Due to the breaking news on the new—as in “Nu”—Covid variant, we are running a Special Edition of our Likes/Dislikes section in order to provide updated information on this latest pandemic development. Read more here.

This week’s Evergreen Virtual Advisor (EVA) comes from Vincent Deluard, Director of Global Macro Strategy at StoneX Group. Vincent consistently puts out prescient big-picture research and is one of our favorite authors in the space. While we don’t typically run back-to-back guest EVAs, we thought this was a particularly relevant missive on why--despite a fairly strong economic outlook for the US--domestic consumers are not only concerned about inflation, but they’re also very worried the country is on the wrong track. Vincent goes on to expound on the investment implications of what this sentiment means both in the US and internationally.

We think you’ll find it to be an interesting read and would also like to take this opportunity to say we hope you have a wonderful Thanksgiving with your loved ones.

Four years ago, Comedian Louis C.K. observed that “everything is amazing but nobody is happy”. This is a fitting description for the US in 2021: households’ net worth has increased $31 trillion since March 2020. An additional 1.5 million workers retired early thanks to soaring asset prices. As I explained in the F.I.R.E economy, engineers at big tech companies have amassed multi-million fortunes simply by showing up for the job. And yet, the University of Michigan Current Economic Conditions index is at the same level it was in March 2020, at the worst of the pandemic and after a brutal bear market.

The first part will show that all the major sectors of the economy are experiencing an unprecedented windfall. Personal income tax collections have soared by 18% this year and gig income is doubling every two years. The household sector purchased a record $1.2 trillion in stocks in the second quarter and $3.2 trillion since March 2020.

Junk-rated corporations get to borrow at negative real yields when nominal GDP is growing by close to 10%, the fastest growth since the Reagan economic boom. Analysts keep increasing their EPS expectations.

Pension funds are fully funded for the first time in 15 years and tax collections in California have soared so much that even Sacramento politicians cannot spend the money fast enough.

The second part will explain why soaring wealth has so little effect on Americans' satisfaction: if the price of every home rises by any 20%, homeowners do not feel richer but first-time homebuyers feel squeezed. Similarly, the “wealth effect” that central banks worship often means that investors are paying more for the same streams of cash flow.

Being long equities generally and rotating towards small caps, cyclical sectors and value stocks seems like the best bet on the US economic boom. However, US small cap indices are dominated by meme stocks, loss-making zombies, and speculative biotech stocks.

The US wealth boom means that American can acquire foreign assets on the cheap. Mexico and Colombia, which have a lot of exposure to the soaring US economy and are hedged against global inflation thanks to their large energy and agricultural sectors, trade for a fraction of US stocks. Those who pile into overpriced U.S. megacaps because “There Is Not Alternative” do not search hard enough.

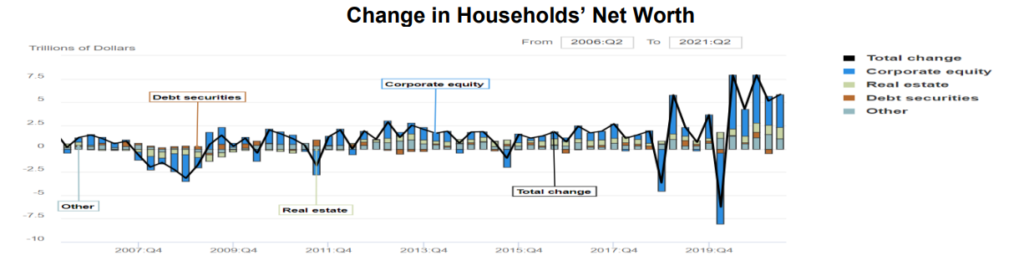

A $31 Trillion Windfall to Households

The most spectacular chart I have seen this year comes from the Fed’s Flow of Funds database: the net worth of the household and non-profit sector soared by $31 trillion since March 2020. The bulk of this mind-boggling gain came from equities (+$20 trillion) and real estate (+$5 trillion).

