"Get acquainted with your shadow, or find yourself surprised when a crisis emerges."

- M.B. Dallocchio

"It’s part of what we call the Shadow, all the dark parts of us we can’t face. It’s the thing that, if we don’t deal with it, eventually poisons our lives."

- S. Kelley Harrell

Much more than a shadow of a doubt. The use of shadows is a dramatic device employed to evoke ominous and uncertain emotions from the audience. The endless possibilities of what may be lurking in the dark create suspense and uncertainty in the mind of the audience. Today’s lack of visibility for investors and regulators trying to shed light on that enigmatic entity known as the shadow banking system should elicit similar unease. Yet, despite playing a large role in the financial crisis of 2008, the market’s opinion of this growing sector has reverted to one of indifference.

In the post-financial crisis blame game, global banks deemed "too big to fail" have taken the brunt of the negative criticism. While these big banks definitely deserved some of the flak, the shadow banking system sailed through virtually unscathed. Unfortunately, many of the same risks of 2008 remain today. Due to post-crisis regulations, some of the riskiest loans (previously held by larger institutions and disclosed to investors and regulators) have now been shrouded in the opaque balance sheets of the shadow banking system. While I don’t think the next crisis will repeat itself, it may have some similar symptoms. And, the shadow banking system just may be the canary in the coalmine for where not to invest.

The shadow banking system is so complex it’s difficult even to define. In 2007, at the prestigious Jackson Hole economic symposium, Pimco economist Paul McCulley coined the term "shadow banking." At the time, McCulley was concerned about risky mortgage loans being collateralized in the US—outside of the traditional banking system. In 2012, former US Federal Reserve Chairman, Ben Bernanke, stated: "Shadow banking, as usually defined, comprises a diverse set of institutions and markets that, collectively, carry out traditional banking functions—but do so outside, or in ways only loosely linked to, the traditional system of regulated depository institutions."

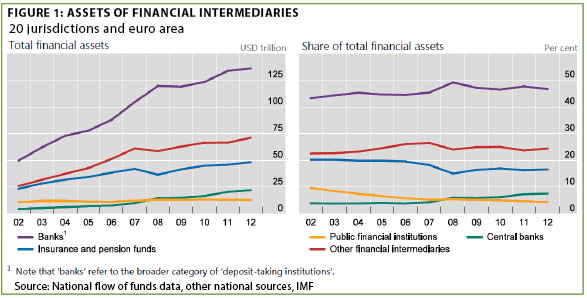

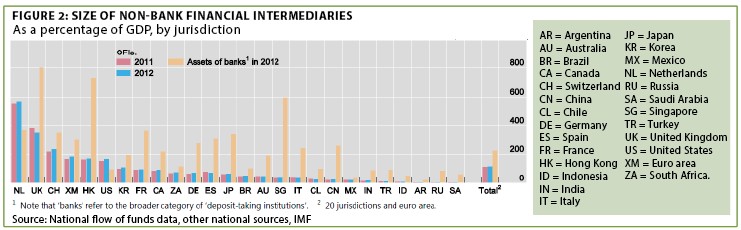

Shadow banks, also known as Other Financial Intermediaries (OFIs), can take on many different forms. This list includes, but is far from limited to, investment funds, broker-dealers, structured finance vehicles, finance companies, money market mutual funds, hedge funds, and other investment entities. According to a 2013 Financial Stability Board (FSB) report, assets held by OFIs comprise more than half of the total global banking system. Further, in 2012, the size of the financial "footprint" by OFIs in the 20 largest markets was 117% of global GDP. In the US, assets held by OFIs are greater than our entire traditional banking system. As you can see in Figure 1 (below) and Figure 2, this is an incredibly large part of the financial system that goes widely unregulated.

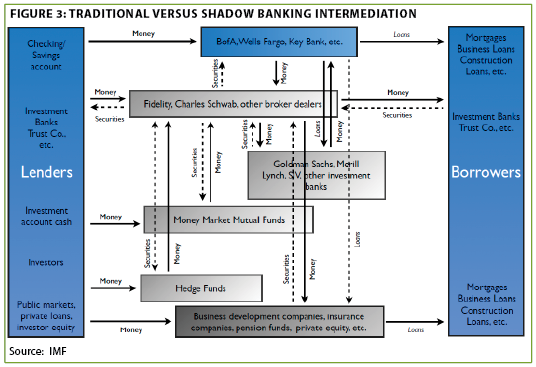

It’s important to point out that not all shadow banking activity is inherently risky. In its simplest form, OFIs can actually align an appropriate lender and borrower. Many of these firms operate in a similar manner to traditional banks, but without an insured deposit base. For example, an insurance company with a long investment time horizon may lend its capital for a large manufacturing project that will take many years to complete. For the most part, these types of bi-lateral loan agreements don’t carry a lot of risk to the financial system. But the more nefarious shadow banking activities such as securitization, pool-funding investments, structured-finance vehicles, security lending, and other investment banking type of activities are a different story. OFIs will generally participate in maturity transformation (short-term funds used to buy long-term assets), liquidity transformation (short-term funds used to buy illiquid assets like mortgage-backed securities), leverage, and credit risk transfer (i.e. credit default swaps). Below is an outline from a recent IMF report on the shadow banking industry, which I’m sure many readers will assume they have little exposure to. So, I’ve provided some relevant, real life examples that alarmingly illustrate most of us have at least some exposure to the shadow banking system.

