“To me, being prepared means being suspicious of trends that common sense tells us cannot last forever and yet have been in force for so long that a majority of investors sees them as being ‘normal’ .“

- Super-star investor, Howard Marks

LIVE BY THE TREND, DIE BY THE TREND

The sound-bite that “the trend is your friend” is one of the most common (and dangerous) misconceptions in the investment world—perhaps rivaled only by “don’t fight the Fed”.

Certainly, nowhere is such thinking more pervasive than in emerging Asia, where momentum investing is as common as chain-smoking and knock-off luxury items. (One amazing anecdote in the latter regard was relayed to me by my close friend, Louis Gave: A few years back, there were more bottles of Chateau Lafite Rothschild sold in China than were ever produced in France!)

Just recently, we’ve witnessed a real-world demonstration of the combination of the “trend is your friend” and “don’t fight the Fed” (in this case, the Communist Party) in the People’s Republic of China. It provides me with a stellar opportunity to point out what I believe is one of the most underappreciated realities of financial markets worldwide: the über-importance of dollar-weighted returns, also known as money-weighted returns. This is a crucial distinction versus the typical way returns are reported on a fund or an index. The standard method ignores when and at what prices investors in the fund or index buy and sell. In other words, dollar-weighted returns are what investors actually realize from a given investment vehicle. As you will soon read, the difference between the two can be enormous.

Most of you are probably saying “Huh?” right about now, wondering how in the world I came up with that linkage. But, believe me, there is a vital lesson to be learned here for US-based investors who, despite the popping of epic bubbles in the 1990s and 2000s, have come to behave more like the trend-chasing Chinese over the years.

As our partner firm GaveKal is constantly saying and writing, there are three basic ways to make money in the markets:

1. The carry-trade, which means borrowing short-term at a lower interest rate and lending (usually longer-term) at a higher interest rate. Examples range from the traditional bank loan model to the highly leveraged arbitrage strategies employed by the “prop” desks and hedge funds—both of which have shaken the global financial system to its core on a number of occasions (and may again!).

2. Reversion-to-the-mean strategies are what most value/contrarian investors do (that would be Evergreen). As prices go lower on a given security or asset class relative to underlying revenues and/or cash flows, the more is accumulated. Conversely, as prices go higher, sell-downs are implemented.

3. Momentum strategies are the antithesis of reversion-to-the-mean. The higher prices go, the more money is invested—meaning that the majority of the capital for those playing this game tends to get allocated near the final stages of a rising trend where valuations are highest and the margin of safety is smallest.

Putting aside the carry-trade (which doesn’t apply to most EVA readers), the majority of investors follow strategy #2 or strategy #3, in many cases unconsciously. The following questions may help you determine which of those two categories you fall into: Were you selling tech stocks as they went hyperbolic in 1999? Were you buying stocks and/or corporate income securities hand-over-clenched-fist in early 2009? Were you buying municipal bonds in 2011 when their prices crashed due to over-hyped predictions of massive defaults, as millions of investors were bolting en masse?

FIGURE 1: MUNI ETF AND TRAILING SIX MONTH MUNI FUND FLOWS Source: Bloomberg, Evergreen GaveKal

Source: Bloomberg, Evergreen GaveKal

If you mostly answered no to the foregoing, then perhaps you may be more momentum-oriented than you suspect. In a moment, we’ll look at a few more recent examples of this phenomenon in the US. But, for now, let’s return to China where recent market behavior can only be described as mind—and wealth—blowing.

BUBBLE-UPSMANSHIP

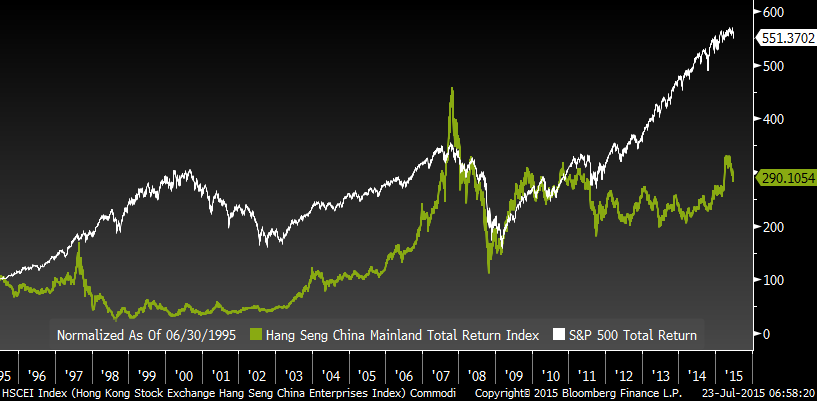

It’s my belief that most investors are not aware of how badly the Chinese stock market has fared versus the S&P 500 over the last 20 years, despite the wimpy 4% per annum total return the US index has produced since 2000. (Thanks to the blow-off phase of the tech bubble in the late 1990s, the 20-year return is a much more respectable 9%, at least until the next bear market.)

