“Price is what you pay, value is what you get.”

-Warren Buffett

Special message: Thanks to your loyal readership, as well as your advocacy, we recently eclipsed 5000 readers of our weekly e-letter. The intent of the Evergreen Virtual Advisor (EVA) is twofold. First, we try to convey to our clients the rationale for decisions we make within their portfolios. Secondly, we want to share our outlook with industry peers and other interested parties so that we may engage in useful dialogues with many of our professional readers.

Jeff Eulberg and Tyler Hay have both been at my side for the last 10 years. Going forward, they, and occasionally other members of the Evergreen Investment team, will contribute their perspectives on the financial markets, economies, and investing, as part of the narrative section of the “Points to Ponder” edition (which is published every other week). They often have opinions that run contrary to mine, but I respect their intellect and think you will enjoy reading their work.

We welcome and encourage your feedback on our new format!

POINTS TO PONDER

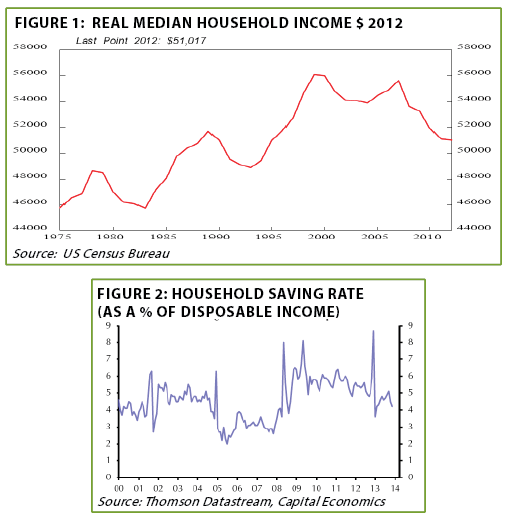

1. With euphoria back in the driver’s seat for financial markets, it seems almost like nit-picking to bring up the twin realities of weak real household income (which continued into 2013) and a subdued savings rate. Yet, both beg the question of how the consumer-driven US economy can experience rapid acceleration, an outcome stocks seem to be anticipating. (See Figures 1 and 2)

2. The February 28th EVA noted that the US energy sector has of late been running at full capacity, unlike almost every other US industrial segment. However, recently announced capital spending cuts by several major oil companies suggest a challenging environment over the next year or two for energy service companies.

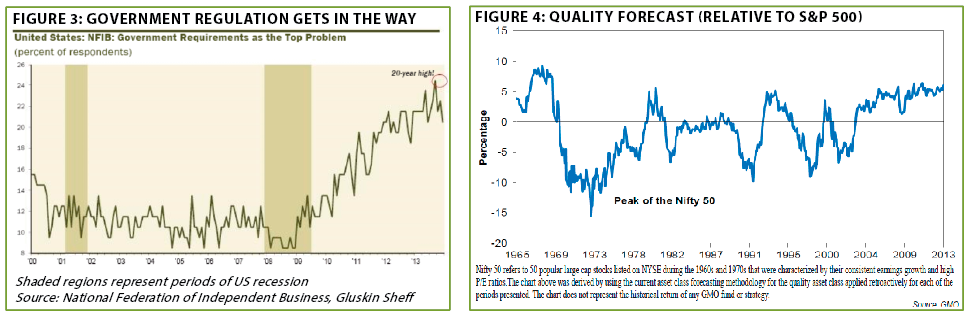

3. It’s universally accepted that small businesses are the primary propellants of job growth. Accordingly, it’s highly plausible that the main reason employment gains have been so deficient during this expansion is the onerous hand of government regulation, a problem the Fed’s printing press cannot fix. (See Figure 3 below, left)

4. Even efficient market adherents concede that high-quality stocks outperform in the long run. However, GMO’s Ben Inker points out that, as with all categories of the market, this is only true when they are undervalued. Currently, high-quality shares are priced to provide one of their best relative future returns over the last 50 years. (See Figure 4 above, right)

5. There was considerable enthusiasm when the initial 4th quarter GDP report was released, showing respectable growth of 3.2%. Unfortunately, Q4 has since been reduced to 2.6%, not far above the lackluster level that has characterized the post-recession era. For all of 2013, the US economy grew by just 1.9%.

