“The tour we've taken through the last century proves that market irrationality of an extreme kind periodically erupts -- and compellingly suggests that investors wanting to do well had better learn how to deal with the next outbreak.”

– Warren Buffett

If you’ve been a frequent reader of these pages since 2018, you’re likely well-aware of our propensity to write about “bubbles.” In fact, over the last 2 ½ years, we penned twenty-five installments in our series on “Bubble 3.0”. Without rehashing our thesis in too much detail, our basic argument was (and is) that central bank policies have been the main driver of inflated asset prices over the past ten years.

As the decade-old equity bubble burst in March due to the Covid-19 pandemic, we wrapped up our long-running series (which is currently being combined into a full-length book). However, the conclusion of the series might have been a tad premature because, after an unprecedented sell-off, stocks rebounded in a major way over a very short period of time. You probably guessed it, but the Fed was once again the major catalyst for equities – with a very strong assist to Congress.

“Big tech” has been front-and-center in the resurgence, as mega-cap tech stocks have flourished to market valuations that were considered outlandish in the not-too-distant past. Which begs the question: are tech stocks the next big bubble?

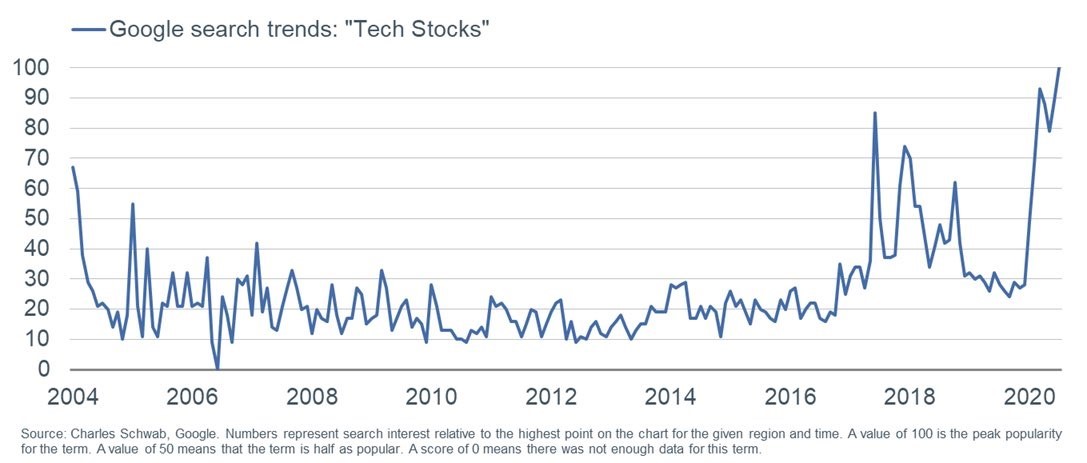

As we outlined in our missive last week, running alongside the thundering herd can be incredibly alluring, but as history has shown time-and-time again, those that jump in at the end of the pack tend to get trampled when the herd suddenly changes direction. And if the latest Google search trends for “tech stocks” are any indication, the herd is running at a parabolic pace towards a very small subset of historically expensive stocks.

This week, we are presenting the second installment in a three-part series from Evergreen Gavekal’s partner, Louis-Vincent Gave, on the question of whether equities in general – and mega-cap tech stocks specifically – have returned to bubble territory. The installment is part of a broader quest to make sense of the exceptional performance of equity markets in the second quarter of this year, despite a still-struggling economy, a raging public health crisis, increased political tension, and an uncertain future. (Click here for Louis’ first missive.) Next week, we will present the final installment in the series, where Louis examines whether the ferocious rally in tech, along with precious metals, has been fueled by the realization that the once-mighty US dollar is destined to become worthless…or, at least, worth a lot less. But more on that next week…

Disclosure: Louis Gave has an equity ownership in Evergreen. Louis’ views and opinions are his own, and are not necessarily the views of Evergreen. Securities highlighted or discussed in this communication are not a recommendation for or against these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Please see important disclosures following this piece.

Charles [Gave] never tires of reminding us that “reading the financial press is bad for your financial health.” Underpinning his belief isn’t just the old adage that “if it’s in the press, it’s in the price,” but also the reality that financial journalists are quick to declare any rising market, a “bubble.”