The risks of the shadow banking system are a result of both the interconnected nature of loans and the unmonitored use of leverage. Shadow banks can fund loans through investor capital (hedge funds, private equity, bank loans, etc.), traditional long-term financing, or even through short-term loans. The most likely causes of systemic risks stem from OFIs’ potential inability to gain access to short-term funding. OFIs, as opposed to traditional banks, don’t have the luxury of government-guaranteed deposits, creating an environment more susceptible to short-term liquidity issues. The most common form of short-term funding for OFIs comes from the over $13.3 trillion repo-market (daily volume in Europe, Japan and US). As defined by the Wall Street Journal: "A repurchase agreement, or repo, functions as a short-term loan backed by collateral—usually a US government bond. The borrower gets cash by agreeing to sell the bond to another party and promising to pay it back at a slightly higher price. Often a bank will act as the middleman between money market funds lending cash and hedge funds that hold bonds." (Click here for full blog article.)

As an example, a money market mutual fund may agree to use its cash from investors to buy a treasury note from another party. The institution selling the note receives cash from the money market fund and agrees to repurchase the note back at a higher price in the near future. Often, these agreements are rolled over and kept in place much longer than the stated period. This is a two-party example known as a bilateral repo agreement. In the US, these agreements use treasuries 90% of the time as the collateral. As mentioned in the definition above, a third party (usually an investment bank) can assist in a repo transaction, creating a tri-lateral repo. Tri-lateral transactions only use treasuries as collateral 40% of the time, making the quality of the underlying non-treasury collateral more critical and elevating risks should its value decline. But shadow banks are not the only participants in the repo market. Traditional banks also commonly use repo transactions as a source of funding. However, unlike their shadow counterparts, traditional banks are bound by stringent capital requirements.

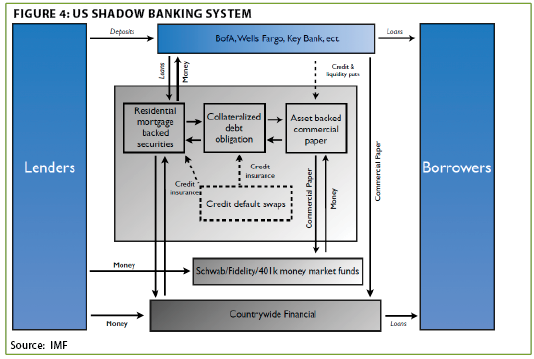

To illustrate how interconnected the banking system is today, let’s take a quick look at the 2008 financial crisis. In the years leading up to the crisis, hedge funds, investment banks, and other shadow banking institutions would buy mortgage-backed securities (MBS) and lend them in repo transactions. They would then turn around and use the borrowed funds to buy more MBS and repeat the process. In order to make MBS qualify as collateral for repo transactions, the bonds were sold with credit default swaps (CDS) representing insurance against a possible default on the underlying assets, and resulting in an AAA rating. Compounding the problem, the new owner (through the repo agreement) could also use the same security to create another repo transaction on its behalf. This increased the leverage in the system to mind-boggling levels. The process was actually quite seamless—that is, until the MBS started to do the unthinkable: decline in value. What came next was a domino-effect that started with rampant panic, followed by short-term lenders demanding cash back, culminating in a gigantic fire sale for non-government mortgage assets. The fallout eventually led to the legendary failure of Lehman Brothers, and forced the federal government to rescue the US financial system. Below is an outline from the IMF on the toxic daisy-chain based of junk mortgages and the credit default swaps (insurance) on them. I’ve again used real parties for a more relevant example.

Who’s afraid of the dark? US Treasury secretary, Jack Lew, recently said, "As regulated institutions in the United States and around the world are becoming more closely supervised, there’s been a shift of resources into institutions that are outside of the traditional banking world. Which isn’t a bad thing in and of itself, unless the risk there grows to the point that it in itself creates the risk of a systemic problem." Unfortunately, it’s impossible to know when a risk becomes a systemic problem or what the exact magnitude of the fall out will be. Developed economies make up the vast majority of the shadow banking system, and with most developed economies in zero interest rate environments, massive sums have chased higher yields. If we learn just one thing from the 2008 financial crisis, it should be that the quality of collateral is incredibly important. There’s no doubt short-term funding is the lifeblood of the shadow banking industry. And when collateral is questioned, the well can dry up quickly, slamming asset prices.

Today, we have several areas of questionable collateral still being used in the system. While we may be many years off from the next banking crisis, several red flags are currently flying—and any one of them could mark the source of the next crisis.

