"An emerging market is a market you can’t emerge from in an emergency."

-Don Coxe, for many years one of Canada’s leading portfolio managers and strategists.

POINTS TO PONDER

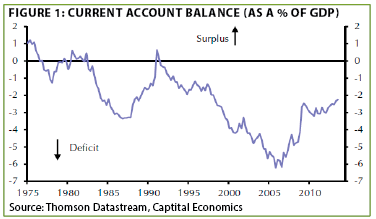

1. The US trade deficit continues to narrow, and this improvement might accelerate given the US energy revival. This does pose problems, however, for the rest of the world given the dollar’s reserve currency status. (See Figure 1)

2. In yet another sign of the prevailing high tolerance for risk and increasingly lax lending standards, sales of US sub-prime auto loans are soaring.

3. Consumer confidence continues to swell, albeit on a jagged upward path. Yet, it remains far below normal and, at a recent reading of 80.7, it is roughly 25 points lower than its pre-global financial crisis level. (See Figure 2)

4. Despite some weaker data lately, the consensus view is that the US economy is set for its best growth year of this lackluster upturn. Illustrating just how anemic the expansion has been, it has taken five and a half years for GDP per capita to surpass the pre-recession level. This is the longest since the 1930s. Moreover, growth has only averaged roughly 2% annually, versus the 6% rate that has characterized bounce backs from prior deep contractions and financial crises.

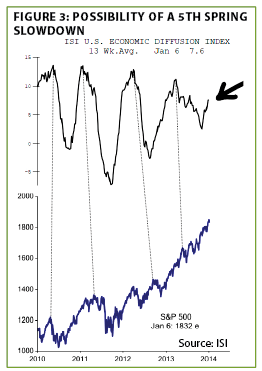

5. Although the pace of US economic activity appeared to be quickening as 2013 faded into the slipstream of time, there remains the risk that we will see the same pattern of a strong fourth quarter into the first quarter, followed by a drop off in the second and third quarters, which has been the case since the Great Recession ended. The good news is that the decelerations seem to be moderating. (See Figure 3)

6. One of the criticisms of the widely followed cyclically-adjusted price/earnings ratio (CAPE) is that it compares against past times of very low market multiples, such as 1910 to 1919 and the 1930s. However, even limiting the "sample set" to just the period since 1979, which is heavily influenced by the absurdly high P/Es of the 1990s (and, to a lesser extent, even the last 13 years), the CAPE is still about 20% above average.

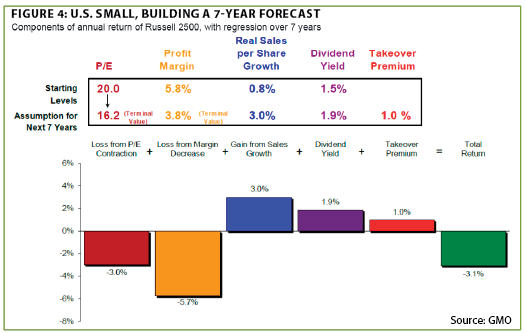

7. The Boston-based money management firm GMO (Grantham, Mayo, Van Otterloo and Co.) has earned a stellar reputation for long-range asset class return forecasts. Accordingly, investors should be aware that it is predicting small-cap stocks will generate losses over the next seven years. (See Figure 4)

8. There is an abiding belief that US households are underweight stocks. However, at 38.7% of total financial assets, equities are not much lower than their 2007 pre-crash level of 40.9% (though this is far below the 53.1% threshold hit in 2000 during the greatest American stock bubble ever). As Barron’s Kopin Tan also points out, large institutions are overweight stocks relative to normal levels.

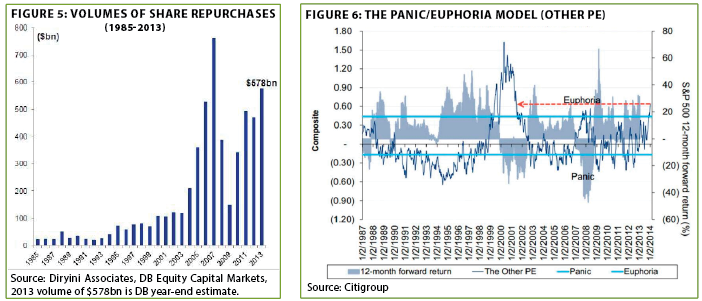

9. The huge sums flowing into share buybacks has definitely been one of the levitating forces behind the US stock market’s 50% sprint over the last two years. Yet, as many have noted, these came at the expense of growth-enhancing investments by corporate America. Additionally, companies have tended, much like retail investors, to buy the most late in an economic up-cycle (when shares are the priciest) and the least at the bottom of both the market and the economy. (See Figure 5 below, left)

10. Citigroup’s proprietary other "P/E" (Panic/Euphoria) is reflecting investor giddiness unseen since the bubbliest days of the late 1990s, even exceeding the level seen in 2007 just prior to the nearly 60% implosion that followed those days of "irrational exuberance." While Citi’s other P/E has generated some strange "panic" readings in the past (particularly in 1995 and 2005), its identification of over-bullish conditions has been prescient. (See Figure 6 above, right)

11. Underscoring the importance of America’s oil and gas production resurgence, the European Union now estimates its energy costs are double those of the US. This obviously confers a huge competitive advantage on the American manufacturing sector, with benefits also spilling over into the much larger service sector.

