"The US stock market has been this high only three times before since 1881."

- Yale University’s Dr. Robert Shiller, referring to the price/earnings (P/E) ratio that bears his name.

Mauled by a bear. One would need to be a very cursory or infrequent EVA reader—God forbid!—to be unaware that this author believes most investment assets are presently priced so high as to virtually offer return-free risk. And I’m aware that many of you think I’m a party-pooper for believing this but the fact is the math is on my side* (a more detailed analysis can be found at the end of this section). Yes, I know most of you also hate math (I can empathize with that) especially when it leads to an unpleasant conclusion. But there is some good news in this regard that I think you’ll want to hear.

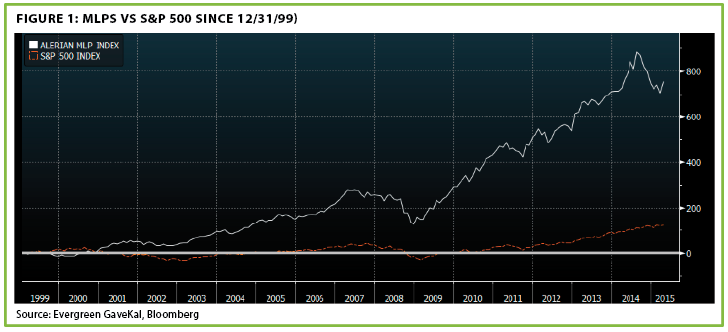

For years I’ve attended the National Association of Publicly Traded Partnerships (aka MLPs), missing only a couple over the last decade. The information I’ve gleaned at these has turned out to be invaluable, as have the relationships I’ve formed. In case you think MLPs are too messy to deal with (those pesky K1s), you should know that this sector has produced an annual return of 16% since Y2K (that would be 1/1/00). Fortunately, Evergreen’s MLPs have done even better, though I don’t want to incur the wrath of our compliance folks by telling you how much better.

Last week was that time of the year for me to trek to the "Right Coast", hot and steamy Orlando, Florida, to hear from the senior management of most of the important MLPs (and a number of the not-so-important ones). At this event a year ago, I was struck by the ebullient, nearly euphoric mood. It was almost like being around a bunch of tech management teams and fund managers in 1999—and that made me very nervous, as I warned in the 5/30/14 EVA.

While this wasn’t the only reason Evergreen began to lighten up on MLPs last summer, it was definitely a factor. We were also concerned about high valuations and excessive popularity among retail investors (funny how often those two go together like, as Sinatra used to croon, "a horse and carriage"). In fact, a year ago I highlighted one MLP that had gone up 400% since going public and the dangerous speculative fervor that reflected. (By the way, that particular issue has been cut in half since then despite spiking another 65% after I noted its extended valuation, showing how fast lush returns can vaporize, as noted on the chart on the next page).

As the summer progressed, our fears of rising credit spreads—almost always tough on MLPs—also led us to have our lightest weighting ever in this, our favorite, asset class. Frankly, we grossly underestimated how much oil prices would fall but that, combined with the above listed factors, led to an actual bear market in MLPs. From their peak on September 5th of last year, to their trough on January 16th of this year, MLPs tumbled by a cool 25% (not so cool if you were loaded up on them).

Consequently, you may have noticed that the incessant advertisements about new and existing MLP funds have almost totally disappeared from the media. Similarly, the once-glowing Wall Street commentary on this space has become far more guarded. There are even sources that are attacking the basic construct of MLPs, especially the portion of cash flows that accrue to the general partners (more on that to follow).

But for us, this is a stellar opportunity to redeploy cash we raised last summer at depressed prices and attractive yields. This is another case study in why, at Evergreen, we like to say: "It’s hard to buy low, unless you sold high."

If you’re like me, you prefer tangible examples over the kind of vague statements I just made in the preceding paragraph. However, if you are our compliance folks, you hate them. So I will try to walk that tightrope between giving you specifics and causing a compliance catastrophe (how other newsletters can go into extreme detail and provide the names, rank, and ticker symbols, for the positions they like—or dislike—continues to confound me).

