"Safety’ is a tricky and paradoxical concept. The safe assets are often the ones most people regard as hopelessly risky."

- Jim Grant, acclaimed author of Grant’s Interest Rate Observer

POINTS TO PONDER

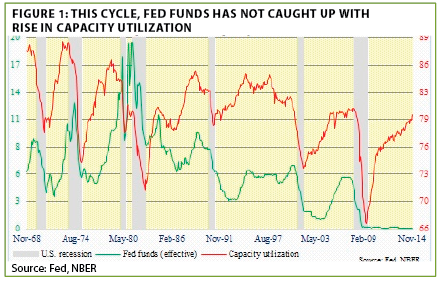

1. The chart shown below, courtesy of the financial blog Hedgopia, vividly illustrates the incongruity between US capacity utilization (essentially tracking how "maxed out" the economy is) and the Fed’s key overnight rate. Despite this presumably unsustainable difference, equity investors seem convinced the Fed’s Big Easy will continue indefinitely. (See Figure 1.)

2. Notwithstanding the relatively elevated level of capacity utilization and the on-going shrinkage in the US unemployment rate, it is sobering to realize that there hasn’t been any full-time job creation over the last 18 years. Similarly, on a global basis, there has been no increase in real wages over the past decade, at least in the so-called "rich countries."

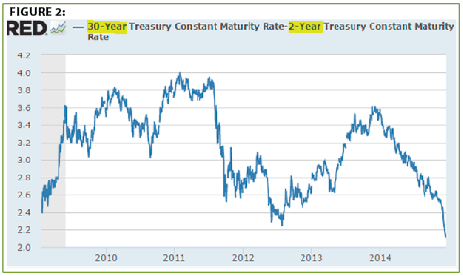

3. Short-term interest rates have been rising of late as bonds, unlike stocks, have begun to anticipate a Fed tightening cycle. But as short-rates have been escalating, longer-rates are declining (at least on treasury debt). This has produced the flattest yield curve since the Great Recession, as can be seen in the chart below tracking the spread, or yield difference, between 30-year and 2-year treasuries. (See Figure 2.)

4. The windshear-like plunge in oil prices represents a $125 billion bonanza for US consumers and, fortunately, for once, particularly benefiting middle- and lower-income households. Yet, Barclays estimates that higher food prices have canceled out 90% of the benefit from crumbling crude. With oil now well below $60, though, the calculus should become more consumer-friendly.

5. The plunge in oil is already producing a supply response. The number of working on-shore rigs has fallen from 1609 to 1540 and given the further erosion in crude, this number seems almost certain to come down much, much further. Globally, the Financial Times is reporting that $1 trillion of fossil fuel development projects are on the verge of cancellation.

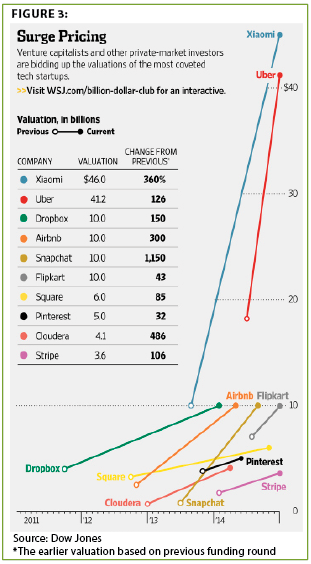

6. There are those who believe that excessive speculation—aka, bubble-type behavior—has not yet become pervasive. Based on the ultra-lofty valuations being placed on a number of the most glamorous tech start-ups, some of which are remarkably "earnings-free," this view seems hard to square with reality. (See Figure 3.)

7. It’s widely recognized that stocks which do well over the trailing twelve months continue to outperform over the next year. What’s less well known is that the best performers over the past three years lag the market on average going forward while the multi-year laggards, as a group, produce market-beating returns. Consequently, investing in those sectors, such as gold miners, that have been massive underachievers since 2011, is likely to be rewarding.

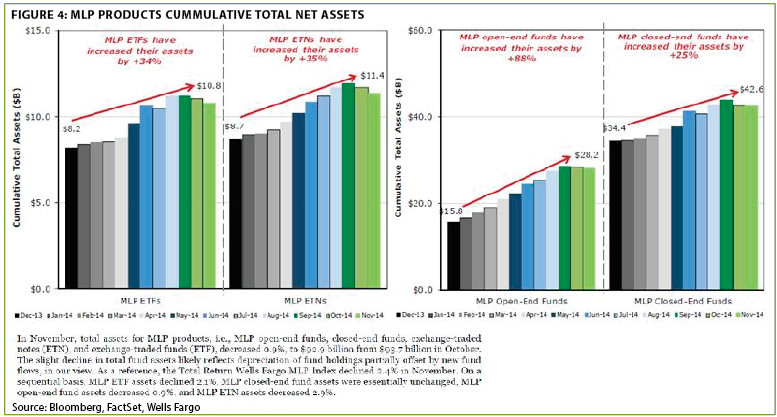

8. MLPs (master limited partnerships) have been crushed lately. Consequently, this asset class is offering extremely attractive distribution yields, in the 6% to 9% range, on issues Evergreen believes should be able to raise their payouts on a consistent basis. Most of these have little to no commodity price exposure. However, a concerning factor is the enormous amount of money that flowed into this space in 2014. (See Figure 4.)

