“In so many areas of life, you need to be a long-term optimist but a short-term realist.”

-CHELSEY “SULLY” SULLENBERGER, the pilot who safely landed US Airways flight 1549 in the Hudson River, saving all aboard.

Bye-bye buy-backs? First of all, Happy 2017 to all our EVA readers! Hopefully, the coming year will provide an opportunity for those few remaining contrarians out there—amongst a swelling throng of passive investors—to generate respectable profits and nail down some attractive yields. It’s also my hope that what I’m going to convey next won’t severely undercut the happy New Year sentiments I’ve just expressed.

There are few subjects as incendiary as Donald Trump. Consequently, a prudent newsletter writer would steer clear of making pro or con comments about our president-elect. However, the reality is that the set of policies he’s proposing are potentially the most market-moving and economy-impacting we’ve faced since the early Reagan years. Thus, we have felt compelled to examine the possible implications of his “Contract with America”, as well as some of its fine print.

Now here’s the part that might upset a large number of EVA readers: Evergreen likes some of what The Donald has proposed while having serious qualms about a number of his other ideas. We say this realizing that there are many—maybe most—of you who either love or hate everything he’s suggesting. But we believe that such binary views are either too optimistic or too pessimistic. As almost always, the reality is likely to reside somewhere in between.

For example, last week’s Guest EVA issue challenged the notion that adding an extra $7 trillion to our national debt—over and above the current horrifically irresponsible trend-line—is a good thing. Even if that red ink binge was partially devoted to an aggressive infrastructure build-out or refresh, we’d still have qualms about it—unless the projects were very carefully chosen and wisely financed. Moreover, since “only” about $1 trillion is hypothetically ear-marked (sorry about the pun) for infrastructure, that means we’d be adding $6 trillion to our national debt for much less productive reasons.

On the positive side, we do appreciate the growth-boosting potential of a sweeping tax reform effort. In numerous prior EVAs, we’ve long railed against the insanely complex and productivity-inhibiting nature of our current tax code, both for individuals and corporations. We believe the promise of a dramatic tax overhaul is one of the main reasons the stock market has been so effervescent since the election. Wall Street analysts are already playing what-if games with earnings estimates for 2017 and beyond, assuming that a major reduction in corporate tax rates occurs. It’s actually perceived to be a double gift to Corporate America, with not only lower tax rates on future earnings but also the potential of a lightly-taxed repatriation of past profits that have been sequestered overseas for many years.

In this month’s Gavekal EVA, we are once again highlighting the joint analysis of Will Denyer and Kai Xian Tan. When it comes to US economic and financial trends, Will and Kai Xian are Gavekal’s two primo authorities. In the highlighted Gavekal Ideas piece, they directly address the implications of the prospective corporate tax code revisions, particularly the profits-repatriation aspect. Wall Street currently is salivating over what that could mean for both earnings and stock prices, with the assumption, on the latter issue, that companies will use these returning funds to buy-back their own stock.

For those of us who have been worried for the past several years about stocks being overvalued, buy-backs have been one of the main reasons—if not THE main reason—they have defied gravity. Share repurchases have been running at around $500 billion annually for the past five years, a truly staggering sum and a huge prop under stock values. Accordingly, anything that will maintain these—or even accelerate them—is almost automatically bullish for the stock market.

As you will read, Will and Kai Xian both question this consensus view. Their reasoning is based on the twin realities that corporate earnings have been falling while companies’ leverage has dramatically increased. They also focus on an element of the proposed tax code revision that has been largely overlooked: the potential disallowance of interest deductibility. As Will and Kai Xian note, if this happens it will take away a key factor for why companies have preferred to use debt over equity to fund operations—not to mention the aforementioned splurge on reacquiring their own shares.

Will and Kai Xian point out that S&P 500 companies are now spending nearly all of their earnings on buy-backs and dividends. Reinforcing this, Barclays recently stated that this “payout ratio” is now over 100% of available (i.e., free) cash flow that Corporate America generates.

As a result, they believe the big surprise in all of this is that while companies undoubtedly will use some of the money returning from abroad for share repurchases, most of it will go to debt pay-downs. If so, this is likely to produce a nice tail-wind for corporate bonds as it means both increasing demand and shrinking supply.

