“This attack introduces a new, irreversible premium into the market.”

–JP Morgan analyst Christy Malek, who expects oil to surge to $80, or higher, over the next three to six months

______________________________________________________________________________________________________

In the mid-1950s, geologist M. King Hubbert theorized that “peak oil” would come when the maximum rate of extraction of petroleum was reached, after which the production of oil would enter terminal decline. At the time Hubbert first presented his theory, he predicted that US peak oil would occur around 1970. While the theory appeared accurate for many years, pessimistic prophesies on the future of oil have continued to prove false as world oil production has not only risen but hit a new all-time high in 2018.

Yet, for the better part of this decade, the narrative of “peak oil” has continued to weigh on oil prices, dragging down energy stocks along with it. If there’s any silver lining (at least for energy investors) in the aggressive attacks last weekend on Saudi Arabia oil facilities, it’s that the long-forgotten energy sector has been re-energized. At one point following the attacks, oil prices surged nearly 20% with Brent crude posting its largest intra-day gain since the Gulf War in 1991. Shares of many major energy corporations also soared on Monday.

It should come as no surprise to regular readers of Evergreen’s newsletter that the long-detested energy sector is one of our favorite corners of the market. Specifically, high-yielding energy stocks and Master Limited Partnerships (MLPs) offer seemingly rare value in an environment where securities with cash flows reminiscent of the 1990s—6% to 12—are nearly impossible to come by.

The long-term impact of last weekend’s attacks will play out over time as Saudi Arabia, the United States and other nations determine an appropriate response to the unprovoked aggression. On Wednesday, the United States announced a major increase in sanctions on Iran as Saudi Arabia presented evidence that the provocation was “unquestionably sponsored by Tehran.” As of this writing, Saudi Arabia and its allies have stopped short of counter-attacking the presumed guilty party through a show of force. However, escalating tensions in a region that has been extremely volatile for decades could continue to create waves for oil prices, energy stocks, energy-dependent companies, and consumers for the foreseeable future. On Monday, JP Morgan estimated that crude could jump by “anything between $5 and $30 in the upcoming months.”

Evergreen believes the attack may accelerate a trend that was already evident prior to this event: consolidation. Senior management teams at energy companies may now realize the urgency of acquiring geopolitically safe US oil and gas reserves and/or infrastructure assets at bargain prices.

This week, we are presenting a very informative Q&A on the Saudi oil attacks, written by Evergreen Gavekal’s esteemed partner Louis-Vincent Gave. In the pages below, Louis seeks to answer some of the week’s most pressing questions, namely:

*Evergreen note: The below article was published by Gavekal on Tuesday, September 17th. Some of the information – specifically in the section “Question #1: Why” – may be outdated as of September 20th based on recent developments. Regardless, we believe the below outlines important information for readers to consider in the week following the attack on Saudi Arabia’s oil production facility. Further, Evergreen believes a rapid return to full production at Saudi Arabia’s massive Abqaiq oil facility, while possible, is unlikely.

