“Possibly without serious vetting and a conscious decision to adopt it, Modern Monetary Theory is here. Whether we like it or not, we’ll get to see its impact much quicker than I had thought."

– Money manager extraordinaire, Howard Marks (for more on Modern Monetary Theory, please see the following introduction)

Veteran EVA readers will undoubtedly recognize the name Gerard Minack, who is the author of one of my regular reads, the Down Under Daily (DUD). As you might expect from its name, Gerard hails from the Lucky Country, more commonly known as Australia.

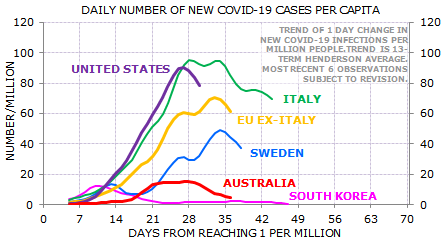

Befitting its nickname, Australia has been quite fortunate when it comes to the coronavirus. Gerard sent me this chart last week, perhaps indicating both the aggressive response by the Aussie government and that Covid-19 doesn’t proliferate as easily in warm weather, something we should all hope happens north of the equator as spring turns to summer.

Despite his southern (and eastern!) hemisphere-located homeland, Gerard is an insightful commentator on American financial markets. In this edition of his DUD — which in no way resembles the US definition of that abbreviation!— Gerard makes some critical points about how the global pandemic will potentially reorient the investment universe.

One of his main themes is that the unparalleled global government responses to the outbreak, totaling in the trillions (possibly over $10 trillion worldwide) is likely to end what he and many others call secular stagnation. This high-falutin’ term basically refers to a long period of sub-par economic growth such as the world has endured since the Global Financial Crisis (GFC) of 2008/2009. As countless prior EVAs have observed, even the US, home to the best performing major stock market of the last decade, has experienced the weakest expansion since WWII.

Thanks to the pandemic, that feeble, though long-lasting, growth cycle is now history. In fact, credible estimates are the US economy might contract by an almost inconceivable 30% to 40% this quarter, with many other countries enduring a similar free-fall. In response, governments around the world, and especially in Europe and North America, are committing to spend trillions of dollars (or euros or pounds) to prevent an economic Apocalypse (or, almost certainly, a worse one than we already have!). And because precious few governments have the ability to borrow the needed trillions through the bond market (at least not without driving interest rates up significantly), their central banks will, in most cases, be expected to ride to the rescue—again! There is little question they will digitally fabricate the equivalent trillions to fund these enormous deficits. How enormous? Good question!

According to another one of Evergreen’s go-to sources, crack economist David Rosenberg has stated that deficit spending will amount to about 20% of GDP in the US. That equates to roughly $5 trillion in US dollars (some estimates are even higher and I’m leaning toward the over in this regard). David has one of the more guarded views of the bounce-back from the virus shut-down, but even he doesn’t expect a full-year GDP hit of more than around 5%. In other words, based on the current (or, at least, what was prior to the outbreak) GDP run-rate of $23 trillion, the US is planning to inject $5 trillion to plug a $1 trillion dollar hole.

That certainly sounds like enough to end secular stagnation…at least if the solution to an under-achieving economy is unprecedented government spending, outside of a world war. (It should be noted that due to its fiscal discipline during the good years, Germany is in a position where it can comfortably add to its debt levels without resorting to money fabrication by the European Central Bank. For the rest of Europe, however, it’s a much different—and depressing—story. On this topic, my great friend and gifted partner, Louis-Vincent Gave, believes we are on the brink of a cataclysmic European crisis – not exactly what the world needs right now.)

Per the Howard Marks quote at the top of this piece, what we are effectively seeing is the rapid and on-the-fly implementation of the once-fringe economic theory known as Modern Monetary Theory (MMT). As some EVA readers may remember, this was a key topic explored in these pages early last year. This thesis created a sensation as several leading Democratic presidential candidates at the time either openly embraced it, especially Bernie Sanders, or, at least, flirted with it a bit. Most mainstream economists, however, even those left-of-center, dismissed it as dangerous, ill-advised, unlikely to work, inflationary, or all of the above—and then some. However, Howard Marks is right. MMT is exactly what we’ve got, a theme to be explored in the upcoming final chapter in the long-running EVA “book in real-time”, “Bubble 3.0” series.

