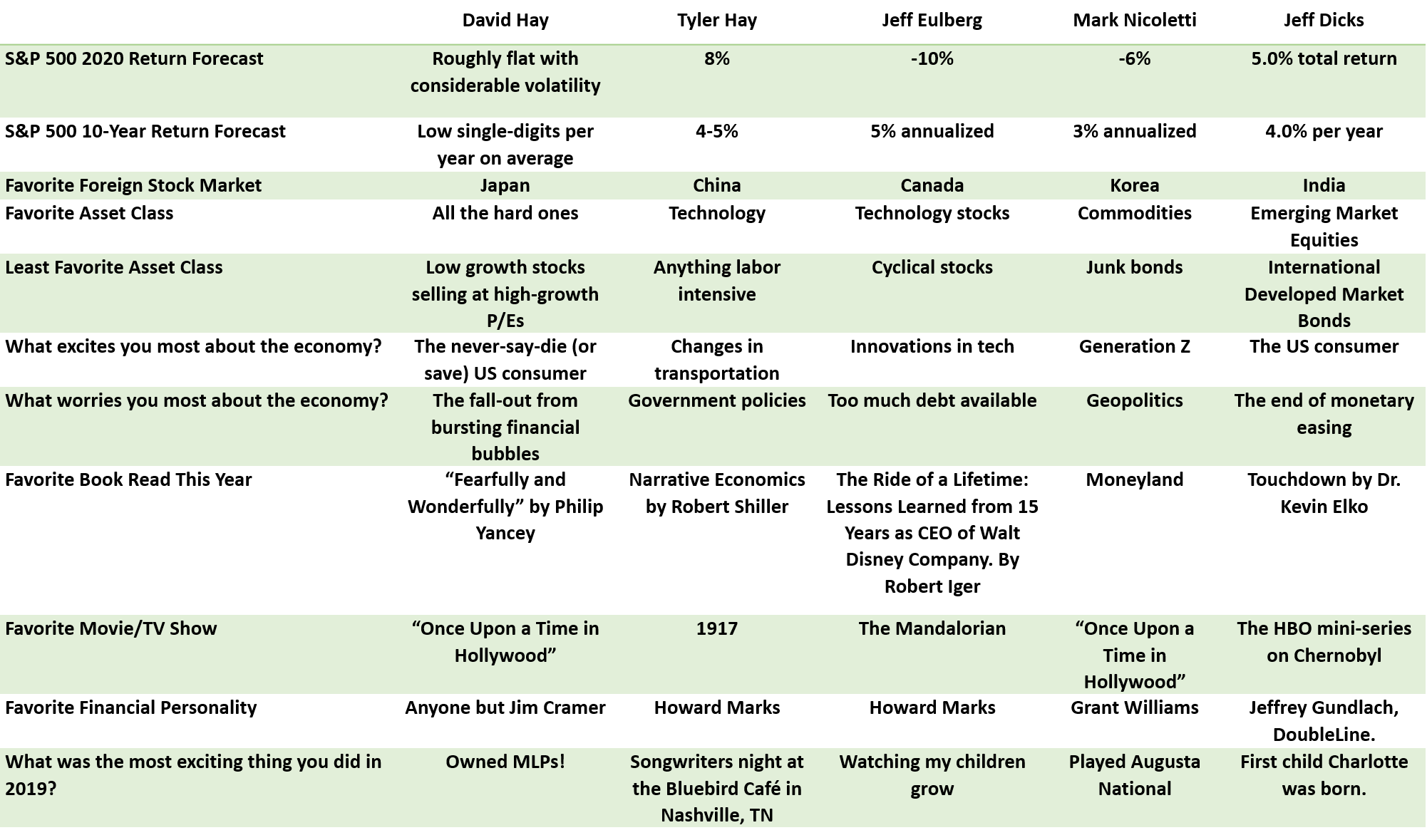

Last week, we kicked-off the first edition of a two-part series where our investment team looked back on 2019 and forward to 2020. This week, Jeff Eulberg (Director of Wealth Management), Jeff Dicks (Director of Portfolio Management), David Hay (Chief Investment Officer), Tyler Hay (Chief Executive Officer), and Mark Nicoletti (Managing Director, Family Office) continue to reflect on last year, while forecasting what may lay ahead for the rest of this year. As always, we welcome your feedback and appreciate your loyal readership.