The definition of a bubble is a period marked by asset prices that have climbed far above historical valuations, and far above the projected earnings capacity of the underlying assets. Of course, the line between a “bull market” and a “bubble” can be blurry even at the best of times—when the visibility of future earnings and the direction of future interest rates is clear enough.

And today is far from the best of times. As we enter unchartered territory for fiscal policy, unchartered territory for monetary policy, and unchartered territory for economic collapse, figuring out where “the blurry line” lies has never been more challenging. In a world in which the Ayn Rand Institute can apply for a Paycheck Protection Loan from the US government with no thought of public embarrassment, anything becomes possible.

This brings me back to the point I made two weeks ago in the first paper of this series: contemplating the exceptional performance of equity markets in the second quarter of this year, investors can come to one of three possible conclusions:

In this paper I shall examine the second possibility: that investors have taken leave of their senses.

Defining Bubbles

Assets typically have value for one of two reasons. They can be rare—gold bars, diamonds, houses on Victoria Peak, bottles of 1982 Pétrus, Van Gogh paintings. Or they can be useful—they help to generate cash flows over time. In past papers, Gavekal has described this distinction as one between “jewels” and “tools.” I bring this up again now because when defining a bubble, the distinction between tools and jewels is extremely important. Throughout history, bubbles have emerged because investors have:

As a result, historically bubbles have either been “efficiency bubbles” or “scarcity bubbles.”

The second key difference between bubbles is the way they are financed. To quote another of Charles’s axioms, investing is first and foremost about finding out whether there are “more fools than money, or more money than fools.” In an environment of “more money than fools,” investors should expect asset prices to rise; when vice versa, asset prices fall.

In our economic system, two sorts of entity have the ability to create excess money: (i) central banks and (ii) commercial banks. When commercial banks provide the excess capital to fund a bubble, as in Japan from 1985-89 or the US in 2005-08, the hangover tends to be deflationary. When central banks provide the excess capital to fund the bubble, as in the US in 1998-2000, a sharp currency devaluation usually follows the bubble’s implosion.

Combining these two taxonomies gives four different species of bubble:

Now we’ve identified the four different species of bubble, the obvious question is whether we are facing a bubble today, and if so, which kind?

Recent times have been “bubble prone”

