Introduction

This week, we are presenting a missive from the always read-worthy Gerard Minack. Mr. Minack, who pens the Down Under Daily, outlines several reasons why he believes that recent inflation indicators are "transitory" in nature (which has recently become a popular term among some economists and policymakers in relation to inflation concerns). Specifically, Mr. Minack believes the labor market holds the keys to the proverbial kingdom when it comes to inflation, and that labor market conditions - not goods-sector inflation - will dictate central bank policy.

Factory inflation good for a scare but isn’t the main game by Gerard Minack

Surging goods-sector inflation is fodder for an inflation scare and may be the catalyst for an overdue equity market correction. However, it isn’t the main game for inflation. The labor market remains the key to both the outlook for inflation and central bank response to inflation pressure.

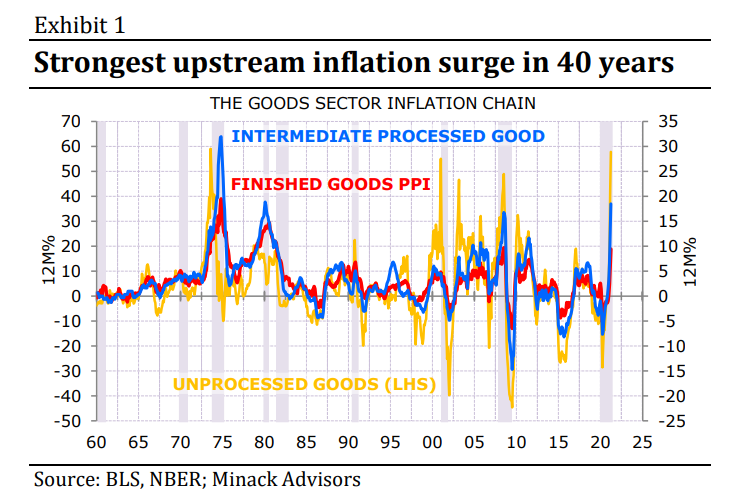

Factory-level inflation – both for inputs and outputs – is soaring. In the US, output inflation is at the highest level since the 1980s and input inflation at the highest since the mid-1970s (Exhibit 1). Of course, much of this is base effects: raw material prices are up 58% on year-ago levels, but up only 17% compared to pre-pandemic January 2020.

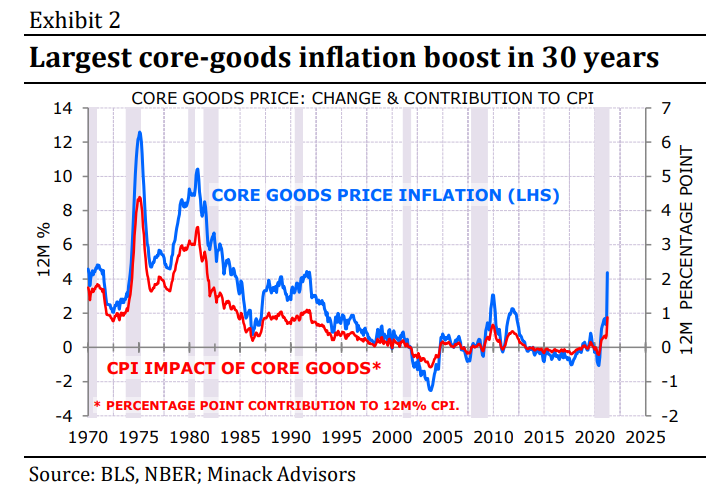

More important has been the flow-through to consumer-level goods inflation, which is now running at the fastest pace in 30 years (Exhibit 2).

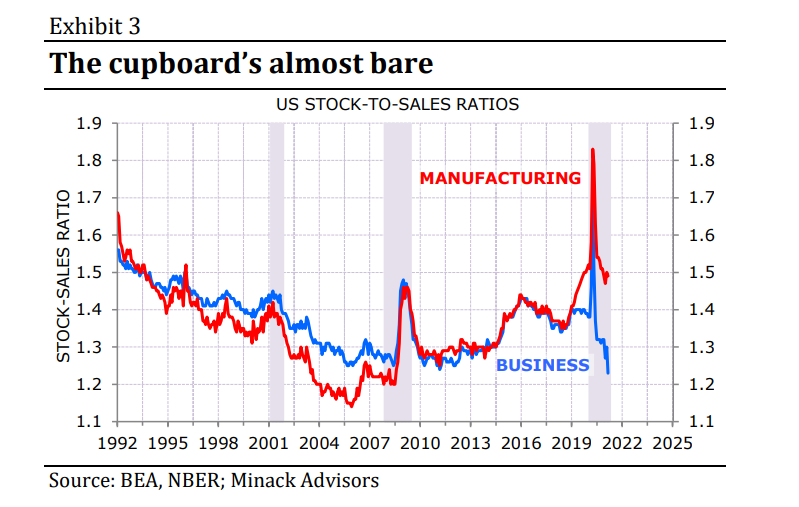

This is a faster rise than I expected, and not solely due to base effects: core goods prices are up 3.6% on pre-pandemic levels. The inflation at the consumer level may be less about input-cost pressures, and more about old-fashioned pricing power when supply is tight (Exhibit 3).

