"No one can possibly achieve any real and lasting success or get rich in business by being a conformist."

- J. Paul Getty

"If you’re looking where everybody else is looking, you’re looking in the wrong spot."

- Mark Cuban, technology entrepreneur and owner of the Dallas Mavericks

POINTS TO PONDER

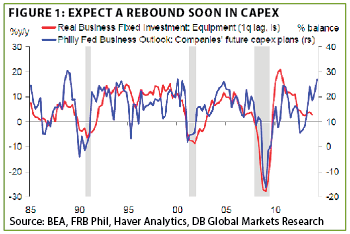

1. Capital spending has been a major underachiever during this expansion. However, it may be poised to surge based on the recent leap in the Philadelphia Fed’s Business Outlook Survey. Over the last 30 years, this report has closely mirrored business investing, often providing advance indications of up-turns. (See Figure 1)

2. Top-notch economist David Rosenberg has noted that given the considerable improvement in the Leading Economic Indicators (LEIs), US GDP growth should continue at a healthy pace for the balance of the year.

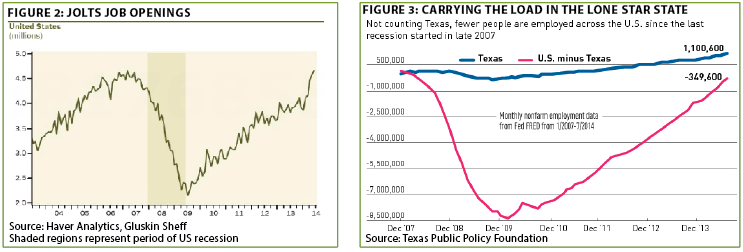

3. Barron’s recently ran a cover story on the new trend toward employable Americans choosing to remain "on the dole." Considering job openings are back to their peak from the prior (and much stronger) business cycle, their contention seems credible, especially considering the near record-low participation rate (percent of population working). (See Figure 2 below, left)

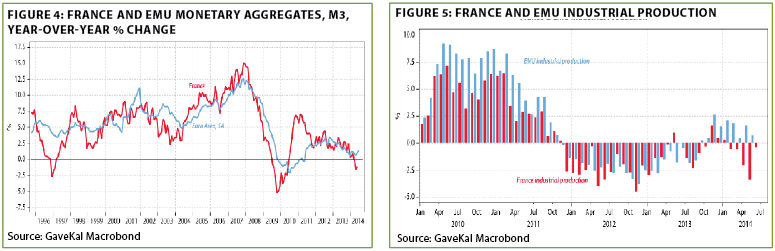

4. Texas is a state that many on the coasts love to hate, or, at least, denigrate. Yet, it is hard to quibble with its economic performance. Since the end of 2007, just prior to the Great Recession, Texas has created nearly 1.5 million jobs, while the rest of the country has lost 350,000. (See Figure 3 above, right)

5. During the ultra-lax lending days of 2007, so-called covenant-lite loans, providing limited protection to lenders, represented 25% of all new deals. Today, that share is 62%.

6. Previous EVAs have noted the increasing "junkification" of the US corporate bond market. Illustrating this trend, 72% of new issues in 2013 were single-B rate (5 clicks below investment grade). In the 1990s, B-rated debt averaged just 31% of total issuance.

7. In addition to advantages such as an AAA sovereign credit rating, a balanced budget, and responsible monetary policies, Canada also offers the lowest total business tax costs among the 10 largest economies, per KPMG.

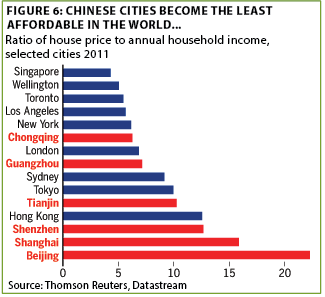

8. European Central Bank (ECB) chief Mario Draghi has announced a program to purchase nearly $1 trillion of Asset Backed Securities, such as business and residential loans. Naturally, in keeping with our new era, this will be funded by the ECB’s printing press. Prior to his latest "Hail Mario" play, money growth in the overall eurozone was exceedingly lethargic, even entering negative territory in France. Speaking of France, its industrial production is also contracting, making it a laggard even compared to its sclerotic neighbors. (See Figures 4 and 5)

9. Evergreen is among those who suspect China’s GDP growth rate is well below the official 7% level. It’s widely believed power consumption is a better indicator of actual economic trends. The fact that it has lately been running in the 4.5% range implies a much more pronounced slowdown than is officially acknowledged.

10. Signs are proliferating that China’s massive property boom has turned into a bust. Based on how expensive real estate prices are relative to income, the downside could be material. (See Figure 6)

THE EVERGREEN EXCHANGE

By Jeff Eulberg, David Hay, and Tyler Hay

The talented Mr. Draghi. It seems implausible, and many investors have apparently forgotten, it was just over two years when markets last feared the entire European Union was on the verge of collapse. European bond markets were panic-stricken with 10-year Spanish and Italian debt yielding more than 6%. Stock markets across the continent were plummeting. Then, with much gusto, Mario Draghi famously proclaimed, "Within our mandate, the ECB (European Central Bank) is ready to do whatever it takes to preserve the Euro." He then added, "And, believe me, it will be enough." Was it ever!

