“When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

-JOHN MAYNARD KEYNES referring to market bubbles.

Vertigo isn’t just a Hitchcock movie. Is your head spinning? Wasn’t it just a few weeks ago when the UK said “see ya, wouldn’t want to be (with) ya” to Europe and global markets were in free-fall? I’ll be the first to admit I’m feeling decidedly disoriented these days. When I am in “what-the-hell?” mode (I’d use another similar phrase, but this is a PG-rated publication), I try to steady myself by reflecting on thoughts from my partners Charles and Louis Gave.

But before discussing their current views, I want to give a hearty hat-tip to Ned Davis Research’s Vincent Deluard whom I’ve quoted in recent weeks. Vincent absolutely nailed it when he was among the very few to view Brexit as a bullish development and for exactly the right reason: Central banks gone even more wild. For the raging bulls out there, I’ve got some good news: Vincent believes there is much more upside to come as the market has broken out to a new all-time high. Based on today’s facts, I think he’s right—despite extreme overvaluation. The reality is, valuations matter almost not a whit on a short-term basis.

The not-so-good news is that he also feels this blow-off surge will ultimately lead to the next market disaster. This is despite his suspicion the S&P may surprise most pundits with how high it goes before the cliff-dive moment.

Vincent’s longer-term concerns are a good segue to the musings from Charles and Louis. As I’ve noted before, both father and son Gave are genetically pre-disposed to being bullish so it’s not reasonable to ignore their rising concerns on grounds of being perma-bears. Also, while Charles has been worried about stocks for the last year or so, he’s been pounding the proverbial table on long-term treasury bonds. And just this year alone, the rocket ship known as the 30-year T-bond has screamed 22%, leaving the US stock market choking on its contrails.

While noting the surprising upside verve the financial markets have shown since Brexit, Louis is afraid investors have become too reliant on the continuing incontinence of central banks. He sees limitations on their largesse going forward and he’s particularly worried about the high-expectations for the Bank of Japan (BOJ). If you missed it, former Fed Chairman Ben Bernanke has been meeting with senior Japanese officials this week. Rumblings are that he has suggested the BOJ embrace Milton Friedman’s mythic “Helicopter Money” strategy. This entails a central bank buying government bonds with fabricated funds. Said government then issues checks directly to its citizens with the hope the money will be immediately spent. (Given the average Japanese citizens’ legendary thriftiness, this is a questionable assumption.) Key to this is that the bonds bought bear no interest and have no maturity; i.e, permanent debt monetization, a most risky gambit.

In Charles’ case, he is primarily concerned that long periods of short-term interest rates below inflation leads to economic stagnation. This is also reflected in stocks underperforming bonds, as noted above, a phenomenon that has been in place since 2000, despite the recent rally to new highs by stocks. He further points out that when silver has been besting equities for at least 18 months, as has also occurred, it’s another reflection of misguided policies, eventually leading to trouble in stockland.

So, for now, go with the flow but betting on safe income—like MLPs and other high-yielding issues that still offer value—strikes team Evergreen as a much more rational way to ride the wave.

David Hay

Before we get into the main section of this week’s EVA, I wanted to thank all of you who responded to our message concerning the appalling killings of an attorney for the US-based non-profit, the International Justice Mission (IJM), as well as his client and their driver in Kenya last month. If you missed the chance to send a digital petition to Kenya’s president protesting these murders, almost certainly by the local police, please click on this link. Also, the New York Times article highlights the international out-cry and pressure that is building on the Kenyan government and its notoriously corrupt police force.

By Louis Gave

Let’s face it, few expected the rally in global risk assets of the past ten days. Even investors who, like Charles, believed that Brexit was a fundamentally positive development did not expect positivity to erupt quite so suddenly. Yet, here we are, with the Nikkei up 10% since its post-Brexit low, the S&P 500 breaking out to new highs and the Shanghai benchmark above 3,000. Even more surprising is how, in this rally, bond yields almost everywhere have registered new lows, while gold has also done decently well. In short, the only way not to have made money over the past two weeks was to be parked in cash.