______________________________________________________________________________________________________

Q&A ON THE SAUDI OIL ATTACKS

By Louis-Vincent Gave

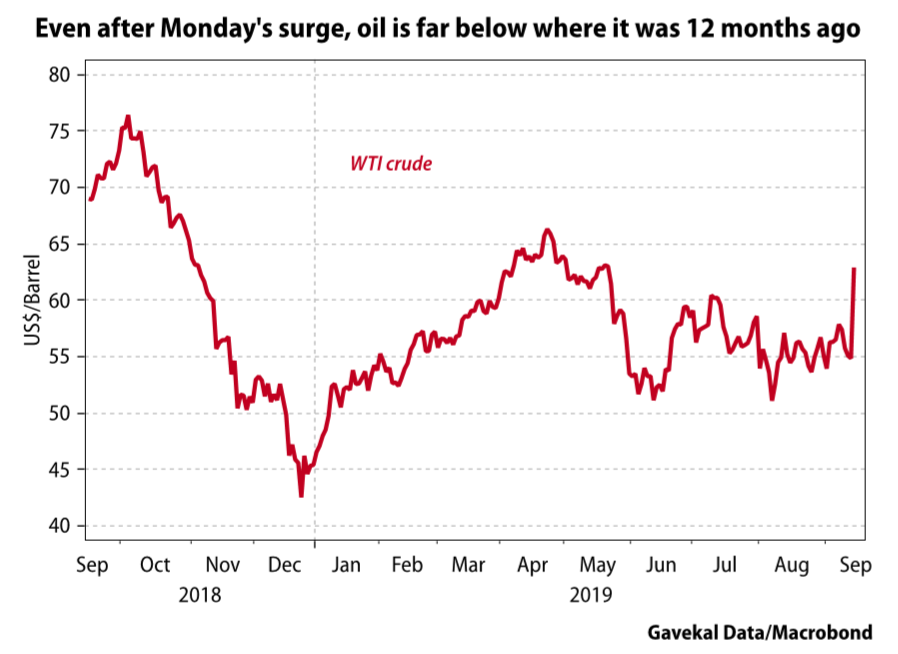

All told, Monday’s market response to the weekend’s attacks in Saudi Arabia was fairly nonchalant. Sure, oil prices shot up. But currencies were broadly stable, as were bond markets. And while equity markets pulled back, the drops were in no way remarkable. In percentage terms, oil prices rose by double digits, but that rise left other asset classes unimpressed. This may be because Monday’s surge only pushed oil back to where it traded in May this year; it still remains far below the levels of a year ago.

Or maybe the market assumes the whole mess will blow over. As Donald Trump put it on Monday, “I don’t want war with anybody.” So maybe investors are resisting the temptation to panic. Even so, this weekend’s attacks have clearly unsettled a number of our clients, and over the past 48 hours we have received a number of questions on the topic. Here are my attempts at answers.

Question #1: Why?

You may have heard the story of the camel and the scorpion. The scorpion wants to cross the river and asks the camel to carry him across. The camel answers: “If I give you a ride on my back, you will sting me and I will die.” The scorpion replies: “But if do that, I will die too.” Persuaded, the camel agrees to carry the scorpion across. But in the middle of the river, the scorpion stings the camel. As the poison takes hold, the camel asks: “Why did you do that? Now we will both die”. The scorpion replies: “Yes. This is the Middle East”.

Jokes aside, considering the likely motive for, and timing of, last weekend’s attacks, there are three possible conclusions:

Of these four possible options, the first would be by far the most “bullish”. If the weekend’s destruction was really the work of internal Saudi insurrectionists, then the world will dodge calls for another war, with the threat of spiraling oil prices. On the other hand, if Tehran did order the attack, and if Iran does not have a nuclear arsenal with which to defend itself, then Iranian policymakers must be crazier than anybody thinks, and certainly a lot more crazy than the market has priced in.

Question #2: Who stands to benefit the most from the current mess?

If Iran and Saudi do start taking out each other’s oil facilities, then Russia will reap the biggest rewards. The US would also be a winner, now that it is a net energy exporter. Other politically-stable oil-producers should also benefit, including Canada, Norway and Brazil.

Question #3: And who loses?

Few Asian countries want a higher oil price—least of all China, which is the world’s largest oil importer and whose current account balance now swings from mild surplus to deficit with shifts in energy prices. So, this is not good for China, on multiple fronts.

*Initial Public Offering, or new issuance of publicly-traded shares.

Still, it is not as if Beijing was caught unaware by these developments. China has long identified its dependence on imported oil and gas as one of its biggest vulnerabilities. In recent years, Beijing has worked hard to solve this predicament by building its strategic reserves (its oil imports have far outpaced its immediate needs), and by signing long term supply deals with the likes of Russia and Qatar. Nevertheless, it seems likely that there were some long faces in the corridors of Zhongnanhai this weekend.

Question #4: Buy or sell bonds?

If these attacks lead to war, whether between Saudi and Iran, or the US and Iran, should we buy bonds, or should we sell them? On one hand, greater uncertainty and mounting fears are usually bullish for bonds. On the other hand, wars are usually inflationary, and inflation is bad news for bonds. What should we do?

