"The iconic actor Errol Flynn is reported to have quipped that his legendary financial problems lay ‘in reconciling my gross habits with my net income’. This is the most concise description I can marshal to explain the problem plaguing our nation’s fiscal authorities."

-RICHARD FISHER, President of the Federal Reserve Bank of Dallas, in a speech this week to the Economic Club of New York.

POINTS TO PONDER

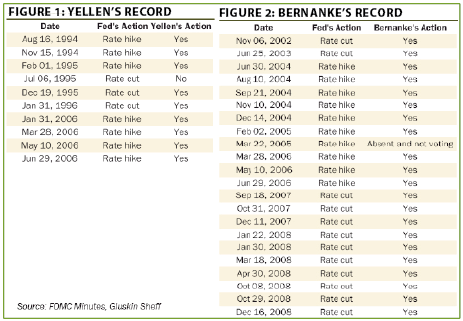

1. Largely obscured by all the melodrama over the budget brinksmanship was President Obama's nomination of Janet Yellen to become the first chairwoman of the world's most powerful central bank. This fulfills a long-standing EVA prediction that Ben Bernanke would not seek reappointment. While Ms. Yellen is widely viewed as a monetary "dove," her voting record tells a different story. (See Figures 1 and 2)

2. The productivity gains achieved by the US manufacturing sector over the last 20 years have been notable. Besides aiding the return of industrial production to the US, this also helps to keep inflation subdued.

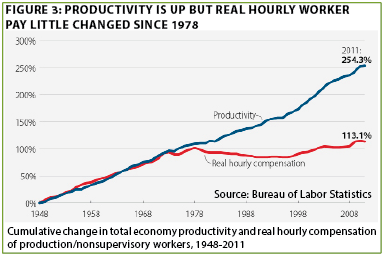

3. Increasing productivity is an extremely beneficial development for any economy. The dark side of this for the US, however, is that these efficiency gains have been at least partially achieved via a 25-year stagnation in the after-inflation compensation of American workers. (See Figure 3)

4. In another example of the US becoming an energy exporter, pipelines heading south of the border are carrying twice as much natural gas to Mexico as they did in 2010. Ironically, hydrocarbon-rich Mexico is experiencing a growing shortage of gas due to years of underinvestment in its resource base and inept management at its nationalized energy company, Pemex.

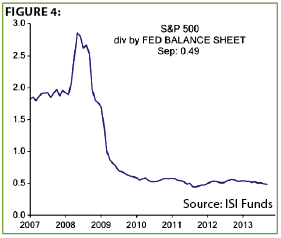

5. ISI’s rock-star economist, Ed Hyman, believes that if the Fed continues to whip up $85 billion-per- month for the rest of this quarter, as now looks nearly certain, then the S&P 500 should approach 1800 by the end of the year. Tellingly, if the S&P were deflated by the expansion of the Fed’s balance sheet, reflecting the nearly $3 trillion it has fabricated, the market would be essentially flat over the last three years. (See Figure 4)

6. Past EVAs have noted the elderly status of the present US bull market. The economy’s up-cycle is also getting rather long in the tooth at 51 months. Since WWII, the average expansion has lasted 58 months. The limp nature of this upturn, however, might allow it to last longer than normal.

7. Typically, the US labor force swells by 150,000 per month necessitating the creation of the same number of jobs to maintain a constant unemployment rate. Yet, since 2009, the work force has increased by just 20,000 per month, flattering the official jobless rate but posing a serious drag on overall GDP. This reality likely goes a long way in explaining the chronically sub-par nature of our recovery from the Great Recession (usually, the worse the downturn the stronger the rebound).

