“Anyone who isn’t confused, clearly doesn’t understand the situation.”

-EDWARD R. MURROW, journalist and war correspondent.

In the cross-hairs of cross-currents. One of our main objectives in publishing the Evergreen Virtual Advisor (EVA) is to offer readers both our views and those that contradict them. Part of our rationale for doing so is that we realize how easy it is to be wrong when making predictions, especially about the future, as Yogi Berra would often say. This fallibility confession is despite the fact that our long-term forecasting record is pretty respectable including warning of past bubbles in tech, housing, Chinese stocks, commodities, among other manias we’ve called out over the years, well before they crashed. We also issued bullish commentary post-9/11 and, particularly, in the midst of the global financial crisis.

On the embarrassing side, we have been expecting the US stock market to have a deeper and more lasting shakeout than it has experienced since 2013, even though the broad market index (NYSE Composite) has gone nowhere for almost three years. That admission is actually a good segue into this month’s edition of the Gavekal EVA which was written by the co-founder of our partner firm, Anatole Kaletsky.

Anatole has been resolutely bullish on US stocks throughout the Obama years, meaning he’s been spot on. Lately, though, he was been expressing some reservations due to rising political risks. One of those, in the months leading up to November 8th, was supposed to be the potential election of Donald Trump. Yet, as we all now know, that wasn’t a risk at all—unless you are talking about the upside variety.

Last week’s Guest EVA featured commentaries by Bill Gross, Lacy Hunt, and Van Hoisington, three of the world’s shrewdest bond investors. They were united in their views that Trumponomics would not produce a major bear market in bonds. Yet, as you will soon read, Anatole takes the opposite view.

Interestingly, he concedes that the man who is considered by many to be the new “King of Bonds”, Jeff Gundlach, is back in the camp of calling for rates to recede, at least temporarily. This is after he predicted both the recent bond sell-off and Trump’s election, two very prescient prognostications. Longer-term, though, Mr. Gundlach and Anatole are each looking for much higher interest rates, somewhere in the 5% to 6% range on treasury notes. It’s important to clarify that they believe this will play out over time, not overnight. Jeff Gundlach thinks this potential rate surge might take five years to unfold while Anatole is postulating it might be sooner, like 2018 or 2019. Even the latter scenario is extended but, regardless of the timing, a rate increase of this magnitude would pose some serious challenges for a number of reasons, as expressed in recent EVAs.

First, assuming the rest of the world remains at suppressed rates, a dramatically widening yield gap is almost certain to send the US dollar screaming higher, as Anatole notes. This both lowers inflation and inhibits economic activity, reactions that are likely to occur much earlier than at the 5% yield level on the 10-year T-note. In my humble opinion, Anatole is underestimating the hefty counterweight this provides against an inflationary boom scenario.

Then, there is the stock market. As Anatole also points out, US stocks are quite pricey presently. The ability of equities to withstand a doubling of rates from here without experiencing a brutal shake-out—with the attendant feedback into consumer spending and sentiments—is highly questionable.

