“What the wise do in the beginning, fools do in the end.”

– Warren Buffett

“There is no better teacher than history in determining the future... There are answers worth billions of dollars in a $30 history book.”

– Charles T. Munger

______________________________________________________________________________________________________

Every year, professional and amateur shareholders have the opportunity to partake in Berkshire Hathaway’s annual meeting where legendary investors Warren Buffett and Charlie Munger field questions on Berkshire’s business and investment decisions. Typically, the annual event is held in Warren Buffett’s hometown of Omaha, Nebraska, at which “The Oracle of Omaha” addresses a packed crowd of attendees. However, due to the ongoing Covid-19 pandemic, this year looked quite different as Buffett and Munger sat side-by-side in a hotel conference room in Los Angeles, California, engulfed by a blue velvet backdrop rather than surrounded by thousands of eager shareholders.

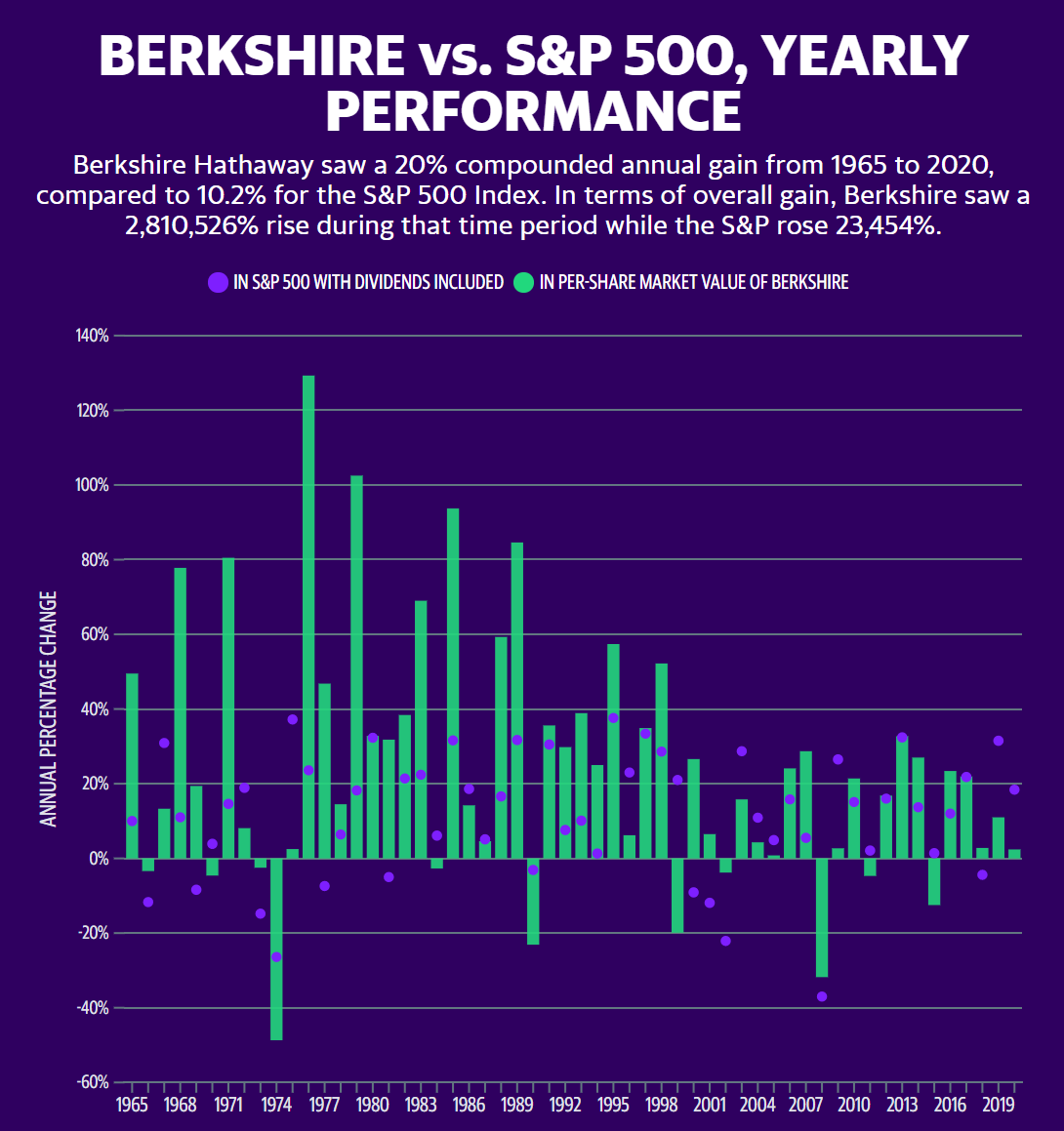

Despite the change in setting and the obvious toll that Father Time is taking on the fabled investors, Buffett and Munger held true to form by providing noteworthy nuggets on everything from bitcoin to inflation, to the Federal Reserve, to retail investors, to Special Purpose Acquisition Corporations (SPACs). Given Berkshire’s long track record of delivering outsized returns to investors – almost doubling the S&Ps annual gain since 1965 (20.0% vs. 10.2%) – its no question why the two garner such attention.

Source: Berkshire Hathaway’s 2021 Shareholder Letter

For those that subscribe to the school of Benjamin Graham and David Dodd, the twin fathers of security analysis, Buffett embodies the incarnation of a long-held set of investing principles. The billionaire head of Berkshire, who many consider the greatest investor in history, has lived prosperously through many market cycles, guided by the belief that value investing – which is an investment paradigm that involves buying securities at less than their intrinsic value – is the most profitable investment strategy in the long run. And it’s hard to argue with a man and investment principle that has delivered investors an average return of 20% annually for over 55 years.

This week we are presenting four soundbites from Berkshire’s annual shareholder meeting. These quotes provide a glimpse into the minds of some of the greatest value investors in history, outlining their views on today’s investment landscape. Following the list of excerpts, we provide some brief commentary on each subject.

