Once a month, we publish EVA in the Evergreen Exchange format. This issue should be a particularly unique exchange of ideas, because Tyler Hay, Jeff Eulberg, and David Hay each selected an influential investment mind whose approach they admire. Aside from explaining the motivation for the individual they chose to write about, each author will also recap the current outlook of their choice. Our hope is to provide insight into how these luminaries view financial markets and investing in general.

The following exchange is by Tyler Hay:

The New King. I believe consensus thinking really limits an investor’s return potential. Our industry in particular can lead us down a path of conformity. Most people in the investment world went to the same universities, studied the same principles, read the same newspapers, watch the same TV stations, and follow the same analysts. Despite all of this uniformity, there is a belief that some of us are going to do a better job than their collective peers. It’s reasonable to wonder how someone can rationally expect to produce significantly distinguishing outputs with remarkably similar inputs. Logically, one would need to interpret information differently than the masses to truly standout. This requires intelligence, courage, and conviction. In our business, it can be hard to find one, much less all three, of these attributes. Though rare, there are certain individuals whose perspective on the world is so unique that they can in fact stand above the crowd. They do not accept the status quo and they certainly don’t hesitate to challenge consensus opinions. They speak their minds and they aren’t afraid to make mistakes. When I think of these attributes, I think of Jeffrey Gundlach.

Born to a middle class family in upstate New York, Gundlach was the son of a bowling alley chemist. Being analytical by nature made math an easy subject for him. In high school, he nearly aced the SATs and went onto study at Dartmouth, graduating summa cum laude in math and philosophy. He was admitted to the PH.D. program at Yale, where he studied theoretical mathematics. Originally promised the freedom to compose his doctoral thesis on the "probabilistic implications of the non-existence of infinity," he dropped out when he was told to reconsider topics. Being musically inclined, he left for Los Angeles where he decided to try his hand as drummer in a rock and roll band. Despite being a talented musician, he became more interested in making money after watching an episode of Lifestyles of the Rich and Famous with Robin Leech. The show cited investment banking as the top earning profession. The next day, he sent 25 letters out to firms he found in the yellow pages; only one replied: The Trust Company of the West (TCW).

At TCW, Jeffrey Gundlach became a rising star as a bond manager, not a deal-maker. He brilliantly navigated the financial crisis, generating positive returns in 2008 while many competitors saw significant losses. In 2009, he then pivoted the portfolio out of ultra-safe agency debt into areas of the market that had suffered undue carnage. Despite his nearly clairvoyant abilities and managing over 70% of TCW’s assets, he was passed over for CEO, a seemingly unimaginable decision. The firm went with someone who was well-connected and possessed many of the leadership traits most expect in a CEO.

Viewing Gundlach’s displeasure of this choice as a cancer to the firm, TCW took a gamble and, in December of 2009, fired him. (It should be noted that Gundlach has a reputation as kind of a mad genius. He’s been known to quote from Shakespeare in meetings, launch verbal attacks on ideas he deems unfit, challenge his superiors, dress in loud clothing, and speak in impossibly cryptic monologues.) In a lawsuit, TCW claimed to have found pornography, marijuana, and other paraphernalia while emptying Gundlach’s office. However, the suit was dropped, and it was Gundlach who won a $67 million settlement against his former employer for owed compensation.

Gundlach took with him 45 of his team of 60 employees from TCW. With start-up capital from Oaktree Capital (co-founded by Jeff Eulberg’s subject, Howard Marks), and a few other early investors, he launched Doubleline Capital. Following his Jerry Maguire moment, Gundlach and Doubleline have quickly risen to superstar status within the bond world. On the other hand, his former firm spent almost seven years licking their wounds, and attempting to recoup the lost assets related to his departure. In 2012, Gundlach rented out a restaurant in the lobby of the building where TCW was a tenant. There, Gundlach and his team celebrated the milestone of $50 billion of assets under management and sipped Cristal. The purpose was two- fold: Throw a lavish party for his loyal followers while rubbing salt in the wound of his former employer.

