Was that it? Was that the long-feared correction in the equity market and especially growth stocks? Was that just one more chance to “buy the dip” (often, with a colorful adjective added between “the” and “dip”.) In my view, a yes response is possible but not probable, despite the bounce-back by the Nasdaq this week.

The ever-popular Nasdaq, despite increasing signs of underlying stress, did put on a spirited rally from Monday’s intraday low when it was down 3% for the day. From that trough until Wednesday’s high point, the “Naz” popped by 5 ½%. Alas, that was not to last.

Yesterday’s bashing of the growth sector was not encouraging for those hoping the breakdown in high P/E stocks—those with exciting stories but often scant earnings, if any--was in the rear-view mirror. Unlike during last week’s drubbing, rising treasury rates were not the culprit. Bond yields have been stable in recent days. There appears to be a very strong bid pinning the yield at a high of around 1.75%.

Rising interest rates are typically tough on the most highly valued inflated stocks. But rates were mostly on the soft to flattish side since last spring which is when a significant numbers of growth stocks began to hit the wall. While the Nasdaq is still up a respectable 15% since the start of 2021 (i.e., over the last 54 weeks), the far more numerous smaller constituents have been sucking wind.

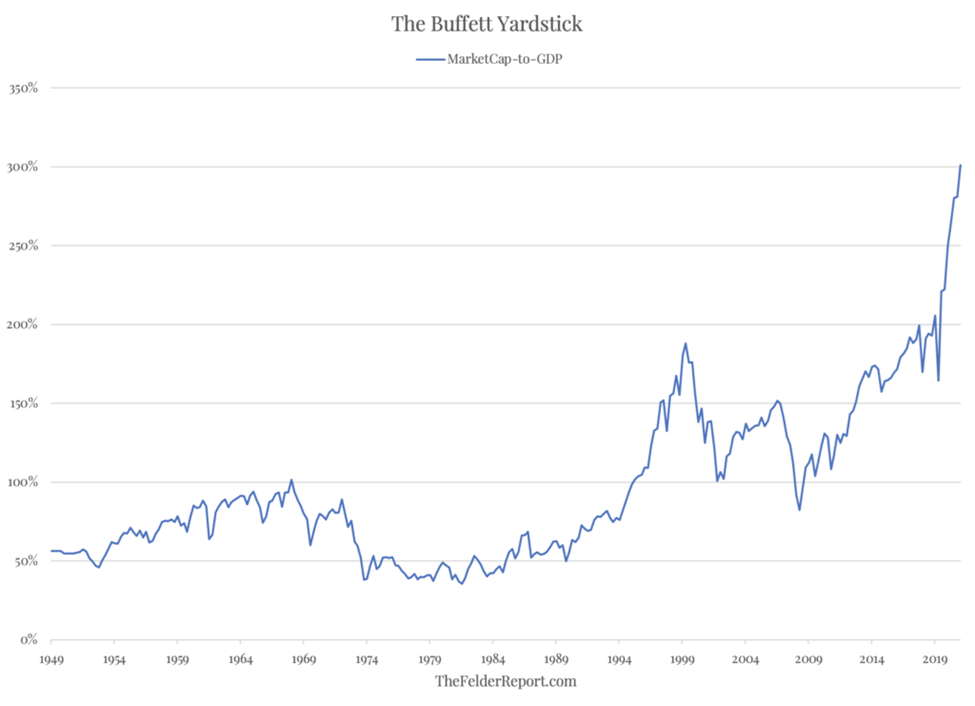

As Jeff Dicks pointed out in his Chartbook EVA, around 40% of Nasdaq stocks are down more than 50% from their 2021 highs. 57% have retreated at least 30%. Two-thirds have eased by 20% or more. Even last year when the Nasdaq was up roughly 20%, the Russell 2000 Growth Index, made up of small cap companies, inched ahead up a mere 2 ½%. 2022 has not started out favorably for small cap growth as it has slid 9%. Thus, its 54-week return has been minus 6 ½%. That, good readers, is not the sign of a healthy market. Another warning flag snapping vigorously in the breeze is The Index of The Volume of Speculation from my friend and regular email buddy, Jesse Felder. It’s also not a bad idea to do a refresh on the current total market value of US stocks relative to size of the economy, or GDP. This is often referred to as the Buffett Indictor or Yardstick because it has long been one of the Oracle of Omaha’s favorite measures of market under- or over-valuation. Personally, I prefer the price-to-sales ratio which actually has a better predictive record of very long-term future returns, like over the next decade. Regardless, both of these metrics are saying the same thing: it’s an incredibly frothy market right now. But, of course, it has been for a very long time.