FIGURE 2: TOTAL RETURN HANG SENG CHINA MAINLAND VERSUS S&P 500 Source: Bloomberg, Evergreen GaveKal

Source: Bloomberg, Evergreen GaveKal

As you can see in the chart above, China’s stock market stagnated for many years despite the fact that its economy grew incomparably faster than the US over the same timeframe. This proves, once again, that there is scant correlation between superior economic growth and strong share price performance.

To make lucrative investment gains in China, one needed to ride the wave in real estate (excluding the private equity industry, which has been dominated by vested interests connected to the Communist Party). Momentum investors reaped spectacular profits in Chinese property for many years, but, starting about two years ago, that game came to a painful end as I warned (prematurely, I might add) in numerous EVAs circa 2011/2012.

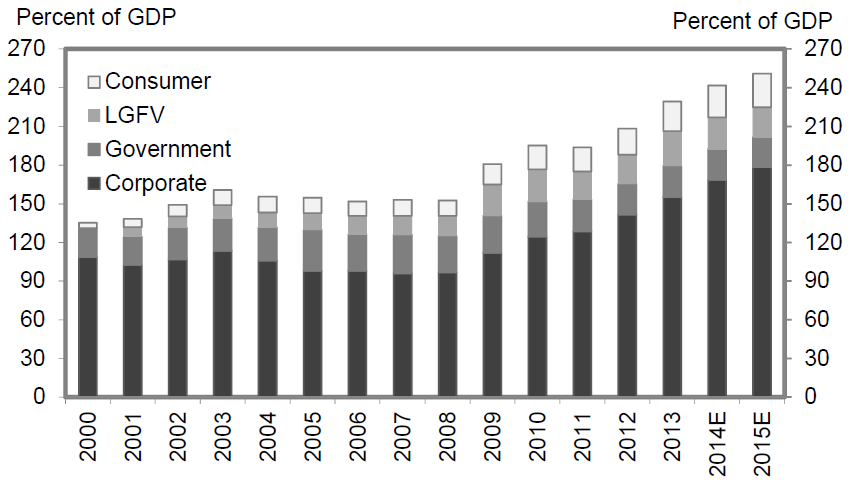

Simultaneously, China’s economic miracle began to look less miraculous. Even though GDP continued to hum along at around 7% (at least officially) —a pace that continues to leave rich countries in the dust—the longer term growth trend is clearly slowing as China approaches the limits of credit-fueled, investment-driven growth. It’s the Chinese equivalent of the “new normal”—the secular stagnation that has bedeviled the industrialized world since the Great Recession receded.

Also similar to the US, Europe, and Japan, China’s ability to borrow copious sums to stoke its economy began to red-line as growing debt loads produced an ever-diminishing amount of GDP gains. Accordingly, a new growth-driver was desperately needed.

FIGURE 3:

FIGURE 4: CHINA'S RISING DEBT LOAD, DEBT BY MAJOR BORROWER SEGMENT, AS % OF GDP

Note: financial institution credit is excluded and only half of entrust loan amounts are included due to double counting

Source: People’s Bank of China, China Bond Online, Gao Hua Securities Research

China’s boss-man, Xi Jinping, certainly must have looked around the planet and noticed that his chief rivals had come up with a plan. Simply inflate your stock markets and all would be well. Mr. Xi proved to be a stellar student as he saw a rising stock market as a key ingredient to recapitalizing troubled firms, restructuring the country’s debt, and rebalancing to a more sustainable growth model driven by consumption, services, technology, and high-value added exports.

Xi and his growth-minded minions also had a few big advantages over the US and the rest of the world. First, margin debt was almost non-existent. Second, Chinese households were sitting on humongous amounts of cash. Third, was the aforementioned genetic predisposition to chase performance. When you think of it, this was the perfect recipe to produce a stock market mania. And, voila! The soufflé rose to amazing, if unstable, dimensions.