For reference, households’ wealth decreased by only $11.2 trillion during the great financial crisis: the past year has been the biggest wealth shock in recorded history. I suggest we invent a new name for it – how about the “gigantesquely gargantuan gain of 2021”?

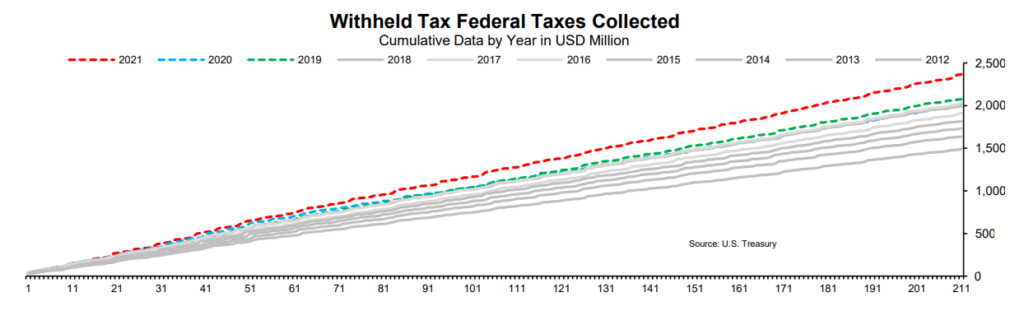

Personal income charts are equally mind-boggling. The Daily Treasury Statement is the best real-time measure of the Americans’ income. While the BEA’s data is based on a monthly survey which gets revised as more responses are collected, the DTS data covers all the Americans who pay taxes and this data is available daily. The fact that so few economists care about this data has always baffled me, but I digress.

The point is that the U.S. Treasury collected $2.4 trillion in withheld personal income taxes in the first 211 days of 2022, 18% more than last year. Tax law has not changed so the only explanation for this year’s record gain is that Americans are making more money. A lot more.

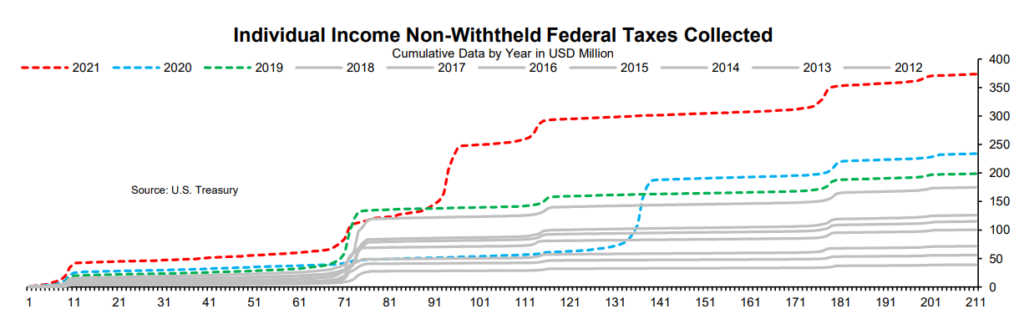

Furthermore, withheld income taxes only covers Americans with a regular job and misses the fastest-growing segment of the economy: gig workers and small entrepreneurs. The U.S. Treasury collected $375 billion in non-withheld personal income taxes in the first 211 days of 2022, 60% more than last year and 88% more than in 2019, the last year which was not affected by Covid. Tax collections from small entrepreneurs and gig workers are on track to exceed corporate income tax collections this year. For reference, corporate income tax collections were six times larger than non-withheld personal income taxes ten years ago. I am convinced that the rise of the gig economy has tremendous macro implications for the relation between labor and capital and is a driver of secular inflation. But I digress again: the main point here is that Americans are much wealthier, earn more on their regular jobs, and are collecting an unprecedented amount of gig income.