Returning to Gerard’s missive, he believes that excessive savings relative to investment demand has been the cause of secular stagnation. Consequently, he thinks the aforementioned government spending blitz will accomplish its objectives. But he’s mindful of the long-term risks this ultra-radical approach poses.

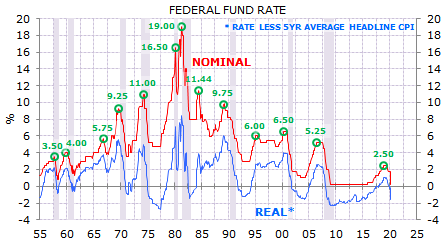

For one thing, with the US now largely eradicating interest rates on its government debt, these bonds will no longer provide a return to investors. This is in no small part due to the relentless Federal Reserve purchases of treasuries, which is what I, and other impolite observers, have called QE4 – i.e, the fourth round of quantitative easing. (Let’s not quibble about 0.75% or even 1%; those are close enough to zero to ignore, barring deflation which is almost certain to be fleeting based on the trillions of fake money coming our way.)

As Gerard points out, this has profound investment implications. If treasury bonds no longer provide a yield to investors, then their diversification benefits for balanced investors (like in a half-stock, half-bond portfolio) are greatly reduced. Further, as he describes, when the rate of return on government bonds is around zero, they become much more volatile*. Thus, a holder of supposedly riskless debt is now subject to high volatility and no return; essentially, it’s the worst of all investment worlds.

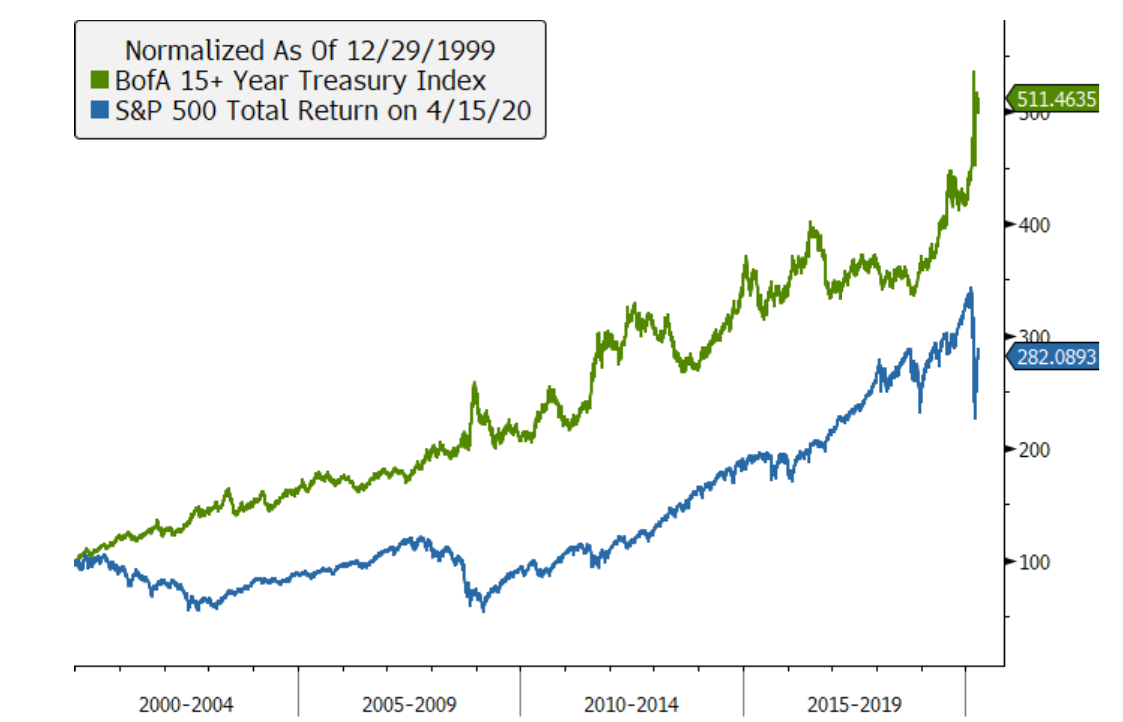

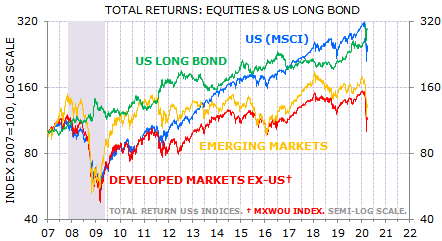

This is a monumental shift versus the way things have been. Most people I speak with are unaware that long-term treasury bonds have trounced even the planet’s equity market star—the S&P 500—over the last twenty years. So much for stocks for the long run! Instead, it’s been bonds for the long haul…but the times, they are a changin’.

