“Witnessing the Republicans and Democrats endlessly bicker over the US debt is analogous to

watching two drunks argue over the bar bill on the Titanic.”

-READER GARY CARLSON in a letter to the editor of the Idaho Statesman

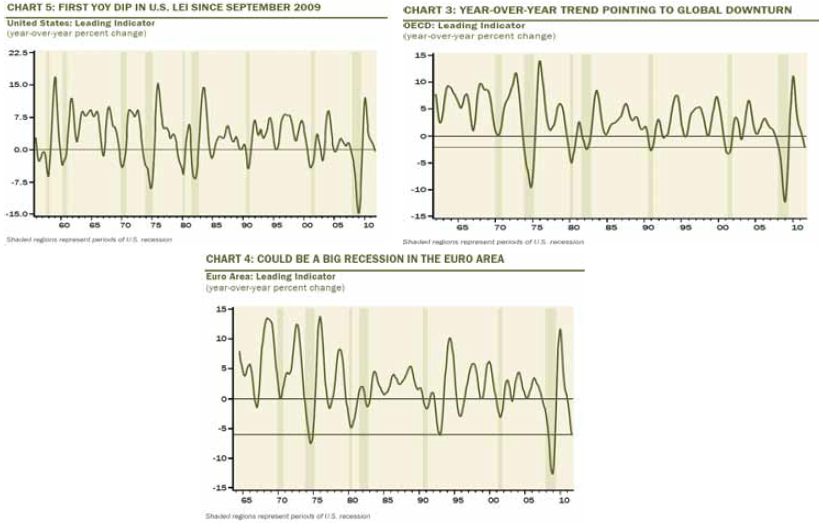

1. While Wall Street economists appear increasingly convinced the US economy is picking up steam, leading indicators are not supportive of that view. For all OECD countries (the world’s wealthiest nations), the message is the same, with Europe likely already entering into yet another serious contraction.

2. Better jobs numbers have definitely been behind much of the improved tone in US economic data. However, the comprehensive Gallup “underemployment rate” was at 18.1% in November, up from 17.2% a year earlier.

3. Obamacare promises to be a focal point of the upcoming presidential race and Romneycare in Massachusetts gives us a sneak preview of what might lie ahead. “Tax-achusetts” now spends $9,278 per resident on health care coverage, 36% above the national average. On the positive side, only 5% of Massachusetts residents are without health coverage.

5. US taxpayers’ anger toward public employee unions is understandable given the ongoing revelations of flagrant abuse. For example, more than 90% of retirees from the municipally run Long Island Railroad claim to be disabled, even those with desk jobs, inflating their annual pensions by $36,000. Similarly, a remarkable 82% of California state troopers become disabled in their last year prior to retirement.

6. One of the more bizarre outcomes of the immense growth in US entitlements is that they have disproportionately flowed to less needy Americans. The Congressional Budget Office has determined that the poorest 20% of households received 54% of federal transfer payments in 1979; in 2007, they received a mere 36%. Medicare, with its exploding expenditures on middle- and upper-income recipients, is cited as a key reason.

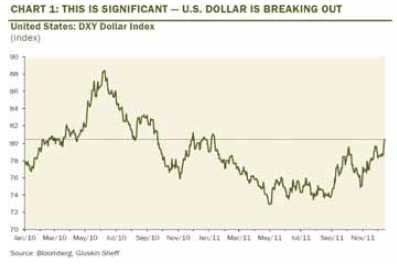

7. Negative sentiment against the dollar, and in favor of commodities, hit fever pitch in the spring, as evidenced by the fact that April saw trading volume in the silver ETF exceed that of the S&P 500 ETF. Since then, the dollar has been on a tear and appears to be in the process of a major upside breakout while commodities have been pounded.

8. One of America’s most underappreciated assets is the enormous investment its leading companies have made in research and development. GaveKal Research estimates that in the last decade the US corporate sector has created $12 trillion in “intangible” capital, such as intellectual property. As an example, GaveKal cites Facebook, which may soon have a market value that amounts to $50 million per employee.

9. US real estate continues to be one of the main casualties of the continuing deleveraging cycle, but a definite bright spot is the multi-family space. A key reason for this comparative health is that 1.3 million more households are renting than a year ago. To put this in perspective, over the entire decade prior to the Great Recession, the ranks of renters rose by just 500,000.

10. A year ago, a high-profile analyst terrified the municipal debt market with dire warnings of widespread defaults. This caused investors in tax-free mutual funds to flee en masse. As is often the case, Evergreen took a contrarian position, arguing in several EVAs that munis were a buy not a sell; subsequently, they went on to be one of 2011’s top performers.

11. While most state governments are increasingly showing budget discipline, national governments continue to destroy their credit ratings at the same time that they need to raise mind-numbing amounts of money. In 2012, OECD countries must finance a collective $10.5 trillion of debt, counting both new funding needs and the rollover of existing debt. As Europe is proving, financing on that scale can be highly problematic.

12. It’s hard to imagine a political elite more coddled than our own, but in Italy politicians even at relatively low levels of government enjoy lofty salaries as well as hefty retirement benefits after just a few years of service. Additionally, even though America has five times the population, there are 600,000 official cars in Italy as opposed to 75,000 in the US.

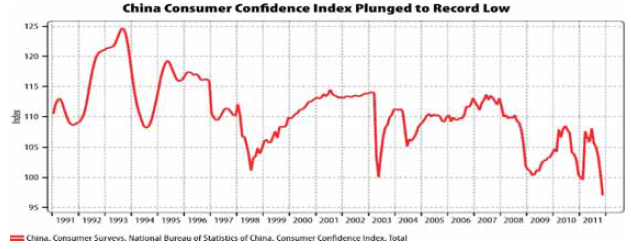

13. Adding to the persistent flow of cautionary data emanating from China these days, Chinese consumer confidence has slumped to a record low.

14. Europe’s problems are admittedly overwhelming in number, and a truly effective and comprehensive set of solutions is almost unimaginable. However, its stocks are now trading at just 12 times the average of the past decade’s earnings. In contrast, US shares are selling at a P/E ratio of around 20 on this basis.

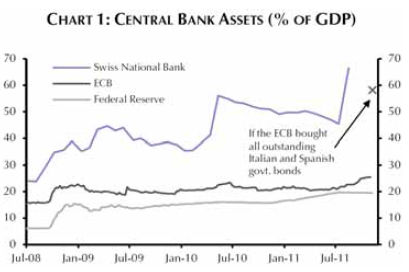

15. Switzerland is perceived as a bastion of hard money policies, yet its central bank has let its balance sheet inflate to almost 70% of GDP as it tries to prevent the Swiss franc from rising further against the euro. Consequently, even if the European Central Bank created 3 trillion euros, enough to buy up the entire Italian and Spanish bond markets, its balance sheet would still be smaller as a percentage of GDP than that of the Swiss National Bank.

Happy Holiday!

IMPORTANT DISCLOSURES: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.