Soundbite #1: Bitcoin is ‘contrary to the interest of civilization.’

Warren Buffett: "I knew there’d be a question on bitcoin or crypto and I thought to myself, well, I watch these politicians dodge questions all the time … The truth is, I’m going to dodge that question. Because the truth is, we’ve probably got hundreds of thousands of people that are watching this that own bitcoin. And we’ve probably got two people that are short. So, we’ve got a choice of making 400,000 people mad at us and unhappy and making two people happy. And it’s just a dumb equation."

Charlie Munger: “Those who know me well are just waving the red flag at the bull. Of course, I hate the bitcoin success. And I don’t welcome a currency that’s so useful to kidnappers and extortionists and so forth. Nor do I like shoveling out a few extra billions and billions and billions of dollars to somebody who just invented a new financial product out of thin air. So, I think I should say modestly that the whole damn development is disgusting and contrary to the interest of civilization."

Regular EVA readers are likely aware that this newsletter has softened its stance on Bitcoin lately. For those that missed it, last week David Hay published a compelling take on why the cryptocurrency isn’t as ‘disgusting’ as Mr. Munger makes it out to be. However, as Mr. Hay shared last week, investors should take extreme caution at current levels because the asset’s upside might be fully baked in for the time being.

Soundbite #2: ‘We’re seeing substantial inflation.’

Warren Buffett: "We're seeing substantial inflation. We're raising prices, people are raising prices to us. And it's being accepted. We really do a lot of housing. The costs are just up, up, up. Steel costs. You know, just every day they're going up. It's an economy – really, it's red hot. And we weren't expecting it.”

Another popular topic that we’ve written on at length is rising inflation. In recent months, we’ve been making the case that the economy would soon be entering a boom phase and that inflation fears would begin to emerge from their long slumber. Readers that missed our most recent post on the subject can find more here. In very short order, inflation has gone from bottom-of-mind to bordering on obsession and, as Mr. Buffett notes, a lot of people “weren’t expecting it.” Fortunately, Evergreen has been preparing for this eventuality for some time in client portfolios.