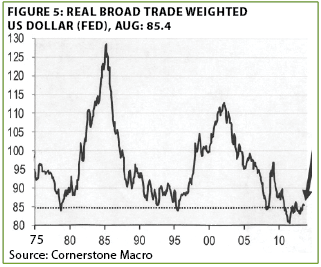

8. Should US monetary policy become less incontinent under Janet Yellen, assuming she is confirmed by the Senate, the dollar is likely to rise, particularly against those currencies that are overvalued versus the greenback. While this is not the case with most emerging market currencies, including China’s renminbi, the dollar does appear both beaten-down and bottoming-out on a broad trade-weighted basis. (See Figure 5)

9. Hopefully, US policymakers will implement serious budget reforms, especially in the wake of the latest debt-ceiling debacle. If not, our country as a whole is at risk of following in the disastrous footsteps of the US territory of Puerto Rico, where one-third of its population works for the government. Additionally, its pension system is 93% underfunded and yields on the territory’s bonds now exceed 10% on its crushing $70 billion debt burden (over $100 billion including the retirement plan shortfall). This amounts to a stunning $25,000 of indebtedness per capita.

10. Last week, the UK government launched an initial public offering (IPO) of the Royal Mail, its national postal system established in 1516 by King Henry VIII (presumably, during a hiatus between beheading wives and Sir Thomas More). The shares rocketed 38% on their first day of trading, sparking protests about under-pricing. The contrast with the loss-plagued US Post Office is quite stark, as it’s almost inconceivable investors would place any substantial market value on America’s USPS.

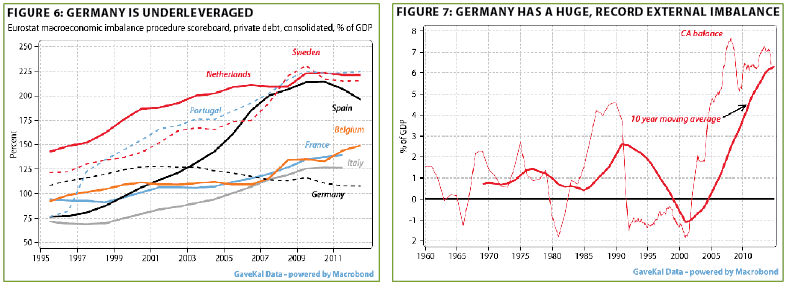

11. Another way in which Germany looks far superior to its fellow eurozone members is its low level of private sector debt. Additionally, its current account surplus remains exceedingly elevated. (See Figures 6 and 7)

12. The economic news out of Europe has definitely taken on a stronger tone in recent months. Yet, the precarious nature of the Club Med countries’ financial condition shouldn’t be overlooked. Spain, for example, has resorted to borrowing from its version of the social security trust to issue pension checks. Moreover, 97% of its national retirement fund is invested in its own government debt which may default or need to be restructured at some point.

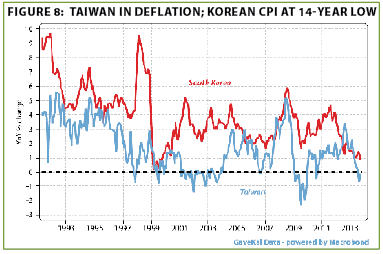

13. Official inflation measures in the US are subdued (with many questioning their accuracy), but in much of Asia actual deflation is not far off. In Japan, Korea, South Korea, Thailand, and the Philippines core CPI is up a mere 0.8% year-over-year while Taiwan is seeing actual price declines. (See Figure 8)

14. China, like all countries, confronts a host of challenges, but at least its stock market reflects the risks. It recently traded at 8.7 times 2013 earnings estimates versus a 12.4 long-term average.

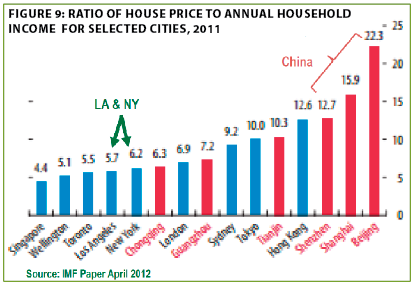

15. Dramatically highlighting the extent of the property market inflation (dare I say "bubble"?) in Beijing, its homes are three times less affordable, relative to household income, compared to New York City. Suffice to say, the Big Apple has never been known for a reasonable cost of living. (See Figure 9)

Ceiling or sun-roof?