6. Evaluating insider selling data has become more complicated. The SEC now mandates that holders of more than 5% of a company’s shares be classified as ‘insiders.’ As a result, raw numbers need to be adjusted to identify actions by true insiders. Screening out big institutional holders reveals the most intense insider selling in 25 years, per Wall Street Journal’s Mark Hulbert.

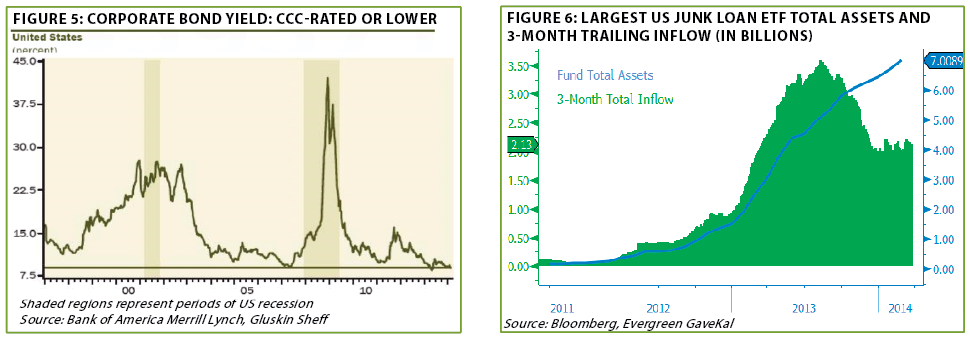

7. Financial market commentators warning of bubble-like conditions have mostly been focused on biotech stocks and glamour issues like Tesla, Amazon, and Facebook. However, massive inflows into CCC-rated junk bonds and loans, combined with puny yields, especially given the amount of risk, are another vivid indication of top-of-the-cycle risk tolerance. (CCC-rated bonds are just a notch above those in default.) (See Figures 5 and 6)

8. Canada has become a net creditor country for the first time since records on this status began in 1990. This is despite recurring trade deficits in recent years and is at least partially a function of the sharp depreciation by the Loonie (which increases the value of Canada’s overseas holdings and lowers the worth of foreign ownership of its assets).

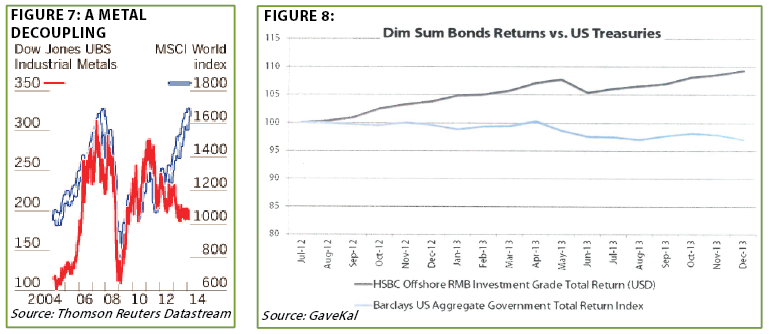

9. Industrial metals and global stock markets have moved essentially in lock step over the last decade. Lately, though, in another example of what acclaimed economist Gary Shilling calls “The Great Disconnect,” there has been a dramatic divergence. This is likely an additional consequence of central banks creating another “Great,” as in “The Great Levitation” of stock prices. (See Figure 7 below, left)

10. Until recently, the high-grade bond market located in Hong Kong and denominated in renminbi, China’s currency (aka, dim sum bonds), was a paragon of stability. This was the case even during last summer’s rout in almost all things yield-related. However, in recent weeks the renminbi has come under severe selling pressure, at least based on its typical steady trading history. This gives US investors another chance to attain superior yields (4.5% for three year maturities) in what likely remains an undervalued and gradually rising currency. (See Figure 8 above, right)