Ok, you’re probably still wondering where the “dollar-weighted” aspect comes in, and it’s time to answer that question.

LOSING WHILE WINNING

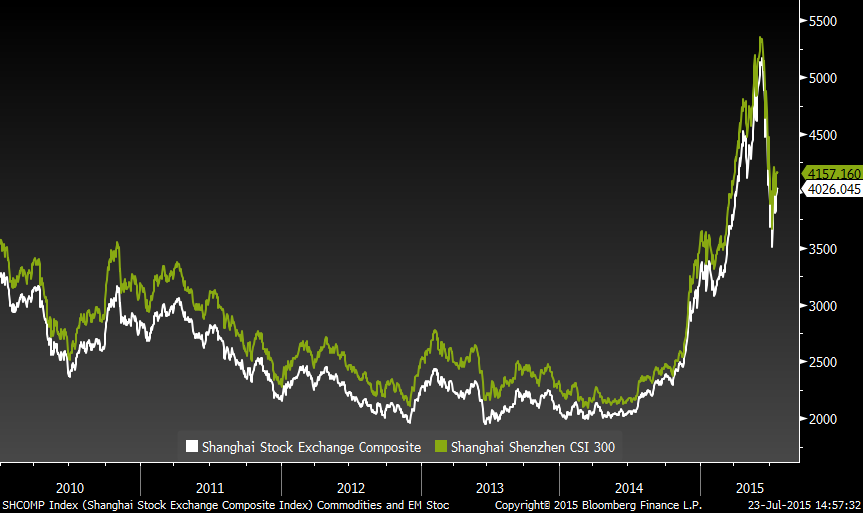

As you can see in the chart on the next page, China’s two indexes that were the foci of the government’s asset inflation efforts—the Shanghai and Shenzhen Exchanges—were both comfortably above their levels of last summer, even at the worst of the recent melt-down. So why all the pain and suffering?

FIGURE 5: FIVE YEAR PRICE ON SHANGHAI, SHENZHEN EXCHANGE

Source: Bloomberg, Evergreen GaveKal

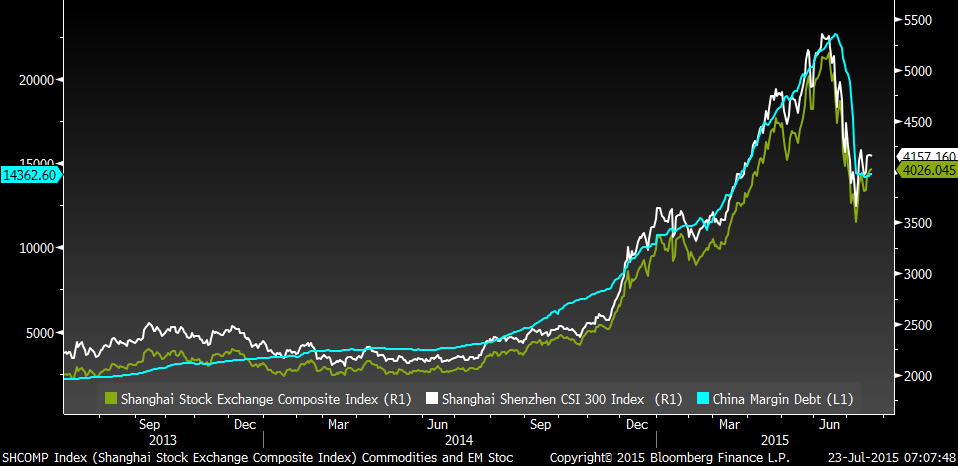

Brilliant question! That’s precisely where the dollar-weighting aspect comes into play. Per the following chart, you can see that the more those two markets went up (both are highly volatile like America’s NASDAQ, only more so), the more margin debt was taken out.

FIGURE 6: SHANGHAI, SHENZHEN AND CHINESE MARGIN DEBT Source: Bloomberg, Evergreen GaveKal

Source: Bloomberg, Evergreen GaveKal

Even so, official margin estimates almost certainly understate the leverage involved. There have been widespread reports of loans taken out against real estate, commodities, and even businesses, usually from China’s “shadow banking system”, to speculate on stocks. And, crucially, as is almost always the case, most of the money went in during the terminal stages of the bull market.