Source: Bloomberg, Evergreen Gavekal

In my view, we are moving back into a period where bonds are known as certificates of confiscation, a derogatory term I remember from my early years in the investment business (circa 1979 to mid-1982). However, presently, the story with corporate bonds, non-government backed mortgages, and preferred stocks is very different. We believe these continue to offer high returns over inflation – at least today’s inflation which is actually deflation for now. (As we’ve written in recent weeks, Evergreen has been avid buyers of these for its clients, locking in some truly remarkable yields. However, the massive rally seen since March 26th has for sure take a decent amount of bloom off the rose—and cash flow out of the equation.)

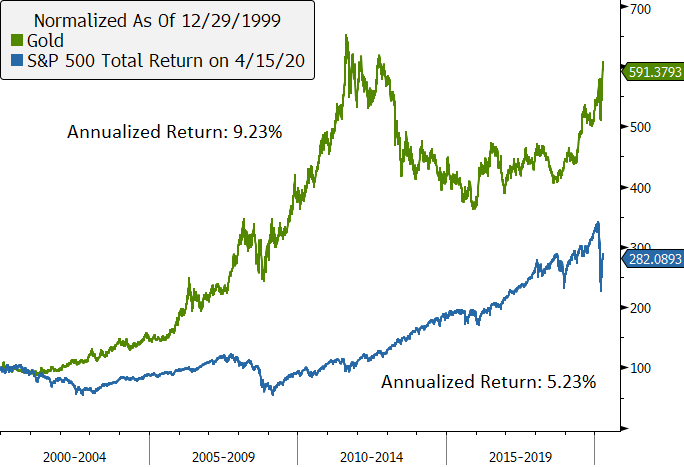

By the way, as an aside, you might also be able to win some serious money by betting your irritating brother-in-law—you know, the one who loves to brag about how great his stocks have done—that it’s not just bonds which have trounced stocks over the last two decades. Another asset class has done the same with little fanfare and despite very low global inflation. Interestingly, it’s the very same one Gerard touts at the end of his note and that we hyped towards the end our April 3rd EVA introduction. Even if you only read Gerard’s summary at the end of his piece, don’t miss that punchline!

Source: Bloomberg, Evergreen Gavekal

*For bond geeks, this is due to the increase in duration when a bond’s yield is around zero. For example, a twenty-year bond paying 6% per year (those were the days!) has a duration of only 11.3 years, whereas a 20-year bond with a 1% yield has a duration of 17.6 years. The reason, of course, is the much higher cash flow received early on with the higher interest rate which shortens the pay-back time—or duration—to the holder of that bond.

If the Covid-19 crisis leads to helicopters sustained fiscal-monetary policy coordination it could end the secular stagnation era. Ending secular stagnation would change many of the trends that have shaped markets for 40 years, particularly since the GFC. Near term markets will remain in thrall to Covid-19 data and expectations about the downturn and subsequent recovery. This note looks at the changes likely to appear after the crisis passes.

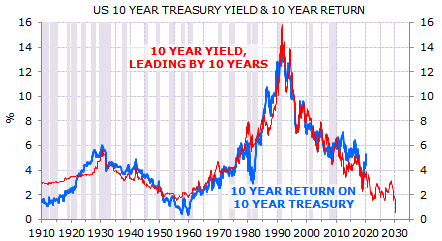

The most important economic feature of secular stagnation was the widening gap between desired saving and planned investment. This increase in excess saving caused the most important financial feature of secular stagnation: the trend decline in the neutral rate of interest. There are always cycles in interest rates. But the trend decline in the neutral rate meant that in the US the cycles in market rates have been a series of lower highs and lower lows through the past 40 years.

If secular stagnation ends, then the neutral rate of interest will start to trend up. That suggests that the next cycle peak in rates will be higher than the last cycle peak – something not seen since the 1970s. However, the early signs of this structural shift may be suppressed if central banks deploy yield curve control (that is, price fixing for rate markets).

