"Never mistake a wish for a certainty."

-Maggie Smith, as Violet Crawley, the Dowager Countess on Downton Abbey

POINTS TO PONDER

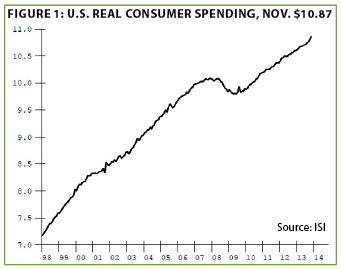

1. Irrespective of the punk jobs number last week, it does appear US consumer spending ended 2013 on a robust note. Real consumer expenditures apparently rose 4% as the fourth quarter came to a conclusion. (See Figure 1)

2. With tax revenues up, at least partially due to the largest tax increase in US history, and expenditures flat, the US budget deficit has been cut in half since 2010. While the remaining $700 billion is still a massive amount of red ink, the drop more than offsets the amount the Fed is buying of US Treasury securities (the Fed has been buying $45 billion per month of Treasuries and $40 billion per month of government-guaranteed mortgages).

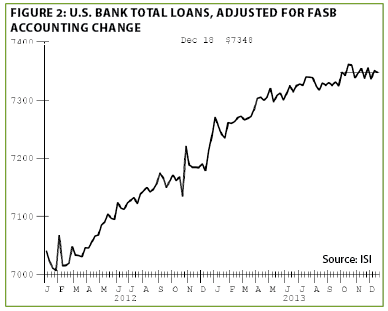

3. The main reason the Fed’s synthetic trillions have not produced either robust growth or rampant inflation is the implosion in money velocity. Given that bank loans, a key driver of velocity, continue to flatline, this is unlikely to change anytime soon. (See Figure 2)

4. At least thus far, bonds have reacted with equanimity to the Fed’s tiny taper. This is possibly because sentiment was fiercely negative before the December announcement of the slight reduction in quantitative easing.

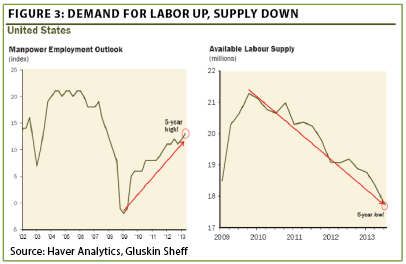

5. Although the number of jobless Americans remains distressingly high, it seems conditions are tightening for the employed and employable. Also lending credence to the thesis of rising wages for those fortunate enough to have jobs, a recent Fed report found extreme labor shortages in sectors involving 40 million workers. (See Figure 3)

6. Based on generally accepted accounting principles (GAAP) earnings—otherwise known as profits including the bad stuff companies so often seek to ignore—the S&P 500 is trading at 19 times earnings over the four quarters ended September 30, 2013. Considering that even this high P/E is flattered by extremely high profit margins, it’s very hard to make a case for the market being inexpensive, despite what many bulls assert by extrapolating even more extreme margins.

7. Although real estate investment trusts (REITs) eked out a small gain in 2013, they lagged the S&P 500 by the widest margin since 1998. Additionally, the chart patterns of the largest REITs look to be forming long-term tops. Moreover, they continue to trade at above average cash flow multiples, even relative to an expensive overall stock market.

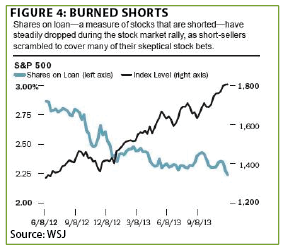

8. Once again demonstrating how the riskiest stocks have soared in the past year, the most heavily-shorted issues greatly outdistanced even a 30% gain in the S&P 500 in 2013. As of November 20, the 10% of the issues with the largest short interest (generally those with the dodgiest fundamentals) had rose 16 percentage points more than the market itself. (See Figure 4)

