“When we look at the high-income economies…we must recognize that they are in a truly extraordinary state. The best way to describe it is as a managed depression.”

- Martin Wolf, Chief Economics Commentator for the Financial Times

POINTS TO PONDER

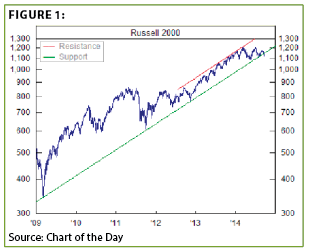

1. A number of EVAs from 2013, and earlier this year, warned about inflated small-cap valuations. As usual, they continued to rise. Since last spring, however, gravity has definitely set in, leaving smaller shares down 11.5%, in stark contrast to the large-cap driven S&P 500’s 3% gain. Moreover, Mauldin Economics’ Tony Sagami has noted, as have others, that the small-cap index is trading at over fifty times operating earnings.* (See Figure 1.)

2. The S&P 500 celebrated last Friday’s jobs number by rising 20 points (roughly 1%, equivalent to about 170 Dow points). Yet, once again, it was a case of less than meets the eye. The percentage of the US population employed actually declined to 59%. Incredibly, this is below the 59.4% reading seen as the recession ended in 2009 (the more closely followed participation rate also fell for the second month in a row to just 62.7%). Average hourly earnings advanced by a paltry 2% year-over-year, flat in real terms.

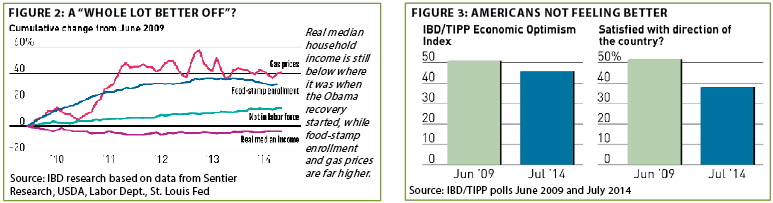

3. Many on Wall Street believe that US stocks are in the midst of a secular (long-term) bull market. However, Evergreen contends that truly sustainable up-cycles require a swelling sense of societal well-being. Yet, the percentage of Americans optimistic about the economy and satisfied with the direction of the country is lower than when the Great Recession was ending, perhaps directly related to the aforementioned abysmal employment ratio. (See Figures 2 and 3.)

*Inexplicably, the keepers of the Russell 2000 index exclude companies losing money; they also reduce P/Es over 30 down to that level in their calculation of the aggregate small cap P/E.

4. Fed chair Janet Yellen has said the majority of Americans would have to sell assets or borrow in order to pay an unexpected expense of just $400. Along the same lines, the Employee Benefit Research Institute noted that nearly three-quarters of participants in employer-sponsored plans have balances of less than $1000.

5. Gasoline futures plunged 20 cents in just two days last month and have continued to fall. They are now down 58 cents from their peak earlier this year, creating a $75.4 billion windfall for US consumers and helping to offset the long-entrenched pattern of stagnant, and even falling, incomes.

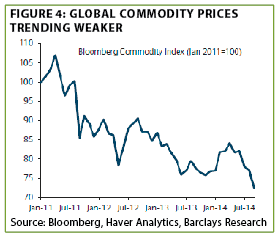

6. This author has to admit that he never dreamed commodities would be so weak in an era of central bank money creation gone viral. The 30% bear market in the Bloomberg Commodity Index since 2011, plus the further collapse in global interest rates this year, seem to indicate the world has a serious growth problem, notwithstanding the monetary deluge. (See Figure 4.)

7. The Canadian dollar continues to be, like most currencies, a weakling versus the omnipotent greenback. Currency weakness tends to be self-correcting, however, as it leads to improving terms of trade. Accordingly, Canada’s trade surplus recently hit a six-year high.