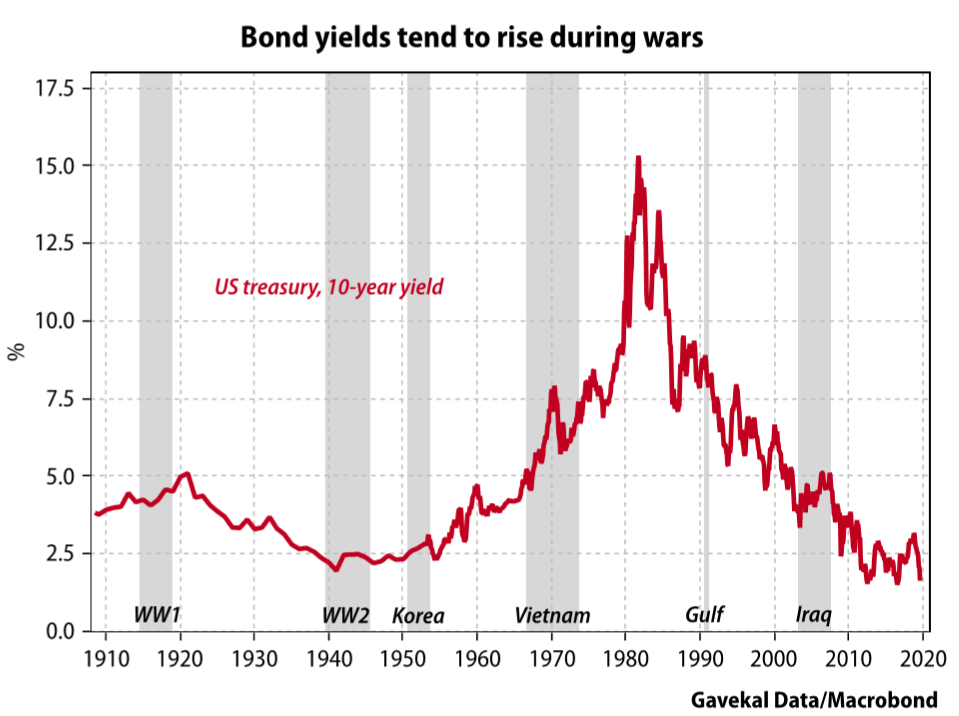

When it comes to inflation, I still believe that Jacques Rueff put it best: “Inflation consists of subsidizing expenditures that give no returns with money that does not exist”. It’s not that wars give no returns. They actively destroy entire capital bases: physical capital, intellectual property, human capital and more. And so, even though at the outbreak of hostilities investors initially seek refuge in bonds, over the course of a war yields tend to rise. And sometimes they continue to rise even after the war comes to an end (as the chart below shows).

The bottom line is that wars are inflationary. Instead of “producing more with less,” which is the essence of what capitalism is all about, wars turn everything upside down, and invariably countries start to produce less with more: more paperwork, more inefficiencies, more bureaucracy etc. As a result, I struggle to see why last weekend’s events should be seen as bullish for bonds.

Question #5: Why hasn’t oil risen more?

The US shale boom of the last decade, combined with the recovery of Iraqi production (Iraq was producing 2mn barrels per day (bpd) a decade ago; it now pumps 4.5mn), and more recently Libyan production (from less than 0.5mn bpd to more than 1mn) may have lulled the market into a false sense of security in which the prevalent belief is that the world is awash with oil. Combine this with the growing rumbles from politicians around the world—in Germany, France, the UK, China, and from the US Democrats—that they are going to pour billions into “green technologies” and investors may naturally be gun-shy.

Another factor may be that for the last decade, energy has been the biggest dog of a sector in the market. By now, any portfolio manager with a pro-energy bias has either been fired or has forsworn energy investing entirely, if only for career preservation. As the financial media have repeated again and again over the last 24 hours, in one form or another: “If it takes the threat of a full-blown war for energy to be interesting, then energy really can’t be that interesting as an investment!”