It’s not a cloudless horizon for corporate debt, however. As they point out, should a recession occur, corporate credit spreads (the difference between government and private sector borrowing costs) will expand, perhaps dramatically. And as observed in numerous past EVAs, we believe spread-widening and-contracting episodes exert powerful influences on both stocks and the economy, with the former almost always a painful event. However, should companies start to aggressively deleverage, this might mean that, in the next economic downturn, corporate bonds hold up even better compared to stocks than they usually do during adverse times. Sorry, I forgot we don’t have those anymore—at least in the equity market.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

By Will Denyer, Tan Kai Xian

With the incoming US administration promising big tax breaks on the repatriation of corporate cash piles held overseas, Wall Street is confidently predicting a renewed equity market buyback boom in 2017. On first hearing, this sounds like a reasonable expectation. For one thing, in recent years US companies have consistently chosen to plough their retained earnings—and a sizable amount of debt—into share buybacks, rather than into investment in new capacity. For another, the last time US corporates were offered a repatriation tax holiday in 2004, of the roughly US$300bn brought back onshore more went to fund buybacks than was used for any other purpose.

However, while new tax breaks will no doubt trigger some buyback activity, we are skeptical that a fresh flood of cash repatriation will lead to anything like the buyback bonanza big banks expect. This is not 2004. Today both cyclical and structural factors are aligning to dissuade companies from launching big buyback programs. On the cyclical side, earnings growth has slowed and leverage ratios are high, both of which suggest that the peak for buybacks and special dividends has now past. Moreover, on the structural front, the new US leadership is proposing changes to the tax code that will reduce the tax advantages of issuing debt over equity, and which, if enacted, are likely to lead to a secular decline in buyback activity.

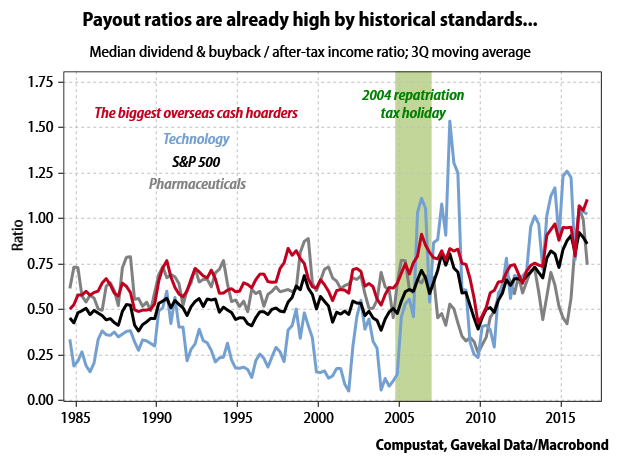

The cyclical story is relatively straightforward. Looking at both the income statement and balance sheet of corporate America, there is little scope for a further increase in buyback activity, but plenty of room for it to “normalize downward”. To some extent this is already happening; the estimated aggregate value of buybacks declined over the second and third quarters of 2016. However, because this downturn has coincided with weak earnings, the median payout ratio (dividends + buybacks / after-tax income) remains high by historical standards—at 86% for the S&P500. A further fall in buybacks will be needed if the ratio is to is to normalize towards its long-term average of 56%.

Nevertheless, Wall Street’s sell-side is hoping that a flood of repatriated earnings will give the buyback binge a new shot in the arm next year, which is what happened when the last repatriation tax holiday was declared in 2004. We have our doubts. In October 2004, when the two-year holiday began, the median payout ratio was modest—just 45% for the S&P 500—which left plenty of room for it to shoot up over the following quarters. But with the median payout ratio today at 86% for the S&P 500, and over 100% for the 30-40 companies sitting on the biggest overseas cash piles, such a sharp increase in payout ratios looks unlikely this time around (see the chart below).