Since the financial crisis, according to the FSB, China has seen its shadow banking system grow from a little over 2% of GDP, to a startling 25% of GDP in 2012. A large portion of the Chinese shadow banking system has grown via Chinese wealth management products. As discussed in past EVAs, Chinese bankers sell wealth management products as conservative investments that yield more than the typical deposit account. These short-term funds have been used to fuel investments in real estate and other higher-risk endeavors. Further, in the post-financial crisis world, China was also a big benefactor of new investment funds. The economy was growing at higher rate than the developed world, and the currency was all but certain to appreciate relative to the dollar. This environment set up a large "carry trade" to borrow low cost dollars and invest in China. Today, as the dollar strengthens and investment returns disappoint, if China doesn’t have sufficient resources and controls to gradually deflate the bubbles caused by its lending binge of recent years, the implications for the global financial system are enormous.

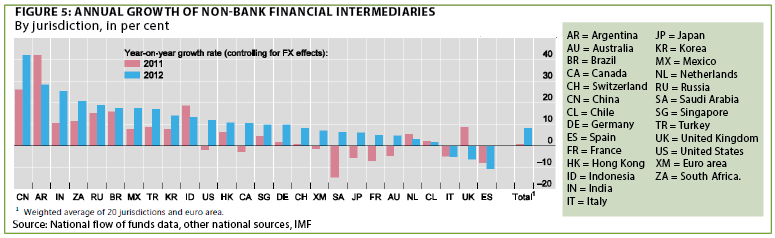

But China was not the only emerging market to see an influx of capital over the last five years. As you can see below, the countries with the fastest growing shadow banking sectors are almost all emerging markets.

Today, if we review the market environments in many of these countries, concerns mount quickly. Individually, these markets are unlikely to cause the systemic panic that could create the next crisis. Yet, collectively, and with a major push from China, an emerging market banking crisis could easily become systemic.

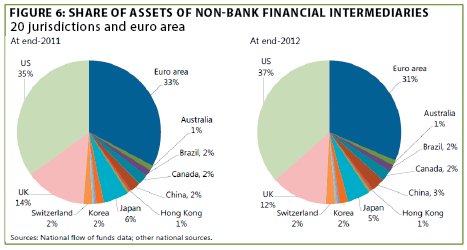

As you can see below, the FSB estimates that Europe has 31% of all global shadow banking assets. The current size of the European repo market, where mainly government bonds are used as collateral, is estimated to be €5.4 trillion (about $6.5 trillion, US). With such a large shadow banking system, the lack of stability in the European Union is a global vulnerability. And today, with several European economies on the verge of recession, it needs to be closely monitored. In 2012, fears of government bond defaults surrounding peripheral European countries threatened the stability of the global banking system. As unrest continues to rise in countries throughout Europe, so will fears about the shadow banking system’s health.

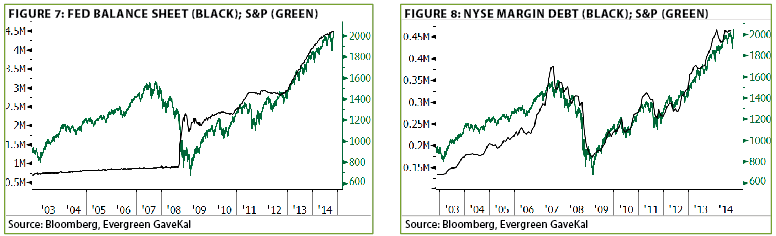

Although less concerning than others mentioned above, there are still several threats to stability in the US. Declining oil prices could slow the expansion of the US energy industry, and OFIs have surely funded long-term investments for building out the necessary infrastructure. Due to the size of the recent investments in the sector, unexpected defaults would be more than enough to create some panic. Further, US equity valuations must also be included in the list of potential culprits, as the market rally has been debt-fueled as evidenced by record-high margin balances. As the Fed prepares to raise rates, a sharp decline in the market has to at least be considered a threat. We have shown the two charts below in the past, which clearly support the correlation between increased debt and asset prices. A rapid and disorderly unwind could create a system-wide margin call with dramatic implications throughout markets.

In 2013, Ben Bernanke said, "As more assets have shifted to the shadow banking system, shocks of one kind or another are inevitable, so identifying and addressing vulnerabilities is key to ensuring that the financial system overall is robust." At Evergreen, we spend countless hours identifying vulnerabilities within the financial system. Most of our concerns will never grow into a systemic problem, but it’s important to remember that the next shock could be just around the corner. And as valuations continue to be stretched, the ultimate decline will only become more extreme. The next financial crisis is not likely to be sparked by US mortgage debt, but it’s very likely to include short-term funding issues, collateral concerns, and other forms of securitization troubles. We can’t predict when the next crisis will occur, and we don’t know the catalyst for the panic. But in today’s environment, with the Chinese government bailing out shadow banks, several emerging markets on the verge of default, extremely elevated US asset valuations, rising geopolitical tensions, and a sinking Europe, it would be foolish to recommend anything other than a defensively positioned portfolio. After all, who knows what else may be lurking in the shadows?

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.