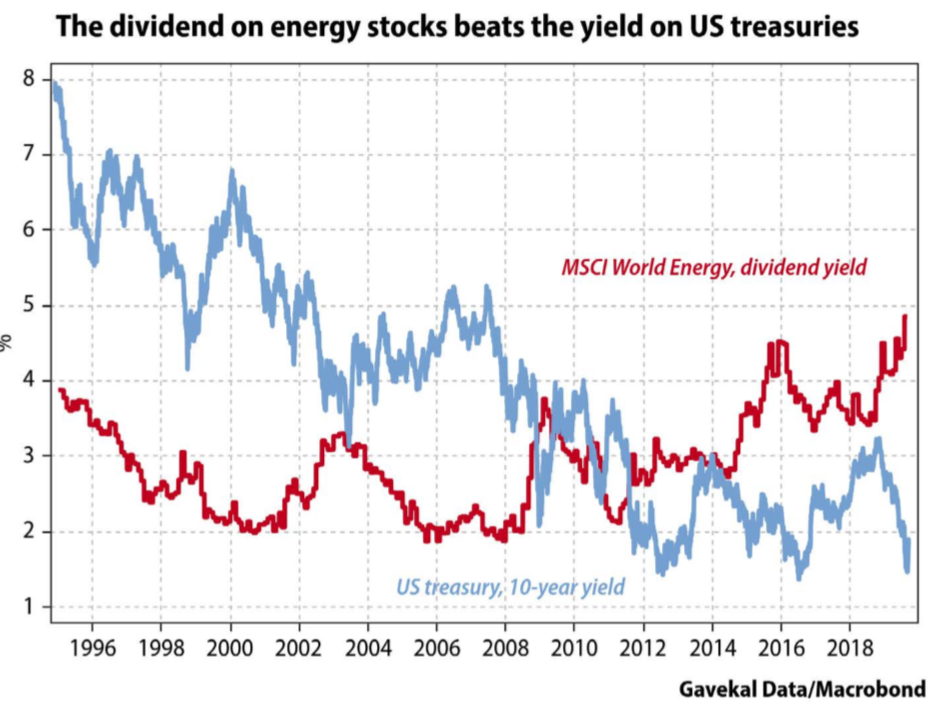

As readers may know, in recent times I have argued precisely the opposite. In a world in which almost every asset is now priced off a stupidly low interest rate and the hardcore belief that central banks will always provide a backstop, energy may well be one of the few remaining genuinely uncorrelated asset classes.

With this in mind, perhaps a truly balanced portfolio no longer consists of growth stocks hedged with a long bond position—that is a “dumbbell portfolio” which is now a doubled-up bet on ever-falling interest rates. Instead, the balanced portfolio of the future might be growth stocks hedged with energy stocks. Instead of owning 10-year US treasuries, investors may be better served holding energy stocks. Firstly, such holdings would offer a buffer should war break out and oil prices continue to shoot up, destabilizing the current narrative of ever-falling inflation. Secondly, unlike most government bonds today, energy stocks actually offer solid yields of around 5%*. In fact, energy stocks offer record high yields, which unless oil prices tank should help cushion any potential price downturn, which is more than bonds can now say.

*Evergreen note: And far higher with US energy infrastructure securities.

Question #6: What about the Saudi peg?

Is the Saudi currency peg to the US dollar at risk? And if Saudi’s peg goes, who else follows in its wake? Could we have a tidal wave like in Asia in 1997?

For the Saudi budget to balance, Riyadh needs oil to be at or above U$80/bbl with the kingdom producing and selling just shy of 10mn bpd. Now, if the Saudis continue to pump only 5mn bpd for any meaningful period, it seems pretty obvious that the price of oil won’t stay where it is. But will it rise to US$160/bbl? If so, then mathematically, selling 5mn bpd at US$160 will be a much better deal for Riyadh than selling 10mn bpd at US$65.

Of course, we are a long way from seeing such numbers, which would surely trigger a surge of production around the world—from US shale producers, Brazilian offshore fields, Russia etc.—that would likely end up considerably undermining Saudi’s long-term position as global swing producer.