Note: Evergreen Roundtable 2020 is running as a two-part series. The first edition of this series is available here.

Continued from last week...

What are your favorite investment themes for the upcoming decade?

Jeff Eulberg: The world can change awfully quickly. Therefore, when looking this far out (and in an effort to not look like a fool in 10 years), it’s wise to be conservative and select themes that are time-tested. I fear the next decade could lead to disappointing returns for public market investors who have successfully relied on passive indexing over the prior decade. However, within the public and private markets, there are areas that I believe can provide outsized returns in spite of what could be a tough decade for markets broadly.

Select private market investments in real estate and income may offer superior risk-adjusted returns. Specifically, real estate in certain West Coast markets. The economic growth in Evergreen’s backyard will undoubtedly continue. While pricey today, I have a high conviction that the total return on leveraged real estate in desirable West Coast markets will continue to be a smart investment.

For public market securities, there are two new “sin” markets in gambling and cannabis that could see rapid growth as they continue down the path towards legalization. However, today these are still very difficult markets to invest in due to evolving legislation at the state and federal level.

The theme that I would select over the next decade has been one of the leading investment themes the prior two decades: innovative technology. The coming decade will see monumental changes with the expansion of 5G, IoT and AI. Analysts believe over the next decade autonomous vehicle fleets could become a reality, dramatically altering how we use transportation.

Over the next 10 years, large global technology companies will continue to be good investments. Many of these firms have reliable cash flow and large moats around their client base. Thus, they’ll remain in a great position to spend on innovation internally or acquire the best new companies around the globe.

Jeff Dicks: There are three investment themes for the next decade I’d like to discuss. The three themes are data consumption and the Internet of Things (IoT), an aging population along with the increased need for passive cashflow, and the evolution of a shared economy.

Big Data/IOT: One the biggest themes I see over the next decade will be the massive growth in terms of data consumption. It’s estimated the amount of data traffic per smart phone will increase by 10x globally over the next five years. In addition, the number of devices connected to the internet will also expand rapidly. According to IoT Analytics, the number of “connected devices” will increase from 7 billion in 2018 to 21.5 billion by 2025. Note this ranges from consumer-related devices like appliances and electronics to industrial and enterprise devices like connected machinery and robotics. This data will need to be stored and analyzed in real-time. This will create tremendous opportunities across multiple sectors including data service providers, cloud services providers, data analytics companies, cloud computing firms, and cyber security companies, among others. 5G technology, the next gen mobile network, will also play a role. 5G will deliver improved network performance, add significant capacity, and improve reliability.

Aging Population: This one is rather simple. The global population is not only growing older, but people are living longer (though not in the US!). According to DBS Bank, the percentage of the global population over the age of 60 will increase to 21% by 2025 from just 12.5% today. This key demographic trend will lead to a higher proportion of retirees. As our world ages, the demand for passive cashflow investments will rise, which is likely to lead to a continued and amplified period of lower interest rates. One of our key themes across our portfolios over the next decade is cash flow generation. We strongly believe investments with high cashflow will outperform non-cash flow investments. I believe this will be true whether its dividend paying stocks, midstream energy assets, income producing real estate, or consumer- and corporate-related credit. In addition, volume plays on healthcare services are likely to see exceptional growth not only as the world ages, but also as emerging economies in Asia see their populations move from low to moderate incomes.