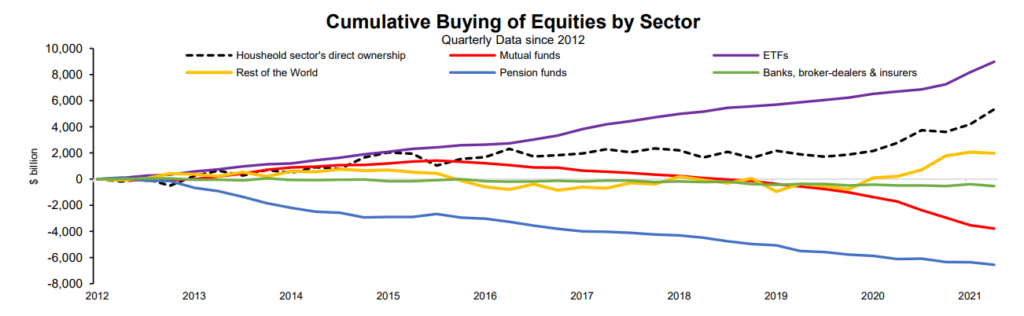

What can Americans do with all this money? Buy stocks, of course! The household sector purchased a record $1.2 trillion in stocks in the second quarter and $3.2 trillion since March 2020. ETFs bought another $800 billion in the second quarter and $2.7 trillion since March 2020. On the other side of the trade, pension funds have sold about $150 billion per quarter as ageing beneficiaries have the good fortune to cash out at historically high valuations.

Corporations Are Minting Money!

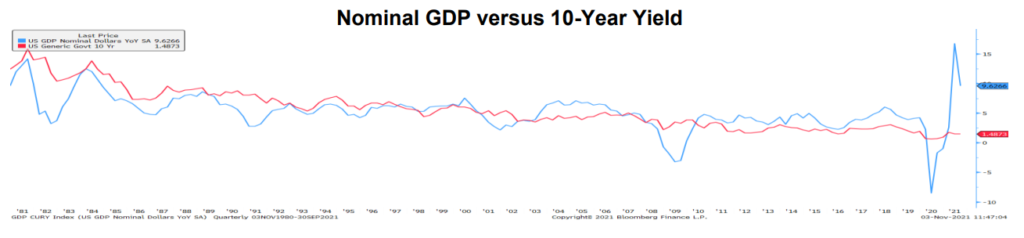

Turning to corporations, the craziest chart I can think of shows that nominal GDP is expanding by about 10%, the same level as during the Reagan boom while 10-year yields are 12 percentage points lower. The spread between the growth in companies’ top line and the cost of their liabilities has never been wider.

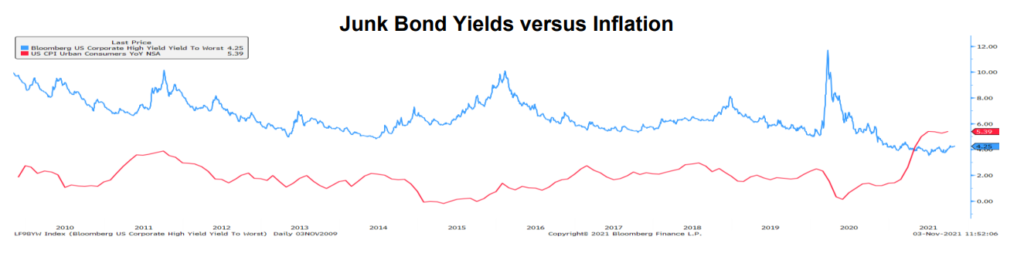

Inflation is acting as a stealth bail-out for junk companies. The yield on the Bloomberg corporate high yield index is 114 basis points lower than inflation.

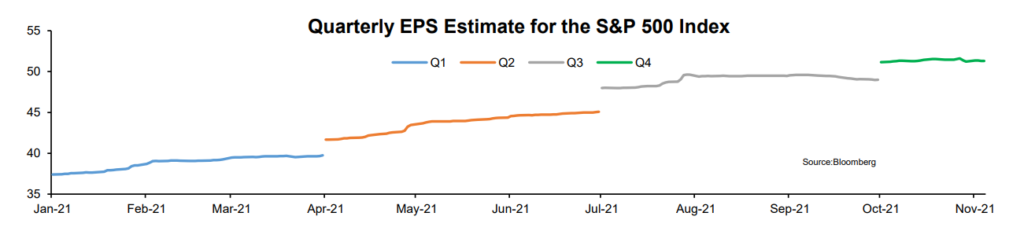

Time will tell whether keeping interest rates at Great Depression levels amidst an inflationary boom is the right policy for the long-term, but stimulus’ immediate effect is clear – profits are soaring. S&P 500 companies are expected to earn $51 per share this quarter, a cool 62% increase from last year. Traditionally over-optimistic analysts have been scrambling to increase their estimates all year-long.