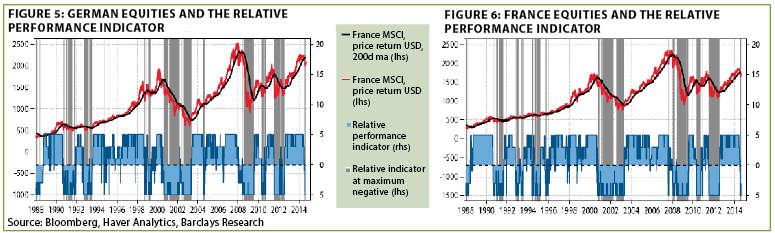

8. GaveKal Research’s proprietary relative performance indicators for the German and French stock markets recently touched its maximum negative threshold of -5. The previous 3 times this signal was produced eurozone shares cratered 33%, 50%, and 33%, respectively.

9. Bulls on the US stock market like to point out high cash holdings in America. Businesses and households in Japan, though, are sitting on a cash mountain that equals 225% of GDP, far more relative to the size of their economy than in the US. This immense reserve has not prevented either Japan’s economy or its stock market from virtually flat-lining over the past two decades.

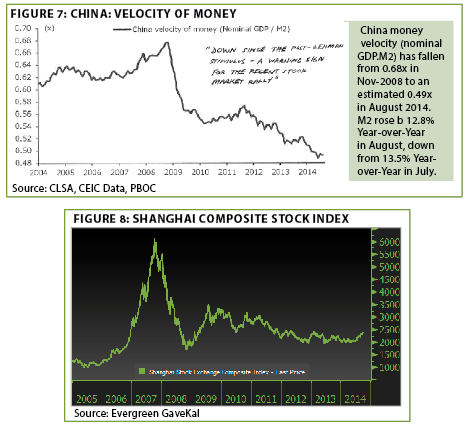

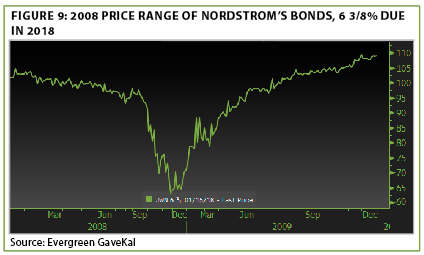

10. The collapse in US money velocity since the Fed started its $3.5 trillion print-a-thon has been a repeated focus of this newsletter. Much less well-known is that China’s money velocity has experienced a multi-year plunge that eerily resembles its stock market performance. (See Figures 7 and 8 on the next page.)

THE EVERGREEN EXCHANGE

By Jeff Eulberg, David Hay and Tyler Hay

When in doubt, don’t. Harry Truman famously quipped about wanting a one-armed economist, having tired of his advisors constantly saying, ‘’On the one hand, this" and "On the other hand, that.’’ Today, you’d be hard-pressed to find an economist requiring a second hand to discuss whether the world is currently in the midst of the greatest monetary experiment ever coordinated. The eventual results of the experiment can be debated, but the fact that we are in uncharted waters is undeniable. In our EVA publications we’ve repeatedly highlighted the extreme measures that the world’s central bankers have taken to stabilize their local economies. The US Federal Reserve’s balance sheet has grown from $800 million to a mind-boggling $4.45 trillion in just 6 years. Accordingly, it’s hard to understand why there isn’t more uncertainty being priced into the US markets. The only explanation that seems to make sense is that the global balance sheet expansion is so enormous that it‘s difficult for some investors to comprehend. The sheer size of the money multiplication has meant that, at least for the past few years, the old adage of not fighting the Fed has been affirmed. Yet, any experiment by definition has an unsure outcome, so is it wise to dismiss the potentially disastrous outcomes of this current monetary adventure? Looking at US valuations today, assets are clearly priced as if failure in this experiment is impossible, but we think a contrarian view is warranted.

The brilliant central bankers have their beliefs supported by models and years of intense study. The illustrious hedge fund managers, and macroeconomic experts, who oppose the central bankers, have similarly compelling arguments coupled with years of real world investment experience. Because we’re in the middle of a learn-by-doing monetary experiment, it’s reasonable to assume that there will be times when the central bankers appear in control (see 2011-2014). But conversely, there will also be times when markets question them, a condition that may be evolving right now.