But I can’t see any reason why inputs should continue to rise at their recent pace, or why producers won’t be able to rebuild stock. It may take time but, yes, I think this inflation is transitory.

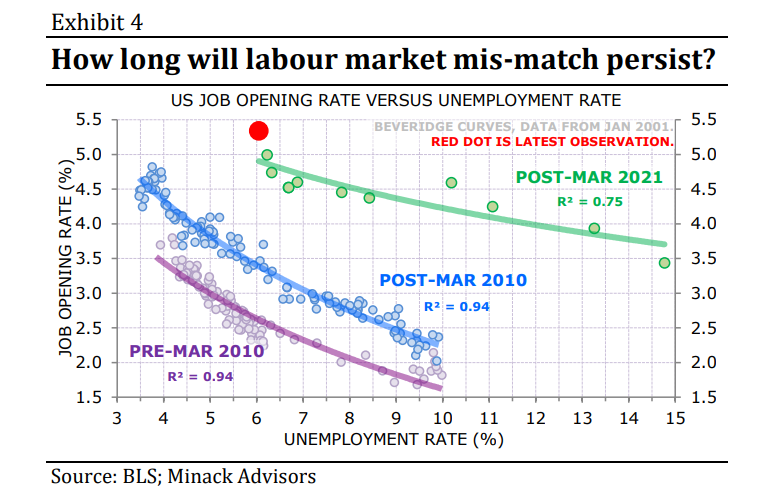

The most important issue for inflation, in my view, is the labor market. Given central banks’ focus on maximizing employment, I think labor market conditions will also dictate when they adjust policy.

This is the context that makes signs of a labour market mis-match so important. The Fed may presume that the unemployment rate can fall at least as far as it did last cycle – to 3½% – before there’s any prospect of inflation-lifting wage increases. The high level of unfilled vacancies (Exhibit 4) is a hint that wage growth may accelerate at a higher unemployment rate.

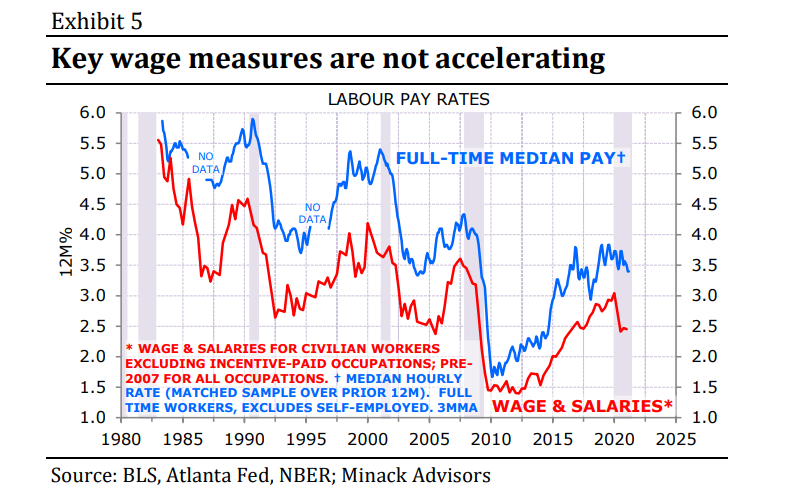

I suspect the situation will improve as vaccination rates rise and child minding and schools re-open. I doubt that high welfare payments are a factor – continuing jobless claims fell by over 2 million in April – but if they are, they end in September. The ultimate test of the issue is wage growth – and for now important measures are flat-lining (Exhibit 5).