Despite the fact that those markets were up around 75% on average from last summer, even at the low point on July 8th, there was sheer panic in not only the streets of Shanghai, but also the rarified halls of Beijing’s ruling elite. By the time China’s equity markets began to crash, more than 90 million retail investors had poured their savings into stocks in hopes of getting rich quickly, more than the 88 million members of the Communist Party itself.

Per the July 10th EVA, the emergency measures the Party took in order to stabilize its stock market—ironically, the ultimate symbol of capitalism—were truly without parallel.

Of course, such wanton (not to be confused with wonton) speculation could never happen in America, right?

SILENCE OF THE CONTRARIANS

In years past, the US market was primarily dominated by value-oriented, return-to the-mean investors. Buying low and selling high, a la Warren Buffett, was the accepted path to superior returns. But times have definitely changed.

The new mantra might be Investor’s Business Daily publisher William O’Neil’s exhortation to “buy high and sell higher.” Further, as GaveKal’s formidable Charles Gave asserts, the increasing dominance of passive investing, or indexing, is fueling the ascendance of “mo-mo” investing. With so many trillions blindly tracking benchmarks, the higher a member of a given index rises, the more money must go into it, causing big upside overshoots.

A classic recent example of this actually was an US/Asian fusion: the Guggenheim Solar ETF (ETFs are essentially index vehicles). Although traded on the NYSE, and run by a US money manager, the largest position by far in this ETF back in April was Hanergy, a Chinese solar company. Hanergy was an early “beneficiary” of China’s stock bubble, rising over 600% from last summer, making it the most valuable solar stock on the planet and forcing indexers to weight it accordingly. At its apex, it became roughly 12% of the Guggenheim ETF’s assets. Then, on May 20th, it crashed 50% in a few hours, causing it to be halted (a condition affecting myriad Chinese stocks these days). It still hasn’t resumed trading. (Thus, one could reasonably wonder if Guggenheim Solar’s true net asset value isn’t what it’s reported to be, officially.)

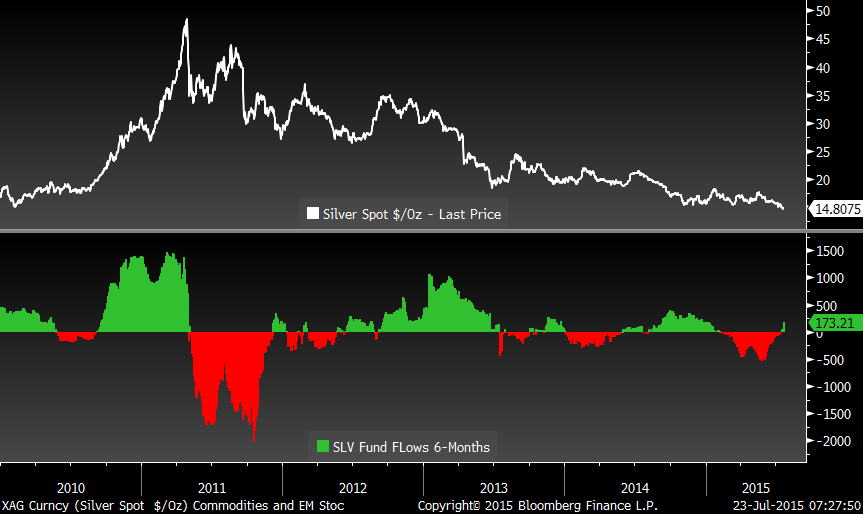

Now, let’s consider a few other more mainstream examples of how US investors have become more momentum-focused. First, there is the silver ETF (ticker: SLV). Back in 2011, as silver rocketed to $60 per ounce, in-flows also did a moon-shot.

FIGURE 7: SILVER AND FUND FLOWS Source: Bloomberg, Evergreen GaveKal

Source: Bloomberg, Evergreen GaveKal

Thus, the collapse to $14, about where it traded in 2010, was very costly to those who got caught up in that mania. For a buy-and-hold investor in silver, though, it’s been dead money (assuming they weren’t wise enough to sell at least some into the up-leg of the parabola), but not a loss. However, on a dollar-weighted basis, it was a disaster due to how much money flowed in toward the peak.

Another illustration regards one of Evergreen’s favorite asset classes: MLPs. As chronicled in these pages a year ago, last summer we reduced our exposure to MLPs to the lowest level we’ve had in the past decade. Euphoria was rampant and prices, especially in some of the “growth-ier” issues, seemed far over-the-top. While we can’t track flows into MLP-only funds, this hyper-zealousness was reflected in the creation of a dizzying number of new in MLP funds and ETFs.