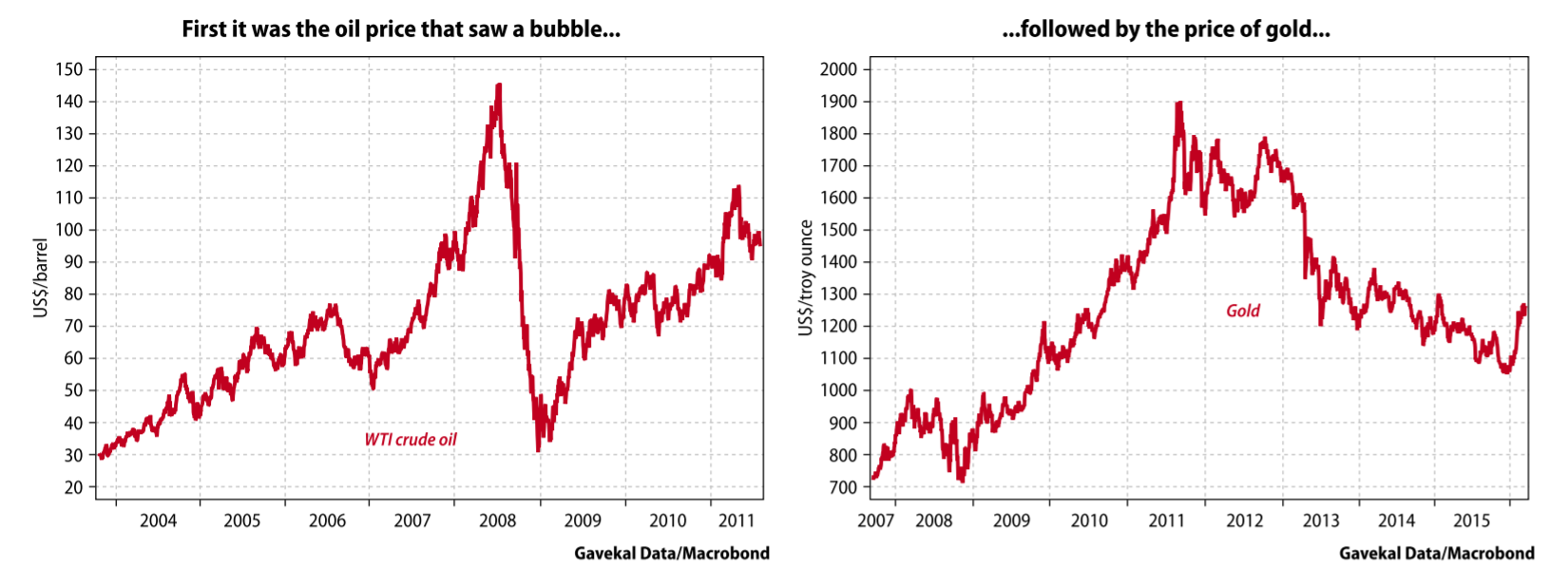

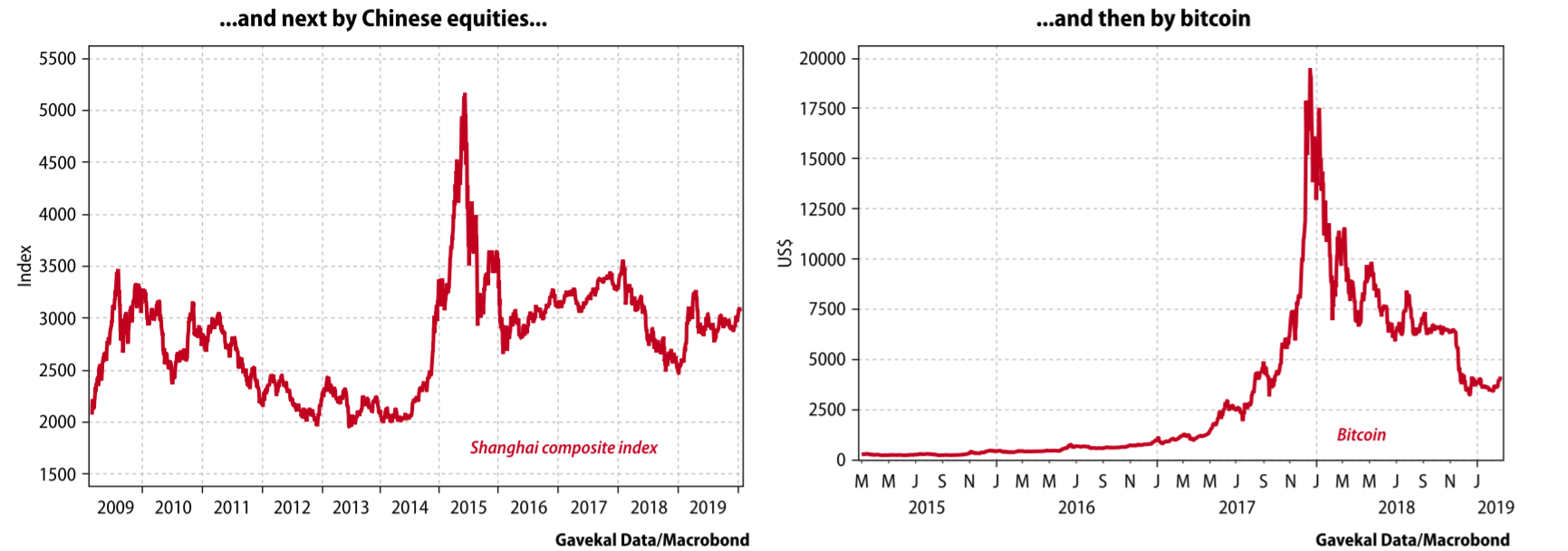

Before I tackle the current situation, I should point out that the years since 2008 have been fertile ground for “spontaneous” bubbles. This may be because of the zero interest rate policies adopted around the world. Or it may be because the savings industry has now become a global business, enabling money from all over the world to crowd into a single asset class. Time and again in recent years, we have seen a particular asset class suddenly catch the imagination of the global investing public, and in short order the prices of the underlying assets begin to rise very quickly indeed. Examples include:

