"If the only reason you find for doing something is because others are doing it then that’s not good enough."

- Warren Buffett

Rebels with a cause. Fortunately for our sanity and overall life enjoyment, we’ve all met a few people over the course of our lives who are truly kindred spirits. In my case, one of those individuals is my partner Charles Gave. In addition to a shared fondness for history, skiing, and tennis, (Charles is too smart to be a sucker for golf like I am), he also has, even at 70, an insatiable curiosity for how the economy and financial markets work, or, as is often the case today, don’t work.

Beyond that, I’m often struck by how often we independently arrive at the same conclusions about economics and market trends. A case in point was a recent essay he wrote called "Indexation=Parasitism." Some of you may have already seen this in our Daily from last week. Despite the overlap, I felt this topic was so important it merited a full-length EVA devoted to its main message.

It would be rather brazen for me to wonder if Charles’ essay was a result of him reading some of my recent writings on the "ETFization" of the financial world. However, I don’t think he peruses my work nearly as closely as I do his. Consequently, I’m quite sure he came to his conclusions free of influence from my thought process. And, in my mind, this makes it much more compelling.

Now, let me take you back several years ago to a time when EVA readers numbered in the hundreds, not thousands. My wife and I were on our annual "date vacation" to Hawaii. While reading a book over in paradise, Justin Fox’s excellent The Myth of the Rational Market, I had an epiphany totally in synch with Charles’ essay from last week. As the handful of you who were EVA readers back then may dimly recall, I wrote about the dangers of what happens when a benchmark becomes an investment strategy.

One of my main points at the time was that when Vanguard’s Jack Bogle first concocted the idea of index investing in the early 1970s, it was a novel concept. It remained that way for many years. As a result, there was very little money devoted to simply replicating the S&P 500, the first iteration of indexing. And, in those days, when almost all money was actively managed, the kissing cousins of index investing, Exchange Traded Funds (ETFs), weren’t even a glimmer in the eye of their progenitor, State Street.

Yet, as the years passed, and a growing body of academic research supported the superiority of passive, or index, investing, the scales began to tip decidedly toward "no-think" money management (using that last word very loosely). Ironically, just as indexing became the accepted mantra, a new generation of academics, personified by Robert Shiller (of the eponymous and famous, Shiller P/E) and Daniel Kahneman, came to the fore. They broke ranks with the dominant orthodoxy and challenged the most basic and sacred assumptions of Efficient Market Theory (EMT), the cornerstone premise of passive investing.

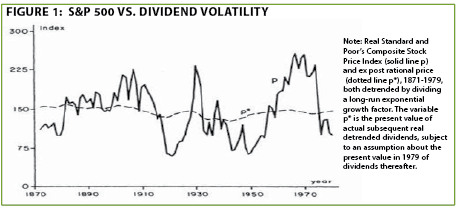

In their view, the relatively mild market volatility prior to the crash of 1987—and well before the incredible bouts of extreme price fluctuations since 2000—were wholly inconsistent with an efficient market. Dr. Shiller’s seminal work on this was an early-1980s treatise showing that stock prices even then were far more variable than the discounted-to-present-value-stream of future dividend income they were supposed to represent.

In very simple terms, his contention was that the price you pay for a stock in the long run should reflect the cash flow it is likely to produce. Because dividend payments have long maintained a steady upward arc (periodically, but temporarily, interrupted by recessions), stock prices should roughly track that path. Instead, as you can see in Figure 1 above, stocks prices swung up and down

far more violently than the dividend trend line, again even prior to more recent extreme volatility. In other words, there was clearly a major inefficiency at work.

One could argue this was because, as indicated above, active management was overwhelmingly the leading investment approach, meaning that emotions might have played a much greater role than if money was simply managed on auto-pilot, mimicking a benchmark.

Yet, the facts of the last quarter-century, as indexing and quasi-indexing have gained so much market sway, tell a radically different story.

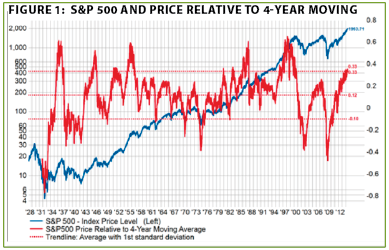

Contrarians—the latest endangered species? In at least one prior EVA, I’ve observed that bubbles and their inverse—crashes—were relatively rare in the first half of my 35-year investment career. From 1979, when I started, to the late-1990s, there was the crash of 1987 and the Japanese bubble and bust. But, other than those events, there weren’t the wild and wooly swings we’ve experienced over the last 15 years. The following chart reveals that since 2000, price fluctuations in the S&P 500 have returned to the extreme ranges of the Great Depression and the immediate post-war years (when another depression was widely anticipated).