Today, this asset class is enduring one of the most vicious sell-offs I’ve seen in all the years I’ve been involved with it (starting when Ronald Reagan was still in the White House). Only 2008/2009 was worse (and it was much, much worse, by the way). Consequently, some of the former high-flyers have truly crashed and burned. Even the bluest chip MLPs are down 30%.

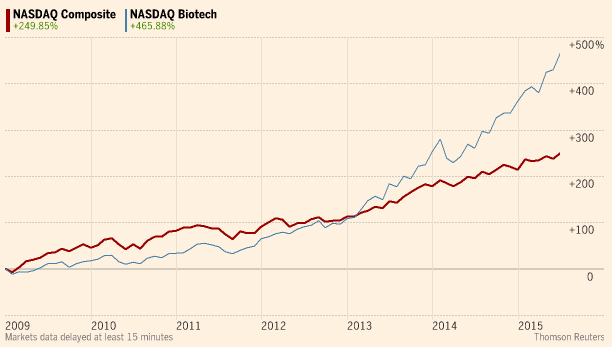

Finally, there is the next bubble that could be due for a pin-prick: the US Biotech sector. Lately, it has left even the soaring NASDAQ in its contrails as it rockets into the stratosphere. As usual, investors just can’t seem to resist going along for the ride.

FIGURE 8: BLUE LINE=BIOTECH, RED LINE=NASDAQ Source: Thompson Reuters

Source: Thompson Reuters

It’s an extremely safe bet that when this sector eventually returns to earth, all those jumping on board over the last year or so will learn you can’t parachute out during a power-dive.

To wrap up this EVA, let’s look back at one of the most flagrant examples of the difference between stated—and dollar-weighted returns I’ve ever come across.

GOING AGAINST HUMAN NATURE

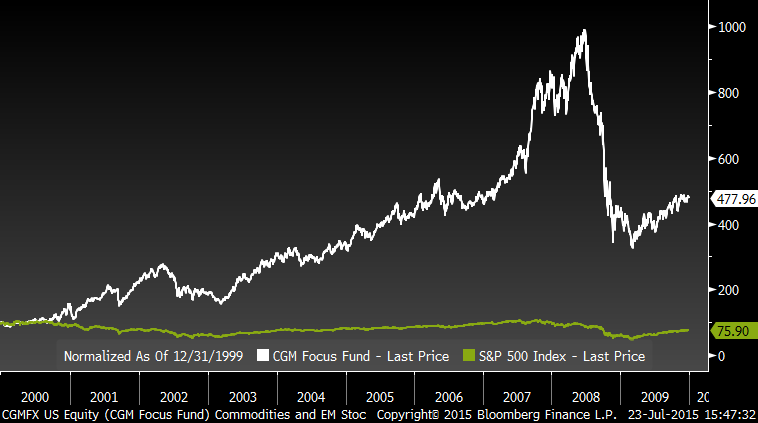

For the decade from January 1, 2000 through December 31, 2009, the S&P 500 generated a bagel—as in zero—when it came to gains—even including dividends. Incredibly, during this return-free period the CGM Focus Fund produced an 18% average annual increase. Fantastic, right? Not so fast. Due to the fact it was a highly volatile performer—with investors injecting huge sums after a burst of fat returns and frantically withdrawing during the sickening plunges—on a dollar-weighted basis CGM’s investors realized a horrific minus 11% per year.

FIGURE 9: CGM VERSUS S&P 500 Source: Bloomberg, Evergreen GaveKal

Source: Bloomberg, Evergreen GaveKal

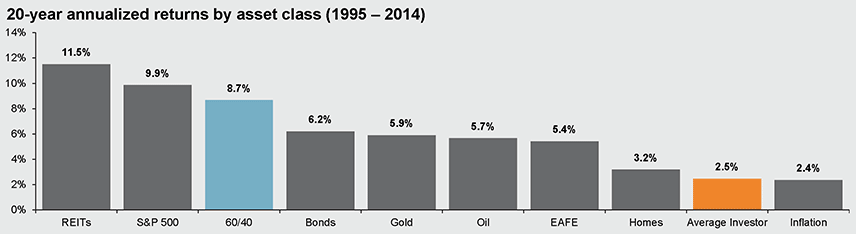

Talk about making lemons out of lemonade! Yet, as noted in many past EVAs, the S&P 500 itself has become much more volatile over the last twenty years. Along with a Fed policy that has often-stoked speculative excesses, Evergreen also believes this boom-bust cycle is a consequence of the increasing influence of so-called “passive” or indexed-investing. This is likely a key reason the average investors’ returns have been abysmal, as shown below.

