"People can foresee the future only when it coincides with their own wishes, and the most grossly obvious facts can be ignored when they are unwelcome."

- George Orwell

POINTS TO PONDER

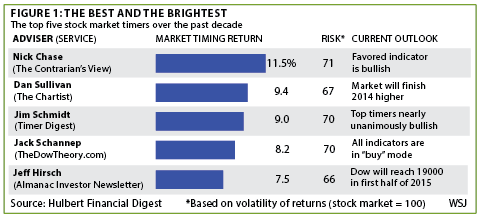

1. Although Evergreen remains convinced that the riskier parts of the US stock market are exceedingly overvalued, the Wall Street Journal’s Mark Hulbert points out that the market-timing newsletters with the best long-term track records are uniformly bullish. (See Figure 1)

2. US GDP growth has been nothing to write (or even text) home about over the last two years, yet corporate America has done even worse. The S&P 500 has produced a mere 1.7% sales growth on average over the past 24 months, versus 3.45% for the overall economy.

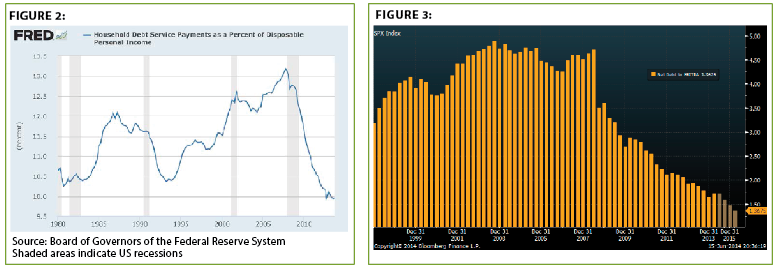

3. Despite the fact that a modest amount of the debt mountain that America has built up over the last 30 years has been reduced—contrary to pervasive assertions of a "Great Deleveraging"—US households are in excellent shape when it comes to debt versus income. This is primarily due to, unsurprisingly, the disappearance of interest rates. Corporate net debt to cash flow is also very healthy. (See Figures 2 and 3)

4. Fears are beginning to rise that the Fed is letting the inflation cat out of the bag, potentially requiring it to tighten soon and forcefully. Per Deutsche Bank, the rate rise necessary to offset the stimulative impact of its $4 trillion balance sheet (versus $800 billion pre-crisis) would push the Fed’s target rate to 6%. It goes without saying that financial markets would be seriously rattled if rates soar anywhere near that level.

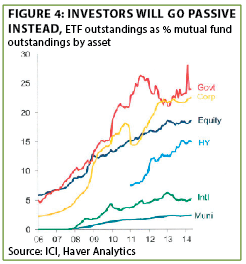

5. A recent EVA theme has been the ETFization of the US financial system. As the following chart illustrates, the market share of Exchange Traded Funds (ETFs) relative to total mutual fund assets has risen radically over the last eight years. (See Figure 4)

6. Most news about America’s energy status has been overwhelmingly positive in recent years. A downbeat exception to that was the Energy Information Administration’s (EIA) recent 96% reduction in California’s estimated oil reserves. This is largely a result of the inability to extract known resources with current technology. Based on the resourcefulness of the US energy sector, that may well change in the not too distant future, barring new production restrictions.

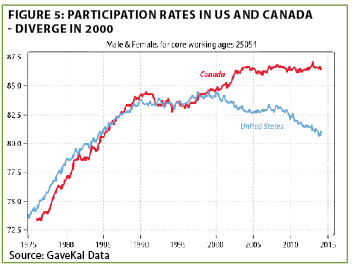

7. The Canadian dollar was left for dead a few months ago with negative sentiment at extreme levels. Since then the Loonie has been on a roll. While it looks over-bought near-term, Canada’s balanced budget, AAA credit rating, and refusal to engage in quantitative easing imply its currency has further upside over time. Additionally, Canada’s core working age participation rate is much higher than in the US, strongly suggesting faster future economic expansion than in America. (See Figure 5)

8. In a recent essay, Bloomberg economic analyst Maxime Sbaihi brought up the crucial point that investors buying Spanish debt need to factor in the distinct possibility of a default and restructuring. Despite this very real risk, Spain’s 10-year government debt continues to yield less than 3%.