Certainly, there are multiple causes for the plethora of mini- and maxi-bubbles we’ve experienced since the late 1990s. Misguided Fed policies would rank high on my list of probable causes, with long stretches of excessively cheap money encouraging multiple episodes of rank speculation, but I think the proliferation of mindless investing is another prime suspect.

On that score, getting back to my Hawaiian "epiphany," if the primary driver of money flows into and out of various asset classes is a desire to closely hew to a benchmark, some very nasty things are likely to occur—and indeed they have. When trillions of dollars now need to match an index, whatever direction it is headed, at various points in time the underlying securities the benchmark represents are likely to be taken way above or below fair value. Said differently, both up-trends and downtrends become magnified by the vast sums of money tracking what was once merely a reference but is now used as an investment strategy.

Market moves have always tended to feed on themselves, but in the bygone days when active managers dominated, a counter-balancing dynamic should have been operative, and often was. In Charles’ words: "If the price of an asset has been going down for the ‘wrong’ reasons, then active managers should buy more of it. Over time this process will help to stabilize the system." Therefore, if prices are crashing and bargains abound, rational money managers will swoop in and scoop them up—unless, of course, they can’t due to forces beyond their control.

First of all, if these managers are merely tracking an index, they have no way to determine if prices are high or low. As proved in the wake of the implosions of the Japanese and US tech bubbles, just because an index is down 50% doesn’t mean it’s cheap. An analysis needs to be performed to determine if a market has gone from absurdly over-valued to simply over-valued. But, since no such appraisal can be performed in the wonderful world of index investing, that type of determination is, by definition, verboten (which in German means "fuh-get-about-it").

Second, an undeniable fact is that when stocks are rising, money flows in and, when they are falling, it flows out. Accordingly, in a severe sell-off, those running index funds are swamped with redemptions. Even if they wanted to buy, they can’t. Instead, they are forced to sell, amplifying the downward spiral. Additionally, they are not allowed to hold more than negligible amounts of cash.

Third, since this dynamic played out on the way up, meaning that index managers were forced to buy as prices rose ever higher during the boom phase, there is much farther to fall on the downside. Basically, the old-fashioned volatility modulator of investment professionals—using high prices to sell and low prices to buy—has actually been inverted! This is one of Charles’ most essential assertions: Indexation is fundamentally a momentum strategy and as it becomes ever more dominant, it turns markets into trend-following vehicles.

Again, quoting Charles: "In the indexation process, there is no attempt at price discovery. The only thing that matters is the relative size of the asset: The bigger the market capitalization, the more an investor should own. This means that if the price of a large asset goes up more than the market as a whole, indexers have to buy even more of it."

A classic example of this was the fact that, in early 2000, nearly half of the S&P 500 had become represented by the two sectors which were at the core of the most bloated of all bubbles: tech and telecom. Conversely, the undervalued areas, such as small-cap and value-stocks in general, were dramatically under-owned.

Perhaps this explains a sad reality…

How good is 4% in the 2000s? Lost in the exuberance over repeated stock market highs is the sobering fact that since the dawn of the new millennium, almost 15 years ago, the S&P 500 has returned just 4% annually. When was the last time you read that factoid? (It will really be humbling for perma-bulls to run this calculation after the next market shellacking.)

It would be reasonable to contend that such a long stretch of below-average returns was not related to the indexation effect but was rather a direct function of the aforementioned tech bubble. Taking that stance, though, would be minimizing the contribution that brain-free investing played in the inflation process of the late 1990s.

Moreover, I would argue that the nearly 80% vaporization by the NASDAQ from 2000 to 2002, almost on par with the S&P 500’s 86% wipeout from 1929 to 1932, was also exacerbated by the indexation phenomenon. How else to explain such a mammoth decline during a relatively mild recession devoid of widespread bank failures, in contrast to the Great Depression when the US banking system virtually collapsed?

As I vividly recall, there was tremendous pressure on value-oriented managers to capitulate and join in the excesses of the tech orgy in the late 1990s. Many formerly venerated contrarian money managers were unceremoniously shown the door. Or they elected to quit on their own terms, putting an end to the constant carping and relentless redemptions from their impatient investors who wanted in on the "easy money" action. Consequently, there were fewer and fewer investment professionals left resisting the mania by selling the crazy stuff and buying the myriad of non-tech companies selling for 10 times earnings or less. It was the first prime-time example of indexation run amok. But it would not be the last…

Triumph of quantity over quality. By 2007, stocks were rocking and rolling again. Memories of the tech wreck had largely become a distant memory. During this bull romp, the excesses weren’t in dot.com issues but rather in housing which, by definition, meant that financial stocks were in the middle of the mania (cheap financing was the industrial gas for the real estate inflation). In fact, the financial sector and housing-related stocks grew to represent approximately one-quarter of the S&P 500’s value. As a result, once again, indexers were heavily exposed to a billowing bubble.