Soundbite #3: Robinhood has driven the ‘casino aspect’, or mindset, that has permeated the stock market

Warren Buffett: "[Robinhood] has become a very significant part of the casino aspect, the casino group, that has joined into the stock market in the last year, year and a half. There’s nothing, you know, there’s nothing illegal about it, there’s nothing immoral. But I don’t think you’d build a society around people doing it. I think the degree to which a very rich society can reward people who know how to take advantage, essentially, of the gambling instincts of the American public, the worldwide public – it’s not the most admirable part of the accomplishment. But I think what America has accomplished is pretty admirable overall. And I think actually American corporations have turned out to be a wonderful place for people to put their money and save. But they also make terrific gambling chips, and if you cater to those gambling chips when people have money in their pocket for the first time and you tell them take my 30 or 40 or 50 trades a day and you’re not charging commission ... I hope we don’t have more of it.”

At the beginning of February, we wrote back-to-back newsletters about the casino environment that had descended upon the stock market (see “When YOLO Meets FOMO” and “When a Stock Goes Viral”). At the time, Robinhood was facing massive heat for its handling of several “meme stocks” that went parabolic when a group of influencers pushed a concentrated basket of names into the stratosphere. Meme-stock mania has tamed over the past few months, but as Buffett points out, new platforms have aided and abetted the gambling instincts of the American public, turning (arguably, but not very) worthless assets like dogecoin (and many others) into multi-billion dollar windfalls. However, as we cautioned back in February, nothing worth having (or owning) comes easy and the house almost always wins in the ill-advised game of gambling with publicly-traded securities. Instead, maintaining a long-term mindset is always advisable—but increasingly rare—in the world of investing.

Soundbite #4: SPACs are similar to a ‘gambling-type market’

Warren Buffett: "SPACs generally have to spend their money in two years... If you have to buy a business in two years, you put a gun to my head and said you've got to buy a business in two years, I'd buy one but it wouldn't be much of one. If you're running money from somebody else and you get a fee and you get the upside and you don't have the downside, you're going to buy something…It's an exaggerated version of what we've seen in kind of a gambling-type market."