In the meantime, for every day that 5mn barrels stay in the ground, Saudi loses approximately US$300mn. That’s unfortunate. And if we assume that most of the production will come back on stream fairly quickly, but that it will be months before the last 500,000 barrels see the light of day, then Saudi Arabia still stands to lose US$30mn per day. That’s US$10bn a year, or in other words, one whole contribution to SoftBank’s Vision Fund.

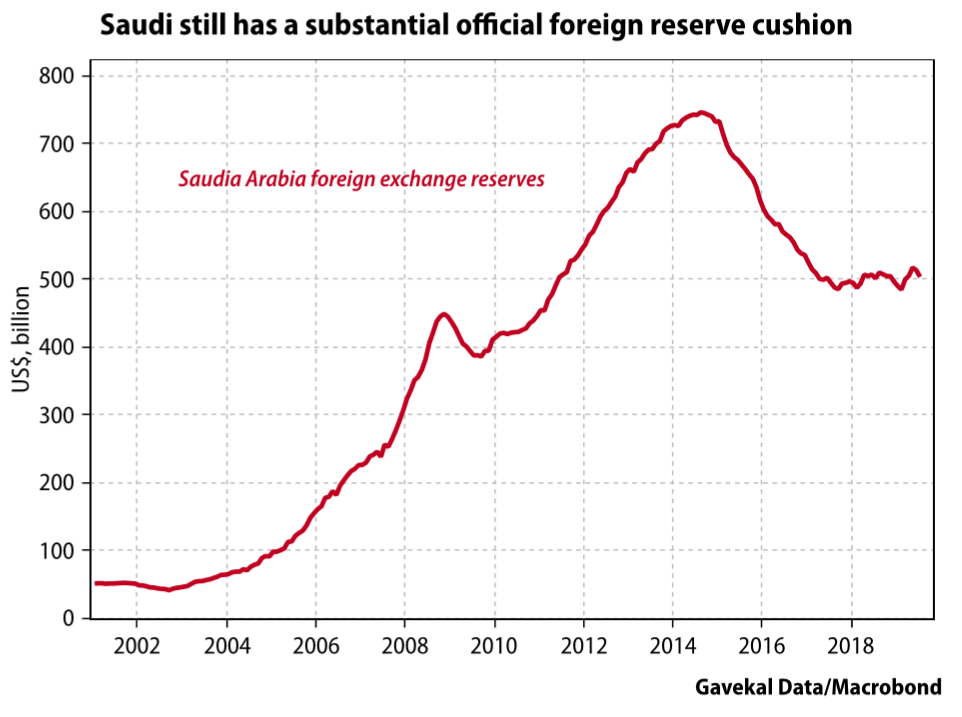

In short, Saudi can easily take a US$10bn hit. But a 5mn bpd, US$100bn a year hit would be crippling, even if Riyadh does still have some US$500bn in official foreign exchange reserves.

On this topic, note how Saudi’s reserves were in precipitous decline up until November 2017. Then the decline stopped, and ever since reserves have been flat lining. As it turns out, November 2017 happens to be the date when the Riyadh Ritz-Carlton stopped taking new bookings, and when the rich Saudis who were in residence found themselves wishing dearly they were staying almost anywhere else!

Clearly, with a little arm-twisting, Crown Prince Mohammad bin Salman managed to “convince” his various cousins to stop exporting capital, and perhaps even to bring some capital home. This helped to stabilize a peg that, at the time, seemed under threat. But is this a trick that can be repeated?

Having said that, for now the peg doesn’t seem to be in immediate danger of imploding. This is just as well, because it is very possible that a rupture of the Saudi peg could unleash a new wave of instability and revolutions across the Middle East. Consider the following:

Meanwhile, we know that the Saudi government helps to prop up a number of regimes across the Middle East. If funding from Saudi were to dry up, what would happen to Egypt? Lebanon? Pakistan? In that sense, a break in the Saudi peg could prove highly destabilizing right across the region, all the way from Cairo to Karachi.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.