The Evergreen Virtual Advisor is over 10,000 subscribers strong, up from just 500 readers towards the beginning of the last decade. Roughly 10% of subscribers are clients, leaving us with the sometimes-difficult task of writing to two distinct audiences. Clients are keenly interested in Evergreen-specific happenings, whereas outside readers are more interested in our macro market outlook. This week’s newsletter attempts to carefully thread the needle between both interests.

Evergreen Roundtable 2020 is our take on the different Roundtable Q&A pieces you might find in Barron’s or other financial publications this time of year. Evergreen’s investment decisions are not made by any single individual. Instead, our team confers nearly every business day to discuss our various investment strategies. This team consists of people with very different lenses through which they view the world and, oftentimes, these daily investment discussions become quite “spirited.” We foster the competition of ideas. Evidence and logic outweigh seniority or rank.

In the newsletter to follow, our investment team was asked to both look back on 2019 and forward to 2020. This team consists of Jeff Eulberg (Director of Wealth Management), Jeff Dicks (Director of Portfolio Management), David Hay (Chief Investment Officer), Tyler Hay (Chief Executive Officer), and Mark Nicoletti (Managing Director, Family Office). The group reflects on what transpired and forecasts what may lay ahead. As always, we welcome your feedback and appreciate your loyal readership.

Note: Evergreen Roundtable 2020 will run as a two-part series. The second edition of this series will be published next Friday, January 24th.

How do you view the upcoming US Presidential election’s effect on financial markets?

Tyler Hay: The view from Wall Street is as follows when sizing up the potential presidential candidates and their respective impact on U.S. financial markets. Trump would be good, Biden neutral, Sanders and Warren would be bad. I am not taking a stance as to who would make a good president for the sake of the country but simply relaying what investors perceive each candidate’s subsequent effect could be on the market.

Narratives are a powerful force when it comes to how investors act, and we shouldn’t underestimate the impact they have on the behavior of market participants. Sanders and Warren are widely seen as having a vendetta against Wall Street and the wealthy, which paints a less than rosy picture for stocks (should one of them reach the Oval Office). In the event that one of them does indeed win the election, the question then becomes: How much support for their policies (such as a wealth tax) can they get from mainstream Democrats? In my opinion, not much. However, I would caution that there could be a period of uncertainty where we wait for this answer. As we know, uncertainty can lead to painful price movements in the market, so a victory by either Warren or Sanders would likely be a near term headwind for stocks as the market attempts to sort out the likelihood of adoption of their economic agenda.

Perhaps most controversial is each candidate’s proposal of a wealth tax. On the surface, the notion that Bezos, Gates, Zuckerberg, and other billionaires could afford to part with more of their wealth certainly has its appeal in the eyes of many Americans. But the implementation and consequences are more complicated. A wealth tax on Billionaires may seem benign, affecting only the ultra-rich, but it does open Pandora’s box. Who’s next? The hundred millionaires? The millionaires? Once the market can no longer anticipate the reach and scope of such a tax, investors are likely to worry. It seems far-fetched to imagine a world in which individuals are taxed on their overall wealth versus income or capital gains but the most destructive events for markets are not anticipated pains but unexpected ones, and this could be a very big one, should it happen.

Jeff Eulberg: According to JP Morgan, 79% of Republicans and 33% of Democrats would rate the current national economic conditions as excellent or good. Clearly, how one votes in the primaries can skew answers to the question above. I’ve never voted in a primary or been a registered affiliate of either party. Here’s how I see the election affecting financial markets.

I expect 2020 to be a year full of headline risk. Meaningful conflicts with Iran or China will be avoided because of the major threat they pose to decimating the financial markets. The administration will make every effort to keep the status quo and tout victories with Iran, China, immigration, deregulation and taxes.

Elizabeth Warren or Bernie Sanders will make a serious run at the Democratic nomination. After a recent surge in fundraising and poll numbers for Sanders, a poor showing in the early primaries could be the beginning of the end for Warren’s campaign. I would then expect her base to rally behind Sanders, creating a powerful coalition to face-off against Vice President Biden.

If Biden, Buttigieg, or Bloomberg win the nomination and ultimately the election, I would expect the markets to view this outcome with very little fanfare. The Senate will likely remain Republican-controlled and will make it quite difficult for the executive branch to influence any meaningful change.