Unfortunately “waiting in cash” was what most investors in the immediate pre- and post-Brexit periods chose to do. So perhaps all we have witnessed was the ultimate “sell the rumor, buy the fact” rally. Since most investors were defensively positioned, and because the markets are set up to make the largest number of investors look foolish the most number of times, a typical “contrarian rally” has unfolded, leaving egg on almost everyone’s face. That, at least, would be the hopeful explanation. The more worrying explanation is that investors are positioning themselves for another round of intervention. And the reason this concerns us is that, if true, investors are either set up for a disappointment, or alternatively for a jump into the unknown. Indeed, as we look around the world, we find:

In the US: there is, at this stage, limited appetite for a new round of easier monetary or fiscal policy. After all, the Federal Reserve was supposed to be hiking rates this year, not injecting new liquidity into the system. More importantly, the US economy, as the latest payrolls data showed, is still chugging along decently well. Hence, there would seem to be little justification for a new round of monetary or fiscal policy easing.

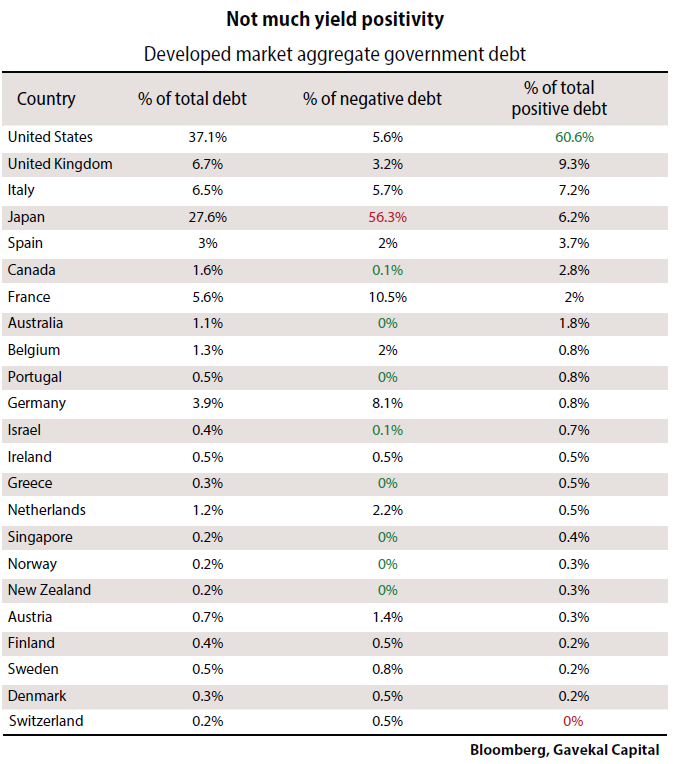

In Europe: arguably, this is where easing should take place. But as recent years have shown, the only European actor capable of action, even when things get really bad, is the European Central Bank (ECB). Indeed, absent a “major” crisis, the nature of European decision-making ensures that bold action never happens. So if any substantial stimulative measure is to come from Europe (and allowing Italian banks to limp a little further as the walking dead is hardly game-changing) the ECB will have to be the source. The problem is that yet more negative interest rates would surely bury banks and insurance companies? And is not quantitative easing constrained by self-imposed limits set by the ECB for its monetary policy activism? Indeed, can 26% of the ECB’s purchases continue to be German bonds as required by the “capital key” stipulation given that such assets are required to yield not less than -40bp? After all, with 90% of outstanding German bonds now offering negative yields, the ECB’s room for manoeuver is tighter than a Scot’s wallet.

In China: stimulus has been the order of the day all year. And now, with service industry growth at about 10%, construction bouncing back, real estate prices making new highs, consumption holding up and exports still gaining market share, it is hard to imagine that a Chinese government currently making noise about supply-side reform and retiring excess capacity will ante-up for another stimulus round.