Shared Economy: This theme in recent history has been rapidly growing in momentum. Think of the shared economy in terms of UBER, or VRBO. Instead of owning a car I can call an Uber. Or instead of paying for a hotel room I can rent my house out and use the proceeds to take a vacation. Basically, using technology, usually via a web or app-based platform, you can facilitate peer-to-peer transactions. This is also known as collaborative consumption, and this idea really boils down to instead of an individual owning an asset or service, a group of people share access to that product or service. There are a tremendous amount of benefits to this concept including cost savings by sharing items, providing access to products or services at a lower cost, reducing negative environmental impact (think Uber pool), and simply creating more sustainable consumption patterns. On the latter, if a driverless car can take me to and from work along with ten other people, why would each of us need to buy a car? In addition, this allows our world to utilize resources at an improved rate, it creates jobs, and is more convenient for consumers. The future for a shared economy likely could include energy-sharing platforms or a shared internet model. Current uses like vacation rentals will continue to expand internationally and this theme will be a massive opportunity across emerging economies. The platforms and apps will improve as well, leading to an evolution of networking capable of finding and presenting relevant data to consumers and sellers. This likely further expands to areas like retail and personal property type items such as clothing or do-it-yourself construction equipment.

If the situation in the Middle East deteriorates further, what impact do you think this will have on markets?

Tyler Hay: Recent events, particularly with Iran, have shifted the eyes of the American investor back to the Middle East. Donald Trump ran his presidency on the basis of keeping American interests first and not sticking our nose into other nation's business. Until recently, he had done just that, with his main threat to Iran being economic sanctions. He broke this pattern when he ordered the assassination of Iranian General Qassim Suleimani. Some observers viewed this as a distraction tactic from pending impeachment inquiries by Democrats. Others viewed this move as a critical response from the US to figure out who has been responsible for undermining America’s agenda in the Middle East. Regardless, of your political viewpoints, it has changed the narrative in the region. The US has signaled to the world that it is willing to surgically strike those who stand in its way. Global financial markets waited anxiously for the Iranian response, which ultimately led to an airstrike on an Iraqi airbase housing US troops that resulted in zero American casualties. The question now remains: Was Iran satisfied with the response? The supposed unintentional downing of a passenger airline carrying nearly 200 innocent civilians, many of Canadian citizenship, further complicated matters. This catastrophe has drawn an outcry from young Iranians who are rightfully blaming the Iranian government. There are also growing reports that Iran’s cyber warfare capabilities have been increasing and, on Monday January 13th, the FBI issued an official statement warning of possible future attacks. If Iran launches cyber attacks that result in American bloodshed, I would expect a dramatic and precedent-setting military response will be made. Trump provided supporting evidence of this when he warned Iran that the US would target cultural sites should he deem their response disproportionate. As it stands currently, markets seemed to digest the Middle East tensions as transitory and oil prices stabilized. I do not think Iran is done and further escalations in the region could prove to be very disruptive, potentially lifting the prices of energy-related assets.

David Hay: It’s been a wild month in that regard. On Wednesday, January 8th, it looked like the Middle East was on the verge of all-out war, with the US in the thick of the conflict. Now it appears that the John Lennon “give peace a chance” mindset is on the rise—thankfully! Of course, the nagging question is if this is sustainable. Let’s face it, peace and the Mid-East go together like the NY Times and Fox News.

Frankly, Middle East politics are out of my small strike-zone. But my close friend and partner, Louis Gave, has studied this subject for decades, partially due to his grandfather once being the French governor of a portion of Syria after WWI (when the allies did ill-advised nation-creating in the region with little regard to common religions and cultures). Louis is quite concerned about full-blown civil war in Iraq that could potentially severely restrict oil exports, resulting in much higher crude prices.

On the positive side, there may be hope for détente between Iran and Saudi Arabia. Louis believes this is even more likely in the wake of America’s killing of the head of Iran’s ruthless Revolutionary Guard. The tragic loss of life caused by the Iranian downing of a Ukrainian jet leaving the Baghdad airport has put even more pressure on the Iranian regime, leaving it more willing to negotiate. In Louis’s words: “Just as the journalist Jamal Khashoggi’s brutal killing in Saudi Arabia’s Istanbul consulate in October 2018 put the Saudis on the defensive and forced them to pragmatically re-examine their regional policies, so will this tragedy do for the Iranians. Make no mistake—this is a significant, constructive turning point in Middle East politics.” (Note his emphasis on “constructive”.)

