"It is the long-term investor, he who most promotes the public interest, who will in practice come in for the most criticism. For it is in the essence of his behavior that he should be eccentric, unconventional and rash in the eyes of average opinion."

- JOHN MAYNARD KEYNES

Special message: Although Evergreen expects 2014 to bring more turbulence to the stock market than we’ve experienced in recent years, we believe solid returns are attainable for prudent and contrarian investors. Accordingly, we want to take this opportunity to wish all of our readers a prosperous New Year!

POINTS TO PONDER

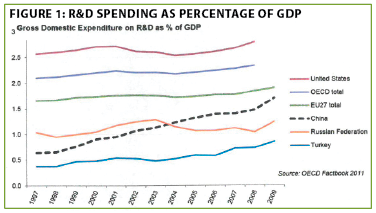

1. Corporate America seems to be more interested in spending on stock buybacks and dividends than the more rigorous, but essential, approach of investing for the future. Despite this, the US continues to be the global leader in research and development expenditures. (See Figure 1)

2. A month ago, expectations for the 2013 holiday shopping season were notably subdued. However, based on UPS’ announcement that its volumes are up 8% versus last year (and also its snafu on Christmas Eve due to a late volume surge), December retail sales might turn out much stronger than anticipated.

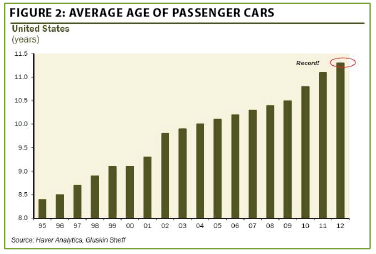

3. Although US car sales have returned to pre-crisis levels, the average age of the auto fleet continues to rise, implying that car makers may not have hit the peak of their cycle. On the less rosy side, it’s fair to note that the situation looked similar in 2007, as the mean age has been steadily climbing over the last 20 years, perhaps due to far superior quality. (See Figure 2)

4. In another indication of a firming labor market, at least for skilled employees, the average factory workweek for manufacturing workers recently rose to 42 hours, a new high since WWII.

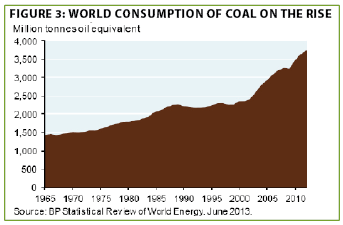

5. It’s common knowledge that coal is the dirtiest form of energy (for example, one-half of man-made mercury emissions come from coal-fired energy plants). Perhaps not as well known is how rapidly coal consumption is growing. (See Figure 3 below)

6. The Fed’s Federal Open Market Committee (FOMC), which implements US monetary policy, may soon have two new independent and strong voices. Mssrs. Fischer and Fisher—Stanley Fischer, former head of the Bank of Israel, and Dick Fisher, president of the Dallas Fed—are likely to vehemently express the perils of creating new asset bubbles based on their past statements and actions, possibly contributing to an accelerated move away from QE (quantitative easing).

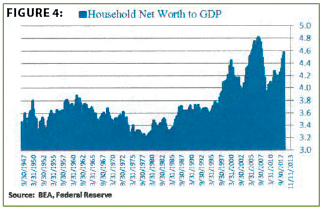

7. Even though US net worth is not as high, in relation to the economy’s size, as it was during the housing mania and long bull market in US stocks back in 2007, it is rapidly approaching the danger zone. Of course, rising asset values can be an indication of economic vitality as long as they are based on healthy fundamentals, and not merely an illusion of affluence. (See Figure 4)

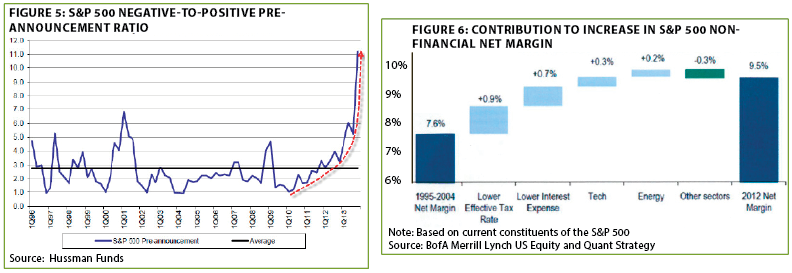

8. The dissonance between a rampaging US stock market and the reality of Corporate America’s deteriorating profit trend is becoming ever more extreme. It’s also important to note that lower taxes and interest rates are the primary reasons why profit margins are at all-time highs. (See Figures 5 and 6)

9. Contrarians should be alert that, based on the latest Barron’s survey, not one leading Wall Street strategist is forecasting a down year for US stocks in 2014. Further indicating extreme bullishness, the new issue (IPO) market has seen the most money raised since 2000.

