Special message: Before we get into the main text of this month’s full-length edition, I wanted to mention that we’ve had a format change. Our Points to Ponder (PTP) section, which also ran monthly, is now being replaced by a daily Tweet. To access those, please follow us @EvergreenGK. We will also be adding one PTP to our Daily that goes out to Evergreen clients. If you are an Evergreen client and would like to receive our Daily, please email Lindsay Hall: lhall@evergreengavekal.net.

We started it, but they’re finishing it. Twice in recent years, I’ve been fortunate enough to listen to famed demographer Neil Howe address John Mauldin’s Strategic Investment Conference (SIC) in San Diego. Neil’s talk stood out both times even among the star-studded array of speakers at the SIC. I was particularly fascinated by his presentation in 2013 in which he made a thoroughly convincing case for why this decade bears a remarkable resemblance to the 1930s.

As time has passed since then, domestic and global events have, in my opinion, further buttressed his thesis. The 1930s began in the shadow of a resounding crash in global financial markets at the end of the prior decade. Unemployment soared—as high as 25% in some countries—and stayed excruciatingly high for an extended period. The economic distress led to the rise of extremist political parties on both the right and the left.

During the ‘30s, the US attempted to avoid direct involvement as Europe and Asia hurtled toward the bloodiest conflict in world history. Most Americans preferred isolationism as the thunderheads of war assembled ever more ominously on the horizon.

Radical fiscal and monetary policies were implemented to stabilize the system and catalyze economic recovery. Complete state takeovers of the economy occurred in some countries. In America, the dollar was dramatically devalued versus gold while, simultaneously, bullion was made illegal to possess.

For a time, these measures seemed to be working, at least in the US, as GDP grew rapidly from the Great Depression trough through 1936 (the recovery then was immensely more robust than our current tepid expansion). Suddenly, though, a vicious second recession struck and the US stock market was cut nearly in half. To this day, many students of economic history believe the only reason the US exited the Great Depression was because of WWII.

Of course, there are many pronounced differences between today and the 1930s. Decisive action by global policy makers, particularly the US treasury and the Fed, prevented the chain-reaction meltdown of the banking system six years ago in vivid contrast to the early ‘30s. Consequently, US unemployment during the most recent global financial crisis never rose appreciably above 10%, much less over 20% as it did during the Great Depression. As we all know, the jobless rate has been consistently falling in recent years, despite the nagging reality that there are around 93 million working-age Americans not in the labor force (with another nearly 9 million unemployed but seeking work).

Yet another striking parallel with the 1930s is that phenomenon known as “currency wars.” This is where a given country seeks to boost its own growth rate by effectively stealing market share from its trading partners via currency devaluation. One of the primary ways this is accomplished is through the now infamous process known as quantitative easing (QE).

Ironically, given current conditions, the US was the first major country to employ QE to combat the ravages of the Great Recession. This cheapened the dollar and caused other nations to react angrily to this overt attempt to “beggar thy neighbor.” Emerging countries were particularly incensed as the flood of cheap dollars triggered unsustainable booms, especially in commodity-oriented economies. It also led to some $9 trillion being borrowed in dollars by emerging market companies as these entities sought to capitalize on the trashing of the greenback.

Authorities in countries like Brazil rightly worried that the boom would be followed by a bust and that ultimately its private sector might suffer yet another currency crisis by essentially having a massive short position in the dollar. Certainly, based on what’s happened over the last couple of years, those fears were exceedingly well-founded.

Like in the 1930s, currency wars have also led to deflation. Just consider Japan and think of it as a company that competes in almost every important global market. Since 2011, it has effectively cut its product prices in half by fabricating hundreds of trillions of yen (the equivalent of trillions of US dollars). As often noted in prior EVAs, this has forced competitors from countries who have not debased like Japan has to cut prices. This is an extremely painful process; consequently, almost every other nation has lately opted to lower the value of its own currency either by cutting interest rates (if they weren’t already at zero) or by doing some form of QE.

The exception—and this is where the ironic part comes in—is none other than the US of A. The once reviled buck has kicked the derriere of almost every other currency over the last few years, including that which is considered to be the ultimate store of value: gold.

As this deflationary trend has accelerated, it has produced another 1930s-like development: Interest rates have been largely eradicated; 16% of government bond markets around the world now have negative interest rates. Even among most of the other 84%, yields are so low as to be meaningless. The 30-year sovereign German bond recently went below 1%. In this case, we’ve outdone the ‘30s. Even then, rates never plumbed such Lilliputian levels.

Consequently, the US, with comparatively generous yields of over 2% on its 10-year sovereign debt, is once again a magnet for capital, elevating the dollar and causing America to be a victim of the currency war we initiated. If you haven’t noticed, the muscular greenback is one of the main reasons earnings estimates for the S&P 500 have been slashed dramatically lately.