If Warren or Sanders win the White House, markets may initially sell off on fears of reversing the current administration's economic successes. However, markets won’t see broadly lasting effects as long as the Senate is controlled by Republicans. Energy and healthcare stocks will clearly be targets of either administration, as those are key issues for both bases.

If Trump is re-elected, a final term will remain volatile. The same fights he’s picked and issues he’s clung to – in opposition of democrats and others — will continue for another four years. Limits will be tested and hopefully, as was the case in his first term, lines that would create sustained issues for the global economy won’t be crossed.

Facebook, Apple, Amazon, Google, and Microsoft have been huge drivers of the US stock market. Will this trend continue into the next decade?

Tyler Hay: I’d argue that technology companies are the only “gimmie” investment of the next decade for two reasons. First, they are in an industry of companies that can grow without significant dependence on human and financial capital. These companies carry very little debt and they are able to grow based on ideas not more people or more money. Second, their customer base is wildly diverse. Finance 101 was taught on the basis of buying a diverse set of stocks, but I think this is old-world thinking. Are Amazon, Microsoft, and Google’s customer bases not spread across enough different company types or geographies? How engrained are these companies in our everyday life both as consumers and companies? Where are your family pictures kept? Where do you log-in every day to do business activities? When you really think about it, how different would life be without Amazon, Microsoft, or Apple? I know I wouldn’t be able to function. These companies don’t supply you with products but ecosystems that touch so many aspects of our personal and professional lives. It is worth noting that, ultimately, it could be their very dominance that ultimately makes some of them the target of governmental antitrust regulation. That said, I think the risk is worth the reward here and I continue to believe that technology companies will be an oasis of growth for investors.

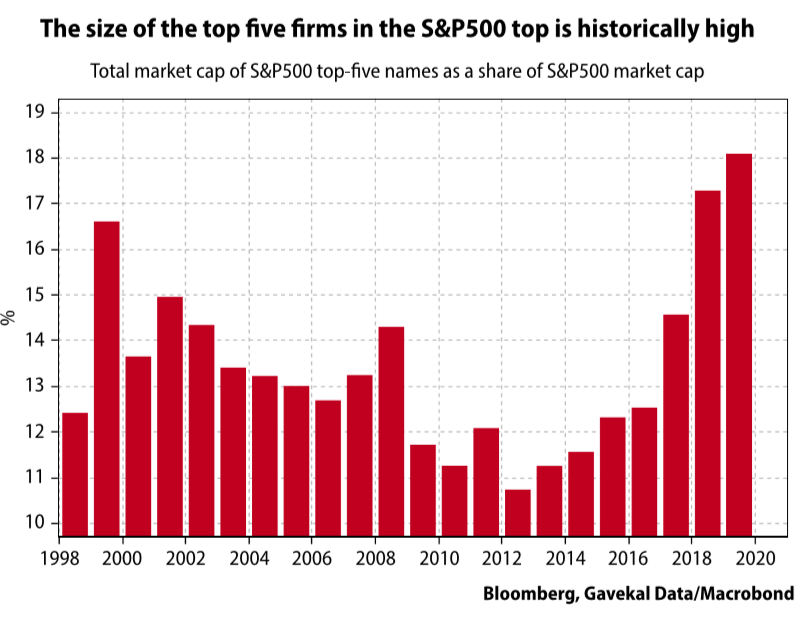

David Hay: Such concentration of returns and market value certainly poses some serious risks. A quick glance at the below chart shows the top five companies – made up today of Apple, Microsoft, Amazon, Google and Facebook – represent an even greater percentage of the S&P 500 than the five biggest did during the peak of the late 1990s tech mania. That alone should raise some eyebrows—and, perhaps, some stop-loss thresholds.

It’s also sobering to realize that of the five ultra-mega cap stocks from two decades ago, the only one still in the top tier is Microsoft. This fits with the historical reality that the most valuable companies at the end of a calendar decade almost always underperform over the next.

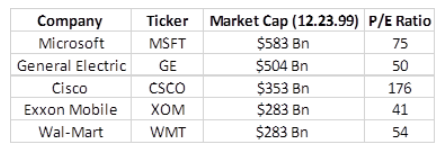

On the positive side, four of the five currently trade at less than 30 times earnings. Only Amazon is in the truly nose-bleed P/E category (69) but an argument could validly be made that its earnings are understated due to high levels of spending on growth initiatives. By contrast, in late 1999, the P/E ratios of the five largest stocks were much higher.