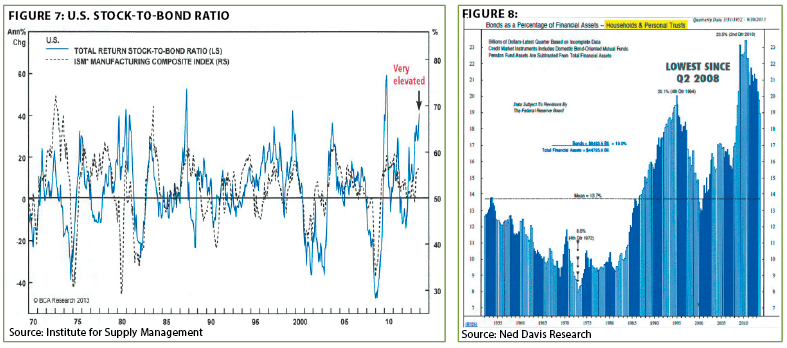

10. As the S&P 500 closed out 2013 up an astounding 32.4%, high-quality bonds were in the red (though, again underscoring voracious risk appetites, junk bonds produced 7% returns overall, with the dodgy CCC-rated segment producing 14% total gains). As a result of the huge lag by upscale bonds, the return difference between stocks and fixed income was at an extreme only seen three other times since 1970. Consequently, bonds as a percentage of personal assets are now the lowest since 2008. (See Figures 7 and 8)

11. Although Europe is supposedly emerging from its latest recession, unemployment just hit a new high. Additionally, Thomson Reuters estimates that the leading listed eurozone companies saw profits drop by 11% in the third quarter, worse than the second quarter’s disappointing 9.5% tumble.

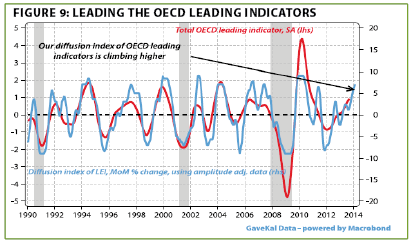

12. Leading indicators may not mean as much as they previously did due to overt central bank manipulation of several key components. But, looking globally, these are definitely on an uptrend. (See Figure 9)

13. China has not experienced a default in its corporate bond market since 1997. However, as part of its necessary but painful interest rate normalization process, multiple defaults seem highly probable in 2014. The excruciatingly elevated cost of current financing was displayed by an AA minus-rated issuer that was forced to pay nearly 10% on a one-year bond.

14. China has long hamstrung its biggest cellular service provider, China Mobile, by precluding it from offering the latest technology, allowing smaller rivals to gain significant market share. Now, though, the wireless giant is rolling out its fourth generation (4G) network and offering the ever-popular Apple iPhone for the first time. Thus, its long dormant stock may begin to stir.

15. Although economic news out of China has been decent of late, the dramatic rise in private sector debt from 128% of GDP in 2008 to almost 200% today raises legitimate concerns of underlying fragility. (See Figure 10)

The bip-ping point. In the peculiar lingo of the investment world, a basis point—1/100 of a percentage point—is known as a "bip." Lately, the ultra-important 10-year Treasury yield has been hovering perilously close to breaking a bip, or even 2 or 3, above the psychologically crucial 3% level. For a sane person, removed from Wall Street’s hyper short-term-focused trading desks, it’s reasonable to wonder how much difference there really is between 3% and, say, 3.10%. A truly rational observer would note that the answer is mathematically obvious. It’s clearly just 10 bips or one-tenth of 1%, and certainly not, superficially anyway, an earth shaking change.