Put simply, there are two ways this monetary experiment can play out. In the positive scenario, the powers and sagacity of central bankers are proven right and global markets recover with minimal negative repercussions. On the other hand (nod to Truman), if the Fed’s models aren’t as effective as hyped hoped, the central bank experiment could fail, leading to varying degrees

of economic deterioration. As asset managers, it is our job to gauge the risk levels of these variables. We monitor many different signals throughout the global economy and attempt to outline several in the pages of EVA. Internally, we’re constantly weighing these concerns and adjusting our client’s allocations and investments. Loyal EVA readers know that we often see many reasons for caution. However, today, there are an increasingly high number of disturbing alarms going off!

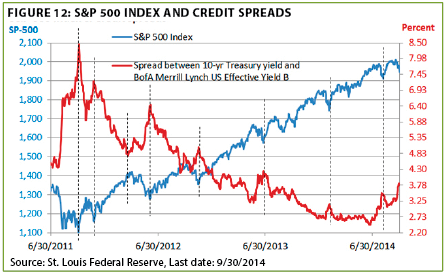

As Dave mentions in his must-read piece this week (see next page), spread-widening has historically led to periods of market instability. Dave once again notes the groundbreaking study by former senior Fed luminary Jeremy Stein, about how even a relatively mild expansion in spreads has historically been a serious drag on future growth. Though spread widening has not yet hit the danger zone, the trend is concerning.

Commodities prices, which are often incorporated into leading economic indicator models, were down close to 10% over the 3rd quarter. Specifically, copper and oil (both key indicators of global growth) are off from current highs by 7% and 21%, respectively. As noted in the Points to Ponder section, commodities are clearly in a bear market.

Europe, which according to the World Bank is collectively the world’s largest economy, continues to see its economic data significantly deteriorate. So much so, they’ve recently started their own monetary experiment, hoping to spark growth and stave off deflation. In spite of the new effort by the European Central Bank (ECB), this week the IMF increased Europe’s recession probability to over 38%, up from a 20% likelihood just six months ago. European equity markets are actually down since the ECB announcement, causing market participants to beg the ECB to do more, but unfortunately for the bulls in Europe, Germany may have tied one hand behind the ECB’s back.

On the other side of the planet, China, the world’s second largest economy, is experiencing a slowdown from its rapid expansion phase. In the last Evergreen Exchange, Dave highlighted the plunging value of Chinese real estate and its potential effect on the global economy (click here). Also, in another effort to spark growth, Japan, the world’s fourth largest economy, is experimenting with massive monetary stimulus on a scale that makes the Fed look timid. A gauge we use to track economic progress is the Citi Economic Surprise Index, measuring data surprises relative to market expectations. Unfortunately, the index is deep in negative territory for both China and Japan.

For the time being, the US economy once again appears to be the cleanest shirt in the metaphorical dirty laundry bin. However, with S&P 500 companies earning close to 50% of sales from outside the US, firms within the index will likely struggle to meet lofty expectations as other large economies stumble. Not to mention, the US dollar, still the ultimate risk-off currency, has appreciated over 8% since its low point in May. This makes American goods more expensive abroad, thus rendering US companies less competitive on a global basis. Given the proportion of sales abroad, this could be a key catalyst for lower sales, or lower profit margins ahead. In global equities, we’re already starting to see cracks in forward earnings estimates. As pointed out by GaveKal Capital, 75% of companies in the MSCI Global Index have had their earnings estimates lowered over the past month. If the aforementioned trends continue, estimates for US companies will very likely follow the global path. Furthermore, signals like the significant small-cap under performance to the S&P (down 7% for the year while the S&P is up 6%), the steady rise in the volatility index, along with the deteriorating breadth of US markets, are items that need to be monitored. While the US shirt may be the cleanest one for now, the overall filth in the laundry room will eventually soil all of them.