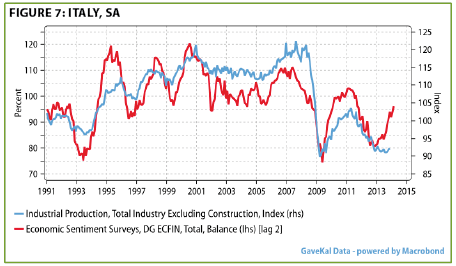

12. The outlook in the eurozone has improved considerably. However, the economic reality in key countries like Italy remains cloudy to the point of dense fog. (See Figure 7)

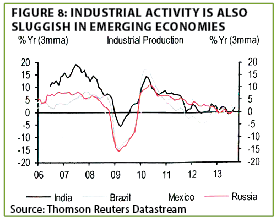

13. The popular view that global economic growth will have an upside breakout is dubious based on sluggish industrial production in the developing world’s trendsetting BRICs (Brazil, Russian, India and China). Further, based on the latest financial turmoil in the emerging markets, it’s even harder to believe these economies are poised to accelerate. Since the developing nations have the fastest intrinsic growth rate on the planet, this is far from a trivial issue. (See Figure 8)

14. The Asian gambling mecca of Macau, once a mere backwater in the gaming world, now generates seven times the annual revenue of Las Vegas.

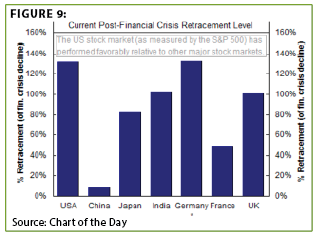

15. Unquestionably, China’s bold new reforms will create dislocations in many areas of its economy. Yet, it has at least started the painful process, unlike in the US. Moreover, the disparity in performance between its stock market and US share prices over the past six years is enormous. (See Figure 9)

For Whom the Bell Bull Tolls? Many have speculated on why the month of January has historically produced the best stock market returns. The tendency for stocks to rise more in the opening month than in the rest of the year was first recognized in 1942, and it has continued in the seven decades since then, obviously with some striking exceptions. Perhaps the most notable, at least for present day investors, is January 2014.

Another aspect of the "January Effect" has been that small stocks out-perform their blue chip brethren. This has caused some head scratching by market mavens trying to rationalize this recurring behavior. Some have speculated that it is due to tax-loss selling in November and December that leads to repurchasing in January. In my simple mind, I would attribute this to the reality that smaller stocks almost always out-perform when the market is rising (and tumble more when it’s falling).

Additionally, since about 1970, it has been observed that the month of January tends to set the tone for the year as a whole. Thus, a buoyant January has typically presaged positive results over the next 11 months, and vice versa, with, once again, numerous exceptions.

The plausible explanation as to why January has historically been such a high return month comes down to, as so many things do, money. More specifically, the flow of money into the market due to year-end bonuses, special dividends, retirement plan contributions, etc.

Consequently, when the market behaves as feebly as it has this January, it raises more than a few eyebrows—not to mention blood pressure readings among the perma-bulls who seem to be as plentiful as the media stories surrounding this Sunday’s Super Bowl. (Not that we’re complaining—Seattleites are always appreciative of any positive attention on our sports teams, which is usually as rare as Denver Bronco fans are in the Emerald City these days.)

The severity of the market decline at the end of last week, with more softness this week, is also raising stress levels among investors, great and small, who have been enthusiastically upping their stock exposure over the last year. Questions are now arising as to whether this is the beginning of the shakeout that many, including this author, have been predicting for what seems like an eternity (actually, eternity seems like too short a timeframe to me).

No doubt many of you would like my opinion in this regard, and I don’t want to disappoint you. Therefore, I will state firmly and unambiguously: Maybe yes, maybe no. Now, before you decide to add this newsletter to your spam filter, let me follow-up by saying it really shouldn’t matter to you. That’s because the odds are very high that the end of the Great Levitation is nigh.

After all, how could it be otherwise?

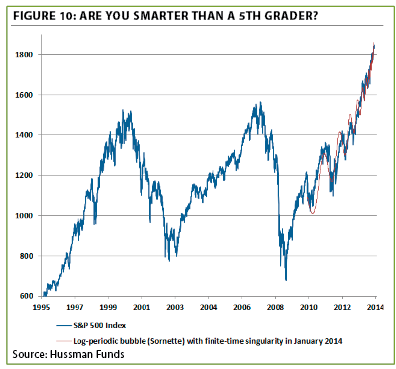

The Morning After. As regular EVA readers are well aware, the almost universal cheering-on of the stock market’s relentless ascension over the last year by the "professional" investment community has both shocked and dismayed me. It’s not that I’m some kind of year-round Scrooge, or that I’m short the market (though I continue to add to my anti-small-cap stock positions). Rather, it’s that I’m mindful of past precedent. And history is as clear as a glacier-fed mountain stream that when you see a chart like Figure 10 below, investors should tune out the "this time is different" crowd and prepare for at least a partial inversion of what we’ve seen over the last couple of years.