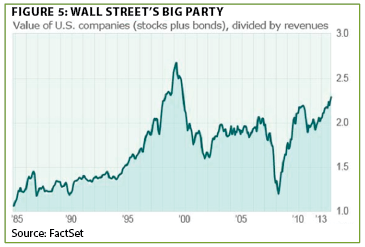

9. There is a tendency for investors to look at just the equity side of the balance sheet. However, it is crucial to also consider the right-hand side of the ledger, where the liabilities reside. In Wall Street lingo, this is known as total enterprise value, i.e., the combination of debt and equity. Looking at this metric for all US publicly traded companies, it again paints a picture of a valuation that is unprecedented with the exception of the frothiest days of the late 1990s. (See Figure 5 below)

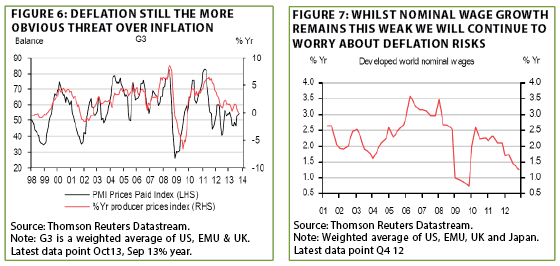

10. Fears continue to linger over a sudden inflation spike, as do suspicions that official CPI measures understate actual cost of living increases. Yet, looking at price and wage trends in the G3 countries (the US, the eurozone, and Japan), both inflation and compensation appear to be eroding. (See Figures 6 and 7)

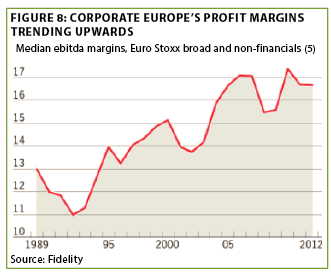

11. Many EVAs have covered the subject of peak US corporate profit margins. Surprisingly, the situation with eurozone companies, despite Europe’s economic sclerosis, doesn’t look that much different. (See Figure 8)

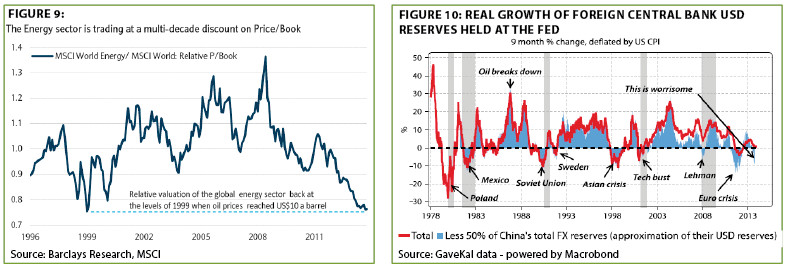

12. Investors wishing to maintain equity exposure, despite an extremely stretched US stock market, might want to consider global energy stocks. This sector is now the cheapest it has been on a relative basis, at least using price-to-book value ratios, since oil hit $10 a barrel in 1999. (See Figure 9 below, left)

13. Crises have consistently occurred when foreign central bank reserves at the Fed turn negative. Currently, this is close to happening, though it should be noted that some of the past "crises" weren’t all that critical, such as the collapse of the USSR and Sweden’s banking crisis. (See Figure 10 above, right)

14. Europe’s banking system continues to look like a ticking time bomb, but its market trades at just 16 times cyclically adjusted earnings versus almost 26 times in the US.

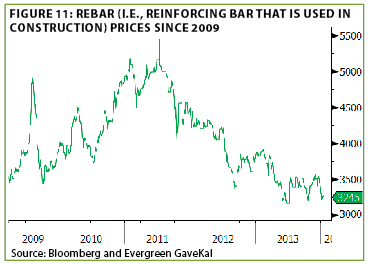

15. Those bullish on China’s growth trajectory point toward the recent bounce in copper prices. Yet, copper demand is increasingly affected by Chinese companies using it as collateral to secure offshore financing due to China’s escalating credit crunch. Rebar prices might offer a better sense of what is occurring in China’s once-booming construction sector and, ominously, they are back to 2009 recession levels. (See Figure 11)

Through a glass darkly. While I’m not sure anyone exactly said anything along the lines of "wise men don’t forecast," it is undoubtedly sound advice, even if it is somewhat impractical when your profession is money management. Of course, flying right in the face of that admonition, for years my team and I have issued our annual predictions, often a humbling exercise, especially when it comes to scoring our prior calls, a process we’ve just completed (for those who missed it, we finished with a 7 out of 11 tally on our 2013 calls). This, and the opening line, begs the question: Why try to anticipate what lies ahead?