FIGURE 10: TWENTY-YEAR ANNUALIZED RETURNS BY ASSET CLASS (1995-2014) Source: Morningstar Direct, Dalbar Inc., J.P. Morgan Asset Management

Source: Morningstar Direct, Dalbar Inc., J.P. Morgan Asset Management

According to Franklin Templeton in 2014, flows into passive funds were 15 times those into active funds. This has led to a radically reduced share of truly active funds, down to under 20% as of 2009 (and likely even lower now as this trend has intensified).

FIGURE 11: Source: Financial Analysts Journal, Franklin Templeton

Source: Financial Analysts Journal, Franklin Templeton

With trillions now blindly tracking index weightings, what is going up (or down) gets carried to absurd extremes. Like with Hanergy, more money must flow into a rising position regardless of how inflated it may be. This clearly exaggerates the momentum effect. As expressed in past EVAs, when an index becomes an investment strategy—and particularly the most influential strategy—strange things start happening.

So what’s a rational investor supposed to do in an ever more irrational world? Get ready for some really tough advice: embrace underperformance. What, you say? That’s not just counterintuitive, it’s downright un-American (thank goodness Joe McCarthy’s no longer on this side of the grass or he’d be hot on my trail!).

But here’s a huge caveat to my advice: The underperformance needs to be for the right reason. If it’s just bad security selection, that doesn’t cut it. But if it’s because a manager is refusing to get caught up in the latest trend or fad—and he or she has solid data that values have become outlandish—that’s an adviser you should stick with; in fact, you should probably commit even more money to them. Similarly, if they are lagging because they are buying into an anti-bubble—a selling panic—you shouldn’t bail in that case, either, even though every cell in your body is screaming: “Get me out!”.

In our view, the convergence of forces described above makes it extremely challenging to be a contrarian, return-to-the-mean, asset manager in the short-run (which might even mean a couple of years or more). But the reward is greater outperformance in the long run—like over a full market cycle—if a professional investor can stay disciplined.

The underlying investor plays a huge role in this drama by controlling when and to what areas of the market she or he is allocating investment dollars. You can actually achieve better returns than the fund or manager you are investing in by doing the opposite of what most folks do. If you can force yourself to add more capital to the disciplined stragglers—again, presupposing the lag is for sound reasons—and reduce those parts of your portfolio that have been on a multi-year hot streak, you are highly likely to have superior dollar-weighted returns.

And that, dear reader, is what savvy investing is all about.

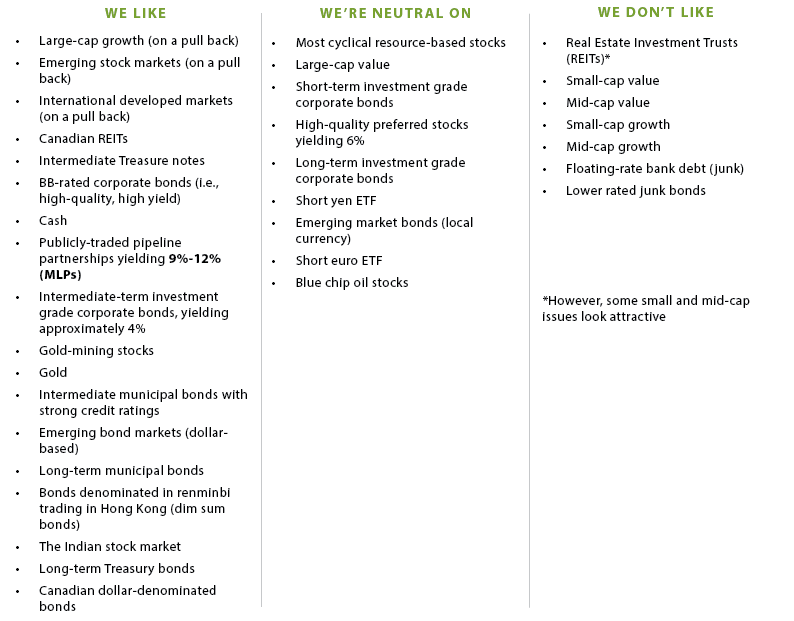

OUR CURRENT LIKES & DISLIKES

Changes are noted in bold.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.