In fact, other than AMZN, the mid-point P/E of today’s “Fab Five” is not much out-of-line with the median P/E of the largest 30 members of the S&P 500. Once more excluding AMZN, their median P/E is 24 versus 21 for the top-30 overall. Consequently, from strictly a relative valuation standpoint, there doesn’t seem to be unusual risk in this elite group.

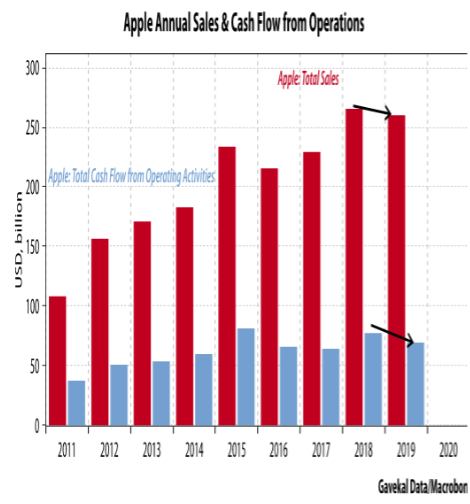

However, one could reasonably argue that with market caps averaging around $1 trillion, it will be challenging to generate enough profit growth to justify their price tags. Apple is particularly noteworthy in that regard. Its capitalization increase last year was $580 billion, more than the entire market value of any other S&P 500 company excluding Microsoft, Google and Amazon (and roughly equal to the total market cap of the smallest Fab Five constituent, Facebook.) Yet, its sales and cash flow growth has been lackluster in recent years.

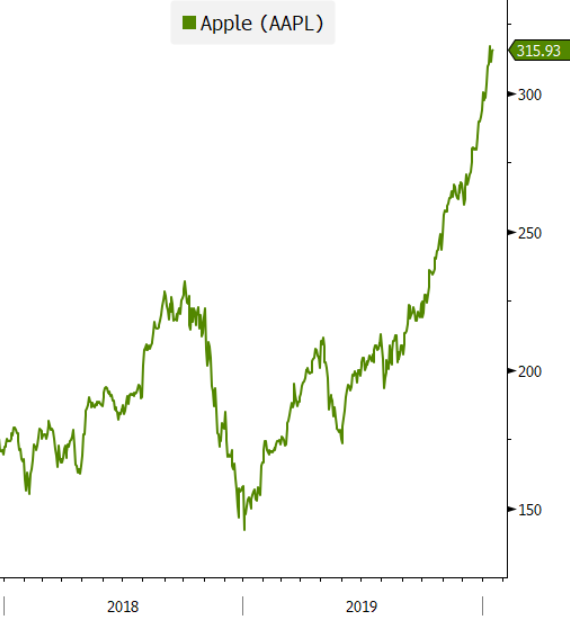

Looking at the below chart shows how extended Apple’s stock has become. The other Fab Five members haven’t had the same vertical price move, but they’ve still been in extraordinary up-trends. However, this isn’t a new phenomenon. According to research from Arizona State’s Hendrick Bessembinder, as reported in Barron’s, the entire return over T-bills globally since 1990 has come from just over 1% of listed companies. What wasn’t revealed was how much of that was a function of the phenomenal gains by US tech stocks over that timeframe. My guess would be a lot. The overarching question is whether this concentration of returns is sustainable AND, if so, will it be driven by the current Fab Five?

Source: Bloomberg, Evergreen Gavekal

What is the biggest risk facing investors over the next decade?

David Hay: A significant risk that almost no one is expecting these days, but I’m old enough to remember, is inflation.

My primary rationale for why much higher inflation is likely down the road relates to official and off-balance sheet federal government liabilities. With a gross debt (and gross it is) rapidly nearing $23 trillion, it is a painful reality that the US will be increasingly hard-pressed to service its IOUs unless interest rates stay low pretty much forever. However, the worst part is the “off-balance sheet” entitlements such as social security, Medicare, and Medicaid. Estimates vary widely but the aggregate number is probably above the present value of $50 trillion projected by the government itself. Many less-biased sources believe the all-in liability to be over $100 trillion.