9. Simon Hunt is one of the economic forecasting community’s best connected China watchers. In a recent essay, he stated that China’s overall capacity utilization has plunged to just 60%. This implies that Chinese exporters will continue to flood global markets with cheap goods.

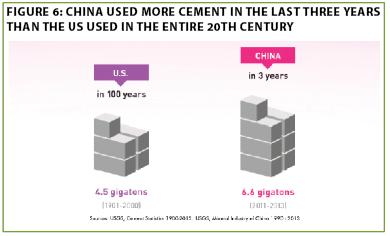

10. Words and statistics don’t begin to fully express the magnitude of China’s fixed asset splurge since the global financial crisis. However, the graphic below, courtesy of Grant Williams, tells the story in most dramatic terms. (See Figure 6)

THE EVERGREEN EXCHANGE

By Jeff Eulberg, David Hay, and Tyler Hay

The Financial Revolution. From 1760 to 1840, the US economy went through an industrial revolution, as companies invested in new machinery and technologies in an effort to lower total costs and grow future earnings. The investments of this era, made with future growth and productivity gains in mind, set the foundation for the US to gradually become the largest economy in the world. Today, we are in the midst of a new economic revolution.

Due to current Federal Reserve policy, companies have access to ample liquidity at historically very low interest rates. Obviously, these funds could be used to fuel future generations of growth. However, unlike the Industrial Revolution, firms today are not investing for the future. Instead, we are experiencing a financial revolution of sorts. Firms are borrowing funds and returning money to shareholders in the form of share buybacks and increasing dividend payouts. In fact, as noted by the Wall Street Journal’s Ahead of the Tape, "The first quarter of this year marked the peak of share buybacks since 2005. Had it not been for share buybacks, S&P earnings wouldn’t have grown at all last quarter." Returning money to shareholders is important, as long as companies are not sacrificing future growth in order to do so.

In spite of the $150 billion sitting on Apple’s balance sheet in April of this year, the company decided to raise $12 billion through a US debt offering in order to fund an increased dividend payment and share buyback program. Why would a company need to borrow with so much cash sitting idly by? As EVA readers are well aware, this was done because a large majority of Apple’s cash was earned in countries outside of the US and has never been repatriated back in an effort to avoid US taxation. Along with the globe’s highest corporate tax rate at 35%, the US is the only country in the G7 to impose a worldwide tax structure. Other countries impose a territorial tax structure, taxing only funds earned in the home country. This onerous US tax structure is leading to the most alarming trend of this financial revolution: US companies are fleeing the US through "inversion" transactions in order to become more profitable through a lower tax expense in other countries.

US corporations are currently estimated to have over $2 trillion dollars sitting overseas in foreign subsidiaries avoiding US taxation. An inversion transaction takes place when a US company purchases, or combines assets, with an international firm located in a country with a more generous corporate tax structure. A common misconception is that these transactions then give the newly formed company access to the cash of the acquiring company’s foreign subsidiaries. This is not the case due to claw back laws available to the IRS. However, it does give the new firm access to the cash on hand of the acquired international company and will shield from US taxation any future revenue earned from non-US subsidiaries established post-inversion.

Recently, Minnesota-based medical device company, Medtronic, announced the acquisition of Covidien, a medical device company domiciled in Ireland. Interestingly enough, Covidien happens to run everything out of Boston, and it is only an Irish-based company because they previously made an inversion transaction after being spun out from Tyco in 2009! Ireland currently has a 12.5% corporate tax rate and does not tax firms to repatriate funds earned in other countries.