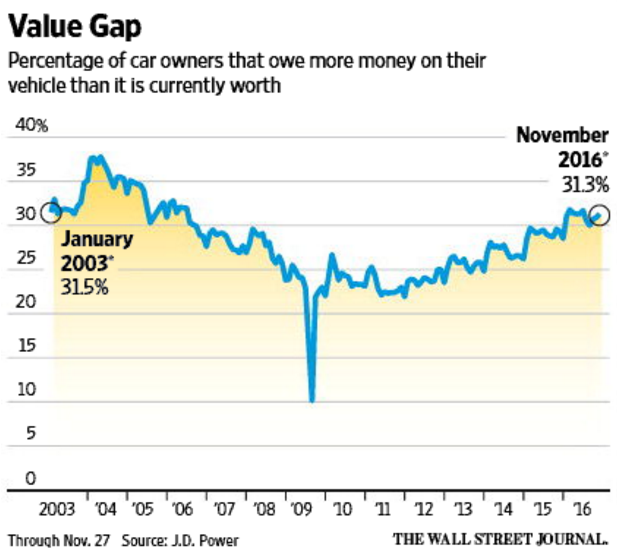

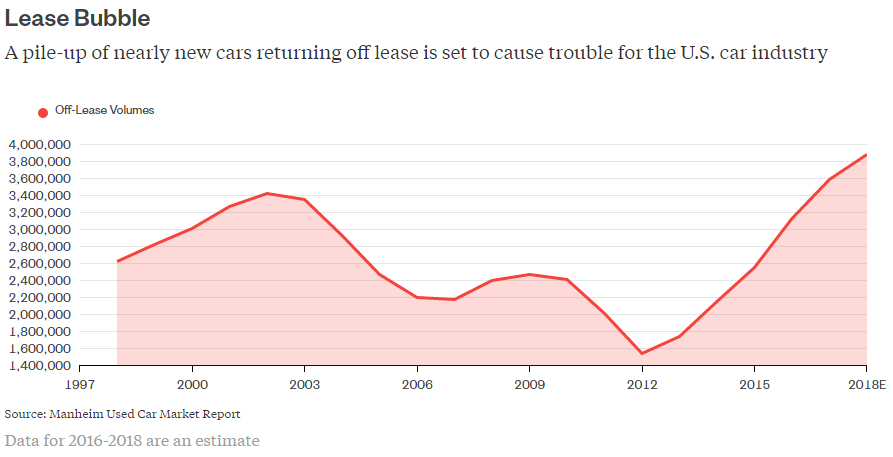

Next, is the big two of household spending: cars and houses. Both are obviously harmed by a significant pop in the cost of money and each is displaying signs of late-cycle fatigue. Auto lenders are already dealing with a rapid rise in dud loans (delinquencies on sub-prime loans are the highest since 2010). To keep things moving—and delay loss recognition—they are increasingly resorting to rolling the debt incurred on prior purchases into the next transaction. The result often is negative equity on the new vehicle. There is also a looming mountain of metal coming off lease over the next two years, threatening to inundate the used car market. Meanwhile, housing was looking winded even before the affects of the recent big leap by mortgage rates.

Finally, per Anatole, emerging markets (EMs) are already suffering, as evidenced by weak stock, bond, and currency markets in most of the developing world. A further jump in the dollar and US interest rates will only intensify the pain and suffering in EMs.

Of course, despite the above factors, as well as numerous others, Anatole and the growing legion of bond bears could be right. Perhaps the most compelling argument is that the combination of the business community now having a more bullish view of the future, along with tax reform and regulatory rollbacks, could ignite a self-perpetuating boom that overrides the negative impact of much higher interest rates. Moreover, the inflationary boom outcome might be accentuated if Congress allows a blow-out in deficit spending.

Clearly, there are lot of ifs and maybes in the foregoing paragraph. Additionally, Mr. Trump’s mercurial nature calls into question how pro-business he truly is. Two recent examples are his PR wars against both Carrier and Boeing, notwithstanding the political points he gained in each case. (It’s noteworthy that Carrier has announced a 5% price hike on its HVAC equipment as a result of the higher costs it will be absorbing). Mr. Trump is also threatening to go after the pharmaceutical industry in a Time magazine interview. Maybe I’m wrong, but those don’t seem to me like actions that make companies feel inclined to open up their coffers to expand operations.

The overall maelstrom of warring forces—some growth-enhancing and others growth-retarding—is making what was already an extraordinarily confusing investment environment even more so. Many of these new trends are an extension of the growing populism racing around the world, with Italy the latest example of that reality. There is a lot that I don’t understand about current conditions but I’m fairly certain rampant populism and a frothy stock market aren’t likely to peacefully co-exist long-term.

Now it’s time to let Anatole make his case for why the bond bull born under Reagan may be headed to the slaughterhouse under Trump.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

By Anatole Kaletsky

More than three weeks have now passed since Donald Trump’s election and, as Louis noted on Monday, many of the market trends that we discussed immediately after the election have now stalled. Louis concluded from these reversals that maybe investors had got too excited about what I called “the biggest economic regime change since at least the 1980s” and that the familiar conditions of global deflation would reassert themselves before too long. This is also the view expressed in a widely-quoted interview by Jeff Gundlach, who has navigated the global markets as skillfully as anyone since the financial crisis.

Nevertheless, I disagree. The idea that over-excited commentators exaggerate the power of politics to influence financial reality appears to have been supported by the stalling of many “Trumpflation” trades, and also by the market rebound after the Brexit vote. But on closer inspection this idea is not true. While broad equity indexes have proved surprisingly indifferent to the Trump and Brexit shocks, in each case there was one asset that moved in spectacular fashion. In Britain, the political shock expressed itself through the exchange rate, which fell faster in the weeks after Brexit than at any time since 1992. In my view it has still not stabilized, despite last month’s counter-trend rally, which itself was largely a consequence of the even greater shock of November 8, and thus emphasized the way that politics can dominate economics. The financial impact of the Trump election has been even more spectacular, since it has transformed conditions in the world’s biggest and most liquid market. US bonds suffered their biggest monthly fall on record after November 8 and this collapse, even more than the post-Brexit sterling sell-off, looks like just the beginning of a long and profound trend.