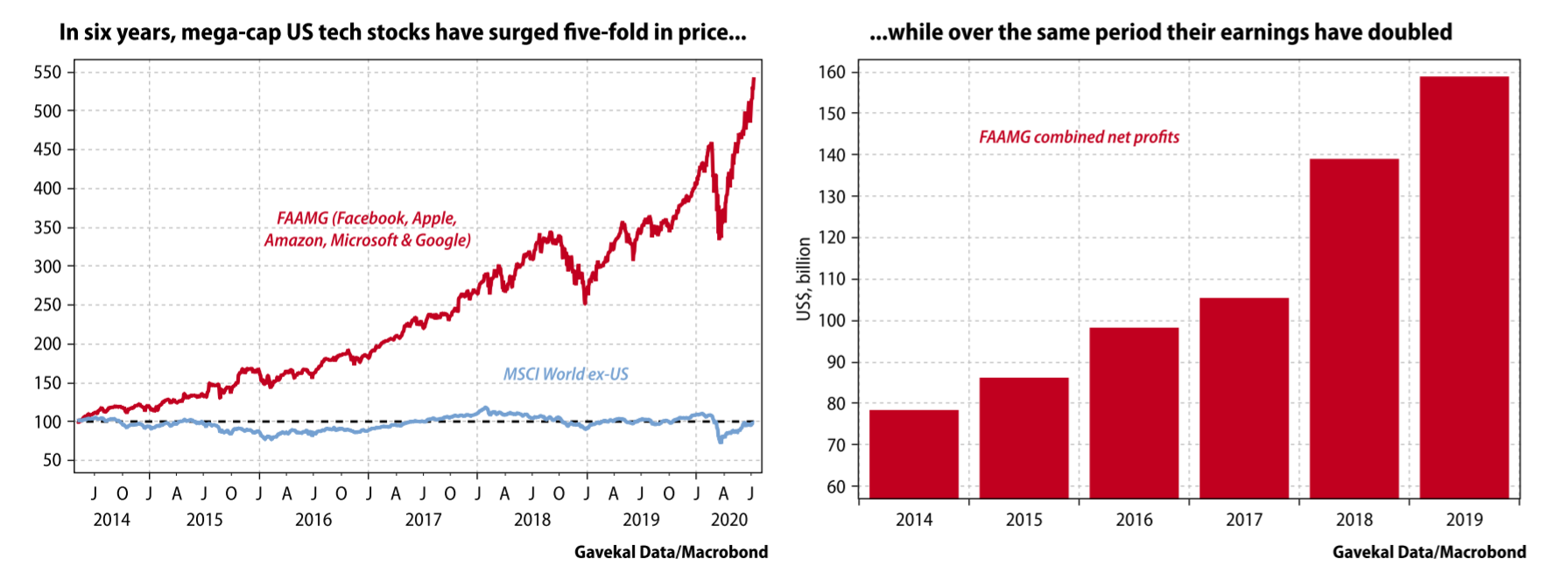

Today, capital is flooding into a handful of mega-cap US tech stocks. In fact, as the left hand chart below shows, the top five companies in the world by market cap today have risen five-fold over the past six years, while over the same period the MSCI World ex-US index has flat-lined. Given the picture shown by this chart, it is hard to argue that equity markets as a whole are in bubble territory. If the MSCI World ex-US index has spent the past six years going essentially nowhere, it falls at the first hurdle of a bubble’s definition—that asset prices have risen so far they have lost all relation to the underlying reality. If there is a bubble in global equity markets today, then the bubble is squarely in “big tech”. The question today is therefore not whether global equity markets are in a bubble (they are not), but whether the people who are investing in big tech have taken leave of their senses.

Is Big Tech in a bubble? And if it is, what kind of bubble is it?

Perhaps the simplest way to answer the first of these questions is to look at the phenomenal rise in big tech’s share prices over the last few years, and compare this performance to big tech’s earnings. Between 2014 and 2019, the combined after-tax profits of Facebook, Apple, Amazon, Microsoft and Google grew from US$78.4bn to US$158.9bn. That’s slightly more than double, or a compound annual growth rate of roughly 15%.