Pension Funds & Local Governments

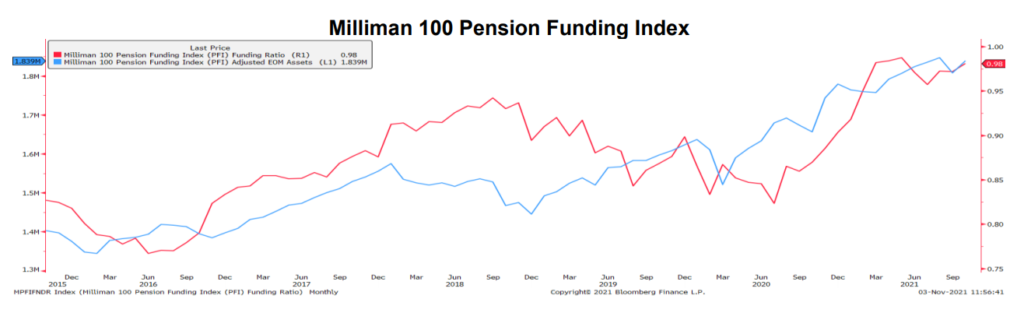

The great wealth shock of 2021 is also bailing out chronically-underfunded pension funds and local governments. The funding ratio of the Milliman 100 Pension Funds Index has risen to 0.98, after more than a decade in the red. Despite net redemptions from beneficiaries, pension funds’ assets swelled to $1.83 trillion from a low of $1.3 trillion in 2016.

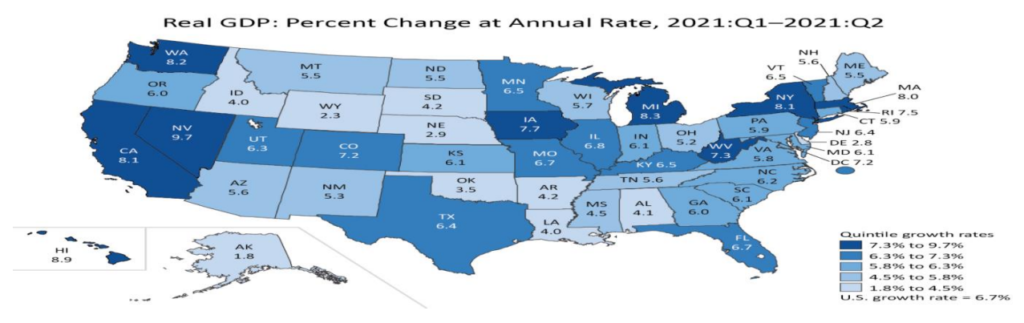

The economies of the largest states are also growing at rates which would make Chinese province governors envious. California, New York, Washington, Florida, and Texas grew at real rates of 8.1%, 8.2%, 6.7%,and 6.4%, respectively.

Soaring tax collections, a real estate boom, and federal payments have resulted in a spectacular turnaround of local governments’ finances. California expects a $75 billion surplus this year and an even bigger surplus next year. California has already collected $14 billion more in tax revenue than expected for the current budget year, on top of the $27 billion it received in COVID funding from the federal government. Some of that money was used to send $600 checks to Californians making less than $75,000 a year, which was not enough to prevent a contentious recall election in September. It seems that all this good news has failed to lift the national mood – to which we shall now turn.

Why Is Nobody Happy Then?