As these cases clearly show, political events can sometimes have a much greater impact than the monetary and economic “fundamentals” that investors normally consider more important. Now that the dust is settling and a (slightly) clearer picture is emerging of the Trump presidency, it seems worth reviewing the seven main investment conclusions I advanced on November 10.

First and foremost, Trump will cause a shift in US growth, inflation and interest expectations. US bond yields will rise sharply as monetary policy tightens and growth and inflation accelerate. This has certainly happened since November 8, but I believe the trend has only just started and has years, if not decades, to go. Nominal GDP growth seems bound to accelerate, with both stronger activity and higher inflation—and not just because of a one-shot burst of fiscal stimulus. Even more important is the change in the philosophy of economic management. Trump and his proposed Treasury secretary Steven Mnuchin appear ready to overturn the taboo against deficit financing imposed by Congress on Barack Obama’s administration and to shift the main objective of monetary policy away from controlling inflation, and towards supporting growth and creating jobs. This change in philosophy has been so widely discussed since the election, and the bearish sentiment about bonds has become so universal, that many investors are now turning contrarian and looking for a chance to buy back bonds. This seems to me a big mistake. Contrarian thinking works when a trend is turning. But once a trend has become established, it is better to be a follower than a fighter, especially if the new trend could last for many years. The election of Trump and the switch from anti-inflationary monetarism back to Keynesian demand management probably marks the end of a 35-year bond bull market that began in 1981 and culminated in what was arguably the greatest speculative excess in financial history: institutional investors stampeding to buy US$13trn worth of government bonds with negative yields. Even if the US government does not repeat the inflationary mistakes of the 1960s, a normalization of long term interest rates, as fiscal policy supplants monetary policy as the main instrument for economic stimulus, would mean treasury yields rising to around the growth rate of nominal GDP. With Trump shooting for 3% real growth and the Federal Reserve surely willing to tolerate inflation of 2-2.5%, the implication would be 10-year rates well above 5%. This is a prospect that few investors can imagine even in their worst nightmares, yet it was the normal state of affairs in the years before 2008.

A second question I addressed on November 10 was whether rising US bond yields would result in higher bond yields all over the world. My view was—and still is—that the European Central Bank, Bank of Japan and Bank of England will continue with their zero interest rate and quantitative easing policies for at least the next year or two, thereby creating spreads between long-term interest rates in the US and in Germany or Japan on a scale not seen since the 1980s. This has indeed begun to happen and, like the US bond bear market, I believe this trend still has much further to run.

This leads to a third trend highlighted after the election: that the US dollar would strengthen, contrary to our earlier belief that the US dollar bull market had ended in late 2015. The main reason for expecting a stronger dollar under Trump was the enormous spread-widening implied by his macro policies. A second reason was the US$3trn of dollar-denominated debts accumulated in emerging markets from 2008 onwards. If US interest rates begin to rise more rapidly and cause a dollar breakout beyond the highs tested in 2015 and early 2016, the result would be a short squeeze in emerging markets—and a further rise of the dollar in the sort of self-reinforcing process that produced rampant dollar strength during the emerging market debt crises of the early 1980s and late 1990s. The strong dollar thesis played out well immediately after the election. The DXY index rose 4.5% in two weeks to hit a 13-year high on November 24, and parity against the euro seemed inevitable. But in the past few days, the dollar has weakened slightly and the euro has bounced fairly convincingly from the floor of its 2015-16 trading range. It now looks as if the euro may gain a respite. Even if Sunday’s Italian referendum forces the resignation of prime minister Matteo Renzi, a banking crisis in Italy will probably be averted by a new technocratic government. By next year, however, a breakout by the dollar from its current trading range will again become a threat, as Europe faces the potential shock of a victorious Marine Le Pen demanding a referendum on Frexit.

Fourthly, emerging markets are the obvious victims of a rampant dollar, especially in combination with the new policy paradigm of US protectionism replacing globalization. This was another implication of the Trump presidency that played out well in the week after the election, when the MSCI EM index fell by -7%. Since November 15, however, this index has rebounded and is now down less than -5%. This may suggest that the Trump effect has faded, but the true explanation is more interesting. Investors have started to distinguish between EMs seriously threatened by protectionism and a dollar short-squeeze, and those that are relatively immune. Relatively protectionist economies such as Russia and India have seen asset appreciation in the last couple of weeks, while highly indebted economies with a strong dependence on global trade growth such as Mexico, Turkey and Indonesia have plunged into severe bear markets with no end in sight. This was exactly the discriminating behavior I suggested after the election, but it has happened much sooner than expected. And it leaves open the possibility that all EM assets could be caught in a more severe and indiscriminate sell-off if the dollar does break out of its trading range or if the Trump administration starts to put tariffs and trade restrictions into effect.