As usual, though, the US stock market is about as alert as Justice Ginsberg at the State of the Union.

Yellen it like it is. Over the last couple of years, I’ve become an unabashed fan of Mike O’Rourke, Jones Trading’s Chief Market Strategist, and his pithy daily, The Closing Print. (If you are an institutional investor who would like to email Mike to receive his TCP, please click here.)

Mike recently dug up the following little gem from a speech that our current Fed chairwoman gave back in 2010, when QE was in its infancy: “Those who sounded the alarms were seen as killjoys who refused to join the party. Words are important, but clearly they are not enough. We need strong policies to back them up. We need macroprudential policymakers ready to take away the punch bowl when the party is getting out of hand. We know that market participants won’t take kindly when limits are set precisely in those markets that are most exuberant, the ones in which they are making big money.”

Ms. Yellen was referring to the excesses of speculative manias past and calling for the Fed, and other policymakers, to discard the standard “see no bubble, hear no bubble, speak no bubble” approach the powers-that-be have taken in the past, at least over the last 30 years. As Mike points out, she was channeling the spirit of one of the greatest Fed chairman of all time, William McChesney Martin, Jr., who in a speech back in 1955, stated that our central bank needed to be “in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.”

Despite Ms. Yellen’s call for “strong policies” to prevent investors’ animal spirits from kicking into hyper-drive, we now have a situation where, for years, the chaperone has been pouring more Everclear into the punch bowl. And, once again, I find myself among the dwindling number of killjoys who refuse to join in the festivities, at least at this late stage of the revelry. As you can see to the right, it’s been one whale of a shin-dig since Ms. Yellen uttered those words on October 11th, 2010.

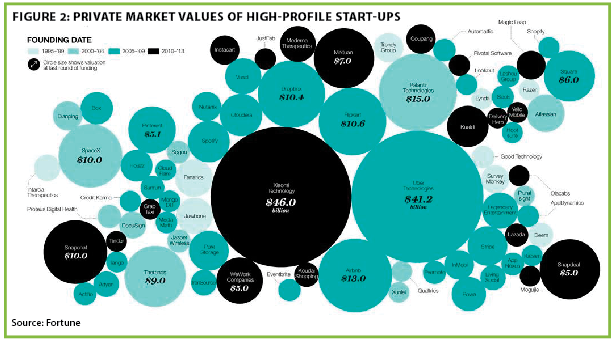

Admittedly, the chaperone quit dumping in the hooch last fall, but there is plenty of spiked punch still left in the bowl. Meanwhile, some new escorts—the Bank of Japan (BOJ) and the European Central Bank (ECB)—have picked up where the Fed left off. Money, being highly portable, has migrated from Japan and Europe, causing further asset price inflation in the US. An extraordinary new example of that is the multi-billion dollar values being placed on start-up companies that haven’t yet gone public. Talk about bubbles, bubbles, everywhere!

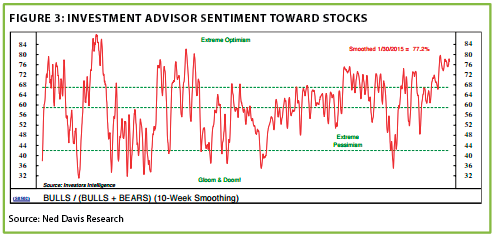

Despite this obvious manifestation of overheated market conditions, I keep reading that a key reason stocks should continue to rise is that investor sentiment is not overly exuberant. In fact, a Merrill Lynch piece just came across my desk making exactly that assertion. Yet, how do you get astronomical valuations on the above assortment of promising, but fledgling, companies if sentiment isn’t ragingly bullish? And, according to the cerebral folks at Ned Davis Research, that’s exactly what we have on our hands these days.

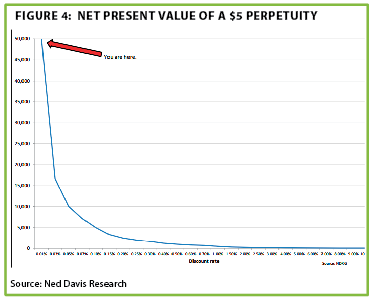

To be fair, the bullish argument, as conveyed by an EVA reader responding to last week’s issue, is that with interest rates at sub-atomic levels, almost any valuation can be justified. In other words, using the standard discounted-to-present-value calculation, when you use a near-zero interest rate—or increasingly, a negative rate—no price is too high. As celebrity economist David Rosenberg has pointed out, 90% of the industrialized world’s economic activity is tethered to short-term interest rates of zero—or lower! Accordingly, as shown in Figure 4 on the next page, again per the Ned Davis brain trust, the sky’s the limit when it comes to valuing current cash flows when rates are nonexistent (the simple equation for this is Net Present Value of a Perpetual Cash Flow = Cash Flow divided by the discount or interest rate).

