Below are Evergreen Gavekal's Likes/Dislikes for November 19th, 2021.

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

Arguably, the attention-grabbing market news this week was the sharp correction in the crypto currencies. The bellwether, Bitcoin, has tumbled 14.4% from its recent peak but it is still up a stunning 100% this year. It continues to be my view—as overly cautious as it has been—that there is a severe shakeout coming in crypto-land due to intensifying scrutiny of the “stable coin” Tether which is the main funding medium for Bitcoin purchases. If I’m right, and there is another 50% dive looming for Bitcoin, that could create a solid buying opportunity, at least for the aggressive portion of an investor’s portfolio.

Personally, hard assets with practical applications remain my preferred way to protect purchasing power against what continue to be spectacularly stimulative monetary policies by the Fed. Copper and silver are two examples of this preference due to the increasing demand these commodities are nearly certain to experience. In turn, this is a function of the massive expansion looming from both solar panel production and electric vehicles (EVs) proliferation.

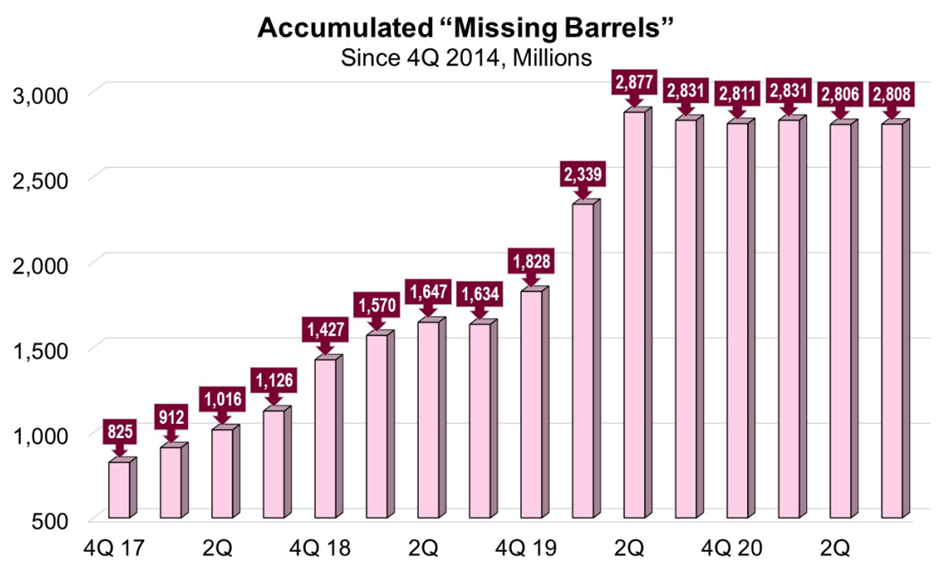

Oil prices are under pressure as a result of the reality of worsening Covid news in Europe. On a less real basis, the International Energy Agency’s forecast of an oil surplus next year has been another source of weakness, as have releases from the US Strategic Petroleum reserves. (Over time, these tend to be more bullish than bearish and this one smacks of desperation on the part of the Biden administration.) The fact of the matter is that the IEA has drastically underestimated oil demand for the last twenty years and, particularly, since 2014. Over the latter timeframe the demand measurement shortfall now amounts to roughly 2.8 billion barrels! Moreover, it is also projecting a highly improbable—based on the spending starvation that has persisted among energy producers for most of the last eight years--production increase of 3 million barrels per day next year.

Accordingly, this pull-back in the energy complex is unsurprising based on how much oil, natural gas and the related equities have risen in price this year. The correction may well have further to go but long-term investors, who believe that persistent shortages are more likely than the IEA’s glut forecast, should use the weakness to engage in dollar-cost-averaging, especially in energy issues that have come down hard.

As far as the stock market goes, there are some warning signs appearing despite the steady cadence of new highs in the S&P and the NASDAQ. There are now almost double the number of stocks making new 52-week lows versus highs. And in a sign of how much froth there is these days, the list of stocks selling at 10 times sales or more is double what it was at the height of the dotcom bubble of the late 1990s. (Thank you, David Rosenberg, for both of these factoids.)

Bonds have been generally stable this week, catching a bid, as traders say, as a consequence of Covid lock-down fears in Europe and a strong dollar. The latter continues to rally but, unusually, so is gold. Bullion has had an upside breakout on a technical basis this week but, typically, the dollar and gold move in opposite directions. Gold mining shares have naturally benefited from the yellow metal’s price revival. I’m sure it comes as no surprise to EVA readers that this author remains highly bullish on the long-term outlook for precious metals which should be even more precious in an era of immense debt monetization and currency debasement by the planet’s leading central banks.

LIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.