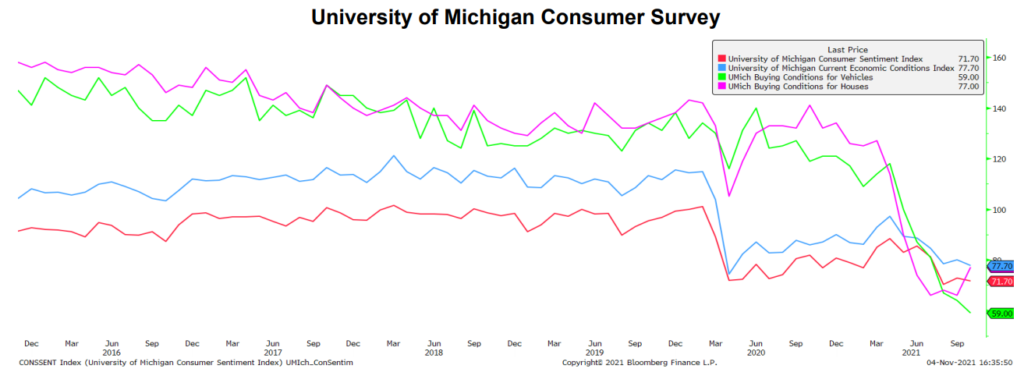

Despite these splendid economic conditions and unprecedented wealth gain, consumers’ mood is grim. The University of Michigan Consumer Sentiment fell to a decade-low of 71. Consumers worry more about rising prices than they appreciate higher wages: the current economic conditions index fell to its March 2020 low of 77, in large part because consumers worry about the prices of vehicles and houses.

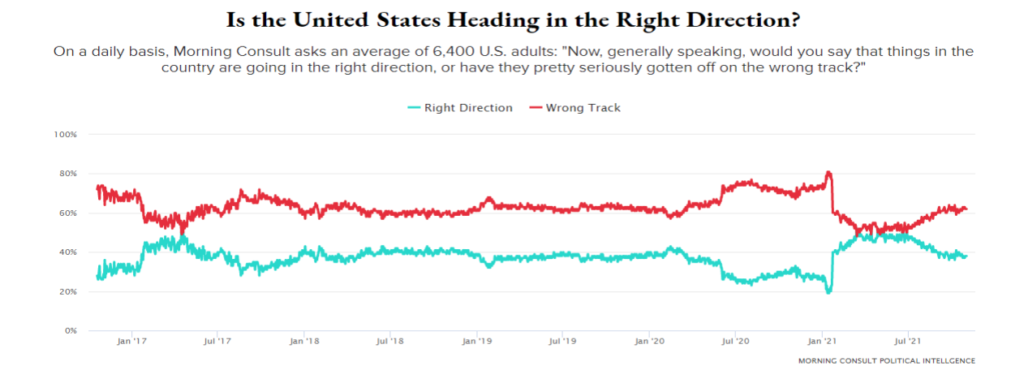

Economic pessimism and inflation worries have convinced many Americans that the country is headed in the wrong direction. According to Morning Consult, the share of Americans satisfied with the overall direction of the country dropped by 10 percentage points in the past four months and the decline was observed for all partisan affiliations.

I can think of three main explanations for the paradox of this unhappy economic boom.

First, soaring wealth is not that helpful on a daily basis. For example, the value of my home has increased by about 25% since the pandemic. But so has every other house on my block or in the country for that matter. My real purchasing power has not changed.

The same is true for bonds and most stocks. Central bankers say that higher asset prices are good for the economy, but I fail to understand how paying more for the same cash flows helps anyone.

The most positive effect of low yields is that it increases the collateral value of financial assets, but most people do not borrow against their 401-Ks (and they should not either). Moreover, the high-net worth investors and institutions who can lend shares find that the value of the other assets they could buy has also gone up so true purchasing power does not change all that much.

