Below are Evergreen Gavekal's Likes/Dislikes for December 24th, 2021.

A Change Comin’ On

Soon it will be a new year and it’s also going to be time for a new EVA look…and name! While the latter is still uncertain at this point, our intent is to radically alter the format of the former Likes/Neutrals/Dislikes section.

You may have noticed that we’ve been recently referring to the Likes, etc, section as “Positioning Recommendations” and the odds are we’ll stick with that heading forward. Our plan is to display each of the three sections in such a way that the basic continuing recommendations are listed horizontally and with much less detail for each one of them. Only our strongest opinions will be shown above the rest of the positioning recommendations. The idea is to focus on those and make this entire section more reader friendly.

Once we begin running it in the new format, feel free to let us know how you feel about the changes. We’ll pay attention to modification suggestions, at least when there are a number along the same lines.

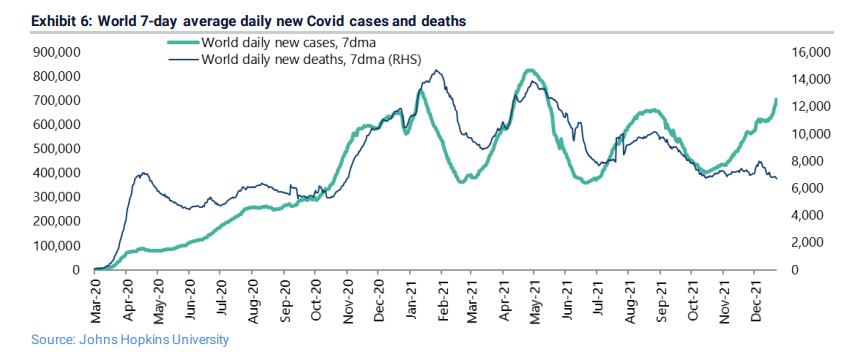

As far as this week’s update, it’s been a bit of a stealth rally this week. The catalyst has been additional news that the extremely transmissible Omicron variant remains benign from a symptom severity standpoint. If you’ve been reading the last few issues of our Positioning Recommendations section, the old Likes/Neutrals/Dislikes, you’re aware that our primary expert source on all things Covid related has been anticipating this outcome. Images such as the below lend credence to that sunny view, despite the considerable disruption this latest variant has caused.

Regardless, most market sectors that are considered to track the economy’s up and downs remain sharply lower, in most cases, from where they traded earlier in the year. Omicron isn’t the only culprit; the Delta variant that went viral in early summer has also been a key depressant. It continues to be this author’s view that Covid news should improve dramatically as 2022 unfolds. Accordingly, I believe the stock market’s best risk/reward opportunities reside within the “virus victim” sectors, with energy remaining my favorite way to play this probable second reopening phase rally. The energy sub-sector of MLPS/Midstream also looks highly attractive in that regard.

As previously noted, tax-loss selling is likely aggravating the weakness in stocks that have been hit by Delta and Omicron lock-down fears. Based on history, this downside pressure should now be largely exhausted.

Certain international markets have also been beaten up because of the one-two punches from Delta and Omicron. Those continue to be appealing destinations for fresh capital and/or funds fleeing the negative after-inflation yields of nearly all bonds, at least of the US variety. Foreign bonds also appear attractive in many cases. For retail investors, ticker symbols TEI and AGOV are worthy of investigation in that regard.

To close this short note, the entire Evergreen team wishes you a happy and, especially these days, healthy Holiday Season!

Positioning Recommendations

(Note: there are very few changes this week.)

LIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.