It’s a valid question, and I often read that many investment professionals believe it is a fool’s game. But, to answer one query with another, how realistic is that? If you’re simply trying to replicate a market and/or an index, that’s one thing; you can mindlessly put all of the assets in your care to work immediately, and without doing any big-picture or company-level research. But, if your mission in life, at least professionally, is to strive for superior returns adjusted for the risk incurred, you need to have a viewpoint.

Thus, even someone who doesn’t make forecasts (at least overtly), but actively manages money, must make certain assumptions and decisions, such as believing US stocks are more attractively valued than emerging markets, or that bonds offer better risk-adjusted return potential than stocks, or that the energy sector should be over-weighted relative to the S&P 500, or simply that they like Google’s shares better than Facebook’s . In all cases, the asset allocator is making judgment calls based on his or her view of the future. And the reality is, no matter how much research you and your firm do, you are going to be wrong a fair amount of the time.

The nearly infinite amount of variables that move financial markets and economies make it as impossible to bat .1000 when it comes to forecasting as it is in baseball. That’s why we have said for years we shoot for a 60% to 70% "hit" rate with our annual outlook and we have mostly been in that zone with the only significant deviation being on the high side back in 2009—so far. We have little doubt that one of these years we’ll end up with less than half right.

But, with all of those disclaimers and qualifiers out of the way, there are tactics we use to minimize the impact of the inevitable miscues. One of them is to look at what most investors are expecting and then examine the other side of the story. For example, coming into this year, investor sentiment on the stock market was heavily skewed to the bullish view. This, combined with valuations as stretched as a pair of one-size-too-small Lululemon yoga pants, means it will be hard to make much money in US stocks even if good news comes along—not impossible, just difficult.

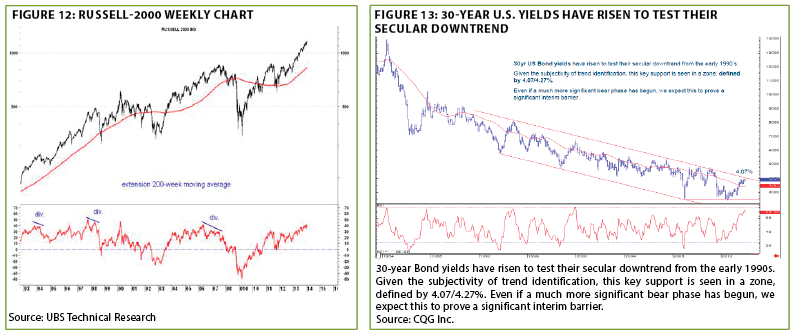

Then, when you have a situation like small cap stocks, per the UBS chart below on the Russell 2000, avoiding a negative outcome, much less making gains to justify the risks, looks as likely as the Seattle Mariners going to the World Series. (Sorry, but it’s been a long time since I took a shot at our once-mighty M’s.) (See Figures 12 and 13)

The reality is that the future is full of surprises none of us can predict. Some will be on the happy side of the ledger, and some on the not-so-joyous side. Yet, the reason Evergreen is congenitally contrarian is because when a negative surprise happens to an investment where there is little hope and lots of angst, losses tend to be manageable. And, theoretically, if there is sound intrinsic value, you can actually buy more at lower prices—that’s allowed, believe it or not. Conversely, when the cup of optimism runneth over, future gains are extremely difficult to attain and disappointments are usually severly punished.

On that note, I thought it might be worthwhile to consider some possible surprises, good and bad, that might be coming our way as 2014 proceeds.

Gomer Pyle lives—surprise, surprise, surprise! First, please realize the following are not forecasts. We stuck our skinny necks out far enough last week and, being a bit worn out from that, we’re going to keep this short and, as you will read, somewhat sweet.