This leaves us with Japan where investors seem to have gotten excited on the back of Ben Bernanke’s visit to Haruhiko Kuroda and Shinzo Abe this week. And perhaps this explains our current discomfort; for if the markets are rallying on the premise that Japan is set to do something big and bold then we are left pondering the following:

Will the coming months be the time when Japan breaks its 25 year form in disappointing foreign investors by delivering above and beyond ramped-up expectations? To be clear, I have lost money so many times in the past two decades on the premise that Japan’s policymakers were set to embark on a bold new set of policies that I now have, engraved on my desk, a plaque with the words of wisdom of an old friend who taught me “lesson #1: never underestimate the pain that Japanese people are willing to take if they take it together, and lesson #2: never underestimate Japanese policymakers’ ability and willingness to dish out that pain”.

If Japan is to act decisively, what concrete options are available to the BoJ? Already, it must buy government bonds totaling ¥120trn ($1.2 trillion USD) in the fiscal year of 2016 if it is to meet its target of expanding the monetary base by ¥80tn ($800 billion USD). However, net Japanese Government Bonds (JGBs) issuance is expected to be about ¥46trn ($460 billion USD) in the period and taking into account the stock of JGBs that the private sector can unload, the Japan Centre of Economic Research estimates that the limit of QE will be reached in the middle of next year (which probably explains why Kuroda disappointed the market a few months ago and did not expand QE). So the boundaries set by QE mean that if the BoJ is to do something substantive it will have to be “something else” other than QE. Which brings us to the biggest question of them all:

Is Japan set to embark on helicopter money? Helicopter money is undeniably more egalitarian than QE (which is welfare for the rich), and in that regard could also prove more effective in boosting economic activity (though perhaps not asset prices—after all, if helicopter money triggers higher bond yields, a number of asset prices could come under pressure). The real problem with helicopter money is how and when it is stopped. If it is successful, politicians will outbid each other in promising ever bigger payouts. And if it is not successful, then, like every other Keynesian measure, the conclusion taken will be that the medicine is sound, but not enough was. Indeed, any adoption of helicopter money opens up a genuine Pandora’s box. And while we do not pretend to understand the psyche of BoJ or Ministry of Finance staffers, it seems unlikely that such drastic action would be adopted right after an election victory for Abe and at a time when the economic situation is not “so bad”. Surely such measures are more likely to be adopted “pre”, rather than “post” election? Putting it all together, is it not more likely that Abe in the coming weeks announces a large stimulus bill that includes more defense spending, pre-Olympic construction projects and the like? And if that’s the case, is that enough to warrant a massive rally in global bonds, equities and precious metals?

In short, is the enthusiasm displayed by investors in the past two weeks the same as that displayed by turkeys getting an extra dose of feed on December 23rd? As we see it, either Japan does pull a rabbit out of its hat, in which case we can probably expect a continuation of the current outperformance of “jewels” vs “tools” (see Tools Or Jewels?) and to see the rush for yield to continue unabated (especially in emerging markets as that rush for yield still has room to run). Or Japan plays to form and disappoints, in which case OECD government bond markets will likely pull back from today’s crazy valuations, thereby dragging other overvalued assets lower.