Yet, as noted often in past EVAs, psychology is immensely important to the near-term direction of financial markets and 3%, no matter how silly that might seem to a non-bond trader, has become the red line. Lending this threshold some credibility are reports from experienced Fed watchers that our central bank doesn’t want to see that level meaningfully breached.

Actually, in recent seasonally slack trading there have been some very minor excursions above 3% (the 10-year closed out 2013 at 3.03%), but not enough to set off any alarm bells—particularly given the lack of liquidity over the last two weeks. However, should a decisive penetration occur next week, when the Wizards of Wall Street are back from their holiday idles on the far reaches of Long Island, the seismic monitors will start to blare. Quite obviously, bond investors should consider what might happen next. Yet, I would also assert that those primarily focused on stocks should also pay attention to how bonds behave early in the new year.

For argument’s sake, let’s assume that the Fed is unable to get the 3% level to hold, not an irrational assumption given that its $3 trillion of "large- scale asset purchases" was supposed to reduce interest rates. This clearly hasn’t happened, at least for long-term debt, since the reality is that rates are higher, not lower, than they were when quantitative easings first began to roll off the Fed’s magical money manufacturing machine. And since the 10-year T-note sets the pricing for the mortgage market, as well as long-term corporate financing, this is definitely a critical part of the yield curve. In other words, these rates matter a lot, regardless of how suppressed short-rates remain.

Therefore, please allow me to speculate that rates break above 3% and run quickly to 3.5%. The general assumption seems to be that this should really only be an issue for the bond market and that stocks can shrug it off, particularly if the surge is due to better economic data. On that latter score, it does appear as though the US economy ended 2013 with a somewhat brisker growth profile that may extend into the new year.

Illustrating this relaxed attitude, in the recent Barron’s interview with 10 top Wall Street strategists, alluded to in the Points to Ponder section, the unanimous view was for a higher stock market this year. Yet, they also foresee the T-note yield scooting up to nearly 3.5%. But, as we all know, markets often overshoot, and if the financial media whip up a frenzy about the rout in bonds (after all, frenzies are good for ratings), who is to say that 4% isn’t the next stop? That would be about 100 bips over the line, by the way.

Of course, this would horrify the Fed, which is reportedly already concerned about the 10-year Treasury at 3%. But if the Fed is forced by better economic data, and mounting fears about what is already an extremely effervescent stock market, to continue to taper down, what can it do to stop rates from rising to a point where all sorts of bad things might ensue?

Come on baby, let's do the Twist! Perhaps one of Janet Yellen’s first moves, once she becomes the new Fed head, is to take some advice from that storied economist, Chubby Checkers. She could watch one of his old American Bandstand videos to get inspired, and then tell the world that the Twist is back.

Actually, it was just a couple of years ago that the Fed did "twist" the yield curve by selling short-term securities and buying long-term obligations. As observed in past EVAs, this was the most successful of its efforts to reduce more distant interest rates. The problem is that it ran out of the shorter stuff to peddle, forcing it to resort to QE3, which has seen interest rates rise from 1.75% on the 10-year T note when it started to 3.03% today. In short, mission very much unaccomplished.

Yet, for better or for worse, the Fed has now re-loaded its cache of short-term Treasury debt as part of its latest buying binge. Thus, it now has $750 billion of shorter issues (five years or under) it can sell in order to buy up longer maturities—theoretically, of course. This does pose the problem of making the Fed’s portfolio, now a rather sizable $4 trillion, even more long duration and clearly raises the risk of wiping out the already skinny capital base it uses to carry this gargantuan sum. Yet, the prospect of future losses does not seem to have given the Fed much pause in recent years.