That’s nothing to sneer at, of course. Growing profits by 15% a year over a period when global growth was just a fraction of that is impressive. But it is not nearly as impressive as the share price performance of the same five companies’ stocks. Between the beginning of 2014 and the end of 2019, FAAMG share prices rose by 26% a year. So, the US$80bn increase in profits delivered by FAAMG unleashed a US$3trn increase in FAAMG market cap— and a US$4.4trn increase if you take today’s market cap. That’s quite a bang for the buck!

So yes, we can say FAAMG are in a bubble. But going back to our initial distinction, is it an “efficiency” bubble or a “scarcity” bubble?

Efficiency bubble or scarcity bubble?

It seems clear that the past decade’s sharp rises in energy, gold and bitcoin were driven by the “scarcity” belief. Not only that, but the 2015 China A-share melt-up was also a scarcity bubble, as it was driven in large part by the hope that China’s inclusion in the MSCI emerging markets index would set off a massive rush among foreign investors for exposure to Chinese assets—and that there simply wouldn’t be enough A-shares to go round.

But what about today’s widening gap between the share price performance and market cap of big tech on one hand, and the ability of the underlying companies to deliver ever-greater profits on the other? Fundamentally, there are two possible explanations of this divergence:

Of these two options, the latter seems more likely. Consider the following:

Take Google and Facebook to illustrate this second point. In 2019, global advertising spending was US$560bn. This includes online ads, but also ads in newspapers, logos on soccer and rugby shirts, the names of stadiums, ads on bus shelters and so on. Of this total, Facebook captured US$73.4bn (or 13.1% of global advertising), while Google gathered an even more impressive US$113.3bn (20.2% of global ad spend). In other words, between them the two tech giants already capture a third of all global advertising spending.

From here, it is natural to ask where the two behemoths’ future growth will come from. If we assume that the global advertising market grows by roughly 3% per year, as it has done over the last decade, while the revenues of Google and Facebook grow at 20% per year, then by 2027 the combined revenues of the two companies will be greater than the entire global advertising market (and this doesn’t allow for the ambition of Amazon to get itself a healthy slice of the ad market, or that of Alibaba and Tencent).

In other words, if Google and Facebook are to register 20% revenue growth for the rest of the decade, they will have to find their growth somewhere else, besides their currently highly profitable niche of online advertising. If the future growth currently embedded in the companies’ share prices is to be realized, they will have to re-invent their businesses.

This may happen, or it may not. Or it may happen for some, but not others. But however you cut it, it is hard to avoid the conclusion that there is a growing dislocation between big tech’s share prices and future earnings capacity. As a result, the rationale underpinning the current FAAMG bull market must be more one of scarcity than of expected future earnings.