Fifth, the euro zone is threatened by the Trump election even more obviously than EMs. This is not because of Trump’s economic policies but because of the precedent he set for political upheavals. This expectation was initially justified by the fall in the euro and European stock markets and by the widening of periphery credit spreads. But like the EM panic, the politically-inspired sell-off in European markets has been quickly reversed. The next big test will come on Monday, after the votes in Italy and Austria, but it now appears that European assets will be less blighted by political uncertainty than expected three weeks ago. One possible explanation for this improvement in sentiment towards Europe may be the emergence of two unexpectedly pro-market politicians—François Fillon and Manuel Valls—as the center-right and center-left candidates for French president. Whether this will be sufficient to overcome fears that Marine Le Pen will win and demand the breakup of the euro or the European Union remains to be seen.

Sixth, the relative performance of US and global equities will be transformed by the Trump presidency. Before the election, it seemed likely that non-US equities would outperform in a broadly benign risk-on environment, because the US monetary and profit cycles were moving in a less benign direction, while the cycles in Japan, Europe and emerging markets were all lagging the US by several years. After the election this cyclical catch-up seemed less likely for two reasons. Firstly, the environment for equity valuations will generally be far less benign if US interest rates now rise as dramatically as expected and if globalization is called into question, even though many US cyclical stocks depend on domestic demand and may benefit to a significant extent from the new policy stance. Secondly, dollar strength and protectionism will be powerful headwinds for emerging markets, while political uncertainty will threaten the eurozone. The one major region not affected by any of these problems may be Japan. In fact, Japanese equities benefit unambiguously from a strong dollar. So far Japanese equities are up 8% in yen terms since November 8, which is almost exactly equal to the yen’s decline against the dollar. But the yen is now cheap enough that Japanese equities should do well by global standards even without any further depreciation.

Finally, should we expect generally better equity performance in the business-friendly world of President Trump than under proto-socialist Obama administration? This seems unlikely. With Wall Street already at an all-time high, profit margins near record levels, the business cycle in its seventh year, wage pressures growing and bond yields rising, US equities are already “priced for perfection”. US multinationals are certainly not priced for the threat of protectionism and the most unpredictable upheaval in global economic management in at least a generation. The enthusiasm on Wall Street for faster growth, tax cuts and monetary normalization that inspired a 3% rally in the two weeks after Trump’s election, may prove as misguided as the despondency that caused the S&P 500 to plunge by 5% in the week after Obama was re-elected in 2012. As it turned out, the two years that followed Obama’s re-election were among the best ever for equities, with uninterrupted gains that added up to 43% by the end of 2014. President Trump seems unlikely to do so well—at least for Wall Street.

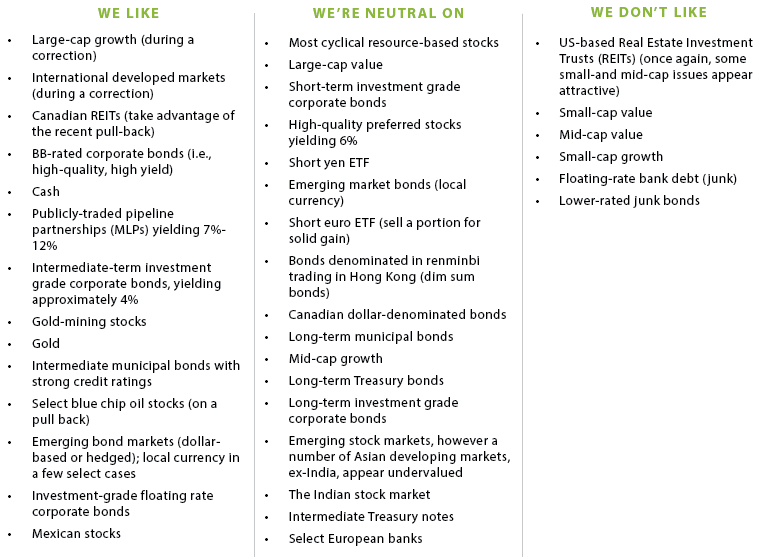

OUR CURRENT LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.