Frankly, in my opinion, even a 10-year old could look at this graphic and realize it’s a classic case of too-good-to-be-true. Then again, young children are generally lacking in that wonderful adult quality known as greed.* (See Figure 10)

The words of one of Wall Street’s best and most independent-thinking market technicians, Bob Farrell, are worth heeding based on the chart above: "Parabolic rising markets almost always last longer than you expect, but they don’t correct by going sideways." Thus, the overwhelming majority who are hoping for a mild rise this year are likely to be seriously disappointed.

The trigger for the disconcerting but, thus far, minor retracement in US stocks has been emerging markets. The formidable Charles Gave has been warning for months that when the US trade deficit is contracting, it is like a global monetary tightening. This is because, as alluded to in Point to Ponder 1, the dollar is the world’s reserve currency, and when America is "exporting" fewer greenbacks, it creates a very uncomfortable situation for developing countries with large trade deficits. His tocsins have now been justified based on the havoc wreaked on nations such as Brazil, Turkey, and Argentina so far this year (a shakeout that began last summer).

*For market wonks, the red-line traces what is known as finite-time singularity of log-periodic bubbles based on the ground-breaking work of acclaimed mathematician Didier Sornette and his analysis of the terminal phases of speculative blow-offs.

In August of 1998, toward the tail end of the most dizzying stock market bubble in American history, a financial crisis that started in little Thailand, and quickly spread throughout Asia, caused the S&P 500 to fall nearly 20% and the NASDAQ to plunge almost 30% in a matter of weeks. Accordingly, even in the midst of a mega-bull market, emerging nations and their travails can cause quite a stir, including from the biggest of them all, one that is look increasingly shaky these days.

Air quality studies have shown that the US is being impacted by the prevailing breezes blowing pollution across the Pacific from China. But there’s another ill wind emanating from the Middle Kingdom lately: An old-fashioned credit crisis. Lax lending has been a hallmark of the Chinese economic miracle, particularly in the wake of the Great Global Recession, which China helped end with an unparalleled borrowing binge. As predicted in many past EVAs, the wages of those sins are now seeking absolution. Yet, the Chinese government doesn’t appear to be in a forgiving mood; rather, it seems willing to let some serious penance take place.

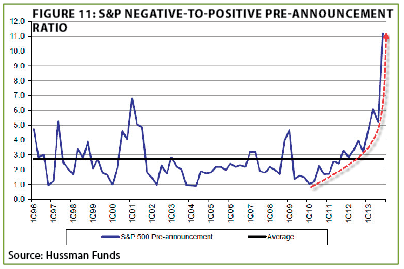

It wouldn’t be fair, though, to pin all of the recent market turbulence, mild as it has been for US equities, on the developing world. The Fed cut its money fabrication by $10 billion for the second time in two months this week, implying they are on a steady path to fully eliminate their multi-trillion dollar injections, possibly by late summer. Consequently, stock investors are being forced to come to terms with a market left to fend for itself. Considering a less-than-idyllic overall news backdrop, including a surge in earnings warnings, it’s no wonder that there is a bit of uncertainty creeping into the minds of those convinced that 2014 would be the sixth up year in a row for stocks. (See Figure 11)

Okay, to end this week’s EVA, let’s try to satisfy those readers who want more than a cop-out as to whether this is the finale of this incredible rally: We don’ think so. Our team believes that this is more likely a prelude of what lies ahead when the succor of the Fed’s mother’s milk runs dry. But, if you haven’t already racheted back your risk exposure, it’s dangerous in the extreme to wait until the last minute to do so.

To paraphrase my favorite senior Federal Reserve official, Dick Fisher, the market will soon have to go cold turkey after years of being saturated by the Wild Turkey the Fed has been liberally pouring. It’s been quite a binge, folks, so brace yourselves for the hangover. It’s likely to be even worse than what many Seahawk fans might be nursing come Monday morning, hopefully due to that infraction known as "excessive celebration."

Special message: Long-time EVA readers know that Seattle sports teams, and their chronic haplessness and misfortune (often at the hands of seemingly hostile referees), have been recurring comic fodder for me over the nearly 10 years this letter has been in existence. However, should the Seahawks prevail on Sunday, as they certainly should (my prediction is that Percy Harvin, our star-crossed star receiver, catches the winning touchdown pass), I hereby promise that I will not deride any Seattle sports team in these pages for a full year. It won’t be easy, but, believe me, I won’t mind a bit.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.