Gundlach’s success shows no signs of slowing down. Fortune has promoted him to a nearly god-like status, dubbing him the "King of Bonds" next to the legendary Bill Gross. In fact, during Gross’ public divorce from Pimco, he reached out to Gundlach about joining forces. Gundlach shrewdly declined, leaving Gross with few options. On short notice, Gross landed at Janus. Gross’ departure to a smaller and less respected firm put Doubleline in a particularly advantageous position to poach assets, which is exactly what’s he done. While he’s controversial to some, Gundlach’s success as an investor is virtually undeniable to those in the investment world.

I began this exchange by talking about the willingness to be different. But, being different has a purpose. It is precisely what allows people to interpret events correctly when many don’t. A model example of this occurred for Gundlach in early 2014 when many where warning that you could not make money on 30-year Treasury bonds yielding 4%. In traditional contrarian form, he took the other side of the bet, stating that if yields fell back to their 2012 levels significant profits were possible. They did exactly that and last year the 30-year Treasury bonds returned almost 30%! I hope by now most readers can see Gundlach has mastered the quality of being different.

Though his stripes were earned as a bond manager, he’s broadened his analysis of financial markets. Recently, he gave his annual outlook in a webcast.

The Federal Reserve (against a hike) — Gundlach believes that the Fed feels compelled to raise interest rates. The Fed is worried that, with rates at zero, if something happens to the economy they will be lacking a lever necessary to help resuscitate it. He does not believe that the economy is strong enough to handle any sustained rate hikes.

The US stock market (bearish) — The market is making record-breaking highs and has been in an unusually long up-trend. Gundlach has admitted that’s he’s been overly cautious with his own assets and has probably given up some return by waiting in cash. The last time markets went up six years in a row it declined 18% (1904). He thinks many traditional warning indicators are signaling correction.

The dollar (bullish) — While Gundlach calls it a crowded trade, he thinks that the long-term fundamentals support a very strong dollar. He cites currency markets price movements as "persistent and long lived."

Employment (bullish) — Gundlach remains extremely concerned that all the job growth has been a result of the energy boom, particularly in North Dakota and Texas. With oil prices slashed by almost half this seems very concerning for employment numbers.

Housing (bearish) — One of Gundlach’s favorite topics to discuss is housing. He thinks millennial’s behavior is a major headwind. Single-family homes face a demographic challenge as this generation is forced to cohabitate and to rent. Increasing student debt burdens will make homes increasingly unaffordable for young buyers.

Energy (wait and see) — Gundlach does not think that many investors are appreciating the risks of lower oil. The potential for contagion to other asset classes is a serious consideration for portfolios, even those without direct exposure to the energy sector.

US Treasury Bonds — Gundlach believes there will be significant capital flows into the US dollar and the 10-year T-note. He expects downward pressure on US yields as they start to converge with European bond yields.

China (bearish equities) — Gundlach thinks China will begin a QE (quantitative easing) program ,and that it’s probably too late in the game to buy equities in that market.

India — The cronyism and the corruption is actually a positive in Gundlach’s view. He believes the notion that any moves toward legitimate capitalism would have very positive implications for investors over the long-term (20 years).

The following exchange is by Jeff Eulberg:

Think different. Next to Warren Buffett, Howard Marks—chairman and founder of Oaktree capital—may be the most frequently quoted investor of the last 20 years. My favorite quote from him perfectly encapsulates a core theme of his investment philosophy: "Skepticism and pessimism aren’t synonymous. Skepticism calls for pessimism when optimism is excessive. But it also calls for optimism when pessimism is excessive." One of the great advantages available to investors today is the immense research produced by brilliant investors. But as an investment manager, one of the equally great disadvantages can be the ever-increasing number of investment "experts" dangerously leading clients down a treacherous path. Due to family commitments and a busy work schedule, I don’t have endless time to read everything published—as much as my wife may think I try to. So, I have to be picky about the research I choose to read. Typically, I seek out authors who have lengthy track records of success, non-consensus opinions, and the ability to stand out from the pack. In my opinion, Howard Marks belongs in the investing Hall of Fame. His firm manages over $90 billion in assets (primarily focused on distressed debt). To boot, he writes some of the greatest newsletters available to investors. While praising Marks in 2011, Warren Buffett commented, "When I see memos from Howard Marks in my mail, they’re the first thing I open and read. I always learn something, and that goes double for his book."

