“I think the Biden tax plan is actually going to do exactly what it’s designed to do, which is to help Main Street, help the average American. And it’s going to come at the expense of the 1%, whose wealth primarily is encapsulated in the stock market and financial assets.”

– Hedge fund legend, Paul Tudor Jones on CNBC as of 10/22/20.

“Secular (i.e., long-term) inflation, which I believe is massively underestimated, will be the ultimate demise of the great bull market in long duration assets.”

– Vincent Deluard, Director of Global Macro Strategy for Stone X, Inc.

“There are other reasons gold should do well…one is that gold has a strong inverse correlation to US budget deficits and that has been the case for decades.”

– Fred Hickey, author The High-Tech Strategist and former member of the Barron’s Roundtable

______________________________________________________________________________________________________

For all of us Baby Boomers, Campbell Soup’s iconic tag-line of “MMM Good” was burned into our collective memories at a young age. As we now transition into senior citizenship, we are discovering that it may well be a case of MMM Bad, totally unrelated, however, to what formerly was America’s favorite soup company.

This author can particularly relate to the “mature” life change experience as I am celebrating my Medicare birthday—i.e., 65—on the same day this EVA is hitting your in-box. And like tens of millions of other how-did-I-get-this-old Boomers, I’m being victimized by an entity that, in trying to do what it thought was the right thing over the last 20 years, has created MMM Bad. (Aren’t we all victims of something these days?) Regular readers of this newsletter will not be surprised that I’m identifying America’s Federal Reserve as the perp. Too harsh? In my view, it depends on your time horizon.

First, I must explain what I mean by MMM before I clarify my timing comment. Over the years, I’ve often highlighted that the Fed’s default response to almost any threat has been to crank up its high-tech digital printing press, what I’ve somewhat whimsically called its Magical Money Machine. Never has it been as magical or machine-like as it has since the virus crisis swept the world.

To be fair to the Fed, it simply had no choice but to print by the trillions to fund the US government’s multi-trillion dollar deficits caused by COVID. One of the most astute observers of the Fed, Luke Gromen, has long predicted it would be forced to make the same choice that the German central bank had to make after WWI: print massive sums or allow society to collapse. You may remember seeing those gritty newsreels from the early 1920s, with German citizens wheeling billions of near-worthless Reichsmarks into grocery stores. Thus, the Weimer Republic’s central bank chose to print in almost limitless amounts--in that case, actual currency.

The Fed is far more sophisticated, of course. Its Magical Money Machine involves hitting Control Alt Print on its banks of computers sequestered somewhere deep in the bowels of its DC headquarters, the Mariner Eccles Building (named after a former Fed chairman). This process creates reserves, rather than $100 dollar bills, and these are credited to the accounts of the big banks that are also primary dealers in treasury debt. Thus, the Fed injects reserves into the banking system and receives government bonds in return. Lately, as I’ve anticipated for a few years, it has used its MMM to buy corporate bonds, as well.

One could reasonably argue the Fed’s MMM has saved the country from an economic disaster and caused the monster rally in financial markets since late March. However, it’s also had a dark side for us old-timers by eradicating interest rates. The crushing of yields on safe securities is posing an existential problem for all of us planning to live off the yield on our hard-earned nest eggs.

This is a topic I’ve explored a few times in the past, even well before this problem became as acute as it is today. The reason I’m covering it again is because of a slightly more momentous event than my 65th birthday that is happening soon: The presidential election. Don’t worry, this isn’t going to be another essay on the investment implications about which party wins next Tuesday. In fact, my contention is that, when it comes to MMM, it doesn’t matter.

As my partner Louis Gave recently wrote, the following matrix he saw in one of Luke Gromen’s typically incisive Forest For The Trees essays has helped him understand what the economic policy future holds, no matter who wins next week.

While Louis’ comment was tongue-in-cheek, I think it’s also totally on-the-money—as in, trillions and trillions of fake money. President Trump, a nominal (and late in life) Republican has repeatedly shown he has no qualms about running trillion-dollar plus deficits, even pre-COVID. And he’s also shown that he’s completely willing to encroach on the Fed’s supposedly inviolable independence.

The Democrats, who ironically displayed somewhat more fiscal discipline when they controlled the White House and Congress, are now trying to trump Trump when it comes to outrageous spending. Vice President Biden’s fiscal plans appear to me to be a dream come true for those that espouse another very similar acronym to MMM, the once avant-garde economic theory popularly known as MMT, or Modern Monetary Theory. The disciples of MMT argue that the federal government can spend nearly unlimited sums when necessary. If there aren’t enough buyers of government bonds (the traditional way of funding deficit spending) at prevailing interest rates--which clearly there aren’t--then the Fed simply cracks up its MMM. Thus, MMM and MMT go together like the NFC East and bad football.

In reality, and as I’ve noted before, the US government began stealthily implementing de facto MMT over a year ago when it started buying $60 billion a month in government bonds. This is formally known as debt monetization. The Fed resorted to this pre-COVID due to dislocations in the repo market (where banks lend gargantuan sums to each other on an overnight basis). It was the first inkling that there weren’t enough buyers of treasuries even prior to the virus crisis.