[*For example, Evergreen’s preferred valuation metric, the price-to-sales ratio has had an 89% success rate forecasting future market returns with the only misses being due to temporary overshoots on both the up-and down-side. For an excellent treatise on this, please go to this link to John Hussman’s newsletter, for his stat on the price-to-sales ratio’s extraordinary predictive track record.]

Another shot at yield you can live on. Let’s start with a couple of energy shipping MLPs Evergreen has owned for years. Nearly a decade ago, I became acquainted with the gentleman who serves as CEO for both entities. He struck me at the time as realistic, straightforward, and credible. Over this period, he has delivered pretty much as he outlined all those years ago. Yet, the unit price of his oil service and transport MLP is lower now than it was when I first met him—despite a 60% increase in the distribution (never say dividend to a MLP CEO!) and the utter collapse in alternative yields like most REITs, utilities, and preferred stocks. As a result, it now yields 9 ½% (it also doesn’t produce a K1) and is poised for a nice distribution hike as a $600 million asset comes on line next month. Moreover, its cash flows are backed by long-term contracts from blue chip energy companies.

The sister MLP, one of the world’s leading LNG shipping companies, has fared better but is still trading with nearly an 8% yield. It is enviably poised to benefit from the frenzy of LNG export construction in the US Gulf Coast, as our country prepares to become a major exporter of this clean fuel to Asia. Its contracts are even longer term—on average running for twelve years, with inflation escalators—and involve a similarly elite list of major oil and gas enterprises.

The first MLP is down nearly 40% from its 2014 zenith while the latter is off a more modest, but still substantial, 25 %. Fortunately, we had reduced our position in both of them, especially the former, around their highs so we are now preparing to buy them back at these juicy return levels (there’s that sell-high/buy-low thing again).

Unquestionably, there are MLPs out there with faster prospective distribution growth, but the predictability of these two is especially valuable in a world where a massive amount of energy projects are on hold. Therefore, we have a bias toward those entities that can maintain their distributions even during an adverse energy environment. Reflecting modest but realistic growth expectations, both of these should be able to elevate their payouts by at least 2% annually. This means that, unlike with a bond where you need to subtract around 2% from the stated yield to arrive at the real yield, an investor is receiving an after-inflation return of 9 ½% and 8%, respectively. That was most attractive in the "good old days" when interest rates actually existed. Today, it is incredible.

One of the knocks against MLPs, particularly those that have been around for awhile, is the general partner (GP) cut of marginal, or incremental, cash flows. In the argot of the MLP world this is known as the Incentive Distribution Right (IDR). It’s a legitimate beef and one I will soon delve into (I promise) as it is the source of an interesting change going on in this sector. But first, I wanted to mention a recently minted MLP that has no IDR "drag".

This publically traded partnership was spun off last year from a couple of venerable energy corporations based in the heart of oil and gas country. It came out with comparatively low debt meaning it could make growth-boosting acquisitions without resorting to the sale of additional units (MLPs are not technically transacted in shares similar to the distribution vs dividend aspect). Because it is new, it also is at least a year and a half away from hitting the trigger point where the GP gets an increased portion of the cash flow—the IDR. Even when it does, it will gradually be working its way up from a 15% split to the maximum 50% cut on additional cash flows. By the time the GP hits the full 50% split, the limited partner will be earning a 10% cash-on-cash return based on today’s price.

The fact that it has no GP drain currently gives said entity a material "cost of capital’ advantage when it comes to bidding for new assets like pipelines and gas processing plants (where natural gas is "fractionated" into ethane, propane, and butane). Nevertheless, this partnership has been hit even harder than the overall index, falling by 35% from its 2014 high. It now yields 7 ½% and although distribution growth expectations have fallen from a range of 7% to 9% to 3% to 7%, this should still amount to the aforementioned real return—or better—not yield minus inflation.