In 2011, Marks outlined the key tenants of his investment philosophy in his book, The Most Important Thing: Uncommon Sense for the Thoughtful Investor. In it, he describes how following "conventional wisdom" and the investing herd can never lead to outperformance. It’s impossible to summarize Marks’ investment philosophy in these two pages, so I’ll focus on this key aspect: Marks is definitely a contrarian investor. In fact, I believe he would say that having a rationally contrarian point of view is the only way to make substantial money for clients. In a 2006 memo titled Dare to be Great, Marks bluntly states, "This just in: You can’t take the same actions as everyone else and expect to outperform." Marks believes that if you want to achieve above-average returns, you must do the following: be willing to invest in unusual market niches, find things others haven’t found or don’t like, avoid "can’t miss" market darlings, and engage in contrarian cycle timing. Or, as an alternative, he suggests concentrating heavily in a small number of things you think will deliver exceptional performance. To me, this is indicative of what the investment team at Evergreen tries to achieve for our clients on a daily basis.

Right Cycle Investing, Evergreen’s trademarked investment philosophy, is designed specifically to avoid "the herd". As Evergreen clients and long-time EVA readers know, we spend an immense amount of time studying fund flows, pinpointing trends that we flag as key signals of a herd mentality. These signals are the backbone of our investment work, but it doesn’t stop there. We also look to valuations as an indicator of investor optimism. When our most important metrics reach above average levels, combined with excessive fund flows, it’s a major warning that investor optimism is starting to boil. At this point, we avoid the herd mentality and look for true long-term investment values—wherever they may be found. It’s counterintuitive, but the best long-term values don’t come from asset classes that everyone loves.

Marks said it best: "Most great investments begin in discomfort."

Earlier this year, Marks updated his famous Dare to be Great memo with the equally brilliant sequel Dare to be Great II. In one of the sequel’s key sections, "Dare to be Wrong", Marks focuses not only on seeking out unloved and unconventional asset classes, but also delves into the question of why so many people follow the herd. Outside of the innate human feelings of euphoria and greed, Marks zeroes in on one of the fundamental conflicts in the investment management business. He asserts that daring to be wrong isn’t worth the professional risk that accompanies the humiliation of looking wrong. Timing is everything, and many great investors have had to wait long stretches before the markets come to their senses. The threat of a salary reduction, losing their job, and, obviously, losing the trust of investors, all lead managers to hop on the benchmark bandwagon. However, while doing what’s best for themselves, they’re not doing what’s best for their clients. If you follow this path, and run with the herd, your clients feel comfortable and happy as markets appreciate and investor optimism grows. And, when the inevitable broad benchmarks go into free-fall, the fact that most of the client’s friends and families are also experiencing the same pain, allows managers to deflect accountability. This creates a sensible business strategy for the investment manager, but also an outcome that is not in the client’s best interest.

Marks is not known for making bold forecasts or flashy proclamations. Instead, he studies probabilities and invests his assets for reasonable risk-adjusted, long-term returns. But, in interviews over the last few years, he has consistently mentioned that he believes it’s appropriate to beef up your portfolio’s defense. He thinks investors have the misguided understanding that higher risks always equal higher returns. As valuations have been stretched, he points out that the intrinsic values of assets haven’t changed. And at some point in the future they will inevitably return to more reasonable levels. Lastly, as what should come as no surprise, after the greater than 50% decline in oil, Marks sees good long-term opportunities in the energy sector.