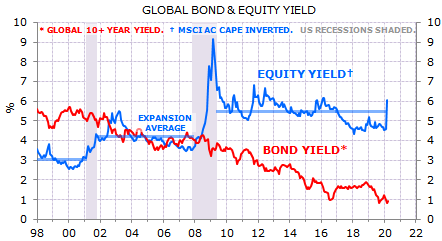

Sovereign bonds provided a number of attractive investment features as economies were secularly stagnating. They generated high returns as yields fell, were typically less volatile than equities, and they were inversely correlated with risky assets so offered tremendous diversification benefits. Looking ahead, I can’t see any scenario where sovereign bonds retain all those attractive features. Arguably the worst scenario is economies remain secularly stagnant, or yields are held at artificially low levels either by central banks or some other form of financial oppression. The prospect of yields rising is not as bad, but not as good as the recent past. Here’s what’s going to change:

Bonds generated unusually high returns as economies were secularly stagnating. Bonds have generated equity-like returns since the GFC. The US long bond has produced higher returns than equity markets outside the US for some time.

The forward-looking point is that yields now at all-time lows point to all-time low prospective returns even if secular stagnation remains intact.

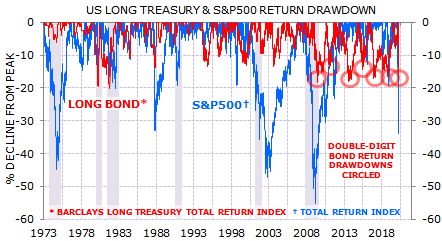

A second attractive investment feature of bonds was that they were less volatile than equities. That feature has already faded: as yields fall duration rises, so a given yield change now reflects larger price swings. While bonds may have produced equity-like returns in this cycle, long-end bonds have also seen more double-digit return draw-downs than equities since the GFC.

If the world remains secularly stagnant bonds would offer low returns with high equity-like volatility. If secular stagnation ends then the outlook would be for significant upfront mark-to-market losses on current bond holdings, but ultimately higher yields would point to higher prospective returns. Moreover, at higher yields (shorter duration) return volatility would fall.

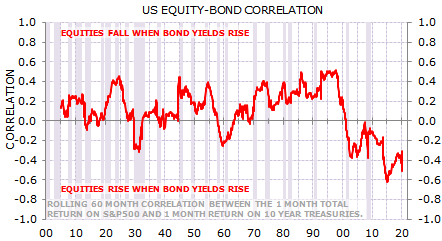

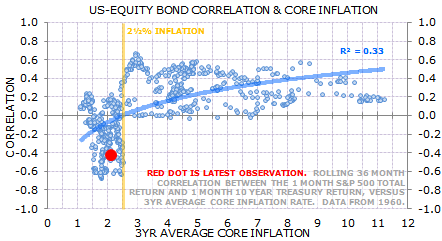

Bonds’ third attractive feature was their inverse correlation with equites. This provided diversification benefits for asset allocators. But the persistent inverse equity-bond correlation of the past two decades is unusual.

History suggests that equity-bond correlations are driven by the inflation regime. The chart below shows rolling 3 year US equity-bond correlation and 3 year average core inflation. If policy makers can end secular stagnation and lift trend inflation then there’s a high prospect that equity-bond correlations will flip to positive, weakening asset diversification strategies.

Secular stagnation has had a material effect on asset valuations. The impact, on average, has been positive – but it has also been uneven. The combination of falling discount rates and anemic nominal economic growth led to a rising valuation premium for assets with a reliable or rising coupon.

Consequently, the impact of secular stagnation on equity valuations has not been straight-forward. The yield on global equities has not fallen on a cycle-average basis after the GFC despite the trend decline in bond yields.

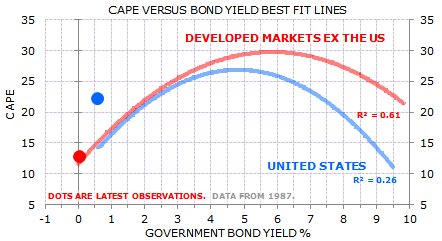

What is going on? Investors recognize that the macro conditions that are driving rates to very low levels also increase earnings risk. As a result, there is not a linear link from rates to equity valuation: equities can re-rate as bond yields fall from high levels, but then de-rate as yields fall towards zero. The chart below shows best-fit lines of the relationship between bonds yields and equity valuation (CAPE).