Big tech—the new scarcity asset

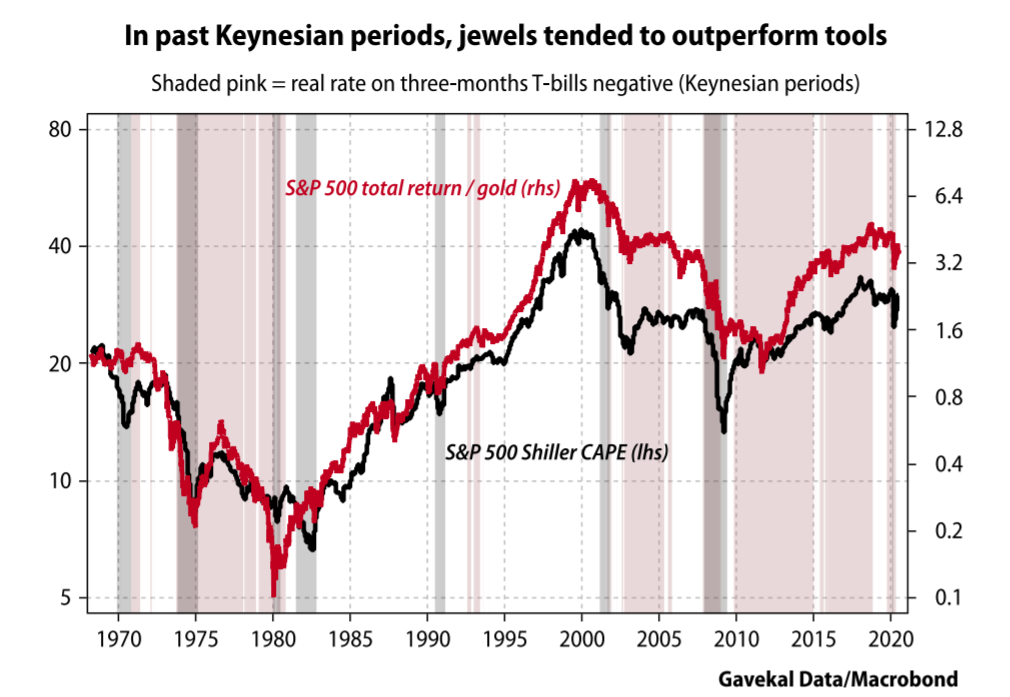

When the US Federal Reserve deliberately keeps interest rates much lower than the structural growth rate of the US economy, and when US monetary aggregates grow much faster than their average over recent decades (for convenience in past reports, we have called such periods “Keynesian”), then “scarcity” assets tend to outperform “efficiency” assets. And vice versa: when interest rates are kept at roughly the same level as, or higher than, the US economy’s structural growth rate (in past reports, we have called such periods “Wicksellian”), then efficiency tends to outperform scarcity. In short, when the central bank is Keynesian, investors should buy scarcity assets (jewels), and when the central bank is Wicksellian, investors should overweight efficiency assets (tools).

This rule of thumb has worked very well since Richard Nixon jettisoned the US dollar’s peg to gold, so lifting the constraints on US monetary policy. The rule’s long-term effectiveness is illustrated in the chart below, in which the areas shaded pink represent Keynesian periods, while the white areas represent Wicksellian periods.

But “worked” in the past tense appears to be the correct word here. For much of the last decade, and doubly so today, the Fed has been pursuing an aggressive Keynesian policy. However, over the same period, US equities, and especially US growth stocks, considered the most efficient part of the efficiency basket, have significantly outperformed gold, the ultimate jewel or scarcity asset.

So why has the rule stopped working? Here is a suggestion: in recent years, there has occurred an historically unusual reversal of perceptions among investors about what is scarce and what is abundant.

In short, we are on the other side of the mirror, where commodities are now an efficiency asset, and big tech has scarcity value. So, as central banks continue to pump ever more money into their economies, instead of going into gold, fine art, or Château Pétrus as before, the newly-minted money is flowing into monopolistic big tech; today’s ultimate scarcity asset.

This is unusual, but not unprecedented. Back in the Keynesian period of the late 1960s and early 1970s, investors flocked into what were then called the “nifty fifty” stocks. Back then, the prevailing view was that only large multinationals could deliver growth and reap the harvest of coming globalization. As a result, the excess money pumped into the system pushed the valuations of “scarce” multinationals ever higher. Or it did until 1973, when oil prices spiked, and all of a sudden investors were forced to reassess what was scarce (oil) and what wasn’t (cross-border production and distribution capacity).

Investors have long ago forgotten about the nifty fifty. Instead, today we have the nifty five—Facebook, Apple, Amazon, Microsoft and Google. What could be scarcer than a duopoly in online advertising? Or a hold on a major chunk of the fast-growing cloud computing business? Or a worldwide retail base, fueled by solid knowledge of your individual customers? Or a tech ecosystem that keeps its users locked in and buying hardware products at prices far above those charged by any other producer? Undeniably, these are rare attributes. And so, the valuations of the nifty five continue to scale new heights. In this environment, the most important question facing investors is whether these scarcity premiums will continue to grow over the coming years. To put it another way: what are the threats to this scarcity premium?

This last point brings me to the discomfort that so many investors (present company included) feel today when looking at the current tech-led market surge. If the assumption that the value of tech shares is soaring because of some kind of scarcity premium is correct, then economic history teaches that in capitalist systems scarcity seldom persists for long.