The pain from the housing and sub-prime implosion was so intense that a reasonable person would suspect it would be a very long time until the next speculative mania. But that reasonable person would be totally wrong. Admittedly, today we don’t see the enormous and concentrated bubbles like we had in tech stocks in 1999 and housing in 2006. However, there is a lengthy list of mini-manias currently, with some bordering on the maxi-variety, particularly in small-cap stocks (which, according to Bloomberg, are selling at actual P/E ratios close to 50) and the riskiest realms of the bond market.

As previously observed in EVA, and also highlighted by Charles in his recent essay, European fixed-income markets are a glaring example of the toxicity of blind indexing. For example, since Italy is the third largest sovereign debt market in the world, those running eurozone or world index bond funds need to have huge exposure to Italian debt. In contrast, they are forced to hold a minimal amount of debt from a small but fiscally-sound country like Sweden. Of course, a thinking money manager would not do this but, remember, we are now living in a world where an increasing number of asset "stewards" aren’t supposed to think!

Returning to the equity world, a relatively new breed of investment professionals—consultants (who Charles refers to as "failed money managers")—play a crucial and, I think, cruel role. As Charles observes, consultants, who are most common in the institutional world but also often hinder advise ultra-high net worth clients, have, in his words, "defined risk as a deviation from the

index against which the money manager is benchmarked. This is idiotic. It forces even mean-reversion managers* to become closet indexers." (I should point out there are consultants who realize this danger and do not pressure managers to blindly follow an index.)

Echoing the original theme of my epiphany from years ago, Charles states: "Indexation could work if it remained a satellite strategy with, say, 10% of money being managed through indexation, the rest being (actively) managed. As such, it would be a parasitic strategy. Indexers would benefit from the price discovery work done by others…But a system where everybody wants to be a freeloader cannot work."

If you think this is just the whining of a contrarian during the late stages of a roaring bull market, I assure you it’s not—actually, it’s quite the opposite. The increasing domination of pure and closet-indexing is a golden gift for congenital contrarians like Evergreen. After all, by definition, it creates the extreme price distortions that a rational money manager should be able to exploit for greater profits than if prices stayed within a narrower band. Yet, this is a classic case of "it takes two to tango"—at least to tango profitably.

Clients invested with contrarian firms—in other words, those who strive to profit from market prices reverting back to historical norms—need to realize that times of underperformance during periods of either over-optimism or excessive pessimism will be more frequent and last longer. Therefore, you need to be more patient with your herd-resistant manager these days than in the past. Your reward, assuming your adviser’s strategy is sound, should be higher returns than in a less irrational, momentum-driven world.

Ok, let me return to the "ETFization of the financial system" theme to wrap up this EVA, both to emphasize and clarify some key points.

Don’t shoot the investment vehicle! In my mind, ETFs are just another instrument. Like a gun, they can be used for good or evil. There is nothing inherently bad about them. In fact, they give firms like Evergreen the ability to access niches of the financial firmament that were essentially "uninvestable" before, ETFs are particularly helpful when it comes to profiting from overpriced asset classes (i.e, hedging downside risk for client portfolios which, by definition, in a rising market, reduces upside—there’s no free lunch!).

However, the fact that there are now over 1300 ETFs in existence means that investors have nearly unlimited opportunity to try to follow Jim Cramer’s "there’s always a bull market somewhere" mantra. Consequently, they can continually find some asset class that is on fire and pile into it, with little regard for valuation. The more illiquid the underlying securities, the more an in-vogue ETF goes up when it’s hot, leading to even greater performance-chasing inflows (again, the manager can’t make value decisions, he or she is forced to buy). Ergo, we are seeing countless incidents of the momentum phenomenon Charles describes, and one that we have witnessed blow-up repeatedly over the last 15 years.

Please indulge me as I quote Charles a final time: "Any economic system based on momentum must be extremely unstable, moving relentlessly from boom to bust and back again, which over time will cause a massive waste of capital." You don’t have to be Robert Shiller to realize we’ve wasted trillions of capital in the last decade and a half due to this momentum-driven, performance-addicted paradigm.

Between indexing and ETFs, we have built a financial system that is extremely highly susceptible to the bubble/bust cycle. Additionally, our central bank has gone out of its way to encourage the elevation of numerous investment sectors to dangerous levels in a frantic effort to make investors feel richer, the fervent hope being that they will go out and spend those paper profits.

The multi-trillion dollar question remains: What happens when the momentum goes the other way, as it always does? My strong suspicion is that it will be messy in the extreme, giving those who resisted the Fed’s siren song—to take on greater and greater risks—an extraordinary buying opportunity, one on which the legions of indexers won’t be able to capitalize.

![]()

*In other words, those of a value-orientation.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.