Now that the debt ceiling has been raised for the 78th time in the last 50 years, it’s safe to say the stock market has an all-clear to resume its dizzying ascent, right? After all, this was the only thing that was holding back share prices lately, given accelerating economic growth, vibrant earnings reports, the fading of the oft-dangerous month of October into the rear view mirror, and, of course, the near certainty that the Fed is poised to maintain its $1 trillion dollar per year print-a-thon. Well, at least some of the above is true, and we won’t quibble with the view that the path of least resistance for stocks continues to be north.

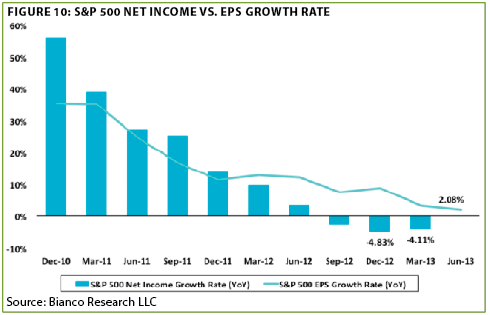

The budget "deliberations," if that is what you can call a process that is so deliberately absurd, have become such an obsession for the markets and the financial media that other issues have faded almost to black. For instance, the economic data has been anything but scintillating with the IMF having just reduced its global growth forecast, for 2013 and 2014, once again. Meanwhile, US corporate profits, excluding share buybacks, have actually turned negative. (See Figure 10)

Remarkably, even the news of Janet Yellen’s nomination to replace Ben Bernanke has been relegated to also-ran status. To the extent that it is discussed, the comfortable consensus view is that she is congenitally even more "dovish" than her soon to be ex-boss. Ergo, she will be the last person to stop the QE presses. However, as noted in Point to Ponder 1, Ms. Yellen’s past voting track record on easing and tightening is not consistent with her uber-dove rap sheet.

Between now and the end of the year, though, there’s little chance of Fed tapering, especially given the near-term hit to already anemic growth caused by the government shutdown. Thus, with the monetary fire hose still gushing as if a five-alarm fire continues to blaze (which, in economic terms, should be reserved only for recessions bordering on depressions), stocks will remain awash in liquidity. The calendar is also supportive as we head into the typically market-friendly Holiday Season.

Frankly, the Evergreen plan was to up our equity exposure a bit, on a tactical basis, if we saw the type of stock market air pocket that so frequently characterizes October. While it could still happen, that’s looking less and less likely. In fact, each dip seems to be shallower than the one before it, possibly because investors have adopted the Pavlovian attitude that the Fed is there to feed them whenever the market’s opening bell rings (paraphrasing Warren Buffett’s observation during the tech bubble).

Thus, we believe it’s probable that this bull will continue to romp and stomp, at least through year-end.

So, why not climb on and enjoy the fun?

Requiem for a bull market.

No American wrote as poignantly about the drama of a genuine Spanish bull fight as did Ernest Hemingway. Even though you know that it’s always going to end badly, at least for the bull, Hemingway captured the nobility and the futility of the fight-to-the-death struggle brilliantly. As most of us remember from our high school "lit" classes, the bloody denouement can be a drawn out affair and, of course, sometimes the matador draws the sharp end of the horn.

In reality, the same is true of a financial bull market: they always succumb in the end. Yet, this unavoidable fact is constantly overlooked, typically when it should be most considered—such as when the bull has been defying the longevity odds.

As observed several times in EVAs over the last few months, bull markets have a very hard time attaining the five-year mark. Given that our current "toro" will be turning "cinco" next March, a prudent investor should really be considering when the coup de grâce is likely to be administered.

Of course, to precisely surmise the demise of our current bull is above the pay grade of mere mortals, but there are certain warnings signs, beyond just age, to indicate when the fatal thrust might be looming. One of them, ironically, is something that is often cited as a sign of strength about this market—its remarkable resilience.