Like Marks, a rational approach to contrarian investing is what Evergreen strives to achieve. In many of the firm’s most profitable years for clients, we’ve had to dare to look wrong in order to achieve this feat. Leading up to 2008, we were forced to constantly defend our conservative stance. We were called crazy to believe housing would decline in a substantial manner. Then, in the depths of the financial crisis, clients were unhappy to see us taking "safe cash" and buying securities that seemed doomed for failure. Again appearing to look wrong, we’d often see these initial purchases continue to decline, allowing us to steadily, if not joyfully, buy more. In 2011, when the US stock market was on the verge of tipping into a bear market, clients were shocked to see us buying equities and pounding the table to endorse equity-like yield investments in income portfolios. Today, we’re in a fairly familiar position of looking wrong. But, like Marks, for the last few years we’ve weighed the odds and think taking a defensive track in our portfolio makes the most sense. As investor optimism runs rampant, and valuations seem to have no ceiling, we’re again forced to defend our contrarian position. I anxiously look forward to the day when we’ll be defending buying a once again out-of-favor US stock market. When that time comes, we’ll have the cash available to buy at fire sale discounts to intrinsic value. As Howard Marks says, "Everything is cyclical eventually."

The following exchange is by Dave Hay:

Fallen angel. The investment business is brutal, pure and simple. Well, maybe not so pure and, as Buffett likes to say, it’s simple but far from easy. Along these lines, there are few occupations where "What have you done for me lately?" is as prevalent as it is in the profession I chose back when Jimmy Carter was first putting solar panels on the White House.

There may not be a starker example of this short-term memory syndrome in the investment business than my guru of choice for this Evergreen Exchange edition, John Hussman. For many years, John was the toast of the mutual fund industry. From the Strategic Growth Fund’s inception in July of 2000, through year-end 2008, it produced a positive annual return of 8.6% per year versus a 3.9% per year decline in the S&P 500. Now, that’s some serious alpha! (Note for those who don’t speak geek: alpha means outperformance.)

In 2008, when even many balanced funds, such as the type Evergreen runs, were down over 20%, the Strategic Growth Fund (SGF) was down a mere 9%. Meanwhile, the S&P lost 37%.

Yet more remarkably, when the market fell 47% from 2000 to 2002, the SGF was up roughly an equivalent amount. By 2003, Dr. Hussman presciently recognized an emerging bull market and rode that toro quite admirably before, once again, in 2007, going into his downside protection mode. These deft switches from bearish to bullish to bearish were the main reason the SGF crushed the S&P for the first eight years of its existence. They also thoroughly discredit the currently popular notion he is a perma-bear.

As a result of this extraordinary streak, John appeared to be on the cusp of achieving true super-investor status. And, unlike many who had anticipated a bear market in 2007, he was making bullish noises by December of 2008 when he wrote: "Why Warren Buffett is Right and Why No One Cares." In other words, he seemed on the verge of shifting back to bullish as stocks neared their trough.

Unfortunately for his reputation and his clients, John felt a fiduciary obligation in early 2009 to stress-test market valuations prevailing at the time against the 1930s due to the severity of our most recent financial crisis. This caused him to miss the gargantuan rally that began in March of that year. To compound the error, he stayed effectively short the market as the bull continued to romp. Consequently, the SGF has actually declined by over 30% since the market bottomed at the satanic low of 666 almost exactly 6—yes , that would be another 6—years ago.

Back in early 2009, I repeatedly disagreed with John in this newsletter. As long-time readers recall, Evergreen was stridently encouraging readers to aggressively invest in common and preferred stocks, gold, MLPs, high-grade corporate bonds, junk bonds, closed-end emerging market bond funds—basically, anything besides treasuries and cash.

As I consistently conveyed at the time, even assuming a return to Great Depression conditions—and we weren’t—bonds and preferred stocks were selling at 1932-type valuations, despite the fact common stocks were not nearly as cheap. Many solid corporate yield securities were trading at 60 cents on the dollar or even less. One preferred issue from an insurance company with a clean investment portfolio was at 40% of face value and yielding over 25% (by the way, today it trades at a 4% premium over par with a miniscule yield to its call price).