Where did the growth go? In keeping with this week’s NFL-themed EVA, per Tyler’s and Jeff’s sections below, the legendary John Madden once quipped that “winning is the best deodorant.” When it comes to economies, and even stock markets, this could be altered slightly to “growth is the best deodorant.” Much like piling up football victories, robust growth can cover up a multitude of sins. However, when growth rates slow, things get rather smelly, causing policymakers to engage in an often futile attempt to cover up the stench.

At Evergreen’s recent Annual Outlook Event, a very astute client brought up the point that our bearish attitude on stocks seems at odds with a growing economy. It’s a valid critique that perhaps numerous EVA readers share. My response was that we are not among those calling for a recession anytime soon. In fact, we feel this could be the best year of the recovery.

Still, this doesn’t change our strong belief that stocks are too expensive and vulnerable to the air pocket effect—like when you’re on a jet and it plunges a few hundred feet in a split second. As we have conveyed in the past, the stock market plummeted by almost 20% in one day in 1987. And this came at a time when the US economy was growing at almost a 7% annualized rate. Moreover, stocks were not nearly as expensive then as they are today.

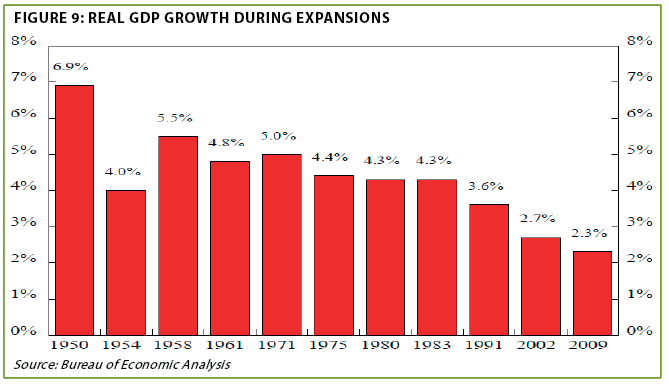

Beyond the potential for a rapid reversal of some of the gains seen over the last couple of years, there is a bigger issue. Corporate earnings closely track the economy’s overall growth rate and, in the very long run, stock appreciation is tightly linked to profit increases (even though on a shorter-term basis there can be a divergence). And therein lies the problem... (See Figure 9)

At our Outlook Event, I neglected to make the important point that this ongoing growth shortfall isn’t just a function of Obamanomics. In reality, growth gone (mostly) missing has been the case since the start of the new millenium. Consequently, over the last nearly 15 years, the US economy has expanded at just 1.4% annually versus the historical 3% or better clip. And while we’ve had two recessions in that time frame--one mild and one horrendous--we’ve also had two expansions.

This era additionally included a pair of bubbles—tech and housing—although, admittedly, the dotcom mania flamed out at the start of this period. Now, however, our team at Evergreen believes we’ve got a third bubble on our hands. Many would disagree, but given all the past factors we’ve previously highlighted—like record margin debt, IPO fever, a bevy of 100 plus P/E stocks, frantic inflows into the junkiest bonds, and many similar indications of rampant speculation—we are serene in the conviction that time will validate our outlook.

Consider this: Even with all these bubbles, more than $10 trillion of accumulated Federal deficits (and debt) since 2000, and over three trillion of the Fed’s funny money, we’re only averaging about half of our usual growth rate. Part of this is due to an older population that isn’t having as many kids. Overall growth is derived from population increases and productivity. And, by the way, the latter is averaging less than 1% yearly since 2010.

Finally, as we’ve shown before, earnings have become far more volatile. Therefore, we’ve got slower and more variable growth, combined with an extremely pricey stock market. If that makes sense to you, I’d suggest you check out next week’s EVA on why the Fed’s surefire plan to reignite growth has backfired—with perhaps the biggest misfire yet to come.