As far as the current deficit is concerned, what’s particularly alarming is the trillion-dollar annual shortfall the US is running while the US economy is still growing. It’s disturbing in the extreme to think how much red ink the federal government will be spewing out during the next recession. An annual deficit north of $2 trillion is definitely possible, perhaps even probable.

Some politicians believe that taxes on the wealthy and corporations can be raised high enough to prevent a US fiscal crisis. The problem with this logic is that tax hikes of a size that would put a meaningful dent in the deficits, particularly including entitlements, would almost certainly crash the economy. Consequently, they would end up self-defeating. This is where the popular new economic concept of Modern Monetary Theory (MMT) comes into play.

According to this thesis, there is no need for tax increases; rather, the US government can spend and borrow all it wants since it issues bonds in its own currency. Should the bond market begin to balk at the torrent of debt offerings, the Fed can then once again crank up its magical money machine and purchase any bonds that can’t be sold to investors (at least at rates that don’t become prohibitive, thereby further exploding deficits).

As extreme and unlikely as MMT sounds, the reality is that the US government is already effectively engaged in it right now. Since October, the Fed has created hundreds of billions of its digital money (technically known as reserves) and is ploughing that into buying newly issued T-bills which are being sold to partially fund the aforementioned $1 trillion (and change) deficit. Lately, the Fed has been financing over 100% of the federal shortfall.

For now, this process isn’t having a major impact on inflation. Eventually, though, given the scale of debt monetization the Fed will likely be facing to finance massive deficits – and the far more massive entitlement expenditures – its well-oiled printing press will look irresistible to politicians.

Many pundits I read are calling for the next ten years to be the second coming of the Roaring ‘20s. My worry is that, when all is said and done, they will have been unwittingly referring to the upcoming decade’s rate of inflation.

Mark Nicoletti: If you were a student of financial markets but only had the last ten years of data, you would conclude that all an investor has to do is stay passive and simply buy the market index. In this vacuum, clearly, passive market investing is superior to active portfolio management.

However, I believe complacency and the return of normal correlations and economic fundamentals are the twin elephants in the room. Distortions are not a new phenomenon near market peaks, but I fear the eventual fallout from this particular top could be one for the record books.

Let’s start with this: every single asset class was up double-digits last year (or at least within a hair of it!).

Let that sink in for a moment.

U.S stocks, European stocks, Japanese stocks, emerging markets, high-grade corporate bonds, high-yield bonds, gold, treasuries – all of ‘em.

I think we’ll get a serious reversion to the mean in terms of asset class dispersion in 2020. I feel confident predicting that ‘just be long everything’ won’t work again this year as an investment strategy.

I won’t blame central bank money printing operations for the abnormalities. I’d never do that without clear evidence…

With correlations so high, benchmarks are outperforming active money managers at a disturbing clip; one that defies simple statistical probability. These index benchmarks are outperforming because more and more money is leaving active managers - not because owning the benchmark means owning the best portfolio.

The real issue here for the average investor is that this new paradigm has not yet been stress-tested. It will be interesting to see how it fares as the investing environment shifts.

I believe this, along with other symptoms of extreme investor complacency, will be proven irrational at some point in the next 10 years. My concern, when the resumption of economic gravity occurs, is that the next bear market will be amplified in both severity and length, and not tempered by the Fed’s inevitable intervention.

The biggest danger from this particular set of dominoes toppling would be that faced by ageing investors who find themselves crowded into passive, equity-heavy portfolios at precisely the wrong time in both their own lives and the economic cycle.

To be continued next week...

Jeff Eulberg, J.D., CFP®

Director of Wealth Management

To contact Jeff, email:

jeulberg@evergreengavekal.com

Jeff Dicks, CFA

Director of Portfolio Management

To contact Jeff, email:

jdicks@evergreengavekal.com

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

Tyler Hay

Chief Executive Officer

To contact Tyler, email:

thay@evergreengavekal.com

Mark Nicoletti

Managing Director, Family Office

To contact Mark, email:

mnicoletti@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect the personal opinions of the listed Evergreen employee, and do not necessarily reflect the views of Evergreen Investment Committee as a whole. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Any opinions, recommendations and assumptions are as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation from Evergreen for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.