By Charles Gave

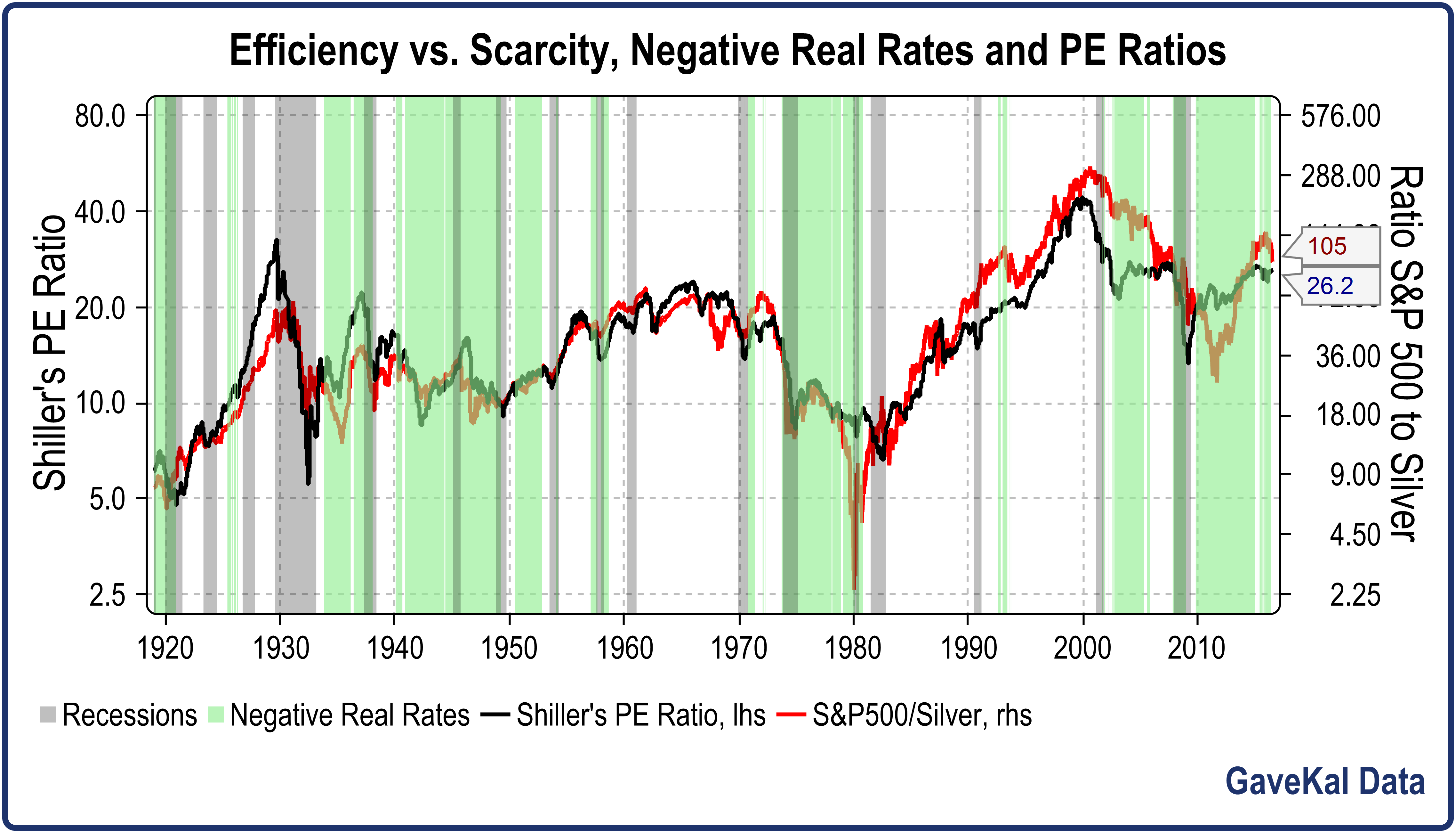

As everyone knows, value can come to an asset either because it aids efficiency (a tool) or because it is scarce (a jewel). By nature, scarcity does not lead to economic growth, only improvements in efficiency does.

Let us assume that I am going to use silver as a proxy for scarcity (gold started to float freely only in 1971) and the S&P 500 as a proxy for the efficiency value in the US system. Then a ratio between the stock market index and the price of silver would give me a ratio of efficiency versus scarcity. If this ratio is going up, it must mean that the economic policies followed by the US are conducive to economic growth. If the ratio is going down, the reverse must be true.