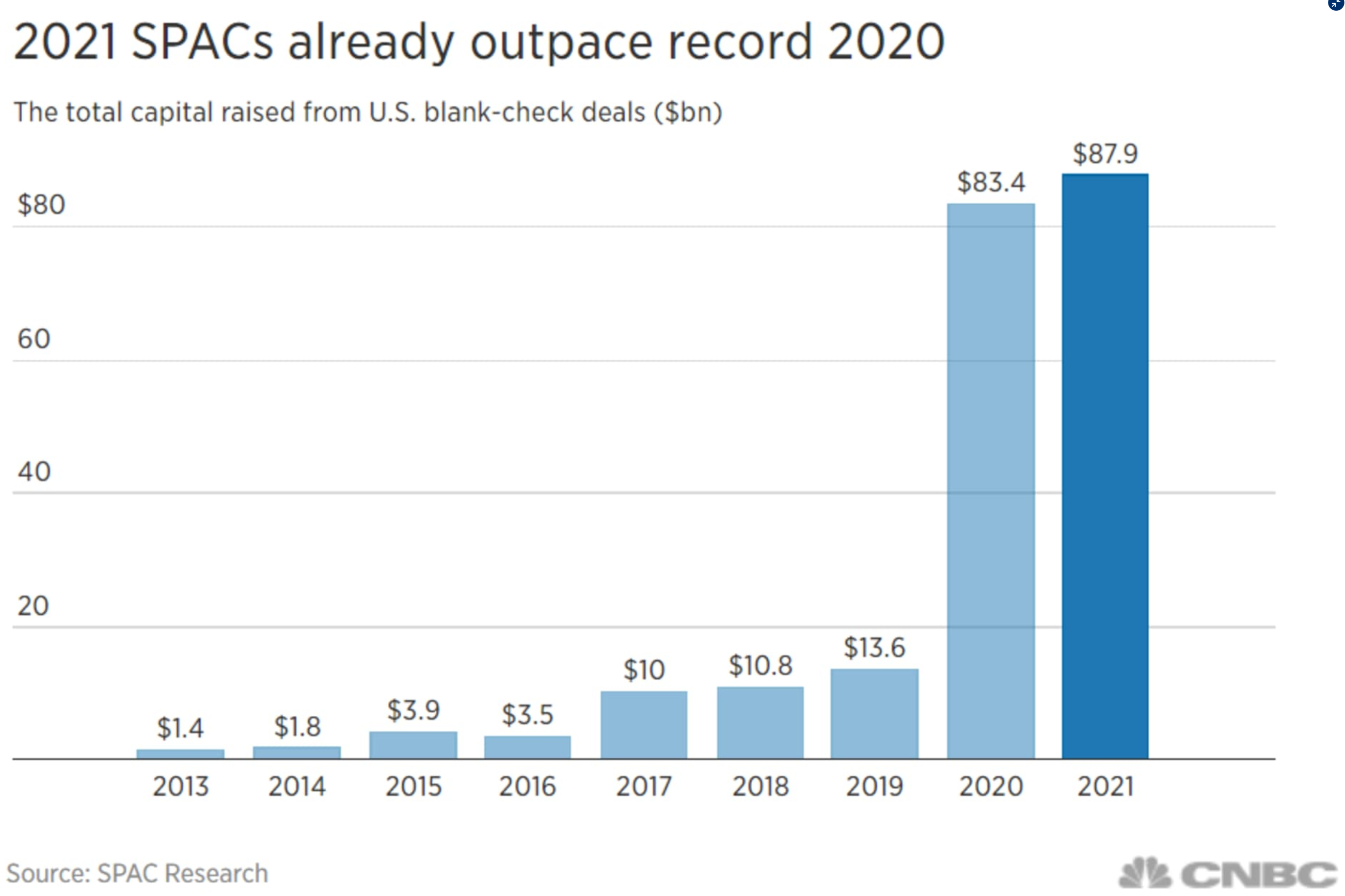

One of the biggest stories in the first quarter of 2021 was the red-hot SPAC market. For those that need a quick primer on the subject, SPACs – or Special Purpose Acquisition Companies – are publicly listed shell corporations that exist for the purpose of acquiring a private company. These “blank check corporations” help private companies circumvent the traditional IPO route, taking companies to public markets by means of a merger or acquisition. While SPACs have existed in the technology, healthcare, retail, media, and telecommunications industries since the 1990s, the market has experienced an astonishing surge over the past two years. In 2020, SPACs raised a record $83.4 billion in the United States, but it took less than three months to outdo its record-breaking 2020, raising $88 billion by the middle of March in 2021.

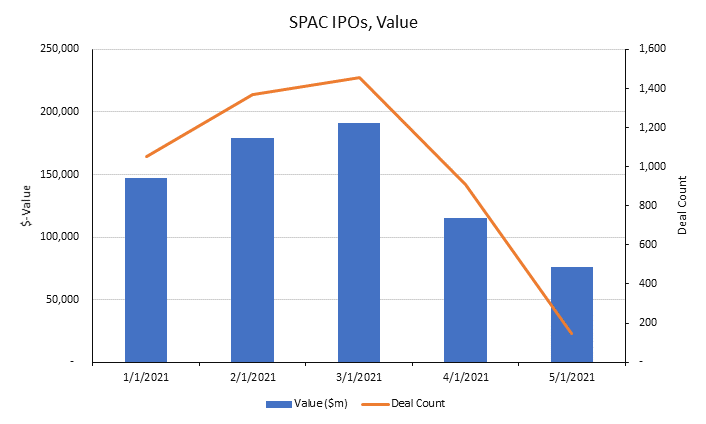

Like most unexplainable and incendiary booms, the industry faced several challenges keeping up with its meteoric rise. One of the many pre-regulatory challenges it encountered was that there were hundreds of deals chasing potential acquisition targets. However, quality companies began drying up like the Sahara Desert, leading to more and more deals that left a lot of seasoned investors scratching their heads and asking, “so how do you justify that valuation?” On top of this, rising interest rates began to make many of these growth companies – which were sometimes pre-revenue – much less appealing.