In such a short piece, it’s difficult to list all of the concerning elements in today’s market landscape. I haven’t even touched on—and it’s definitely not due to lack of importance—the myriad geopolitical concerns in the Middle East, Ukraine, and Asia. Due to space considerations, I also didn’t have room to discuss the increasing tension between France and Germany, or the lofty valuation metrics seen in many US asset classes (I know, you’ve heard it before!).

It’s important to remember that any experiment sets out to validate an initial hypothesis as fact. In today’s global central banking experiment, only time will tell which hypothesis is correct. All of these disturbing signals I’ve highlighted could very well stabilize and markets might revert back to a risk-on phase. Still, ignoring the extreme number of red flags currently being raised is a risky game to play. In the past, and very likely again in the future, believing that central banks were able to make those dangerous words "this time is different" a truism, instead of a trap, has led many investors to misallocate capital. However, this time is different—at least from the standpoint of unparalleled central bank experimentation. If you place all your chips on one unproven hypothesis or the other, then I fear you’re likely to bear the brunt of the next down-cycle. I suggest monitoring the signals, and being ready to adjust as the experiment plays out in real time—especially since the ultimate outcome might be anything but real fine.

The Spread’s the Thing, redux. Years ago, during the most intense phase of the global financial panic, I expressed the opinion that one aspect which made the calamity so severe was the almost incomprehensible blow-out in credit spreads. Rather than describe this in writing, as I have done countless times in the past, I thought a simple graph would drive home the point much more powerfully.

In many client—and potential client—conversations since that time, I have used this example to explain why Evergreen-managed income accounts declined sharply in the months immediately after Lehman collapsed, even though we were very conservatively positioned. There simply was no place to hide, other than cash and government bonds, during what was, unquestionably, the greatest global margin call this side of 1929.

Frankly, I don’t think most people appreciate what happened during that panic-stricken era. What drove this disbelief home to me was when we pulled up the Nordstrom’s bond chart in a recent Evergreen Investment Team meeting. Even though my crew has heard me repeatedly describe its implosion, I could tell by the shocked looks on their faces that seeing truly is believing.

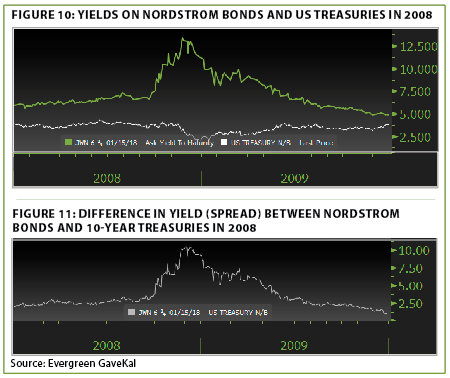

What made its price crash all the more extraordinary was the concurrent government bond yield collapse back in late 2008. As you can see below, the yield on the 10-year treasury bond was falling as fast as stock prices were in those days.

As a result of these two opposing moves in market interest rates, the "spread" in yield between the 10-year treasury and the similar maturity Nordy’s bond rocketed from a normal pre-crisis 250 basis points to a stunning 1070 basis points by October of 2008 (i.e, the yield differential rose by over 8%). And this was on an investment grade (i.e, low-risk) obligation!

Because this type of grisly carnage was occurring throughout the financial markets, I wrote almost incessantly in late 2008 and early 2009 that the Fed and the Treasury needed to reduce credit spreads. As I’ve noted before, I prescribed the issuance of $1 trillion in government bonds (note: I did not suggest printing money) to buy up vast quantities of these absurdly depressed high-quality income securities. There is little doubt this would have triggered a massive rally in the corporate credit markets, as well as equally enormous gains for US taxpayers.

In the days before QE1, my proposal was regarded as outlandish. However, the Fed soon launched its first quantitative easing (QE) program by creating $1 trillion of digital money (called reserves), using the proceeds to acquire government bonds and federally-guaranteed mortgage. Since these were the most over-priced debt securities at the time, it seemed to me a huge missed opportunity. Nevertheless, eventually, after months and months of horrific damage done to the global economy and the financial markets, the added liquidity began to turn things around, however inefficiently.