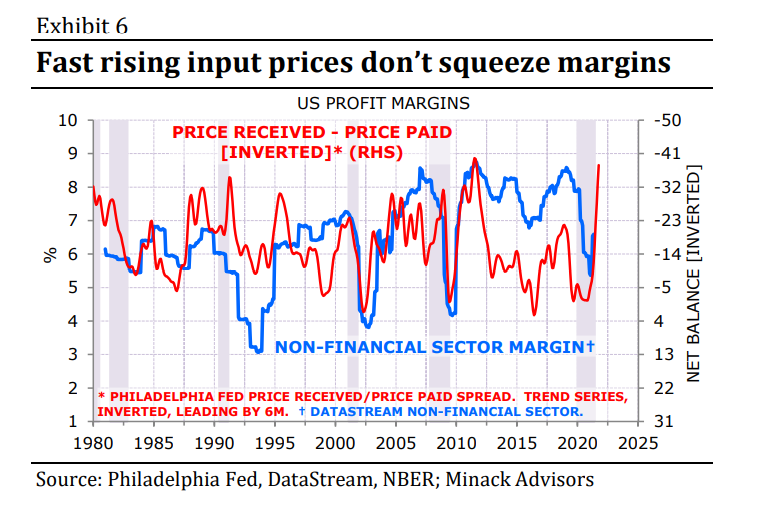

What does this mean for investors? Rising input prices are almost always good for profit margins (Exhibit 6). To be fair, this may be correlation not causation: input prices rise fast in a recovery, and recoveries are good for profits.

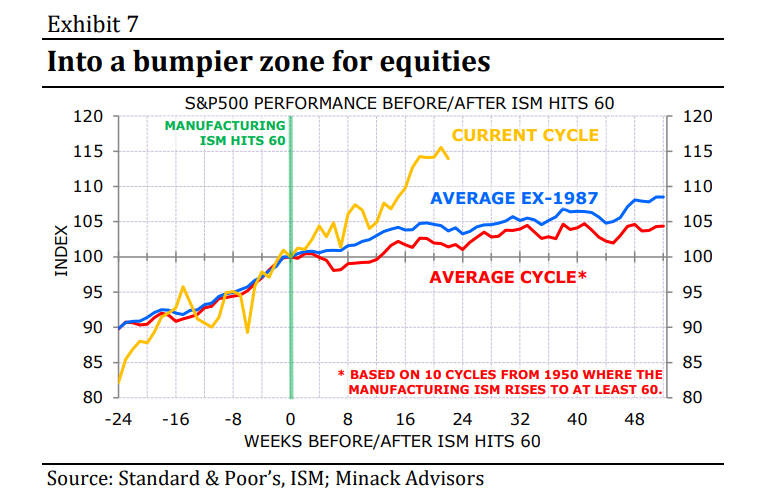

However, an inflation scare will likely mean that good macro news will no longer be unambiguously good for equities as it raises the risk of a policy response to inflation. Once perceptions shift to the view that strong macro news increases the risk of higher rates then equity gains slow, and volatility rises. The typical threshold for that shift in the US has been the ISM hitting 60 (Exhibit 7).

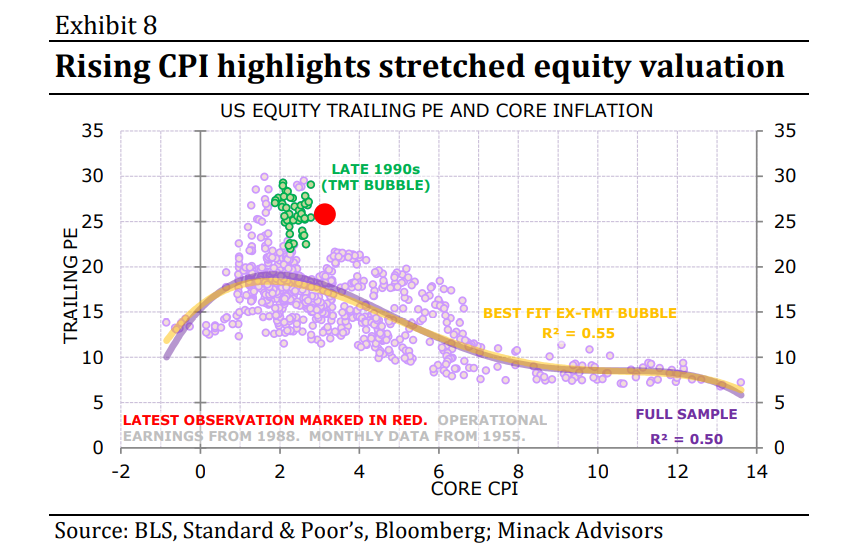

This may be the catalyst for a reasonable correction given stretched valuations (Exhibit 8).

The pace of the recovery has surprised most, me and the Fed included. However, the Fed hasn’t changed its rate forecasts. I agree with the market: those forecasts are looking increasingly too dovish (Exhibit 9). The question is when the Fed acknowledges that: I suspect before year-end.