For starters, let’s consider what would be a truly shocking surprise: Our two warring ruling parties decide that constantly threatening mutually assured destruction is unwise. Instead, Congress passes, and the administration signs off on, a series of badly needed, and far overdue, restructuring initiatives. As many of you know, we think this will play out, but, realistically, not until another crisis is bearing down on us. If rationality reigns before the next blowup, that would be very good news indeed and might go a long way to offset the following potential surprise.

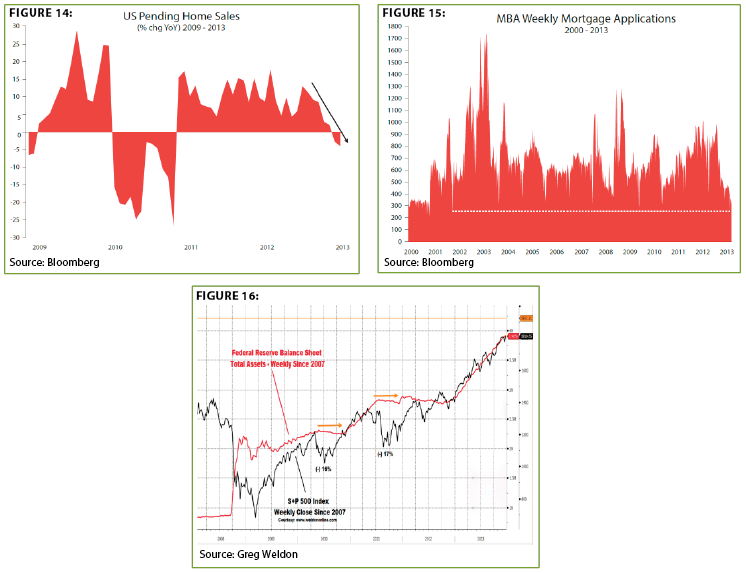

Next up is the possibility that the Fed decides to continue dialing down its pseudough fabrication machine, even if the economy continues to stutter like someone saying Walla Walla 10 times, very quickly. While that seems improbable now, the new voting members of the FOMC, who control monetary policy, might be more willing to admit the various QEs have not helped the real economy. They may shock the markets by letting stocks fend for themselves, while using their various tricks to keep long-term interest rates stable in order to avoid putting further pressure on housing. Although the residential markets remain healthy, there is some fraying around the edges. And, although past EVAs have run charts like Figure 16 below, underscoring the market’s utter reliance on QEs to push it up, it’s not a bad idea to have a refresher. (See Figures 14-16)

Oil prices have been remarkably stable for an extended time frame despite the gusher in US production. The assumption is that a stronger global economy will consume the additional supply. Therefore, a series of related surprises could be that China and other emerging countries, which now represent a tad over 50% of the planet’s GDP, experience an even more severe growth slowdown, causing oil prices to fall precipitously. This could pull other commodities down with it, pushing already tumbling global inflation to veer dangerously close to deflation, rocking the world’s equity markets (due to the ominous implications for earnings this would imply).

The good news is that lower oil prices act like a massive tax cut and should help support, or even accelerate, consumer spending. But there is also the risk, bordering on a true surprise, that the developed world continues what has been a pretty close replay of Japan’s post-bubble, i.e., years of sub-par growth, intermittent deflation, and a sequence of bull and bear stock markets that leaves prices largely unchanged over many years. It’s worth noting that despite last year’s 30% leap by US stocks, the S&P 500 has still returned a mere 4.64% annually since December 31, 1999.

Another looming surprise, which really shouldn’t come as a shock to anyone who has been around financial markets for a while, will be the rediscovery that Wall Street—aka the world’s largest venal colony—exists to make money for itself and its many constituents, not investors. Therefore, those hoping for the leading lights on "The Street" to provide advance warning of impending trouble are almost certain to be disappointed. Bull markets are terrific for business and bonuses; the last thing these folks want to see is this aging toro’s demise. Frankly, the crosswalk signals are already flashing with that cautionary red hand, indicating the traffic flow is going to soon change direction. It’s incredible how many are missing that warning, so don’t be surprised by the panic when the stoplight actually turns red.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.