It was also my belief in those days that, once credit spreads started falling, both stocks and corporate income securities would go ballistic. In fact, I further suggested credit spreads coming down from such incomprehensibly high levels would be akin to the plunge in overall interest rates that provided the rocket fuel for the 1982 bull market lift-off. Now, let’s think about what’s happening today.

As indicated in last week’s EVA, credit spreads have recently broken above their well-established downtrend since stocks troughed in August of 2011. So far, they have not come close to spiking as much as they did in the summer of 2011 which, as you can see, coincided with the near 20% bungee-jump by stocks. Please also observe that the nearly one-fifth value wipe-out three years ago occurred in just two weeks! Of course, as we all know, such sudden declines have gone the way of the VCR (and sound-dollar policies).

You may be wondering why credit spreads have such a mega-impact on financial markets. Well, first of all, they affect much more than just asset prices. Several EVAs earlier this year summarized the seminal study by former senior Fed official Jeremy Stein who found that a 50 bps (0.5%) pop by BBB-rated credit spreads over a fairly short time frame (like six months) causes a 2% drop in GDP. Thus, far they are up only 25 basis points (0.25%) but their direction is clearly higher and wider.

Then, there is the issue that credit spreads are a real-time reflection of risk-appetites. When they rapidly expand, as they have since August, it sends an unmistakable message that broad "de-risking" is underway. Compounding this is that we’ve had so many years of tranquil financial markets and steadily falling spreads. This has encouraged hedge funds and other aggressive market participants to take on short-term debt to finance the purchase of yield instruments that carry a positive spread (there’s that key word again). Astute readers will recognize this as the famous, or infamous, "carry trade."

Further aggravating this situation, the market-based short-term cost of money has jumped even though the Fed has not actually raised its benchmark rate. The increase hasn’t been material, but with many institutional players levered ten times or more, it doesn’t take much of a rate rise to create serious problems. Finally, widening credit spreads automatically means that yield securities are falling in value (assuming US treasury rates are stable or rising, which has been the case lately), further pressuring the gunslinger borrow-short/invest-long community.

In other words, all those who have gotten carried away playing the carry trade, are suddenly in a world of hurt. If spreads come in—and stay in—then this will be just another false alarm (the kind I’ve been repeatedly hearing for the past year or more). But if there is a true reversal at hand, it soon will be all hands on deck as highly levered investors frantically try to save their ships.

![]()

Umbrella politics, sunny values. Almost twenty years ago, my parents returned from a charity auction and announced that they’d bought a family trip to Hong Kong. It seemed odd to me at the time, but anyone who’s attended a charity auction has witnessed first hand alcohol’s effect on decision-making. So, in 1996, we traveled to Hong Kong and found an amazing city nervously holding its breath as it prepared to change hands.

Originally "colonized" by Britain, it had been leased for 99 years from China. On July 1, 1997, it was returning to Chinese control. Under an agreement struck between Britain and China, Hong Kong, at time of transfer, would become a Special Administrative Region. This meant that there would be "one country but two systems." China would leave Hong Kong to govern itself and maintain its sovereignty while being "protected" militarily by China.

Operating as a British colony for almost the entire 20th century allowed the tiny island to become the financial epicenter of Southeast Asia under the tutelage of western financial practices. It’s home to one of the world’s busiest ports and its enviable commercial position made the Chinese keen to absorb such a valuable asset. Coming under China’s command in 1997 was a huge unknown and now, 17 years later, many Hong Kong residents find themselves back in a tenuous situation, as China’s influence has become too intense for comfort.

