almost got there last fall, but it was too short and shallow to even qualify for “ette” status. This time, though, it’s a very different story. The 5.2% drop on Thursday and Friday of last week, followed by a thunderous 1000-plus point cliff-dive in the first few minutes of trading on Monday morning, certainly qualifies for at least the crashette designation. While stocks rallied vigorously through much of Monday’s trading session, they still entered official correction terrain, and did so in a hurry. So is that it? Did we get this fall’s fall out of the way early this year?

In my view, that’s unlikely. The excesses of years and years of free money—leading to the most overpriced market ever on a median price-to-sales ratio basis—are not going to be flushed out by a mere 10% correction. Furthermore, the bubblemania went far beyond biotech stocks and to-be-issued IPOs (unicorns), as it engulfed asset classes as diverse as collector cars, rare books, fine art, commercial real estate, and luxury residential properties.

Unquestionably, stocks became deeply oversold on Monday. Accordingly, a rocking rally was close to a slam-dunk and, after a false-start on Monday, we’ve seen a snappy snap-back. The question is will this be a counter-trend move in an emerging bear market, or the next chapter in this magnum opus of a bull market?

One reason I think it’s the former and not the latter is what has happened to volatility lately. My primary prediction at the start of 2015 was that the eerily quiescent level of “vol” that characterized 2013 and 2014 was going to change in a big way this year. As Worth already conveyed, volatility has made a resounding reappearance.

Why does that matter? Because high volatility is consistently associated with periods of market weakness. As CNBC’s Bob Pisani breathlessly observed on Monday, “We saw an entire year’s worth of volatility play out in half an hour.” Similarly, my ever-observant partner Louis Gave noted that the S&P swung by a cumulative 4500 points during Monday’s session. Consequently, it’s safe to say something is definitely different about this market. It’s called fear and it’s been MIA for a very long time.

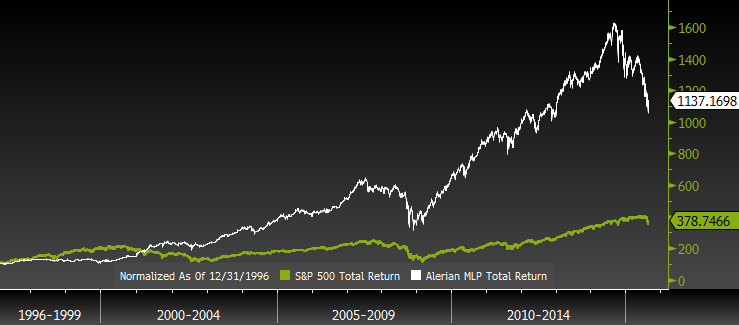

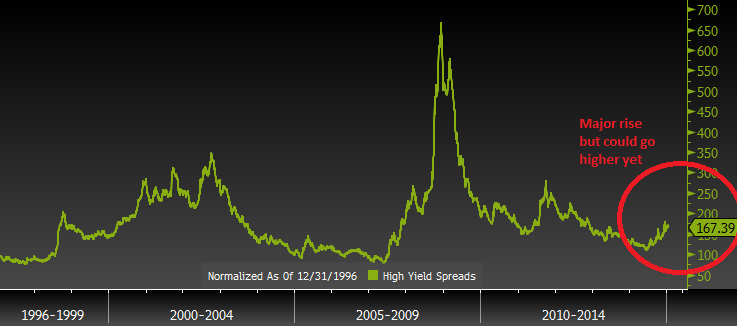

In my opinion, this newfound angst isn’t misguided. Yield-oriented securities have been flashing red for months and, as I’ve conveyed to numerous Evergreen clients, credit market-related issues typically lead the stock market. If MLPs are any indication, this market’s rabbit hole goes deeper than 10%.

FIGURE 6: S&P 500 AND ALERIAN MLP INDEX Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

FIGURE 7: HIGH YIELD SPREADS (EXCESS YIELD OF JUNK BONDS VERSUS US TREASURIES) Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

Tide going out—multiple bottoms coming into view. There is a mounting sense that the planet’s economy is experiencing the inverse of the much-anticipated “escape velocity.” Should a global recession be waiting in the wings, those hoping for the US market to take flight once again may have a long wait. Although the high-profile economist David Rosenberg points out that, aside from a spike in oil prices, “No external force has ever dragged the US economy into recession or a bear market,” the prevailing mindset that America’s economy can decouple from the rest of the world may soon be put to a serious stress-test.

A more plausible bottom for the S&P 500 is around 1600. This would amount to approximately a 25% peak-to-trough decline and it should create some very compelling bargains in a wide range of stocks. This level would also bring the S&P back to its crucial break-out point from 2013, when it shattered the resistance of roughly 1580 that marked the ceiling for both the 1990s’ mega-bull move and the 2003 – 2007 up-market. It’s my experience—recently corroborated by the venerable Art Cashin—that former key resistance zones become support levels on the way back down.

A 25% market decline is also likely to terrify the Fed. Our cherished central bank is undoubtedly aware that a plunge of that magnitude could tip the wobbly US economy back into recession, particularly given the weakness hitting our shores from overseas. Accordingly, the Fed will likely throw all of its resources at stabilizing the market somewhere in the down 20% to 25% range. It will probably have plenty of company from other central banks who may, in some cases, resort to actual money printing versus fabricating bank reserves. If I’m right and the Fed, along with its global cohorts, drenches the world in money, we are likely to see a resounding rally—for a while.

My overarching concern, as Tyler touched on, is that the era of central bank financial market manipulation is drawing to a close. China’s inability to stabilize its stock market despite unprecedented intervention may be the canary in the coal mine (and, goodness knows, they have a lot of those over there, a few of which haven’t blown up or caved in).

Should a renewed global quantitative easing (QE) effort create only a fleeting up-lift, then a far worse decline may well lie ahead. Breaking below 1600 sometime in 2016 would, in my mind, confirm that we are headed considerably lower. The mega-risk is that a market melt-down produces a US recession—rather than the other way around—despite David Rosenberg’s soothing view. This would be a huge and nasty surprise to the complacent consensus.

The months to come are almost certain to be highly volatile, filled with air-pocket opportunities to accumulate pummeled securities and rallies in which to reduce exposure. As has been the case for the last 15 years, the buy-and-hold investor is likely to continue to have a hard time holding onto the transitory gains generated by bull markets that rise far above reasonable value.

___________________________________________________________________________________________________________________

OUR CURRENT LIKES AND DISLIKES

Changes are noted in bold.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.