Historically, scarcity has been more commonly associated with socialist systems. In fact, no one excels at delivering scarcity as much as socialists—to the extent that you have to wonder whether scarcity isn’t a bug of socialism, but rather an inherent feature. In contrast, the core feature of capitalism is the delivery of abundance; when a situation develops in which established players earn outsized rents, competition usually emerges (for example, with TikTok coming in to eat Instagram’s lunch). And if competition doesn’t emerge by itself, then democratically-elected governments will soon step in to claim their pound of flesh.

Bearing in mind capitalism’s historical track record, to project the current monopoly rents of big tech far into the future looks much like a second wedding—a triumph of hope over experience. Unless, of course, you want to assume that the capitalist system has started a transition to a far less capitalist future...

Conclusion

Mike Tyson used to say, “everyone has a plan, until I punch them in the face.” To some extent, the same is true of equity investors: each of us has a plan, even as we acknowledge that the punches can come from every different direction.

This year, the punch in the face came from the Covid-19 pandemic, an exogenous shock of a severity seldom seen before. And this punch in the face has split global equity markets into four sub-groups, each with very different drivers and trajectories.

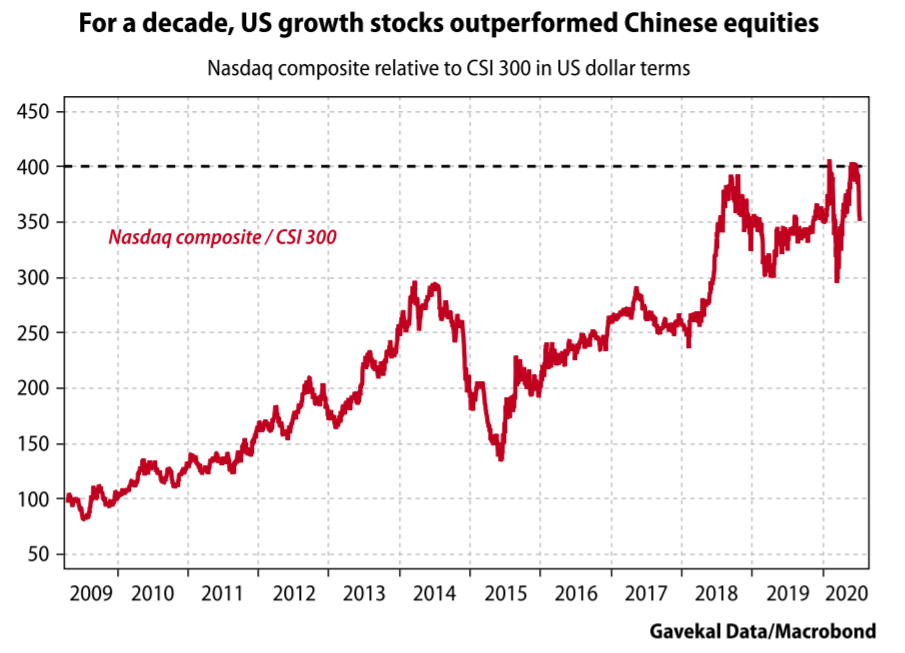

A few weeks ago, global equity markets were being pushed higher by a combination of the first and second baskets: big tech and Covid victims. In recent weeks, this has shifted and instead the bull market is being driven by a combination of big tech and the fourth basket: cyclicals, financials and emerging markets. As a result, while most major equity markets are still down year-to-date, which makes sense given the magnitude of the economic shock, two markets have bucked the trend: the Nasdaq with a 17.6% YTD gain and China’s CSI 300 with a 15.3% YTD US dollar advance. The first of these—big tech—depends on a strong US dollar to thrive. The second—China—tends to do best when the US dollar weakens. As a result, the next move in the US dollar is likely to dictate whether the relative performance of big tech surges to new heights, or whether a new bull market centered on China takes hold.

As readers know, for a multitude of reasons I am a US dollar bear. My strongly-held conviction that the US dollar is cruising for a bruising leads me to believe that the days of US tech outperformance are also numbered. But having said that, and to finish on a positive note, the great news about the current tech bubble is that it is broadly the best kind of bubble: a bubble in productive assets, funded by excess central bank liquidity. That means the hangover shouldn’t be too painful.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.