“I believe in the Golden Rule - The man with the gold... rules.”

– Mr. T

______________________________________________________________________________________________________

For several years, Evergreen’s weekly publication of Likes/Dislikes has maintained gold and gold-mining stocks in our “Likes” category. However, despite our long-term conviction, at times we have conceded that the asset class looked overextended and, thus, advised some profit taking and rebalancing. Last August is one example, when we updated our recommendation and presented a missive from Louis-Vincent Gave titled “What Will Stop the Gold Bull Market?”

In the introduction to that newsletter, we shared that Louis Gave has – for most of his career – been the furthest thing from a gold bug. Therefore, his shift in tone was noteworthy. Around the same time, Warren Buffett changed his long-dismissive view on the shimmering asset and took a small position in a well-known gold-mining stock. Despite the endorsements from two extremely respected investors, we warned that the asset class had become uncharacteristically crowded and looked expensive on a near-term basis. Between August 2020 and March 1st, 2021, the price of gold bullion sold off 18.4%. Gold miners were also hit hard, falling nearly 31%.

However, after a lackluster fall and winter, gold has made it to the front page once again. Of course, that’s not entirely unexpected after a 12.4% rebound in the price of gold bullion since March, which shot the asset back above its 200-day moving average.

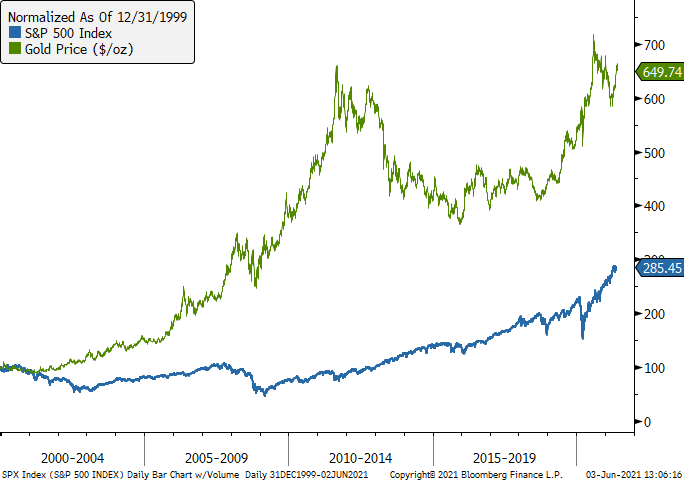

This week, we are relaying a thoughtful letter on the subject from, once again, Louis Gave. In this article, Louis makes the case that gold could be the next trade to break out into bubble territory and join a series of rolling bubbles that has seen everything from electric vehicle companies to digital coins fly themselves to the moon…and beyond. However, unlike EVs and cryptocurrencies, the once-mocked “barbarous relic” has maintained its allure for thousands of years. Even looking at a much shorter time horizon (which is still before the genesis of EVs and cryptocurrencies), gold has – to the surprise of many – significantly outperformed the S&P 500 since the turn of the century. (As David Hay has noted in the past, you can win a lot of money at cocktail parties with that little trivia teaser.) The question for investors becomes: is there more good fortune ahead for gold bulls? Thanks to the concerted efforts of the Fed and the US treasury, we think the answer is…full stop! Let’s allow Louis to take it from here.

My friend Kevin Muir, whose terrific MacroTourist newsletter is both very actionable and very affordable, has described the last year’s investment environment as a series of rolling bubbles: as electric vehicle plays reached dizzying valuations, investors seemed to realize that EVs use about five times as much copper as combustion-engine cars, so copper miners duly soared to new heights. Then crypto was the next big thing, followed by video games, lumber, shipping... and so on. The bubbles have just rolled on from one exciting asset to the next, with investors wondering which will follow. In this note, I will explain why I think gold may be the next one.

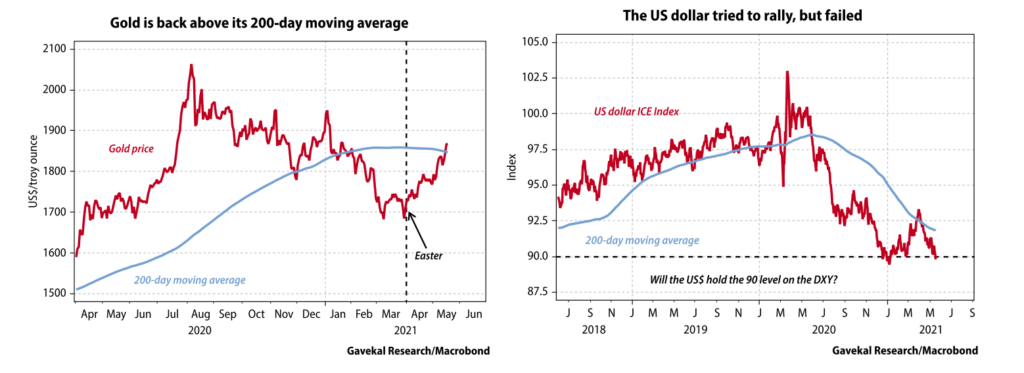

To start with, after a fairly ugly August 2020-March 2021, gold is looking technically stronger. On Tuesday, May 18th, the gold price sliced through its 200-day moving average (see left-hand chart below), which may have the effect of attracting the attention of algos and momentum investors.

Also, this rebound is occurring against a macro backdrop that is generally favorable to gold: US treasury yields seem to have stalled in the 1.60-1.75% range (gold’s August-March downdraft coincided with the rebound in US bond yields) yet US inflation data is surprising (some people) on the upside. At the same time, the US dollar—as measured by the DXY index—seems to be breaking down (the right-hand chart below shows that on Tuesday it fell below the psychologically important 90 level).

An environment of constrained yields, rising inflation and a weaker US dollar is manna from heaven for gold bulls. This environment may change but until it does, the gold price is likely to grind higher, posing the question: will it take out last summer’s high? For the following reasons, I think it will:

Putting it all together, the odds thus seem skewed towards precious metals being the next “rolling bubble”.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.