Louis summed up his essay on this topic with the following: “War with Iran is widely unpopular in America and won’t help Trump win re-election. The president himself said from his Mar-a-Lago resort as he announced the attack: ‘We took action last night to stop a war. We did not take action to start a war.’ It is worth remembering that the toppling of Saddam Hussein’s statue in Baghdad shortly after the invasion of Iraq in 2003 and the civilian uprisings in 2011, dubbed Arab Spring, were celebrated and covered by the media as a historic achievement for several months. In reality, both events led to a disaster of epic proportions. Today, we believe the opposite is happening. Global media is echoing warnings of mayhem and blood-curling destruction after Trump’s Iran strike. In truth, we are moving toward the brink of peace.”

Everyone sing together now: “Give peace a chance”!

If you had to buy one stock for the next 10 years, which one would it be and why?

Note: Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect the personal opinions of the listed Evergreen employee, and do not necessarily reflect the views of Evergreen Investment Committee as a whole. Investment decisions for Evergreen client accounts are made by the collective Evergreen Investment Committee. Any opinions, recommendations and assumptions are as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy.

Jeff Eulberg: As I mentioned in my answer to my favorite investment theme over the next decade, due to how quickly most things change, I tend to be conservative with these long-range answers. The first company that always comes to mind when I’m asked this question is Disney. Disney has world-class content that it has consistently monetized for multiple generations. Just this week, I was reminded of the company’s staying power as my kids were home from school on a snow day and I noticed my 3- and 6-year-old daughters watching "Alice in Wonderland" from 1951, all the way up to "Toy Story 4" released in 2019. And, as the media landscape shifts over the next decade with a focus on direct-to-consumer streaming, content will remain king.

Over the last 15 years, Disney has accumulated some of the strongest assets in media. The recent $71.3 billion-dollar acquisition of Fox, to go along with, Marvel, Pixar, Star Wars, ESPN and Disney’s internal library, has given the company an unmatched war chest to create new content. In my opinion, no company better monetizes their content through theme parks, licensing, and future spin-offs.

Disney’s new streaming service, Disney+, has exceeded expectations since its launch in November. As of early December, the service had 24 million subscribers. As Disney’s existing content licensing contracts expire with other streaming services, they’ll continue to add valuable shows and films to their streaming services. And, the competition will continue trying to catch up to the entertainment icon’s 70+ years of creating world-class content

Jeff Dicks: My stock recommendation for the next decade is Dell Technologies (ticker: DELL). Dell trades with a market capitalization of $36 billion, holds $8.5 billion of cash, and carries $54 billion in debt. Including minority interests in subsidiaries (less than 50% ownership), this works out to a total enterprise value of $87 billion. In 2019 alone, Dell is expected to generate nearly $6 billion in free cash flow (i.e. excess cash flow) or an estimated $6.47 earnings per share (EPS). This works out to a 16.7% free cash flow yield, or a price-to-earnings multiple of just 6.8x given a stock price of $50.26. From a valuation standpoint, the stock value of the company is extremely cheap. This is especially true when comparing to the rest of the technology sector, which trades at an average FCF yield of 4%, or 23.5 times 2019 estimated earnings.

The primary reason for the huge discount is the high amount of debt carried on Dell’s balance sheet. Dell has a history of acquisitions, and in 2015 Dell acquired EMC Corp for $67 billion. At the time, this was the largest technology combination ever and was primarily debt-financed ($50 billion of additional borrowing). The acquisition made strategic sense given Dell, primarily a tech hardware company, acquired EMC that along with servers, networking, and storage, added a faster-growing cloud computing and virtualization software component.