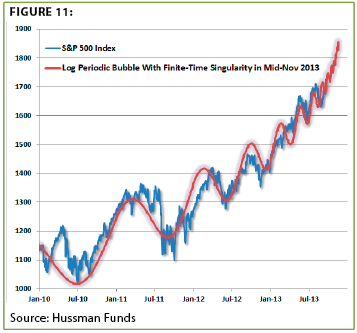

As mentioned above, the dips are becoming increasingly shallow. Yet, as the quantitative whiz John Hussman points out, such patterns are characteristic of late-stage bull markets when investors have been conditioned that all pull-backs are buying opportunities, soon to be rewarded. The following chart is one John ran based on the work of the gifted mathematician, Deidier Sornette, showing how recent market activity has displayed this high-frequency behavior. (See Figure 11)

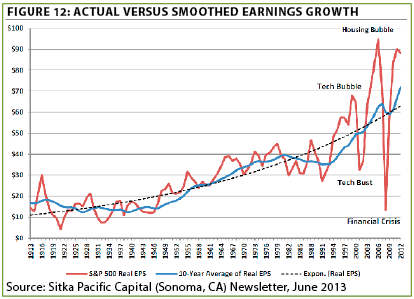

One of the other red flags is that the business cycle is becoming as superannuated as the market itself. While we are sympathetic to the view that the faltering nature of this recovery might give it a longer life span, the degree to which current corporate profits are above their long-term trend line does appear unmistakably ominous. (See Figure 12)

Next up is the issue I raised two weeks ago regarding the growing list of white-hot stocks selling at 100 times earnings or more. Interestingly, Fred Hickey, who is one of the savviest money managers extant, was quoted in this week’s Barron’s discussing the very same topic. (Thanks to Evergreen’s Rob Dainard for bringing this to my attention). Here’s what he had to say: "Just as in 2000 and again in 2007, I could fill a whole newsletter with these nonsensically priced story stocks. But by now, you should get the point. The valuations are out of control."

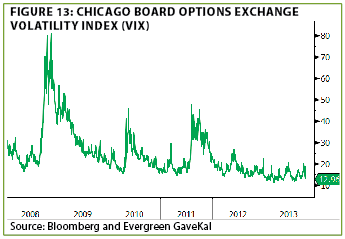

Then there’s the threat raised by the constant companion of aging bulls, investor complacency. One of the traditional measures of this is the Volatility Index, popularly known as the VIX. Even the government shutdown, and the long-shot potential of the US defaulting on its debt, failed to materially move the needle from the subdued levels that reflect extreme nonchalance on the part of market participants. Additionally, the bull/bear ratio is heavily tilted toward the bullish attitude with the venerable Investors Intelligence poll showing 45.4% bulls versus just 20.6% bears. (See Figure 13)

The ultra-critical issue, though, is Fed policy.

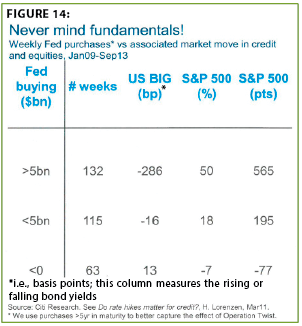

Yellen then screamin’? Normally, the truly nasty reversals of market up-cycles occur when the Fed has been tightening for a number of months and the monetary constriction begins to choke the economy. However, the last few years have been anything but normal. Thus, there may be a faster adverse reaction this time as stocks have become extraordinarily reliant upon Fed money creation, per the following table created by Citi’s Matt King. (See Figure 14)

As mentioned above, the prevailing wisdom is that Ms. Yellen will continue what the Fed prefers to call Large Scale Asset Purchases (LSAP), otherwise known in the financial media as QE, and considered by those of us with simple minds as simply printing money. Yet, another newsworthy item lost in the budget boondoggle has been the "exit interviews" given by some of the Fed doves who have been flying the coop in recent weeks. Tellingly, these individuals are admitting they were never fans of LSAPs, after all. As the old saying goes, success has a thousand fathers but failure is an orphan.