Now, if all of the above isn’t enough to sound some alarm bells at the Fed, what will it take? NASDAQ 10,000? Rather than coming forward with “strong policies,” not just “words,” the Fed is agonizing over removing a single innocuous word—“patient”—from its forward-guidance language.

It’s quite clear that the reason the Fed is so reluctant to say that their patience is wearing thin is because “we know that market participants won’t take kindly when limits are set precisely in those markets that are most exuberant, the ones in which they are making big money.” Frankly, the Fed is terrified of how unkindly those participants may react despite Ms. Yellen’s earlier—and totally correct—contention that it is essential for a responsible central bank to intervene when conditions become this bubbly (or preferably before).

As we’ve seen during the tech and housing bubbles, no policymaker—best intentions notwithstanding—wants to be caught holding the pin in his or her hand when the big bang happens. As a result, asset prices are left to continue on their seemingly endless journey to infinity.

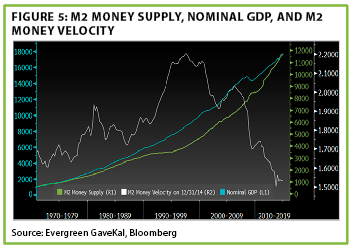

A Tale of Two Velo-cities. It’s been quite awhile since we’ve covered the vital topic of money velocity. Accordingly, I thought it would be helpful to return to a theory developed by one of my true heroes, Charles Gave. This is because I believe his thesis holds the key to why we find ourselves in this nonsensical world of non-existent interest rates, non-stop asset price inflation, and non-responsive economies.

To briefly review Charles’ “Two Velocities” concept, the normal velocity referred to in the world of economics is money velocity; the other, per Charles, is financial velocity. The first is what impacts the real economy as it measures how much GDP increases relative to the rise in the money supply. More money sloshing around in the economy should create more growth. At least that’s the way it used to work...

In recent years, though, the multi-trillions conjured up by the central banks have had minimal impact on the real economy because, as shown in Figure 5, money velocity has done a convincing imitation of the Greek stock market. In fact, Merrill Lynch now believes global GDP will actually shrink by $2.3 trillion this year, at least in US dollar terms. This is shockingly poor considering that there have been 514 monetary easing actions by central banks around the world over the last three years.

On the other hand, this unprecedented liquidity infusion has had a truly massive effect on financial instruments. This brings me back to that relic of the 1930s—currency wars.

When a country launches a mega-QE, the first domino to fall is the currency, and currencies these days are very much financial instruments. As mentioned earlier, this amounts to a price cut in the goods and services said country exports. Other nations then feel compelled to similarly depreciate their own monetary unit. Thus, deflation begins to spread around the world, a very 1930s-like scenario.

But, unlike during the Great Depression, when QEs were not employed, the tsunami of central bank funny money has flooded into financial assets, driving stock prices up and bond yields down (rising bond prices by definition lower yields). Other asset prices—like real estate, art, collector cars, first-edition books—also have been caught up in the great tidal wave.

Unfortunately, at the corporate level, money that would normally flow into productivity-enhancing investments—new computers, robots, etc.—instead is largely diverted into dividends and stock buy-backs. Consequently, productivity suffers. As John Taylor (creator of the famous Taylor Rule for the Fed funds rate) noted this week in a Wall Street Journal Op-Ed, productivity over the last five years has been expanding at just 1% annually versus the 2.5% average of the prior twenty years.

Since economic growth is a function of productivity plus labor force expansion, this is a huge hurdle to overcome in order to get back to a normal growth rate. This is especially true since, as Dr. Taylor points out, the percentage of the population working or seeking work is below where it was at the end of the Great Recession! There are now roughly 102,000,000 employable Americans not working, amounting to three-quarters of the total who are employed.

To compensate for these growth impediments, central banks encourage rapid debt increases through their ultra-low interest rate policies. Sadly, though, much less GDP is generated per unit of debt created than in the past. Additionally, the higher debt levels mean that the global financial system becomes more fragile.