When economic activity is perceived as being favorable for years to come, something strange happens in the stock market: P/E ratios go up, a sign markets are slowly, but surely, expanding their time horizon. In other words, this reflects durable confidence.

So in a perfect world, we would have a strong relationship between the ratio S&P vs. Silver and the long- term evolution of P/Es, in the US stock market. And we do. If I take the Shiller CAPE (the Cyclically Adjusted P/E, a smoothed form of the classical P/E ratio), the relationship is extremely tight with a correlation rate of around .9 since 1920.

To know if prevailing economic policies are correct, I simply use the real interest rates on 3 month T- bills. When they are negative (euthanasia of the Rentier)*, the graph is shaded green. Good economic policies lead to higher P/Es, bad economic policies to lower P/Es. Amazing…

As one can see, every time a Keynesian** policy is followed, silver starts to outperform the S&P after a while and, as long as we have negative real rates, the P/E ratios go nowhere or down (though there can be some fleeting counter-trend improvements). The decision rule I follow is fairly simple: If silver outperforms the S&P for 18 months in a row, then I am quite certain P/E ratios will start a structural decline. For the last 18 months, silver has outperformed the S&P by 13%, so we have probably started a structural decline in P/E ratios. And the potential contraction starts with the P/E ratio (CAPE version) at a hefty 26 times.

Roughly, for every point decline in the P/E, earnings will have to go up by 4 % for the market to remain stable. Yet, as an aside, earnings have declined by 4 % annually over the last two years. So, the market has risen a modest amount over the last two years but only because of P/E expansion, not profits increases, probably due to the decline in US long-term interest rates. This P/E inflation did NOT prevent the stock market from underperforming silver for the last 18 months, however.

Once again, I find that negative interest rates are a disaster, as are increases in government spending to “stimulate” growth. The fact that these two absurdities are pushed forwards by central bankers all over the world just shows that they can be as incompetent as French generals, which we already knew.

It also shows that these fellows do NOT have a scientific mind but a religious one, dominated by fervently held, but non-fact based, theories. And when a theocracy takes over the ruling of a Nation, the end results are always bad, except of course for the high priests.

*I.E., savers being punished with returns below inflation.

**Typically associated with “easy” money.

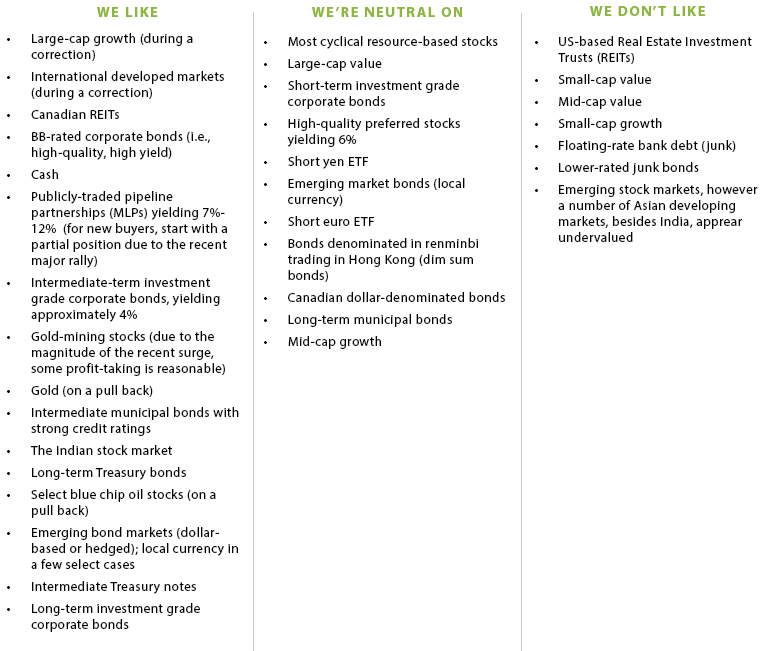

OUR CURRENT LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.