It’s my contention that as we move into 2014, LSAP, QE, money printing, or whatever you want to call it, will be increasingly relegated to orphan status. My reasoning is that there’s a growing dossier of evidence indicating it simply hasn’t worked as advertised (for one of the best overviews of this issue from an extremely erudite source, please click here.

Moreover, as expressed in prior EVAs, Ms. Yellen is one smart woman and she is acutely aware that the need to extinguish $3 trillion of the Fed’s funny money will have to happen on her watch. It’s my belief she realizes that when you’re in a chasm deep enough to make the Grand Canyon look like a drainage ditch, it’s best to shut down the excavators.

Rather than being a dove for all seasons, Ms. Yellen may rediscover her prior independent thinking streak, one that prompted her to challenge "Maestro" Greenspan in the mid-1990s and to warn Mr. Bernanke, to no avail, about both the housing bubble and an impending recession in 2007.

If so, 2014 could be a catch-up year for the corrections that should have naturally occurred over the last two years, but were inhibited by the Fed’s hyperactive printing press. Should a much deeper correction, or even quasi-crash, unfold, magnified by the long artificial suppression of volatility, you can bet Wall Street will start screaming bloody murder. But, given the multitude of warnings about excessive reliance on the Fed, it will be a case of suicide not homicide.

Special message: A decade ago, the war in Afghanistan was known as the "good war." Now, it has become the forgotten war, even though America still has tens of thousands of heroic young men and women fighting in that desolate country.

The reason I’m bringing up a subject most of us would rather ignore is an event that just occurred at the White House. You may have read that on Tuesday of this week, President Obama bestowed the Medal of Honor, our nation’s highest military award for valor, on Captain William Swenson.

Capt. Swenson earned his Medal of Honor, the first US Army officer to do so since Vietnam, through his extraordinary actions during a seven-hour gun battle in the Ganjgal Valley on September 8, 2009. Repeatedly risking his own life, Capt. Swenson rescued his fellow troops, who had been trapped by a Taliban ambush. He also re-entered the "kill zone" to recover the bodies of those who didn’t survive. In all, five American and 11 Afghan soldiers lost their lives during this battle and two dozen coalition troops were injured.

Capt. Swenson’s journey to his award ceremony on Tuesday was not an easy one. The Army managed to lose the computer file on his award nomination for 19 months. The implausibility of this has raised suspicion it was due to his criticism of superior officers in delaying air and artillery support for his ambushed unit. Fortunately, with this week’s White House ceremony, that transgression has been rectified.

Unfortunately, however, Capt. Swenson, a Seattle resident, has been enduring what he refers to as his "forced early retirement." According to the Washington Post’s David Nakamura, who has written two moving articles on his plight, Capt. Swenson has been unemployed since 2011, which brings me to the main reason for this special EVA message.

Evergreen GaveKal would like to thank Capt. Swenson, at least monetarily, for the exceptional service he has rendered to his country. We are also inviting EVA readers who feel so inclined to consider donating to a special fund we are establishing for his benefit. We are donating $5,000 to this fund and will match all contributions received up to another $5,000. If you would like to contribute toward this, please make your checks payable to Union Bank for the benefit of Capt. William Swenson in care of Evergreen GaveKal 10500 NE 8th Suite 950 Bellevue, Wash. 98004.

Given that almost 5000 individuals receive EVA, many of whom are businessmen and women in the Seattle area, my hope is that a few might consider interviewing Capt. Swenson as a job candidate. He is reportedly considering returning to the military but, should he elect not to re-enlist, having serious employment options locally is likely to mean a great deal to him. David Nakamura was kind enough to immediately respond to my email this week and is advising Capt. Swenson of the fund we are establishing, as well as the potential for job interviews.

There have been a number of media reports on his award and battlefield heroics, but in case you missed those please click here to watch. During this era of bitterly partisan politics and chronic government dysfunction, I believe it’s imperative to assist those who have truly served our nation and have done so with uncommon valor.

Thank you!

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.