On the last point, the crown jewel of the EMC acquisition was the ownership stake in VMWare (ticker: VMW), which is the software side focused on the cloud and server virtualization. Today, Dell owns 81% of VMWare. That stake is worth north of $50 billion given VWM’s publicly traded market cap of nearly $63 billion. That $50 billion ownership value is worth 138% of Dell’s own market cap. Said differently, this is essentially valuing Dell and EMC’s legacy businesses with negative equity value.

If you exclude VMW, legacy Dell and EMC are generating $3 billion of free cash flow per year. These businesses include commercial and consumer PCs, and other hardware products such as monitors, along with servers, networking equipment, and storage solutions. Dell ranks #1 in almost every category, and the IDC (International Data Corporation) expects IT spending to grow at 4.1% per year. No doubt this is not the most exciting part of the technology sector, but it’s a cash cow, and even if you have slower growth there is considerable value in the cash flow over time. There is also a major value add, for Dell customers, when one company can handle nearly all their information technology needs.

Back to the debt side: since the EMC acquisition, Dell has paid down over $18 billion in debt, which shows they have a proven track record of rapidly paying down liabilities. It’s also worth noting that out of the $54 billion in current debt, $8.4 billion is from Dell Financial Services (which is backed by customer receivables), meaning core debt is closer to $45 billion. Additionally, in today’s world where executive comp is generally tied to earnings or cashflow - which can mean goosing those metrics at any cost - it is especially important to think about executive incentives. In this case, given the significant insider ownership, Mr. Dell is deeply incentivized to reduce debt as he currently owns 50% of the company. Shareholders should have some added peace of mind knowing management’s interests are closely aligned with their own.

Over the next three years, Dell should be able to reduce debt by an additional $12 billion due to their cash flow generation. As the debt gets paid down, it should enhance the stock’s market value. The valuation multiple applied to earnings, or sales, should also expand as the risk of the overall enterprise declines. In addition, with lower debt, you will see a boost to earnings as interest costs come down. There is also a potential for significant simplification where Dell and VMWare combine into one entity, which could remove any subsidiary discount that is implied by the market. We should also continue to see faster growth in IT spending relative to overall economic activity leading to long-term earnings growth for Dell. In three to five years, as debt gets paid down, the multiple expands, earnings grow, and a potential for an improved corporate structure, I think Dell could be worth 2-3x more than it is today. In 10-years I believe we could see the stock 3-5x higher.

David Hay: My stock to tuck away for the next decade is Enterprise Products (EPD). My recommendation presumes an investor is willing to receive a K1 which makes tax preparation slightly more cumbersome; on the positive side, 60% to 70% of the income is tax-sheltered. (Additionally, for more “mature” holders, that portion may become tax-free). EPD is structured as a Master Limited Partnership, or MLP (hence, the K1).

A key reason why I believe EPD will be a superior long-term investment is its current 6% distribution yield. This is over three-times what the average stock in the S&P 500 yields. Further, because I feel the overall US stock market is likely to produce little more than a 2% net return to investors over the next decade, having such a lofty cash flow is a significant tail-wind.

A prime benefit of owning EPD is the likelihood its payout will continue to rise as it has done every quarter for almost 14 years. Very few companies can make that claim. It has slowed its distribution growth down to around 2% in recent years in order to retain excess cash, thereby strengthening its coverage ratio (the amount by which distributable cash flow exceeds the payout) and allowing it to “self-fund” the equity portion of growth capital spending (such as building additional pipelines and/or energy export facilities.)

The last five years have been extremely challenging for the entire energy sector due to the collapse in oil prices that started in late 2014. This led to widespread financial stress and, even, bankruptcies among the energy producers that are customers of mid-stream entities. Many of Enterprise’s MLP peers have been forced to reduce their payouts as earnings and cash flow fell short of projections. Yet, EPD has continued to systematically increase its payout. Since the energy sector went into its long bear market in 2014, Enterprise has raised its distribution from $1.43 per unit (equivalent to per share) to $1.78. Over the same timeframe, earnings per unit have risen from $1.47 to an estimated $2.15 for full year 2019. Therefore, it now sells at just 13 ½ times earnings. This is near the lowest P/E ratio of the last decade (it has often traded at 20 times earnings, even in recent years).