On the positive side, most of these excesses are a function of the aforementioned hyper-growth stocks that, in many cases, continue to trade extremely expensively. This is despite that a long list of them have experienced two-for-one splits but without the additional shares. (Yes, that means they’ve been cut in half.) On the other hand, “old economy” shares remain generally reasonably priced with some pockets of fairly eye-opening bargains. It’s no secret to any regular reader that we’ve been pounding the table on the energy sector for over a year. After an outstanding 2021, it’s up another 11% already this year. Mid-stream energy issues (MLPs) have also tacked on another 6 ½% to what was a boffo 2021. Energy is essentially the inverse of the crazy over-priced go-go stocks: it’s up a lot but still stunningly cheap vs down a bunch but still outrageously pricey (with some notable exceptions).

As I’ve previously observed, including last week, the only other market I’ve seen behave this way was in 2000 when the tech wreck back then began in March and the S&P 500 was still actually up 3½% for the year by September thanks to resiliency in several large cap names. The Nifty Fifty market of the early 1970s might also qualify but even I’m not old enough to have been in the business at that time. (However, I was buying stocks; my first was Boeing in 1971 when the billboards around my hometown said: “Will the last person leaving Seattle please turn out the lights?” Once a contrarian, always a contrarian.)

Another expression of how exceedingly expensive the Nasdaq titans have become is also from Jesse Felder, relayed in turn from small cap stock maestro Eric Cinnamond. The top five names—Apple, Microsoft, Amazon, Tesla, and Google—trade at 46 times free cash flow* or 57 times if you adjust for stock-based compensation. No doubt this is skewed by the low profit profile of TSLA but even Apple, Microsoft and Google, which traded inexpensively for many years, are now heroically valued. Evergreen believes retaining a core position in those three, plus Amazon, is reasonable based on their exceptional businesses and profitability. However, even with those superstars doing some profit-taking (there’s that controversial phrase again!) is appropriate, particularly if they have become a disproportionately large part of your portfolio.