Inefficient markets: Don’t say the NFL didn’t warn you! You may be wondering what the National Football League has to do with financial markets, but I believe there is a connection. The typical NFL franchise is valued at around a billion dollars. The owners are typically extremely wealthy individuals who have had wildly successful careers. But ,when behavioral economist Richard Thaler studied the NFL’s annual draft of collegiate players, he found the single greatest inefficiency in markets he’s ever encountered. Those are pretty bold words for a Nobel Prize winner who earned his fame exposing irrationality in financial markets.

The NFL draft occurs every April. There are 32 picks per round and 7 rounds that constitute the draft. Its purpose is to restore the balance of power throughout the league by allowing the worst team from the previous year to have the first pick of every round, the second worst team gets the second pick, and so on. The last (or 32nd) pick of every round is the team that won the most recent Super Bowl. (Just in case any of you missed who won this year, it was my favorite team, the Seattle Seahawks.) The hope is that struggling teams pick the best players in college football and, in turn, improve their team relative to others.

Competition in the NFL is fierce. The owners are presumably smart people. They dedicate entire personnel departments to the exhaustive scrutiny of potential draft picks. These individuals, called scouts, possess intimate knowledge of the game of football and analyze college players year-round. Heights are measured, countless hours of film dissected, forty-yard dashes timed, mental and behavioral tests administered, and even interviews of family members are conducted. Such intensive research should ensure that teams thoroughly know the players and the value each can add to their potential team. It should, but it doesn’t.

Thaler found that NFL teams behaved in two highly irrational ways. First, teams had a tremendous misunderstanding of what each pick was worth relative to another pick. Second, the difference in value between any two players drafted consecutively was barely better than chance.

Let’s first look at the “relative value” mistake Thaler discovered. In the early 1990s, a minority owner of the Dallas Cowboys, who had a background in engineering, was tasked to solve a recurring problem that occurred on draft day. Specifically, teams needed a way to determine what each pick was worth in relation to another. For example, was the first pick in the draft worth the same as the 15th and 47th overall pick? There was no formula for comparing different picks’ worth. The result of the Cowboys’ analysis became what is known today as “The Chart.” This insight helped create a system for valuing picks and allowed for quick assessment when considering trading them.

The Chart (which you can see here) assigns a point value for each pick. The first pick is worth 3000 points. The 7th and 8th pick combined are also worth 3000. It could also be stated that 29th, 30th, 31st, and 32nd pick equal 3000 points, or the first pick. If you’re thinking that trading four picks for one seems a little unbalanced, you are onto something.

Given the NFL’s deeply competitive nature and highly “cross-pollinated” coaching staffs, The Chart quickly became a draft day Bible amongst NFL executives. But Thaler’s work found something extremely interesting when analyzing The Chart.

First, and most importantly, he found that teams dramatically over-weighted the value of high draft picks. The drop-off between the 1st and 32nd selections was marginal, yet teams perceived the drop-off to be very steep. Along these same lines, he found that very costly draft picks in the early rounds often don’t turn out THAT much better than ones in the later rounds. This is because it’s true that players taken in the first round do turn out to be better selections over time than later picks. BUT, and a big but it is, not by a very wide margin. If you examined every draft pick ever taken, the higher draft pick (i.e. 4th vs. 5th or 100th vs 101st) only turned out to be better than the player taken after him 52% of the time. You could have flipped a coin and done about as well!

When Thaler published his study (click here to read) in 2010 and attempted to share his findings with NFL teams, they weren’t interested. Thirty-one out of thirty-two teams in the league dismissed his analysis, but one was curious. Any guesses who that was? Bill Belichick of the New England Patriots. For non-football fanatics (though they all surely stopped reading long ago), he’s considered the best coach of the last decade, and it’s not even close. In the last few years, you’ve seen more and more teams adopt Thaler’s analysis. That said, there are still plenty of teams who are grossly overvaluing high draft picks.