In an effort to remain out of political crosshairs, most executives who attempt inversion transactions claim that these deals are done for purely strategic reasons. When asked, Medtronic’s executives wouldn’t even comment on questions concerning the tax advantages of such a move. Although, in spite of their disavowals, Medtronic has maintained the right to withdraw the offer for Covidien should US tax laws change requiring the newly formed entity to become a US corporation. And, furthermore, as an olive branch to the US, the newly merged firm has promised to invest $10 billion dollars over the next 10 years in the US.

There is an ongoing effort in Congress to stop this element of the financial revolution. The former head of the FDIC, Sheila Blair, recently wrote an article for Fortune Magazine and thinks that Congress may have identified the right issue, but they’re presenting the wrong solution. Simply put, an inversion transaction is legal as long as the international company’s shareholders own 20% of the combined firm. In 2004, congressional leaders attempted to stop the practice of inversion acquisitions, but the bill that passed in Congress had many loopholes and, like good tax lawyers do, companies started to take advantage of its provisions. Senator Carl Levin, a Democrat from Michigan, is attempting to present new regulations; his main proposal is to increase the percentage ownership requirement from 20% to 50%, making many of the most recent transactions nearly impossible to consummate.

If seeing large and strategically important companies like Medtronic and Pfizer attempt to leave the US for a better tax environment isn’t a signal that something is wrong with our current tax code, it’s hard for me to fathom what would actually get Washington discussing a real solution. Former Medtronic CEO and current Harvard professor Bill George recently stated, "Our tax rates are out of line with the rest of the world, so companies are leaving." Regulation will not change this pattern; firms will continue to hire the best accountants and tax lawyers in an effort to pay a globally competitive tax rate, even if this means leaving the US. These are multinational corporations, and the executives that run them have a fiduciary responsibility to do what’s best for all stakeholders.

In the last 10 years, 44 US companies have executed inversion transactions. The US has always been seen as the land of opportunity, but if we don’t rework our tax code so that it’s competitive on a global basis, we will continue to see fewer firms established here, and more of our great companies leaving for greener pastures. The financial revolution does nothing but harm America’s working class, the only benefactors being the wealthiest shareholders, Wall Street investment bankers, accountants, and lawyers. As Sheila Blair noted, "Today, fewer Americans have jobs, and the median income for those that do is 4.4% lower than when the recession ended." Increasing regulation or raising taxes on the wealthy will not change this phenomenon. Through tax reform, we need to incentivize firms to invest in the US and grow our industries for the future, much like we did during the Industrial Revolution.*

*Disclosure: The specific securities identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. Apple, Medtronic and Pfizer are used as examples to illustrate tax policies in the US. Evergreen GaveKal currently holds Apple, Medtronic and Pfizer and purchases it for client accounts, if Evergreen GaveKal believes that it is a suitable investment for the clients considering various factors, including investment objective and risk tolerance.

Why high P/Es equal low yields. There are few fields of human endeavor that are as acronym-happy as the investment business. One of the most fundamental and prevalent of those is the famous P/E, or Price/Earnings, ratio. Those who might be considered professional investors automatically assume that our clients know what this stands for. In most cases, this is true, but I wonder how well they understand what it actually means.

Recently, I came across an unusual essay making the sensible case that clients would fathom P/Es better—and, particularly, grasp their importance—if they were inverted and expressed as a yield. Please don’t panic at that last algebraic-sounding phrase! It’s actually very simple. Let’s say that a company’s stock is selling for $50, and it is earning $2.50 per share. Thus, the P/E ratio is 50 divided by $2.50 or 20.

Now, let’s invert that and divide $2.50 by $50. This creates what’s known as an earnings yield, which in this case is 5%. The reason for doing this inversion (as opposed to the type Jeff discussed in his piece) is to make stock valuations more similar to the way investors value bonds, CDs, and, even, income producing real estate. These days, in the era of the Fed’s war on savers, a 5% yield isn’t too shabby, at least superficially.

However, there is another aspect, which all investors should take into consideration when they reach for yield—that four-letter word known as risk. As we should all know, stocks are inherently risky. The extreme swings in market prices we’ve seen over the last quarter-century (and indeed since US shares were first traded under a Buttonwood tree over two centuries ago) should have made that very clear.