However, as the years—and a series of new market highs—have gone by, I’ve found myself moving closer to John’s viewpoint. Undeniably, I wish I’d waited a couple more years before I’d started vectoring in his direction. Yet irrespective of the fact that his concerns (and mine) have been way early, I’ve found his weekly newsletter, which I’ve read for years, to be a steady source of rational market analysis.

Sadly, John’s huge lag since the market bottom has now put his SGF into a deep hole versus the market since inception. This performance deficit has caused him to be ridiculed in cyberspace (Twitter, etc.) to a merciless degree. Candidly, my heart goes out for him because I believe he’s truly a brilliant and good man. Having been in this business for so long and having personally incurred intense criticism for calling out both the tech and housing bubbles (both times well in advance of their popping points), I have special empathy for his travails.

Despite these relentless and withering attacks, John has maintained his poise and his convictions. In my mind, this is a quality—perhaps the most important quality—that makes a great investor. He has also freely admitted his mistakes and has sought to modify his process so such a massive miss doesn’t happen again. This type of honesty is another attribute that I think is essential to be an outstanding portfolio manager which, notwithstanding his big whiff, I believe he still is.

As David Horn, professor of value investing at Columbia University, noted last November, in a spirited defense of John, other superstar investors have suffered similar falls from grace. Jeremy Grantham, so often lauded in these pages, and his ultra-successful firm GMO, experienced over 60% client defection during the tech bubble in which his firm refused to participate. Former Morningstar Portfolio Manager of the Year, FPA’s Robert Rodriguez, saw roughly half of his firm’s clients leave—twice—when he was warning about the tempest he saw coming both in 2000 and again in 2008. . (Speaking of Morningstar, this is what they had to say about the SGF in 2008: "We highly recommend this fund for investors looking to add a dash of diversification to their portfolios." Today, they give it their lowest rating.)

Please don’t get me wrong: I think John made a huge mistake by not at least capitalizing on the Depression-like valuations available in corporate yield securities in early 2009. However, I also remember how panic-stricken even professional investors were in those days and the amount of heat we caught for buying securities that continued to fall in value almost every day.

Very few professional money managers, yours truly included, avoid periods when they fall out of phase with the market. For value-oriented folks like John Hussman and me, this usually happens late in a long running bull market (thankfully, Evergreen caught most of the current one). There is usually intense pressure to cave in and throw traditional valuation metrics out the window with the recurring, but not very rational, rationale being: "This time is different." Back in 2000, it was the Internet. In 2007, it was the Fed’s Great Moderation. This time it’s the From Here to QEternity paradigm. But, in the long run, valuations always carry the decade, if not the day.

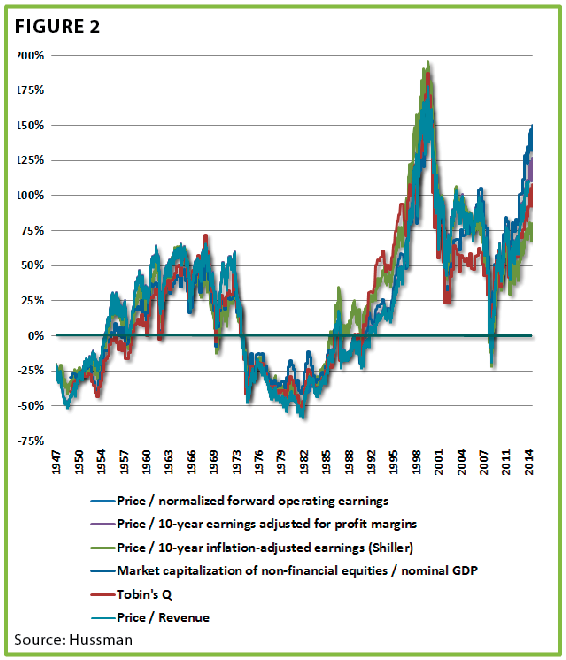

Another reason I respect John Hussman is that he employs a number of proven valuation techniques--unlike the Fed, which relies so heavily on a single model that has had little predictive value. As he admits, it wasn’t that his process failed back in 2009 and during the first few years of the bull market. Rather, it was that he overrode his ensemble of valuation indicators due to the severity of the financial meltdown.