This type of behavior should be alarming for introspective investors. First, who would believe that compelling evidence could stare intelligent people in the face, only to see them bury their heads in the sand? Surely, investors aren’t capable of this—after all, they are dealing with something more important than players and some silly game. Investors deal in the very serious business of money, where people are much more rational.

But are investors really better at being rational and disciplined? Are they truly able to identify the relative value trade-off that exists within the financial markets? Do investors refuse the allure of high returns when market conditions warrant caution? With hindsight as your cheat sheet, since 1999, during what two time periods would it have been most prudent to minimize your portfolio’s stock exposure? Answer, 1999 and 2007. Yet, as we shall see, investors did the opposite.

Now, you’re probably thinking the collapses that followed 1999 and 2007 were impossible to predict. In magnitude, I concede that few got it right, but directionally, it was staring investors in the face. The first warning sign was high valuations. The two highest cyclically-adjusted P/E (CAPE) peaks of the last 50 years occurred in 1999 and 2007. Historically, these extreme levels of overvaluation led to subsequent average 10-year real-returns on the stock market of just 0.5%. Said another way, paying over 25 times the CAPE in the past, which is where we are today, led to barely getting your money back over the next decade.

A market that has a high P/E is very similar to a high draft pick. You buy the stock market because you want the additional return that stocks provide over lower returning asset classes such as bonds. In a market environment like today’s, US stocks are the sexy first round picks, while asset classes like gold and emerging markets are 7th round picks no one wants. The US stock market is the media darling, momentum is strong, expectations are high and people have retired the notion that with higher returns comes increased downside risk.

Technology stocks fifteen years ago were another classic example of the equity market version of the ultimate number one draft choice. The Internet was truly revolutionary. Following its inception, tech companies were formed and made both massive profits for shareholders and life-altering products for society. Unfortunately, there were also many companies that were barely final drafts of a business plan selling for crazy prices (worryingly, this same phenomenon is also playing out today). And, despite the fact that the internet and most things tech-related have grown rapidly over the last 15 years, tech stocks have turned out like numerous number one draft choices: Terrible investments.

If only you could know when prices were CRAZY! Well, we think you can. As many of you know, we have a proprietary methodology for tracking investor exuberance or pessimism through fund flows. But you don’t have to have a fancy quant model to know when investors are rushing late to join the party. It usually just takes some basic fund flow data and common sense. There has been one year over the past decade and a half where investors added more money to stocks than they did in 2013. That year was 2000 just as tech stocks were ready to vaporize (another year of large in-flows was 2007, mostly into overseas markets, right before they crashed).

The stock market, like a high draft pick, can offer the most upside in your portfolio relative to other safer investments. But, just like savvy NFL teams, smart investors should understand the need for balance. And the ones that trade away several picks for a single high selection are playing a game of roulette. For investors, especially those who rely on their portfolio to sustain them through retirement, betting too heavily on the stock market is a big gamble. Use the common sense indicators of valuation and sentiment to ensure you’re not risking your franchise—i.e., your personal net worth—on a few high-priced, and hyped-up, draft choices. If you don’t, your portfolio could end up NFL (NOT FOR LONG!).

Fan does stand for fanatic. By now, it should be painfully obvious that the Evergreen team is quite sad this past NFL season has come to an end. So, in an effort to keep the Seattle Seahawks’ magic alive, I too will use the NFL for comparison purposes. To be sure, the NFL is a copycat league. Once a successful franchise does something that works, the rest of the league emulates that winning formula.

After the Seahawks convincingly won the 2013 Super Bowl, teams quickly admitted that they’d be duplicating Seattle’s blueprint. Teams now are committing to tall and physical defensive backs, strong running games, and a defense-centric philosophy (Unfortunately, for the rest of the NFL, Richard Sherman, Earl Thomas, and Russell Wilson don’t exactly grow on trees.) Basically, to mimic a champion, these teams often create cheap imitations that fall short of desired returns.