Yet, it’s reasonable to wonder why. As long-time EVA readers are aware, I would emphatically assert human emotions play a huge role in this volatility. However, there is also the economic reality that stocks are a very long-term claim on the profits they generate. The price an investor pays today is an opinion of what earnings will be not just this year but many years into the future (and, of course, discounted back to present value, which is why prevailing interest rates matter).

We’ve seen this play out countless times over the years. A company gets on a roll, makes huge profits for a year or two, and then flames out. Even entire sectors can hit the wall. For example, in the distant past, airlines were considered to be growth stocks and traded at high P/Es. This was obviously well before almost all of them went bankrupt, in many cases more than once!

Another major consideration when it comes to P/Es for the overall market is that profits for corporate America are highly variable. Additionally, as conveyed numerous times in past EVAs, they have become even more volatile over the last fifteen years. Consequently, it is essential to adjust profits down to normal when they are very high (as they are today) or up to average when they are very low (as they were in 2009). This helps create a realistic earnings yield for the market as a whole.

Going through that exercise today, with stocks having been in full-blown rally mode for over five years, is interesting. Admittedly, this isn’t an exact science, but as John Maynard Keynes once wisely noted: "It is better to be roughly right than precisely wrong." Lowering current way-over-the-top profit margins by around 25%, leaving them still well above their long-term average, means the S&P 500 is trading at about 20 times roughly normalized earnings. In other words, pretty much in line with that 5% earnings yield on the hypothetical stock discussed earlier.

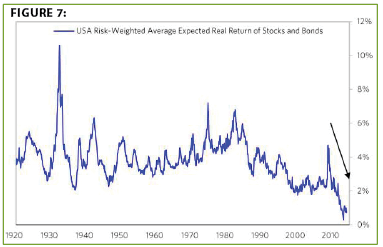

Based on a historically low 5% earnings yield on stocks, combined with miniscule interest rates on bonds, a balanced investor is realistically looking at extremely muted future returns. You may recall this chart from one of the most successful hedge funds of all-time, Bridgewater, that we ran last month, vividly illustrating this reality.

Given this situation, one would think that investors would be increasingly defensive, preparing for the next market decline which would re-set future returns higher—at least for those who build up cash now for future opportunities. But that’s not what’s happening. As is so often the case, investors are consistently moving into riskier assets at higher and higher prices and, similarly, lower and lower yields.

When we talked with many, if not most, clients back in 2011 and early 2012, and explained that our goal was to generate decent returns as the Fed printing press ran wild, while still being protected against the inevitable reckoning, we heard universal assent. But as time has passed, and the stock market has moved relentlessly higher, we’ve received a fair amount of "constructive criticism" of our less than all-in approach.

In the past, when we have been criticized for being too conservative, those complaints have continued to be valid in the short-run, but very misplaced in the long-run. With virtually all yields—from earnings and interest rates—at such depressed levels, we think our tortoise-like style is close to another vindication moment.

To close my section of this Evergreen Exchange EVA (or EEE—hey, there’s another acronym!), I’d like to relay an analogy with apologies to those who have heard it from me previously. What the Fed has done to the financial markets today seems extremely similar to what another government agency has done to western forest lands. The US Forest Service, in its wisdom, has worked vigilantly to prevent small fires. This sounds logical but, much like the Fed’s monetary policies, which have magically eliminated all market brushfires, the problem is that when a major conflagration gets rolling, it is much more intense and difficult to control (as we are witnessing in our state right now!) And that’s another reason why Evergreen is on high alert for a financial fire of the 5-alarm variety.

![]()

Beware of sheer yoga pants AND sheer price drops! Earlier this week, I was 1200 feet above the Pacific Ocean in Big Sur, California, a mecca for any hippie or yoga enthusiast. (My wife is the latter, and I’m neither, but it’s her birthday and, like a good husband, here we are.) As anyone who’s been to this part of the coast can attest, it is truly breathtaking. I realize now that a photo (see beautiful shot to the right) would be much better than any scenery description I attempt. (Note to self: Going forward, when I write my piece from anywhere remotely interesting, always include a picture!)