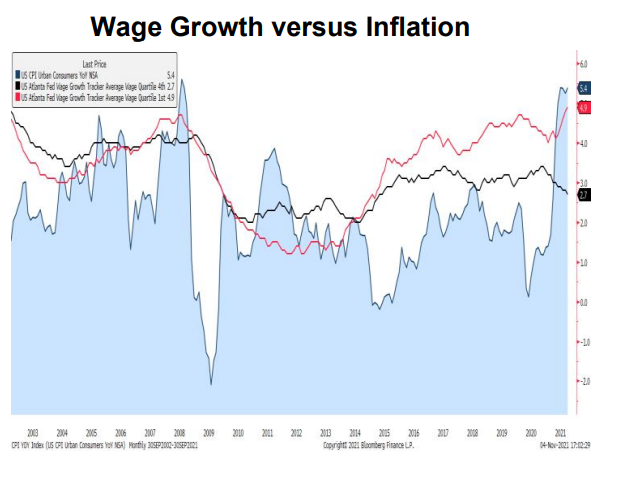

The same goes for income. Inflation exceeds wage growth for the lowest paid quartile of the U.S. population for the first time in five years – and the gap would be even bigger if the CPI correctly accounted for house price inflation.

Second, the middle class feels squeezed: the cost of basic necessities (gasoline, food, heating) is soaring and the vast majority of middle-class Americans own no financial assets outside of their retirement plans. The squeeze is made even more painful by the sight of the soaring wealth of the billionaire class and kids killing it with meme stocks, arcane cryptocurrencies, and NFTs.

To paraphrase Charles Kindleberger, “there is nothing so disturbing to one’s well-being and judgement as to see a friend retire early thanks to a fortunate purchase of Tesla’s stock”.

Third, there is a pervasive sense of “uneasiness in the culture” (a poor English translation of Freud’s 1930 book Das Unbehagen in der Kultur). The trends described by R. Putnam in his seminal 1995 essay, Bowling Alone: America’s Declining Social Capital, have accelerated with Covid. The institutions which provide a sense of meaning and community, such as churches, unions, political parties, marriage, and the workplace, are in terminal decline.

All studies show that money does not add much to happiness past a threshold of $75,000 and that humans crave deep connections with others above all. The Survey Center on American Life found that the percentage of men without any close friends jumped from 3% to 15% and the General Social Survey that 23% of young men have had no sexual relation in the past year. I need to come back to investment-related topics, but I am convinced that these trends matter a lot over time.

Investment Implications

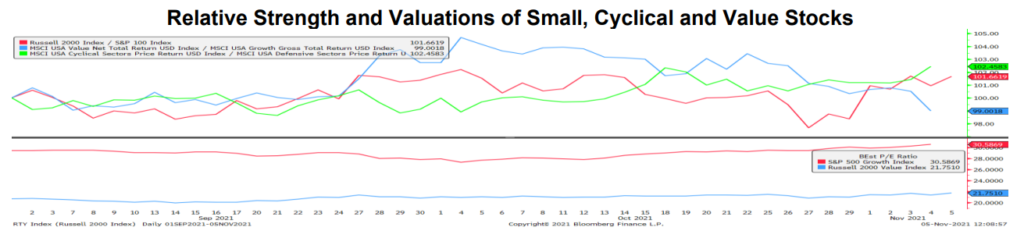

The combination of a booming economy, deeply negative real rates, and excessively negative sentiment should bring investors to two logical conclusions: stay long equities in general and rotate towards small caps, cyclical sectors, and value stocks.

Yet, this trade seems impossible to complete for anyone who cares about valuations or looks at the actual composition of small cap indices. The two largest holdings of the Russell 2,000 index are AMC and Avis. These two stocks have rallied by 1,584% and 809%, respectively, in the past year. Both stocks have negative book value and AMC and Avis’ free cash flow for the year was negative $1.3 billion and negative $6.1 billion, respectively.