The CEO is newly arrived from a senior position at arguably the finest MLP of all time (though there is no argument in my mind). According to one of my unimpeachable sources of quality "MLP intel", someone who worked with him for years at that best-of-breed enterprise (that’s a big hint for you sleuths), the new CEO is an extremely capable manager.

Let’s look at one more specific situation and then examine a few of the most interesting new developments in this space.

Boring no more. Generally, Evergreen tends to trim back on our MLP exposure rather than sell out completely. This is due to tax considerations and the reality that often, like regular stocks, they continue rising well beyond what we believe to be fair value. This next MLP was an exception to our partial-sale tendency, however.

After generating a return of around 60% in little over a year in this security, we liquidated our entire position. Although it appreciated substantially from our sell point (we’ve got a knack for selling early), since last summer it has executed a 40% power-dive and is now basically back to the price at which it was sold. At today’s nearly half-off level, it yields 7%. However, what struck me even more from hearing the CEO’s presentation is how confident he is in achieving 20% plus annual cash flow (EBITDA) gains over the next five years. This won’t translate into 20% distribution increases, as they’ll need to issue both additional units and debt to finance this high level of growth. But they believe their payout is likely to rise materially faster than current estimates of around 5%.

One of the reasons we sold this issue completely was that it originally operated in just two relatively unexciting oil and gas producing zones, typically referred to as basins. However, they are now far more diversified and are exposed to the exceedingly hot Marcellus Shale that extends through much of the western areas of the Mid-Atlantic Seaboard states. Moreover, original two "boring basins" has become anything but—a very interesting nugget of info I learned last week.

It was at this event five or six years ago that I first became convinced that the marriage of fracking and horizontal drilling was going to revolutionize US oil and gas production. At the time, few outside of the industry believed it was possible to halt the long slide in America’s energy output, much less see it virtually double in a few short years. But that’s exactly what happened, defying countless skeptics.

As part of this shocking revival, basins such as West Texas’ Permian, long believed to be mostly played out, have come roaring back as prolific producers of both oil and gas. Last week, I repeatedly heard the same dynamic is occurring with the Barnett Shale which sits below the cities of Fort Worth and Arlington. And this happens to be one of the "boring basins" in which this MLP is now enviably situated.

Moving to an even bigger picture theme, another stand-out discovery for me was a new process known as re-fracking or re-development. This is where previously fracked acreage is re-worked through drilling multiple wells in an area that previously had only one. Typically, just 10% to 20% of the hydrocarbons in a "play" are produced, even with the one-two punch of fracking and horizontal drilling. If the single well was on a 320 acre site, for example, the operator is now going back in and drilling a new hole on each 80 acre parcel. A more concentrated, high-intensity process is then used to produce an amount of oil and/or gas far greater than what was originally extracted. This is both a very low risk and high-return technique that has almost everyone in the industry pumped up like Pete Carroll celebrating a Seahawks touchdown. Yet, like fracking six years ago, it is not receiving mainstream media coverage.

Now, it’s finally time to talk about that confiscatory 50% general partner rake off...

The shale also rises. First, please realize that in order for the GP to be receiving 50% of distribution increases, it means that the original limited partners have enjoyed a substantial increase in their payouts, as illustrated above. This almost always leads to a similar rise in the unit price.

Second, many GPs are now publicly-traded, so if an investor wants to be involved in the entire enterprise he or she can buy units in both—or just the GP. The trade-off is that these sell with lower yields due to expectations of much faster distribution growth.

Nonetheless, having 50% of additional income flow through to the GP does make it quite challenging to make "accretive" investments—i.e., those that add cash flow—to the MLP, creating what’s known as a cost of capital disadvantage. This reality is behind a somewhat shocking development: Two of the largest MLPs have been reabsorbed by their C-corp parent. In the past 12 months, both Kinder Morgan and Williams Companies have bought back, or are in the process of doing so, the various MLPs they previously spun-off.