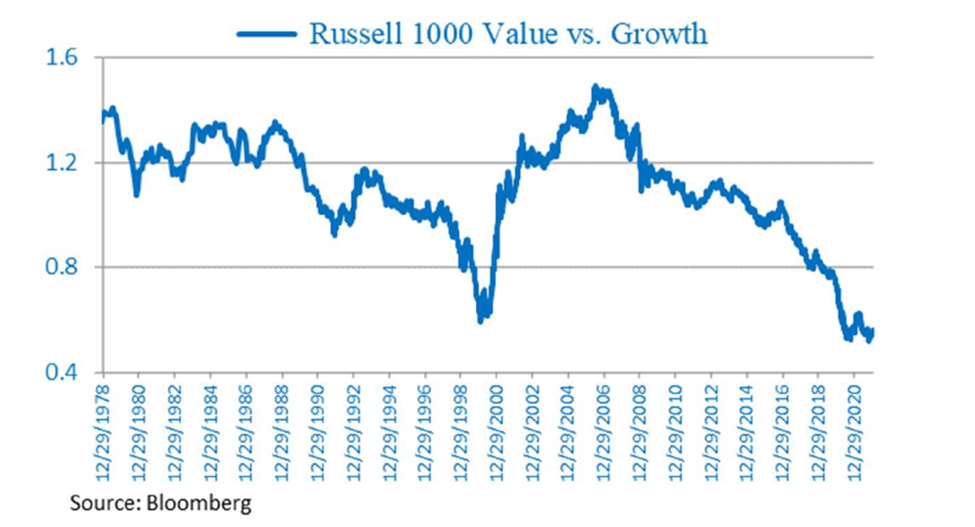

Based on the seemingly endless lag of value shares relative to growth, Evergreen thinks this performance inversion we’ve seen recently has much further to run. This week JP Morgan CEO Jamie Dimon gave an interview in which he stated he expects a strong economy in 2022. Having worked with him for years back in the 1990s, I’ve long been a fan of his and I think he’s spot-on with his outlook. If he’s right, that creates a highly supportive backdrop for cyclical stocks, which almost always have a value bent. While they aren’t as cheap as they were when I was touting them after the initial Omicron scare, there are still a number of issues that offer attractive risk rewards.

One of the most out-of-favor sub-sectors continues to be precious metals miners. While they have failed to mount a meaningful rally, they do appear to be stabilizing. Again, stay patient. The US dollar looks to be softening and if it comes down as much as I think it will over the course of this year, the miners should reprise their explosive 2020 rally.

*Free cash flow is often thought to be a superior measure of a company’s profitability than earnings per share. The latter is frequently manipulated to inflate profits. Free cash flow is essentially the cash a company generates after accounting for the capital spending needed to sustain and grown its operations.

Positioning Recommendations

For EVA readers who acted on our recommendation to buy into the mid-stream energy sub-sector (MLPs) during the Omicron weakness, cashing in some of the gains may be advisable. MLPs often sell off in November and December, partially due to tax-selling pressure. Late last year, that was triggered by the Black Friday Omicron news. Often the tax-related rally peters out in January. However, this group continues to provide excellent payouts to investors and its fundamental outlook may be the best it has been in its history. Free cash flow is abundant and growing, allowing both debt paydown and share repurchases. Spreading energy shortages also highlight the value of in-place pipelines which are becoming increasingly difficult to replicate. Accordingly, this is definitely just a tactical trim recommendation and we are keeping mid-stream energy in our Likes section.

LIKE

NEUTRAL

While it is difficult to hold cash during a time when inflation is eroding its value at a 7% annual clip, such as now, it becomes a very valuable asset during market dislocations. It’s critical, though, to deploy it when those happen such as the recent Omicron event, the Delta-driven sell off in cyclical stocks last summer, and, of course, the greatest buying opportunity of the last thirteen years, during the March 2020 pandemic panic. Sadly, far too many investors do the opposite—selling stocks and raising cash when the headlines are apocalyptic and drawing down their cash reserves after prices have significantly recovered.

Based on the severe weakness experienced by the Reddit/WallStreetBets meme stocks such as Gamestop and AMC Entertainment, I am deemphasizing my negative stance. The former is down 20% this year already and has been cut in half since late November. The latter is off 22% in 2022 (22 in ’22!) and has tanked nearly 60% over the last two months. (In full disclosure, I have been systematically covering my personal short positions in these names as they have melted.) However, I believe they have further yet to fall over time.

DISLIKE

DISCLOSURE: This material has been distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, are subject to change, and reflect the personal opinions of David Hay (an employee of Evergreen Gavekal) as of the date of this publication. This publication does not necessarily reflect the views of Evergreen’s Investment Committee as a whole. All investment decisions for Evergreen clients are made by the Evergreen Investment Committee. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this letter have been selected to illustrate the author’s investment approach and/or market outlook and are not intended to represent Evergreen’s performance or be an indicator for how Evergreen or its clients have performed or may perform in the future. Each security discussed in this letter has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. The securities discussed herein do not represent an entire portfolio and, in the aggregate, may only represent a small percentage of a Evergreen’s client holdings. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Before making an investment decision, the reader should do their own research and/or consult with their financial advisor. Past performance is no guarantee of future results. All investments involve risk, including the loss of principal.