9. Hedge funds have been frequent cannon fodder in numerous prior EVAs. Goldman Sachs just reported a factoid that supports this negative view: Its hedge fund index was down 1% as of late 2014, dramatically trailing the S&P 500 and even the Barclays primary bond index.

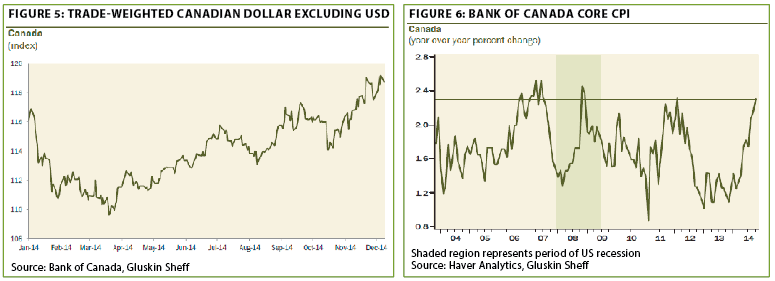

10. The Canadian dollar (CAD) remains reviled among speculative investors who have accumulated a huge short position in the Loonie. This is often a bullish indicator as extreme negative sentiment among traders typically presages sharp rallies. Interestingly, the CAD has been holding up against non-US dollar currencies. Moreover, Canada is one of the few developed countries not grappling with "lowflation" or even deflation. (See Figures 5 and 6.)

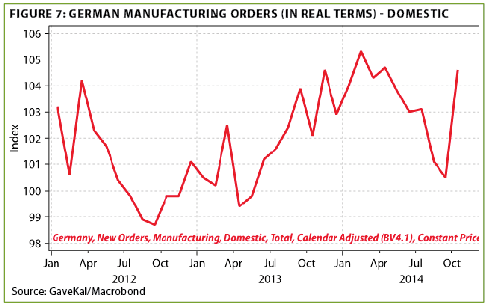

11. Some economic data out of Germany has perked up of late. Nevertheless, the Bundesbank, German’s uber-powerful central bank, has cut its growth forecast in half for 2015. (See Figure 7.)

12. Microchip Technology, one of the leading semi-conductor producers, caused a stir back in October by suggesting that chip demand had suddenly, and broadly, weakened. In December, however, it projected a normal seasonal decline of 2% to 5% for the fourth quarter, significantly allaying fears of a negative inflection point in this key industry.

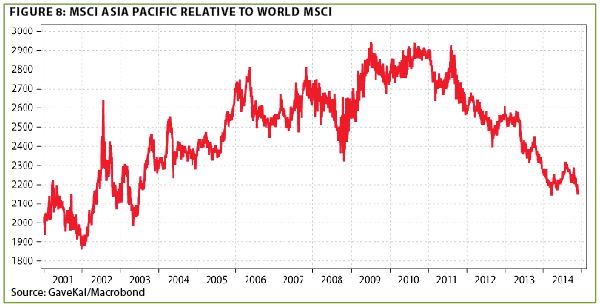

13. Asia is a big beneficiary of lower oil prices. Additionally, Asian stock markets have been lagging the World Index, mostly because of the S&P 500’s exceptional performance, in recent years. Consequently, unlike with US equities, future returns from Asian shares should be satisfactory, possibly even lucrative. (See Figure 8.)

14. No major industrialized country has followed more stimulative monetary and fiscal policies (excluding the recent sales tax hike) than Japan. Yet, it has just entered its fourth recession since 2008. Fortunately, there are signs the economy may be rebounding including corporate bankruptcies at a 23-year low, improving exports, and a better outlook for job growth in early 2015.

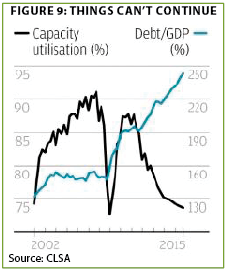

15. In another vivid illustration of the Great Disconnect (which is far from just a US phenomenon), China’s debt-to-GDP remains on the rise even as its capacity utilization continues to plunge back to recession lows. This raises the odds China will export deflation even if it resists the global trend toward currency debasement. (See Figure 9.)