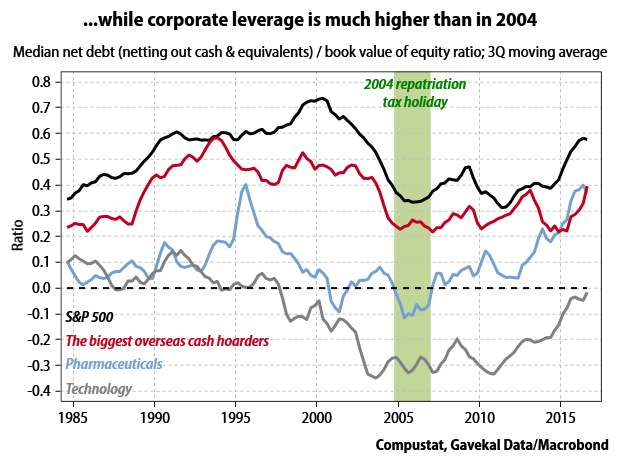

Similarly, with leverage also high, there is little room on corporate balance sheets for a fresh round of equity buybacks. The chart below shows median net-debt-to-equity ratios for the S&P 500, big cash hoarders, and the technology and pharmaceutical sectors, both of which have sizable overseas cash piles. As the chart illustrates, even if US companies were to use all their cash to pay down debt, they would still be highly leveraged by historical standards. With a net-debt-to-equity ratio of almost 0.6, the median S&P 500 company is far more highly geared today than in 2004-06 or 2010-14, which were the blockbuster periods for buybacks. If companies were now to go ahead and use their newly repatriated cash to fund fresh buybacks, their leverage ratios would only rise further.

So, if US companies are not going to hand their repatriated earnings back to shareholders in the form of buybacks or special dividends, what are they going to do with the cash? First and foremost, they will pay down debt. With balance sheets already stretched and interest rates heading higher, US corporations are likely to channel much of their free cash flow and repatriated earnings into retiring outstanding debt or substituting upcoming borrowing requirements. If all else were equal, this display of financial prudence would lead to narrower corporate credit spreads.

It is possible that a pick-up in earnings driven by rising sales could encourage US corporates to devote more cash to capital expenditure. That hasn’t happened in recent years, because earnings growth has come largely from margin expansion rather than from higher sales. Now, at this stage of the cycle with the labor market tight, wages rising and margins under pressure, the only way earnings are likely to accelerate is from stronger top-line growth. That is certainly possible if the growth outlook improves under a Trump administration, which would encourage US companies to invest in additional capacity. And because of the threat of protectionism, much of that capacity could be located in the US. However, we are concerned that the US economy is more likely to experience its next recession before any lasting rebound in growth.

In short, at this point in the cycle, increased buybacks and dividend payouts are the least likely uses for repatriated cash. Some increase in capital expenditure is possible. But with interest rates rising, debt reduction is likely to take priority over additional capacity expansion.

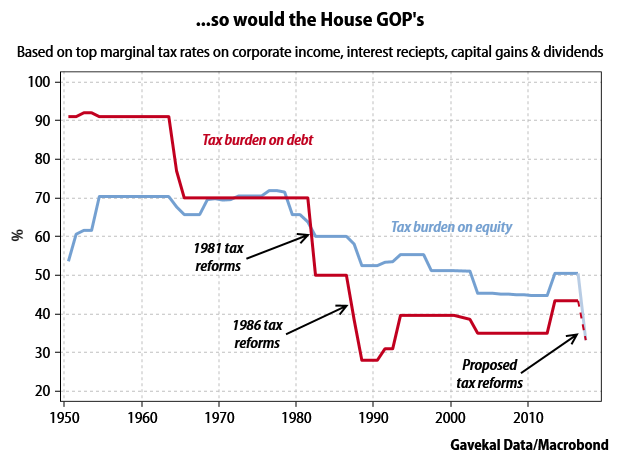

As well as cyclical reasons, there are also structural reasons to expect a shift away from equity buybacks. Both Trump and the Republican majority in the House of Representatives have proposed changes to the US tax code that would reduce, and even wipe out entirely, the present tax advantage of debt over equity financing. If such a change makes it onto the books—still a big “if”—it would both exaggerate the cyclical shift away from buybacks in favor of paying down debt, and have major implications for the capital structure of US corporations in the future.