The markets, in a similar fashion, also tend to have a copycat aspect to them. If one investment style works in a given year, you’ll likely see significant fund flows into the outperforming asset class the following year. Flow-of-funds analysis is an integral part of the Evergreen investment process. We use this data to guide us away from overvalued and trendy asset classes, and towards undervalued and underappreciated investments.

While the overall US stock market might not be in a full-blown bubble just yet, we are seeing areas that seem worthy of this ominous distinction. Specifically, some newly-listed Nasdaq companies, healthcare’s biotech space, and definitely small cap US stocks.

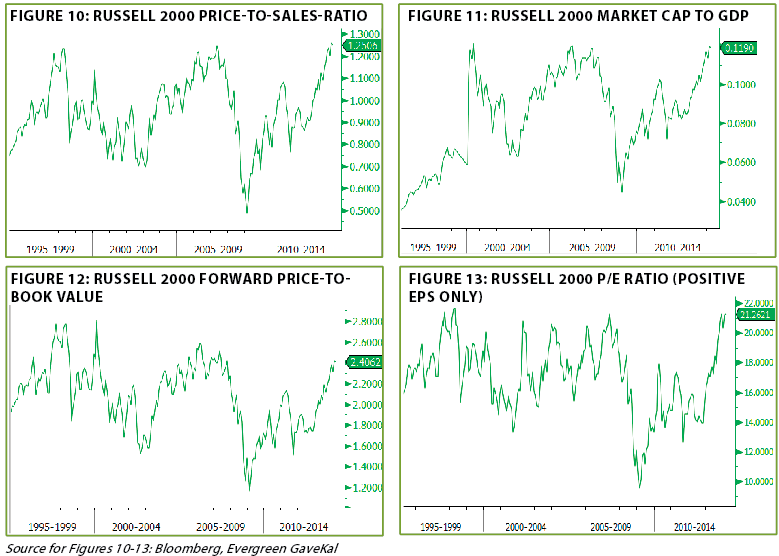

For the past few years, investors have been attracted to the US small cap space due to the belief that these investments closely mirror the US economy. And, if you were to look only at the annual returns in excess of 29% since the bottom of the Great Recession, you’d be hard-pressed to dispute this notion. However, it doesn’t take much digging to find some flaws in this line of thinking. In fact, the price appreciation of this style comes from loftier valuations, while actual earnings and revenue growth hasn’t kept pace with this meteoric rise. On the next page, are a few charts that plainly illustrate this style’s overvaluation. Since most investors have vivid memories of the tech and housing bubbles, I thought it best to compare current valuations to the two most recent peaks. (See Figures 10-13)

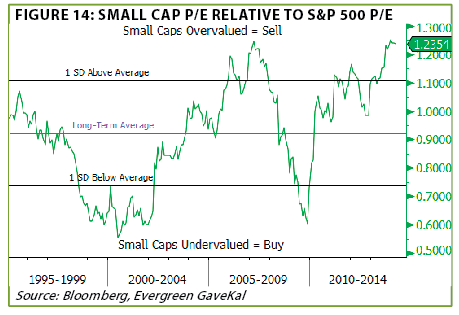

As mentioned above, we believe the S&P 500 is overvalued at current prices, but not quite as expensive as previously inflated levels. Jeff Dicks, a vital member of the Evergreen investment team, recently created the chart below. In it, he clearly shows the dramatic overvaluation of small companies compared to an already expensive S&P 500. Based on historic valuation, it’s hard to argue that this space still presents decent value for investors. (See Figure 14)

When building a client’s portfolio, it is best to avoid looking through the rearview mirror to determine proper allocations. Professionals who are willing to go in a different direction from the herd usually end up reaping the greatest rewards. I certainly can’t blame NFL teams for trying to copy the greatness of the Seattle Seahawks. Investors, though, should stick to investing in companies with reasonable valuations and avoid using past performance as a guiding compass for future returns.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.