Auld Anxiety? This is the time of the month when we would normally run our EVA Exchange issue, where several Evergreen team members joust over their outlooks. However, given the Holidays, we are deferring that issue until later in January.

Accordingly, I’ve run a longer version of our Points to Ponder, but I realize the danger with sending out this section on its own is that it can come across as a bunch of unconnected data. So, I wanted to provide a little bit of (mis?) interpretation on the implications of some of the foregoing factoids.

First, one of the recurring messages from them is that the threat to world price stability isn’t inflation but deflation. This is true despite the fact that both the US and Canada continue to report core CPI numbers (i.e., excluding food and energy) that are around 2% (or even higher in the case of our neighbor to the north). This no-flation reality is a key reason that government bond yields in the developed world continue to make multi-century lows. Clearly, something isn’t working with the central bank plan of flooding the global financial system with funny money in order to produce higher inflation--other than in a shrinking number of asset classes—and vibrant growth.

This phenomenon is also a prime factor in why Evergreen believes the risks of a worldwide" deflationary bust" are unusually high. If you don’t know what that term means, consider the recent performance of a wide range of commodities, not just oil. Iron ore has also been cut in half. Then there is the metal with a "PhD in economics"—copper—which is melting, as it hits multi-year lows and looks, technically-speaking, as if it is in the process of a major breakdown. Crashing commodity prices and evaporating sovereign bond yields are not the contrails of a rocketing global economy—more like one that is spiraling toward a collision with the meme of imminent "escape velocity".

Moreover, a number of countries are clearly experiencing a deflationary moment of truth. These include Russia, Venezuela, Argentina, and, possibly, most ominous of all, China (the latter in its long over-heated and crucially important property market). However, right up there with China in terms of importance is Europe on-going battle with very low inflation that continues to flirt with turning into a broad-based fall in consumer prices.

But, returning to North America, the economic trends look healthy. While that’s good news for Main Street it might be more challenging for Wall Street. That’s because this positive growth pattern makes the Fed’s ultra-easy policies, which remain the most stimulative in history (at least prior to the last few years), totally inappropriate. Thus, Evergreen is in the camp that Fed rate hikes are headed our way, possibly as soon as this spring. Fed Chairwoman Janet Yellen is even dropping hints she might jack up rates faster than the gentle ¼% bumps that occurred during her predecessor’s tightening cycle (which seems like it happened so long ago dinosaurs were still roaming the planet).

Our anticipation of a more militant Fed assumes, however, that the main engine of feel-good wealth creation—the US stock market—doesn’t fall down and go bust boom. If it does, the Fed is likely to maintain a highly accommodative stance. It’s our belief, though, that one reason the Fed is itching (finally!) to raise rates is to have something other than the printing press at its disposal during the next recession/crisis/panic. If it can get short-term interest rates up to somewhere around 2%—which is our guess at about the max they’ll be able to attain before something snaps somewhere in the financial world—they’ll have loaded some bullets back into their monetary magazine.

Should events break favorably despite the long litany of threats and challenges, Evergreen believes Asian stocks offer a considerably more appealing risk/reward proposition than does the US. Lower oil prices are exceedingly beneficial to Asia given that it is both consumption-heavy and production-lite. Invoking the three-year rule mentioned above, and also per PTP 13, Asian markets have been cabooses since 2011 on the global equity train whose primary locomotive continues to be the S&P 500. For our—and our clients’—money we believe the odds favor Asian stocks out-legging the S&P 500 over the next 3 years.

We are also of the opinion that there are attractive yield opportunities among MLPs and US corporate bonds that are either BBB-rated or just below that level. This is notwithstanding our realization that, should fears of a deflationary bust mount, these returns are almost certainly going higher, which, by definition, means lower prices.

To summarize my summary, as 2015 opens, there are places to put money to work with a realistic expectation of producing respectable returns. Most of them, though, aren’t the ones that have been running for years (the recent shellacking of MLPs has removed much of their froth).

Current conditions are increasingly reminding me of 2007 when the underpinnings of that Fed-enabled up-cycle (during which it turned a blind-eye to the housing bubble) were beginning to buckle. Perhaps the strongest echo is widening credit spreads which is why so many corporate income securities have been under pressure lately. We suspect spreads will stabilize around here, and possibly even recede a bit, at least near-term. But we believe that holding a high level of cash is prudent in case the "risk-off" behavior of so many markets recently is sending an important signal, similar to what happened seven years ago.

It’s stating the obvious—one of my natural gifts—to say that being of an anxious nature hasn’t been very rewarding over the last three years. However, investors who have forgotten the meaning of the term "downside risk" may need to stock up on some Xanax before the strains of auld lang syne are heard again.

(If you would like to hear an interview with yours truly on Real Vision TV regarding these points, please click here.)

With that, Happy New Year to all of our EVA friends!

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.