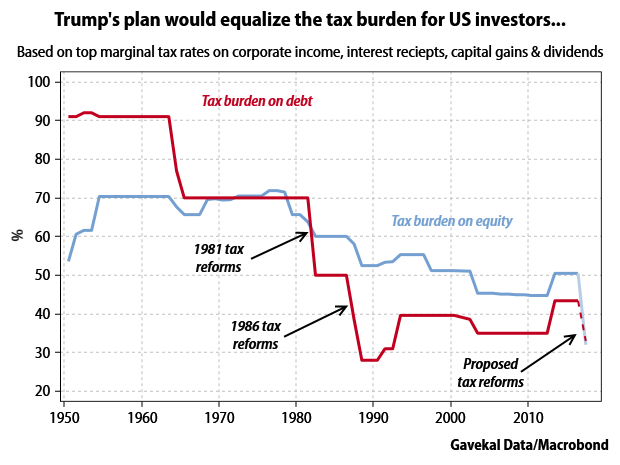

It was Ronald Reagan who ushered in the age of equity buybacks, when in 1981 he signed into law tax changes that made it highly advantageous for companies to substitute debt for equity. The advantages have persisted ever since, incentivizing profitable companies to borrow and buy back stock in order to maintain their desired capital mix between debt and equity.

Now things may be about to change. The Tax Policy Center’s analyses of Trump’s tax policies and the House Republicans’ proposals conclude that both plans would equalize the effective corporate income tax rates on debt-financed and equity-financed investments, eliminating the 35-year old corporate tax advantages of financing new investments with debt rather than equity.

Corporate income tax is important, but what really determines corporate capital structures is the overall cost of debt relative to equity, which is also influenced by taxes on interest paid to investors, capital gains and dividends. Factoring these in, our back-of-the-envelope calculations suggest that the plans advanced by both Trump and the House GOP would roughly equalize the total tax burdens on debt and equity, although by different means (at least for US investors; things are more complicated for foreign investors—see the box overleaf). Consequently, if all else is equal, the implementation of either of these plans will mean that in future US corporations will rely less on debt and more on equity than in recent decades, when capital structures were skewed by lopsided tax treatment.

Reagan’s tax changes favored debt even more than it appears at first. That’s because in 1984 the US removed the 30% withholding tax on coupon payments to foreign holders of US bonds, while leaving the withholding tax on dividends in place. This made it even more advantageous for US corporations to raise capital from overseas investors by issuing bonds rather than equity. If the new administration really wants to level the debt-equity playing field and eliminate capital structure distortions, it should also repeal the withholding tax on dividends. In the long run, this would benefit the US hugely, not only because it would attract more foreign investment and lower the cost of capital, but also because by eliminating the current tax distortion on capital structures, it would boost capital efficiency. In the short term, however, it would lend the US dollar more upward momentum, something policymakers may wish to avoid (see Trump’s Tax Plans And The Dollar).

Corporate earnings have weakened and financial ratios are stretched. This we already know. But markets are made on the margin, so the question is: what happens next?

The first possibility is that we could be wrong. The tax changes that actually make it onto the books may leave the preferential treatment of debt in place. And despite high leverage, companies may choose to double-down on equity buybacks next year, stretching their financial ratios even further. If so, it is likely that credit spreads will blow out, in which case buying corporate bonds now will prove a very poor investment.

On the other hand, if the politicians deliver on their tax proposals, and corporate executives act prudently, then most investors currently hold too few corporate bonds. Why? Because if policymakers do reduce the tax incentive to substitute debt financing for equity, and if business managers do choose to pay down debt rather than step up buybacks, then companies will begin to deleverage. This will be bullish for corporate bonds in three ways:

1) If companies borrow less from the US banking system, on the margin there will be less money multiplication, less inflation, and so generally lower interest rates than would otherwise prevail.

2) If all else is equal, lower leverage suggests lower credit risk and tighter corporate spreads.

3) Again if all else is equal, as corporate debt issuance declines, bond portfolio managers will compete to purchase the shrinking supply, depressing borrowing rates.

The implication is tighter corporate spreads. Admittedly spreads are already fairly tight by post-crisis standards, and as interest rates go up, recession risk will rise, which argues that investors should reduce their exposure to risk assets. However, within that exposure, the low probability of a renewed buyback boom and the high chance that companies will use repatriated cash to pay down debt suggest that investors should increase their holdings of US corporate bonds relative to equity.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.