Since then, the federal government has gone from running trillion-dollar annual deficits, to trillion-dollar monthly deficits, at least during the worse of the lockdowns. With the Democrats seemingly unwilling to go along with a miserly $1.8 trillion additional stimulus package (and the GOP-controlled Senate equally reluctant to spend that amount), the spending has tapered off a bit…emphasis on “a bit”. Once the election is past, however, the floodgates are likely to open as wide as the Grand Canyon. Per the above graphic, this is likely regardless of which party emerges victorious.

Meanwhile, the Fed has announced to the world that it is altering its decades-long policy of targeting 2% inflation. It has stated it is now willing to let inflation run hotter than that level, one which is harmful enough particularly for the Boomers who now are lucky to earn 2% on our bond and CD portfolios. This is essentially a zero return after inflation and negative after inflation and taxes. We may soon need to start referring to ourselves as the Busters.

A loyal EVA reader sent me this message last month that is one of the best summations of the current fiscal and monetary madness I’ve seen. With his permission, here it is:

“Dave,

Let me see if I’ve got this right. The Fed has to keep rates low because it’s the only way the government can afford its debt and the benefits it’s promised people. But they need higher inflation because that’s the only way to manage the debt – reduce it by devaluing it. But at some point, higher inflation will lead to at least higher long-term rates, which the Fed needs to avoid. Meanwhile, something like 90% of the people in this country (maybe I mean 98%) aren’t in a position to buy gold, other commodities, real estate, to hedge against that inflation and will be hammered by the rising cost of living. But the debt has to go away because as long as it’s this high, getting any meaningful GDP growth is probably impossible. Meanwhile, the Fed has spent all this time failing to get inflation to 2% (who knows why they want to) but are confident that once they get it to accelerate, they can control it. They can’t get it to go up, but are confident they can keep it from going up too much, whatever that means.

What could go wrong?”

As a minor point of clarification, I’m sure he was referring to real estate other than one’s home since tens of millions of Americans do own their homes. But, overall, I believe he’s on-target that most Americans are woefully unprepared for the new era that lies ahead. That includes the Fed in my estimation. As I’ve written before, it’s my belief it will get a lot more inflation than they are hoping for and this relates to my earlier timing comment.

As the Wall Street Journal’s James Mackintosh wrote in a September 28th article titled “Inflation Is Already Here For Key Goods”, prices are already rising at a healthy clip for goods that consumers need or want during the virus crisis. The inflation rate for items like bicycles, medical care, cable/satellite TV, cleaning products, and food at home are all rising at a 4% to 5% clip. This is being offset by the plunging prices of things like airline tickets and hotel rooms but that’s not where people are spending much money these days. (Of course, that’s also why these costs are falling.) Actually, I would argue that considering the deep hole the economy is in, inflation is running surprisingly high.

Even long-time disinflationist David Rosenberg wrote the following this summer: “The money supply binge is dramatically above anything we saw in the 1970s…The inflationary nature of the coronavirus shock will take time to be realized, but as the recovery slowly takes hold it’s important to highlight the potential for an upward surprise on prices.” (Emphasis added)

Note David’s time reference. On a near-term basis, inflation isn’t a threat other than in the in-vogue areas. But next year is likely to be a much different story once a vaccine is widely distributed and demand levels return to near normal (fully recovering is likely to be a 2022 event).

Let’s assume there is a “Blue Sweep” and the Biden tax and spending platform is passed. The only way it will get funded is by the Fed using its Magical Money Machine. Taxes can’t possibly come up with the needed trillions. Moreover, any truly dramatic tax increase will serve to slow the economy, reducing government revenues and offsetting much of the take from higher rates.

Basically, the only way we’ve been able to hold things together is because of the Fed’s MMM. Everything, and I mean everything, has been contingent on our central bank’s ability to buy US government debt with its trillions upon trillions of bogus bucks. And such dependence is only going to become that much more intense as the next stimulus package kicks in, regardless of which party crafts it. (However, the spending tsunami is likely to be more stupendous under a Democratic president and Congress; if the Senate remains controlled by the GOP, it will likely be somewhat more muted… but not much.)