But the cherry on the top that put the SPAC hot streak on ice at the beginning of the second quarter was unexpected regulatory warnings around questionable accounting practices and growth projections for newly public startups. In what many consider an attempt by the SEC to cool off the market and protect investors from getting burned, the SEC blindsided the industry by stating that some companies might have to restate their financial results due to the way these companies accounted for warrants (essentially, free call options awarded to insiders). Additionally, regulators questioned whether some of these companies went too far in providing unrealistic projections about future results.

As a result, the number of SPAC IPOs took a nosedive in the second quarter of 2021.

Source: Bloomberg, Evergreen Gavekal

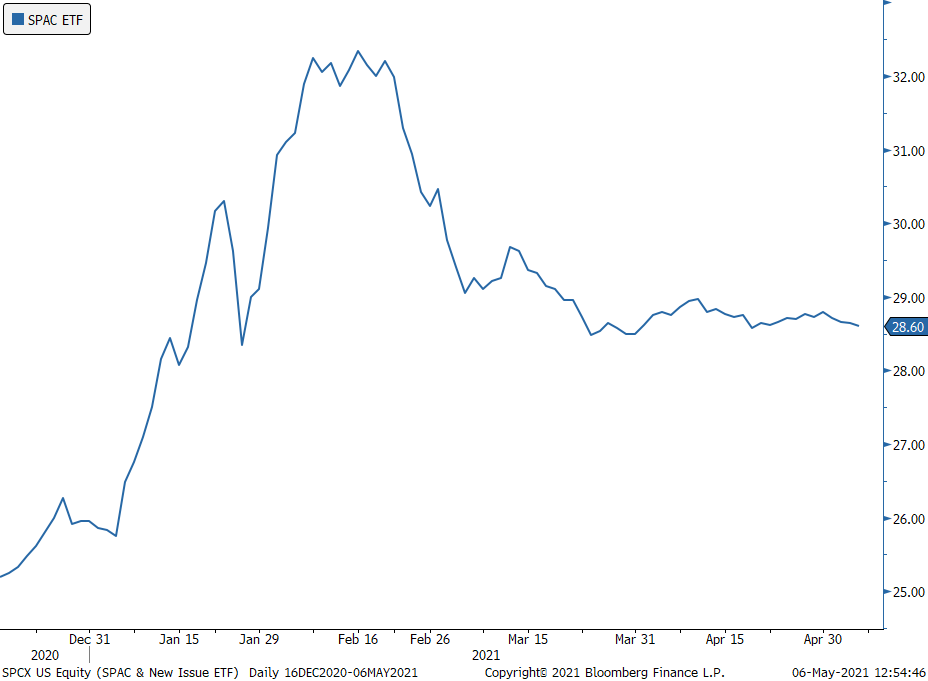

Likewise, newly public companies have seen their shares beaten up like Muhammad Ali’s ‘phantom punch’ since February in a reversal from the beginning of the year.

As Mr. Buffett shared during Berkshire Hathaway’s annual shareholder meeting, in his view SPACs are similar to the ‘gambling-type market’ discussed in Soundbite #3. As such, it’s not surprising that many pre-revenue or low-revenue companies have struggled as pressures have mounted on the SPAC industry and interest rates have ticked north. The question facing the market is whether new deals will see a resurgence, or whether regulatory demands will continue to stifle the market. To borrow two quotes from Mr. Buffett: “I hope we don’t have more of it” and “What the wise do in the beginning, fools do in the end.”

On his last point, investors were wise to be extremely aggressive in the spring of 2020 when most were in the fetal position. But that spring has sprung and it’s time to let the fools have their way—until they are carted away on stretchers.

Michael Johnston

Tech Contributor

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.