It also has been making noises about "encouraging" major financial institutions into holding more Treasury debt. Under the new regulatory regime, which greatly favors government securities, they may not have to do a lot of arm-twisting; consequently, they can save most of their twisting efforts for the yield curve. Even households are not exactly overexposed to bonds (i.e., credit market instruments) in general, as you can see from the mountain chart below. (See Figure 11)

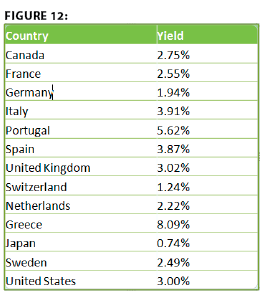

Another source of demand for bonds, particularly if yields spike, as they certainly could, is from overseas. The belief that US Treasury yields are out of synch with other countries, even those not engaged in QEs, is belied by the table below showing government bond rates from other key countries. As you can see, our yields look rather husky in comparison, other than versus chronically shaky southern Europe. (See Figure 12)

In particular, those controlling the purse strings in Japan might find Treasuries irresistible should yields elevate further. Mrs. Watanabe, the mythical retail Japanese investor, can shift from 0.7% on 10 year JGBs, Japan’s equivalent of Treasuries, to 3%, even now, picking up a cool 230 "bips,"

and moving into a stronger currency. Frankly, I’ve been surprised there hasn’t been more of this happening yet, especially since Japanese households are sitting on $10 trillion (US) in cash. This is roughly the same amount American retail investors currently hold, but in an economy one-third the size of ours (i.e., the Japanese are three times as cash heavy, on a comparative basis).

My point is that the Fed might have some allies in its efforts to contain the damage in the bond market should yields move further into the danger zone. There is also another supporting factor that could result from a less than positive development, one that would confound the sunny Wall Street consensus.

A reason to cheer not fear! Before I discuss that last possibility, please allow me to re-remind (my editing team will hate that one!) readers that a year ago Team Evergreen was quite negative on the bond market, as well as admittedly far too cautious on stocks (forecasting a roughly flat year). Even today, with 10-year yields almost double, we are not shouting from the roof tops that this as a stunning buying opportunity. However, the carnage that has been wrought in areas like closed-end municipal and emerging market bond funds definitely has gotten our attention—and investment dollars.

But what has made even the 10-year T-note yield more appetizing is that inflation has been falling synchronously with bond prices, a very unusual occurrence. Because of this, and our inherently slow-growth economy, nominal GDP (essentially, the total revenue stream in the US, prior to any inflation adjustment) is running at its lowest level since the 1930s, at least outside of a full-blown recession. My partner Charles Gave has done extensive studies of the relationship between longer term investment-grade corporate bonds and nominal GDP. He has found that when such bonds return 3% or more above this measure of GDP, recessions almost always occur. Right now, we are 2.5% above but another .5% jump by the 10-year Treasury would mean we’d likely hit that ominous threshold.

Interestingly, the one time that the 3% spread didn’t trigger an economic downturn was in 1987. The reason this intrigues me is that I frankly don’t see a recession in the cards for the US in 2014, even if rates rise another .5%. But a serious contraction in the stock market is a very different story. Recent EVAs have repeatedly made the case that there are pervasive signs of excess speculation these days. Moreover, the bull market will be five years old in March, and bulls which last that long have consistently tended to end with major downward "adjustments."

Again, let’s assume that the 10-year Treasury soars all the way to 4%. First, this would produce a negative return of 4% over the next 12 months for current holders of those securities; not fun, but it wouldn’t exactly be the end of the world, either. This hit would also make T-notes highly competitive with, and perhaps even superior to, the realistic future gains from stocks—and with oodles less risk. Several of the best long-term forecasters of prospective equity returns—such as Jeremy Grantham, John Hussman, and Rob Arnott—have repeatedly noted that stocks are almost certain to generate exceedingly meager future profits due to how high they are currently. Even at current yield levels, I’d rather own a solid income security paying 6%, which is very easy to attain, than speculate that stocks will go from very overvalued to incredibly overvalued.

My key argument here is that a serious upward burst by bond yields could be highly problematic for a pricey stock market. Spiking bond rates were one of the main reasons the stock market fell out of bed in the fall of 1987. And, it may surprise you to learn that the market today is actually materially more expensive than it was just before the crash of that year.

Should stock investors rediscover downside risk, so long suppressed by the Fed’s QEs, they may decide that a reliable 6%, or even a 3.5% to 4% Treasury, is a much safer bet. If so, the vaunted "Great Rotation" of money moving from bonds into stocks might, at least for a time, rotate the other way.

Evergreen has already been making its wagers for the coming year and it will press those bets should income investments become even more tantalizing. For investors with staying power and a long-term perspective, further weakness in yield securities should be something to toast, not roast.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.