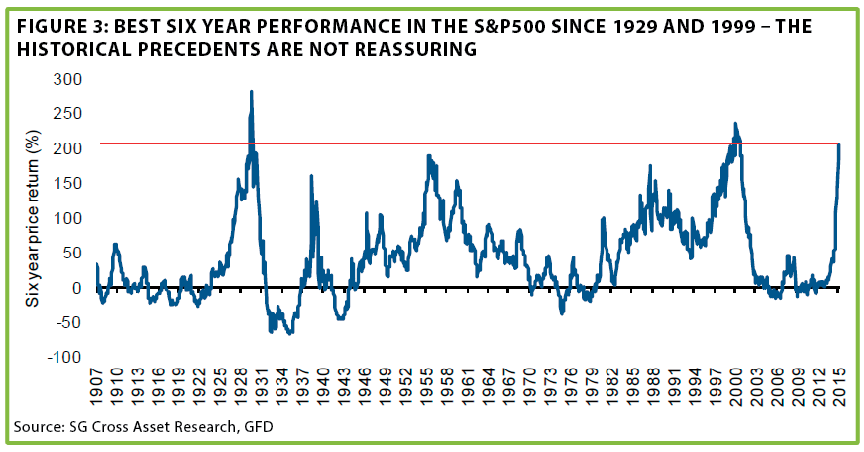

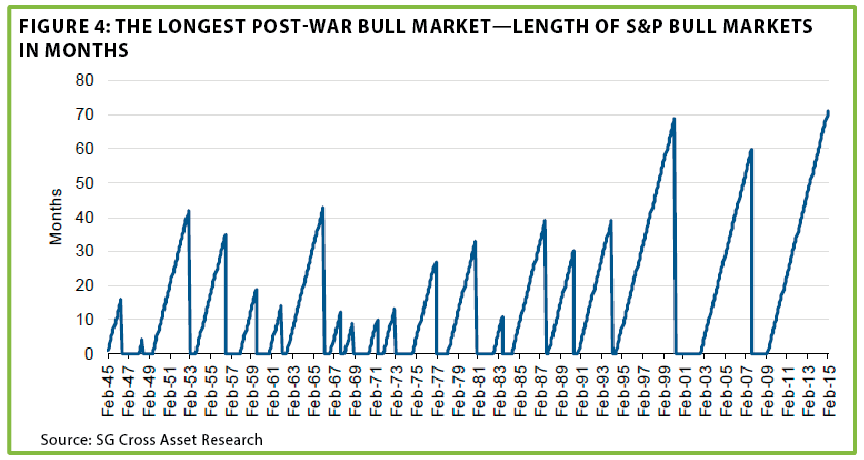

It also appeals to me that his value determining process is designed to avoid the pitfall of concluding the market is cheap during periods when earnings are unsustainably high, a trap Wall Street continues to fall into again and again. Below is a chart that incorporates all of his key indicators accompanied by a couple non-Hussman graphics we think reinforce the basic message that we are very, very late in this up-cycle.

Over the years, an important lesson I’ve learned is to listen to smart people who have been relegated to dummkopf status by the market’s "intelligentsia". I vividly remember many pundits proclaiming that Warren Buffett had lost his touch because he didn’t get the new math of multi-billion dollar dotcom valuations for eyeballs and click counts. Guess who came out on top of that one? (By the way, that not- so-new math is making a comeback these days.)

When the next downturn arrives, I am convinced John’s fund will once again be among the best performers and that he will quickly climb out of the supposedly inescapable performance hole he is in now. It’s tough to keep a good man down—especially one who has the courage of sound convictions.