The US market has re-rated through this cycle. I think this is partly because (so far) US long-end yields have not fallen as far as rates elsewhere. Second, US corporate earnings are seen as being more resilient or reliable than other markets’.

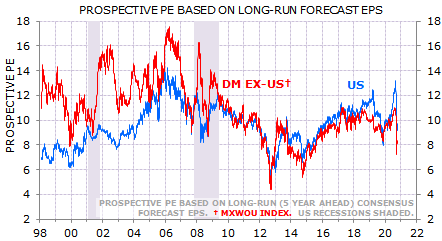

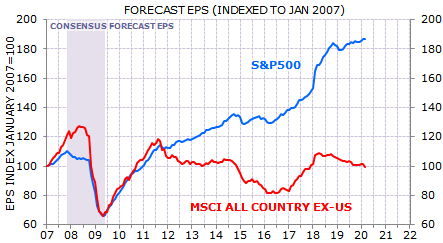

Long-run (5 year-ahead) expected EPS levels capture the presumed superior resilience of US earnings. US equities had not re-rated relative to history or relative to other markets once account was taken of long-run EPS expectations.

Put another way, US equities out-performed as rates fell because investors were more confident of long-run expected earnings in the US than elsewhere. This makes intuitive sense: European and Japanese markets have a heavier weight to cyclical sectors than the US, so macro weakness is a major threat to earnings. In any case, aggregate EPS outside the US has shown no growth since 2007 and has fallen from 2011. Put simply, global equities outside the US have not been able to generate a reliable coupon and so no re-rating was warranted.

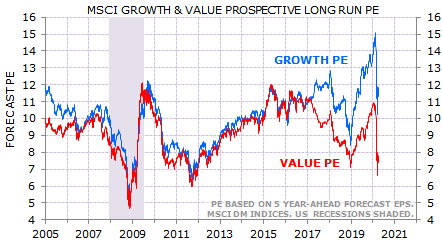

The out-performance of growth versus value is a similar phenomenon. However, the performance gap has been more extreme than the US versus non-US gap. The chart below shows the prospective PE for developed market growth and value sectors, based on forecast 5 year-ahead EPS levels. Growth has re-rated relative to value, even taking into account the expected superior EPS growth.

The forward-looking point is that the end of secular stagnation could provide cyclical markets with a boost both in terms of relative valuation and relative EPS growth. The prospect of higher trend nominal economic growth would reduce the premium now being paid for sectors or markets that appear to offer superior earnings growth and earnings certainty. In short, if the ability to grow earnings becomes less scarce, the premium valuation of companies that have been able to grow earnings in stagnant economies will start to fall.

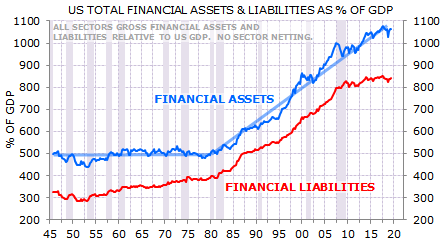

The trend decline in rates encouraged the use of leverage to enhance returns. This often involved creating new financial instruments that combined leverage with an economic income stream. The result was a trend rise in financial leverage and financial assets. Financial leverage will become less attractive in a world of rising rates.

The second major global crisis in just over a decade has highlighted the fragility of many economic systems. Increasing financial resilience may include policies to discourage leverage, reduce buy-backs, and strengthen corporate balance sheets. This would imply lower corporate distributions to shareholders and lower return on equity.

Policy makers have struggled to hit inflation targets for two decades. The policy tools that can end secular stagnation can also lead to inflation overshoots. Inflation hedges will become more attractive. Whether bond yields will be allowed to price this reality is moot, but inflation swaps will do the trick. Oh, and yes, gold also.

Finally, none of this is a view on the near-term. In the initial rally from the Covid-19 crisis lows it may be that markets look much as they did prior to the crisis. This note is about how markets behave once we settle into the post-Covid-19 cycle.

In summary:

Inflation is more likely to hit policy targets, and the risk of unacceptably high inflation will rise. Buy inflation hedges. Buy gold.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.