The company indicates that it will continue to raise its distribution at about a 2% rate. This is roughly equivalent to inflation, meaning its 6% yield is effectively real or net of inflation. If anything, I believe its payout will increase at a faster rate than 2% going forward, particularly if inflation accelerates in upcoming years.

Enterprise is considered to be among the premier operators in the mid-stream energy sector. In my opinion, it has the most diversified mix of energy infrastructure assets in the industry and is particularly well-positioned to benefit from the rapidly growing business of exporting now abundant US oil and natural gas to an energy-intensive developing world. It also has one of the strongest balance sheets in the industry, carrying a solid investment grade credit rating of BBB+. Despite all of its competitive advantages and its proven history of growing through energy booms and busts, it remains 30% below its 2014 peak price.

The biggest risk, as with any energy investment, is that fossil fuels in general—and shale oil and gas in specific—become so highly regulated and/or heavily taxed that US production contracts rather than grows (as it has done in spectacular fashion over the last decade).

Mark Nicoletti: Although I was hoping to be asked about my outlook on all seismic activity for the next decade, I’ll have to settle for being assigned to pick a single stock winner. How thrilling, for me, really.

They say the past is the best guide to the future; so let’s take a look at the 2010s to see what was the best performing stock of the last decade.

The answer (surprisingly to some but less so to others) is Netflix, which soared +4,011%. Across the world, husbands like me, whose wives like to drag them to the movie theater, said a silent prayer of thanks for the company’s existence while NFLX investors of both genders popped the champagne corks.

Incidentally, for a little perspective, and to show that the last decade wasn’t perhaps as big an outlier as some metrics might suggest, Medifast (nutrition), +16,209% was the best performing stock for the decade beginning on January 1, 2000 (AAPL was a distant 2nd). Over the other tech-crazed decade, the 1990s, Dell, +91,863% was the best horse in what was the race-to-end-all-races.

So, with all that in the rear-view mirror, let’s look forward. For the Twenty Twenties (finally, after two decades without a proper name, one that works) I’m going to opt for a unicorn in a trillion dollar industry – a unicorn that’s never turned a profit (and won’t for the foreseeable future), Uber.

My grandmother is 94 and going strong. She has the Uber app on her phone; I put it there. I’d call Uber the most-likely-app-to-have-on-your-phone-even-if you-only-have-one-app app. The company has changed the way we get from place-to-place; and possibly only scratched the surface in changing the way we live.

Strategically, Uber must continue to grow revenue at the expense of profits. It’s the Amazon model: don’t let losses undermine the ultimate goal of world domination or, in this case, market preeminence.

The company is building up an ecosystem of services that make it less vulnerable to competition. It’s one of the market leaders in autonomous vehicles, which could be a growth lynchpin for the future. It also has the potential to turn itself into a bedrock advertiser, empowering brands with the massive amount of data it collects.

Caveats: leadership, competition, and regulation all pose challenges…oh, and it’s share price is down 25% since its IPO in May ’19 in a strong broad market.

To be sure, the WeWork debacle has made life a little tricky for unicorns and Uber may well be dragged into the fray, but the company remains my pick for the Twenties.

Jeff Eulberg, J.D., CFP®

Director of Wealth Management

To contact Jeff, email:

jeulberg@evergreengavekal.com

Jeff Dicks, CFA

Director of Portfolio Management

To contact Jeff, email:

jdicks@evergreengavekal.com

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

Tyler Hay

Chief Executive Officer

To contact Tyler, email:

thay@evergreengavekal.com

Mark Nicoletti

Managing Director, Family Office

To contact Mark, email:

mnicoletti@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect the personal opinions of the listed Evergreen employee, and do not necessarily reflect the views of Evergreen Investment Committee as a whole. Investment decisions for Evergreen clients are made by the Evergreen Investment Committee. Any opinions, recommendations and assumptions are as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation from Evergreen for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.