The nice thing for unit holders was that hefty premiums over the prevailing market prices were paid in both cases. The not-so-nice thing was that an even heftier tax bill was triggered, at least for long-time investors. (The previously largely tax-sheltered payouts became taxable upon the completion of the transactions.) For tax-deferred accounts, however, these buyouts were unalloyed positives, another reason it’s not a bad idea to own MLPs, with careful selection, in IRAs—despite popular "wisdom" to the contrary.

For taxable accounts, though, these deals negate one of the underappreciated benefits of MLPs, especially for "mature" holders. Few realize that if units are held until one of the two joint owners dies, in the case of a married couple, a basis-step up at the first death eliminates both the gain from the original purchase price and also the cumulative sheltered distributions. (The same step-up occurs for single holders, benefiting his or her heirs.)

So, for example, let’s assume Mr. and Mrs. Jones bought 1000 shares of XYZ MLP at 20 back in 2005. It is now trading at 50 and has additionally paid out $20 of distributions over the years of which only $4 was taxed (MLPs typically shelter about 80% of their payout). If Mr. Jones dies (let’s face it, us guys usually go first), there would be zero tax on either the unrealized gain or the 80% of untaxed cumulative distributions.

However, if XYX MLP actually stood for KMP, as in Kinder Morgan’s MLP, they would be looking at a double tax bill: a capital gain of $30 combined with $16 of ordinary income recapture. Even ignoring state income taxes, the tax liability could be as high as $13 per share or 26% of the realized price. This would still be an excellent after-tax return but far lower than if the investor could literally "go to the grave" with the holding and avoid almost all taxation.

As a result of these two "re-absorptions", speculation is running rampant that there are more in the offing. This is probably true in those larger and older MLPs where it takes bigger deals to move the needle on cash flow and where the GP cut is at the full 50%. Some have wondered if this means the end of the trend toward large energy companies spinning off their "midstream assets", as MLP-quality infrastructure assets are known. This seems unlikely based on the fact that Shell and Devon have both recently off-loaded significant quantities of their midstream resources into MLPs. More probable is that there will be further spin-offs and additional reabsorptions based on the specific circumstances.

In my mind, the biggest story about MLPs today is that because of the buzz-cut many of them have endured, realistic double-digit total returns are now available at a time when these have gone the way of the mullet hairstyle. Doing the math on the MLP value proposition, if an entity is paying out 7%, it only takes 3% distribution growth to hit the 10% threshold for total return (assuming that the yield stays constant at 7%, so that the price gradually rises to match the 3% payout boost). And most of the MLPs I listened to last week are likely to bump their distributions by more than 3% annually.

If this sounds too good to be true, as is so often the case in the investment world, realize that those MLPs operating essentially as "toll-collectors" for America’s energy infrastructure have been able to maintain their earnings and cash flow during this vicious shake-out in the oil patch. In other words, their business models have been seriously stress-tested and, while future growth rates have come in a bit, their distributions have continued to rise, albeit at a more moderate pace. (Note, this has not been the case with MLPs that are producers of oil and gas, a sub-sector Evergreen has avoided.)

This is not to say the coast is totally clear. Oil prices appear likely to pull back again after their dizzying rally. And a general market sell-off would almost certainly clip this space. But prices have reset enough to the downside that investors should be adding selective MLP exposure. You don’t have to be a math savant to realize that a realistic shot at double-digit returns from MLPs is much more attractive than the S&P 500 with just a 2% dividend yield priced at one of its loftiest valuations ever.

In fact, there’s a guy whose math skills, when it comes to the stock market, deserve Hall of Fame status—Dr. Robert Shiller. He continues to warn investors that the investment calculus today is daunting. Yet, few are listening to him, despite his prescient warnings during both the tech and housing bubbles. Oh, that’s right—there aren’t any bubbles today. Well, that’s true with MLPs, where a lot of helium has been sucked out over the last nine months. Take it from another New Englander, Tom Brady, that it’s a lot easier to cheat beat the odds if you let a little air out.