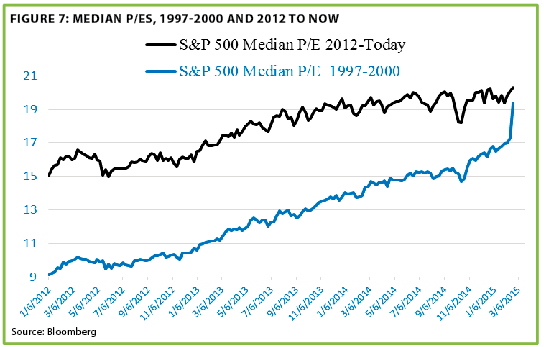

For a time—in this case, a very long time—financial markets rejoice as the abundant liquidity drives prices higher and higher. Meanwhile, the “killjoys” become fewer and fewer. It’s all good until something goes wrong, as it always does. The extreme valuations create just as extreme downside risk. As you can see, again courtesy of Mike O’Rourke, the median stock is selling for a higher P/E ratio than it did in 2000, despite the blow-off surge that occurred at the beginning of the new millennium.

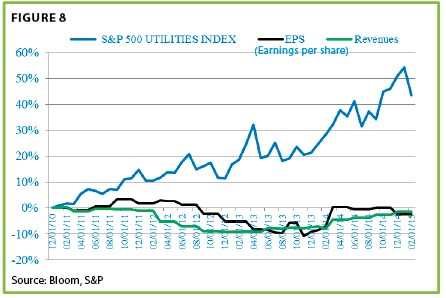

Thus, financial markets don’t reflect economic velocity but rather financial velocity. Drawing one last time on Mike’s excellent daily, the utility sector is a classic case of this divergence between stock prices and underlying fundamentals.

Ok, it’s unhealthy and unsustainable but as a loyal EVA reader and Evergreen client recently asked, in so many words: "When will reality bite?"

Don’t know when but maybe why… Geez, I hate questions like the one from our client, particularly since I’ve been so “premature” on when the tide will finally go out. But Charles and I both believe credit spreads are crucial in that regard. Encouragingly for the bulls, the difference between what Corporate America and the government pay to borrow money has come down lately after the big bust-out from the lows seen last summer. It will remain to be seen if spreads are done widening but, if not, stocks will have a hard time ignoring the competition for investor capital caused by even higher yields.

Additionally, economic velocity may also trigger a nasty mean reversion, in the dual meaning of the word “mean.” Some pundits have speculated that the Fed, and other central banks, can simply allow the trillions they’ve created to stay in the system forever. This also means they will theoretically never sell the enormous portfolio of bonds they’ve accumulated with their fabricated funds. Is it just me or does that sound too good to be true?

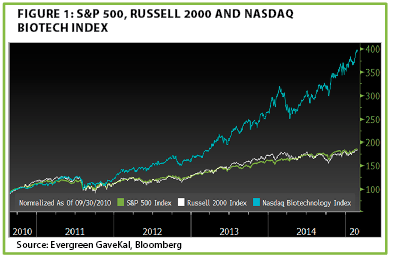

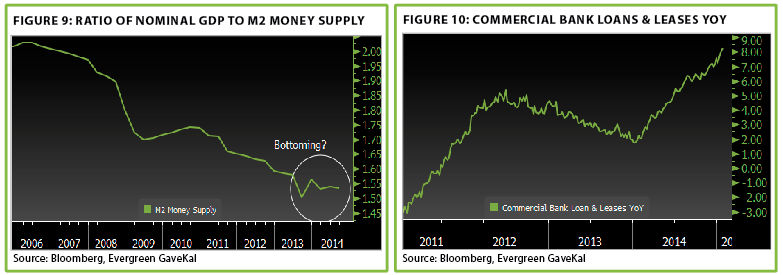

What happens, again theoretically, if the standard measure of money velocity begins rising? There is some evidence of that already happening, at least in the US. Loan growth logically should lead velocity and its chart is beginning to resemble the biotech index.

If velocity really is turning (we are reserving judgment on that for the time being) and the Fed doesn’t start draining at least some of the excess trillions they’ve created, inflation could become a very serious problem, as unlikely as that seems right now. With the Fed currently owning around 50% of the entire Treasury bond market with maturities of 10 years or longer, any aggressive liquidation program could prove exceedingly disruptive.

On the other hand, currency wars are pushing in the other direction, with all the deflationary effects mentioned above. If deflation continues to be the dominant trend, we’ll almost certainly continue to see interest rates stay at virtually invisible levels. If so, asset prices may remain at their dizzying heights until gravity finally kicks in for some reason almost no one can predict. (However, my money would be on vaulting credit spreads caused by the type of deflationary bust we’ve seen in the energy space hitting other sectors.)

Conversely, if it becomes clear the Fed has fallen behind the economic velocity curve, with inflation finally stirring from its long slumber, interest rates could spike for a time. Ultimately, though, the financial market panic this would create should quickly bring yields back down, as was the case in 1987, 2000, and 2008. The damage to the economy from another asset bubble implosion would, of course, not be a pretty sight.

As we’ve written before, the Fed has printed itself into a very tight corner where there is no easy exit. It started the currency wars and America may soon learn that these are just as expensive as the shooting kind.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.