The recent protests in Hong Kong occurred as citizens felt the People’s Republic of China (PRC) was beginning to waver from its previously more hands-off approach. Hong Kong doesn’t use the title of mayor or governor. Instead the city’s leader is known as the Chief Executive Officer, a nod to the business-oriented culture on which the city prides itself. The current CEO is a man named CY Leung, who will leave office in 2017. He and all of his predecessors are considered pro-Beijing puppets who facilitate the agenda of the Chinese government. The recent protests were specifically an objection to the process of naming Leung’s successor. Citizens of Hong Kong had been promised autonomy but the PRC has started to show signs that they will have complete control over the candidacy process.

While the 2017 election is the current hot button, a deadline that looms more ominous is 2047. Although this date seems almost too distant to type on my screen, it is likely to have even more profound consequences. Hong Kong will give up its Special Administrative Region (SAR) status and be subject to the same rules as the mainland. That’s 34 years away, but it’s likely to reach a boiling point far sooner. I think there are really only two end-game scenarios for Hong Kong as the clock ticks on their status as a SAR and both have significant risks. Either China caves and allows Hong Kong to remain under the "one country, two system" model indefinitely or it forcibly assimilate Hong Kong under Chinese rule. In the latter scenario, Hong Kong protestors are likely to be squashed by pro-Beijing military forces, producing a horrific repeat of Tiananmen Square. Under the first scenario, can China realistically risk allowing a full-scale rejection of this agreement by the people of Hong Kong? What message would that send to Chinese citizens on the mainland?

Consequently, China is walking a dangerous tight rope. Despite the government’s best efforts to suppress coverage, people all over China are watching (or trying to) what’s happening in Hong Kong. China’s fragile social "contract" with its people is at risk. People live without any real freedom in "exchange" for full employment, rising real income, and improving infrastructure. Rampant corruption and smothering pollution are already putting officials in the crosshairs, many of whom have been incarcerated or summarily "terminated" (and I don’t just mean fired!). If authorities bend on Hong Kong, it would seriously undermine the government’s control over its mainland people. A brief analysis of historical dictatorships would suggest that losing control over the teening masses is quite detrimental to the health of the installed leadership.

Shaky politics and a laundry list of economic headwinds have dogged the country in recent years causing the investment world to leave China for dead. It’s true that GDP has cooled from a scorching 10% clip to around 7-8% causing investors to question its growth prospects. While I am the first to admit that the political situation will likely get worse before it gets better, the region offers an interesting risk/reward tradeoff from an investment perspective. Chinese and Hong Kong stock markets are trading at their biggest discount to US stocks in 13 years. Any further political scuffling is likely to push the markets to even larger discounts. Yet, it wasn’t long ago that every client or prospective client asked us how we planned to "play" China. Today, bringing up China is a meeting buzzkill.

It seems obvious that things don’t stay in a state of disequilibrium for long periods of time but, for now, Hong Kong remains stuck with one foot in the democracies of the west and another in the totalitarian state that is China. Can China slowly progress away from the tenents of communism toward a more democratic state? And, can it do this without losing complete control of the economic and political situation? I think most would conclude that to be a very tricky transition at best. But the volatility will likely create compelling investment opportunities at times.

The region’s wealth has been growing at a staggering clip. According to a study by the Boston Consulting Group, the number of Chinese millionaires in 2009 was 500,000 and, by 2013, it was over 2.5 million, a 500% increase. Unfortunately, these millionaires aren’t sticking around. Paul Krake points out in his excellent October 6th research piece, View From the Peak, that 60% of all wealthy Chinese already have either emigrated to another country or plan to do so—not exactly a ringing endorsement of the political backdrop! But such negatives are definitely priced into Chinese stocks. In 1998, just one year after the Hong Kong handover, The Shanghai Composite traded at almost a 50% premium to US stocks; today it trades at a 50% discount! It’s tempting to confuse the political landscape with the investing backdrop, but history has shown it’s not as crazy as it seems to be long the markets but short the politics. After all, the US stock market has been on a tear in recent years even though the political climate in Washington D.C. has made the Gobi desert seem hospitable. The world faces some major challenges in the years ahead, as does China, but at least its stock prices reflect the risks, unlike another market much closer to home.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.