As my wife practiced one of the six schools of Hindu philosophy also known as Yoga, I sat perched above the water and wondered if our readers understand what goes into our consideration of stocks. I joked last month that some clients probably think we just toss darts at a board. In all seriousness, it’s quite the opposite, and while the frustrating ebbs and flows markets make it difficult at times to achieve out-performance, we think there are powerful reasons for continuing to pick stocks.

In that regard, let me offer up a couple brief comments on what’s quickly becoming the lost art of individual stock analysis. First of all, stock picking is hard, and even the best go out of favor. Second, luck does play a role, especially in the short-run, but the common denominator among those who succeed over time is staying consistent in your process even--actually, especially--when it’s not in style. Lastly, with the emergence of ETFs we have entered a world where fewer and fewer firms are willing to take the time and energy to perform company-specific analysis. This creates significant opportunity for those willing to roll up their sleeves and do the research. What follows is a peek behind the scenes of our investment team’s due diligence of a company very near and dear to my wife’s heart—not to mention her body!

The company I’m alluding to is Lululemon. For those unfamiliar with it, they are a publicly-traded Canadian-based apparel company that makes "technical athletic apparel for yoga, running, dancing, and most other sweaty pursuits." The company has catered mainly toward active, health-conscious females. The racy brand has evolved and now offers a recently launched children’s line, Ivivva, as well as some products for men.

Lululemon’s stock went public in July of 2007, with a market cap of $2.6 billion. Staggering earnings growth, coupled with eye-popping margins, made the stock a darling. In 2013 the company’s market cap peaked at over $12 billion, up almost 600% (known as a six bagger in the world of stock picking). But, as is normally the case with high-flying growth stocks, Lululemon hit some turbulence. Over the past year, sales have slowed and the stock has experienced a massive decline in share price. Despite a rising market, the stock has fallen nearly 50% from its 2013 peak. Expectations became so lofty for LULU, that when disappointment finally struck, investors ran in mass for the exit, and the stock got annihilated, which is when, as usual, our team became intrigued.

We were familiar with the company, because many of us either own the clothing or have seen the litany of charges on our wives’ credit card bills, but we needed to further investigate before we considered the stock for our clients’ portfolios. This research begins with Wall Street research reports, any news articles we could find, and company filings. We also connected with one of the leading portfolio managers in the retail industry for his input (thanks to our partners at GaveKal’s incredible Rolodex). All of the above allowed us to compile a collection of arguments on opposing sides of the spectrum. From there, we created a worst-case and best-case framework and debated their likelihood.

After thorough reading and countless hours of discussion, the majority of the investment team deemed the stock attractive. In our opinion, Lululemon’s strong brand, untapped product pipeline, and limited international penetration overwhelmed its recent

growth disappointments. However, in spite of our positive long-term outlook, at this time, we concluded it wasn’t a buy for our client’s portfolios.

Even I admit this seems counter-intuitive and confusing, but we trust in our process. We have a risk-control discipline in place that steers us away from companies that have displayed extreme price weakness, specifically selling or avoiding companies making new three-year lows (i.e., breaking three-year support in the jargon of technicians) as LULU recently has done. While this can occasionally lead to us missing depressed stocks on the verge of sizeable rebounds, it also helps us avoid those headed to zero. Presently, we believe our due diligence has prepared us to buy Lululemon if and/or when the price action stops displaying these distress signals.

Having certain disciplines and risk controls can help you avoid catching the proverbial "falling knife" of cheap stocks that are on the verge of becoming much cheaper. While sometimes inconvenient, we’ve found that these parameters help limit nasty cuts into your portfolio returns. Now, if our rules-based approach keeps us from buying my wife’s favorite stock, and it goes straight up from here, catching a falling knife might prove to be less painful than trying to explain to her why we passed on it!**

**Disclosure: Lululemon is not currently, and has never been, a holding of Evergreen’s. It is used in this example to illustrate part of Evergreen’s investment process.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.