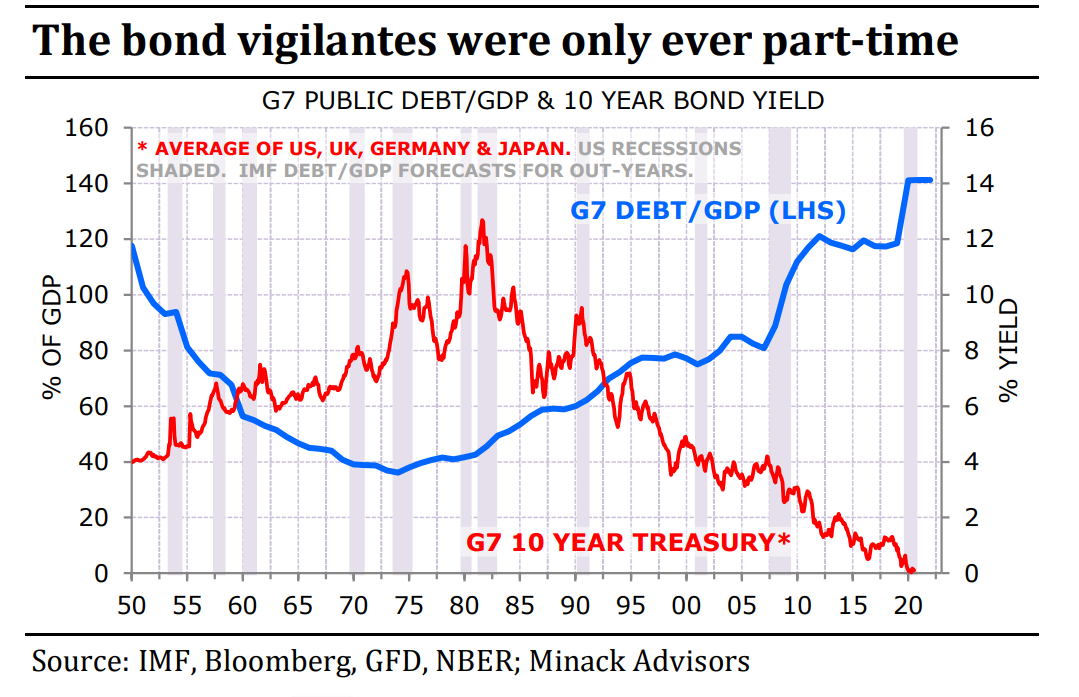

The always insightful Gerard Minack, often a contributor to our Guest EVA issues, recently wrote a note with the clever title of “How I learned to stop worrying and love the (debt) bomb”. In it, he maintains that those studies showing high level of government debt leads to slower growth are erroneous. Yet, as much as I respect Gerard, a chart he ran seems to me to indicate there is logic to the belief that excessive government indebtedness does, indeed, inhibit economic vitality.

The above graphic shows the tremendous debt accumulation in the G7 countries, the largest developed nations, since 2000 (when policymaking seemed to go off the rails in the western world). While this debt binge certainly didn’t raise interest rates (as you can see, it coincided with a stunning drop in treasury yields and this was also the case in all other G7 countries). Growth, however, has suffered mightily over the last twenty years in nearly all developed nations.

Intuitively, this makes sense to me since debt is the pulling forward of future demand. You buy something on credit today and you have to pay it back later, constraining your ability to make purchases down the road. The same is true for governments—unless, that is, they have a Magical Money Machine. This is particularly true for America which borrows in its own currency, a monetary unit that also happens to be the planet’s reserve currency.

My partner Louis Gave has often written that currencies are where the sins of bad policymaking eventually show up. Anyone with a modicum of common sense and historical knowledge realizes America (and most western countries for that matter) have been sinning for years like a sailor on shore leave after a year at sea. It’s my belief—and concern—that nearly all US investors are far too exposed to a long bear market in the dollar, at least versus strong currency countries and real assets. The recent resurgence in crypto currencies--despite their plethora of drawbacks--is a reflection of this, as are the powerful rallies in gold and silver seen since last spring.

With Modern Monetary Theory (MMT) giving US politicians from both parties the greenlight to spend like they never have before, at least in peacetime, financed by the Fed’s MMM, it’s just a matter of time, in my opinion, before we have both a weaker dollar and higher inflation. As Gerard stated in his missive: “Ultimately, sustained aggressive fiscal policy could push economies through their capacity limits and lead to higher inflation. Policymakers will be delighted if that happens.”

As with David Rosenberg, note the “ultimately”. There’s that timing thing again. Related to that, policymakers might be delighted at first with inflation moving above 2% but when and if (I think it’s when, not if) it hits 4% or even 5%, that delight is going to turn into fright very quickly.

Prior EVAs on the topic of MMT have pointed out that the history of prior implementations of such policies has led to a near-term boom caused by the cascade of liquidity. Initially, it appears to be manna from heaven. Asset prices boom, as they have since March – notwithstanding this week’s COVID-caused convulsions.

As I’ve also written previously, inflation is invariably the pin prick of the bubbles caused by MMT “solutions”. That’s when MMM good suddenly turns into MMM bad. The happy news is that the soup isn’t yet bubbling and certainly not close to boiling over. Once the election is over, MMT, Act 3, might well trigger another stunning rally – especially if this correction drives stock prices down even further.

But don’t forget the big picture. The next decade is likely to be hard on soft assets, like most stocks and bonds (see the 1970s), and easy on hard assets such as precious metals, commodities, and securities from overseas countries which are not employing MMT-type policies.

The Boomers who want to avoid being Busters need to recognize how at-risk their retirement futures are as a result of the terrible twins known as MMM and MMT. The good news is there are solutions. The bad news is that very few of us are employing them. Actually, though, for the committed contrarian, that’s good news, too.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.