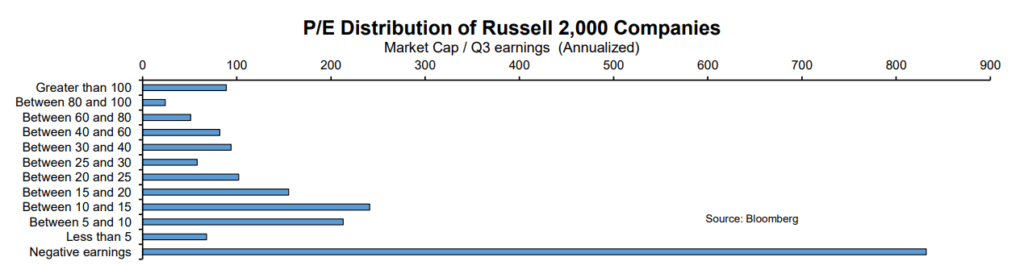

Turning to valuations, I annualized this past quarter’s earnings to minimize COVID disruptions and graphed the distribution of Russell 2,000 P/E ratios below. 41% of small caps have had negative earnings, despite the most favorable macro conditions one could imagine: deeply negative real rates, 10% + nominal growth, and pent-up demand from the re-opening. Another 12% trade for more than 40 times earnings.

Relative valuations and momentum seem to be the best rationale for the small/cyclical trade. Large cap growth trade for 30.5 times forward earnings versus 21.8 for small-cap value stocks, the largest gap on recorded history. Small caps and cyclicals have outperformed in the past three weeks and value should eventually benefit from rising rates.

Last but not least, bulls can always turn to “There Is No Alternative” arguments: what is the appropriate P/E for stocks when a 10-year TIPS pays a yield of minus 1.1%? What is the P/E on gold and Bitcoin? Who wants to hold cash when inflation is running at 5.4%?

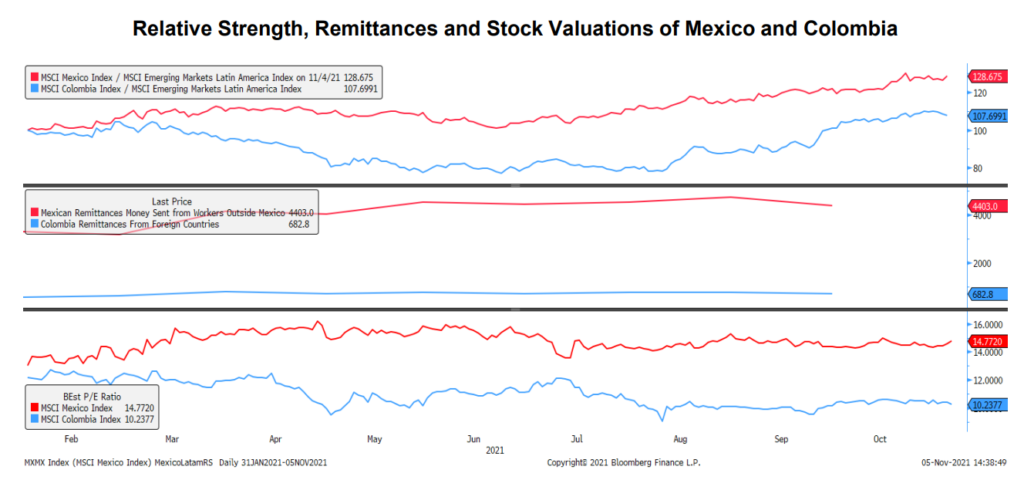

I think the TINA crowd does not look hard enough for alternatives and is far too eager to justify the absurd valuations of US stocks. The massive bubble in US wealth means that selling US assets can finance large purchases of cheaper foreign assets.

Mexico and Colombia offer a rare combination of a strong exposure to the US economic boom and still-depressed valuations. These two countries are the only large Latin American countries which export a lot more to the U.S. than to China. Furthermore, they are participating in the US economic miracle thanks to their large diasporas: remittances have grown by 25% year-over-year in Mexico and 26% in Colombia so far this year. These two countries benefit from global inflation due to their large energy and agricultural sectors and are relatively immune to China’s slowdown and they have outperformed the MSCI Latin America Index in the past four months.

Mexican and Colombian shares trade for 14 and 10 times 2022 earnings, respectively, versus 23 in the U.S.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.