Fast-forward to today: Spanish and Italian debt is barely yielding 2%, and both currently trade at lower yields than US treasuries. Perhaps not since Jesus’ "Sermon on the Mount" has rhetoric been so widely embraced. Who knows what wonders Mr. Draghi could have worked with some bread and a few fish?

Since Draghi’s proclamation, economic data out of Europe has continued to be lackluster. Many of the EU’s largest countries are struggling to stay above recessionary levels, while smaller member countries struggle to fend off deflation. Despite Draghi’s aspirational promises, the ECB had done little to actually support the European economy, but last Thursday that changed. In an effort to spark growth and defend against deflation, Draghi announced that the ECB would use more of the monetary tools available to them. The central bank committed to expanding its balance sheet by purchasing an estimated $1 trillion (US) in asset backed securities. Then, on top of the new quantitative easing, the bank lowered its main lending and bank deposit rates to negative .05 and negative 0.2%, respectively.

Now that we know Europe is firing up their printing presses, traders must be salivating at the opportunity to put on a massive carry trade. As a quick refresher, a carry trade is defined as borrowing in a depreciating currency (at low interest costs), and investing those funds into assets in a stronger currency, which offers higher rates of return. If Draghi is willing to do everything necessary to support the Union, then expect low interest rates, lots of added liquidity, a declining Euro, and a commitment to these policies—an almost perfect scenario to borrow and invest elsewhere. So where may the funds be headed?

With all of the turmoil in the global markets, I see the US as one of the few destinations (along with Canada) for these funds. Even after five years of the US economy growing at less than a 2% clip, it’s tough to envision a more suitable place to invest the proceeds of Draghi’s policies. The Federal Reserve is about to part from its easy money ways, and markets seem to have complete confidence in a US recovery. However, with its yields close to multi-year lows, the US debt market may not be the only place where European money lands. The excess liquidity could also spill into equity markets, along with other US assets not typically used in large carry trades. As Hyman Minsky famously said, "Stability breeds instability."

If I’m right, and we see a colossal carry trade out of Europe, I see two likely scenarios that could spell trouble for traders. First, due to fears about increased asset inflation and excess liquidity, the Fed may tighten monetary policy much sooner than the market currently anticipates. Initially, markets may not react drastically, but once interest rates start to normalize, the unwinding of the carry could quickly gain momentum, causing numerous asset prices to weaken, perhaps significantly.

The second scenario, and the one that I find most concerning, would be a major rally in the US dollar. Currently, we are seeing considerable selling of the yen, euro and, recently, British pound (the latter suffering due to the potential of the UK to be a much less united kingdom) to fund purchases of US dollars. If the dollar rises significantly from here, the global price increase of US goods may cause our already meager recovery to falter, forcing the Fed to fire the printing presses up—again. The Fed initiated this debasement game, and I wouldn’t bet against Janet Yellen in the contest to see who can make the cheapest currency.

When announcing the policy changes, Draghi warned, "No amount of fiscal or monetary accommodation, however, can compensate for the necessary structural reforms in the euro area." Unfortunately, some of the more troubled countries in the EU aren’t exactly known for their ability to implement positive structural reform. And, it’s important to remember that Germany doesn’t want to print money and don’t fully endorse this policy. Germany has surely paid close attention to the American and Japanese QE programs, and I think they’ll have such an experiment on a much shorter leash than those countries. So, if traders think this policy can be implemented for many years without true results, they’re likely to be seriously disappointed. Germany will want quick results, and they won’t be fooled by higher asset prices.

Due to easy money policy across the globe today, barring geopolitical crisis, the table appears set for another rally in US asset prices. This scenario would create a party-like financial environment of soaring valuations and unbridled investor ebullience. At Evergreen, though, we’d RSVP "no" to such an extravaganza. We don’t seek expensive assets, hoping that someone else will come along and elevate prices even further. We continue to stay invested where we think there’s reasonable long-term return potential, maintaining enough liquidity to take advantage of opportunities when panic sets in and leveraged trades unwind. While bold speeches from Mr. Draghi may invigorate the masses, meaningful reforms and reasonable valuations are far more important in our investment process.

The REIT stuff? There’s an axiom among financial professionals stating that in a crisis, all correlations head toward one. That’s a fancy way of saying that, during times of panic, almost all investment categories—aka, asset classes—start behaving the same. Simply put, in episodes where fear reigns supreme, domestic equities, foreign stocks, commodities, and most bonds (excluding the very safest) all do a synchronized face-plant.

Today, however, we’re seeing a different version of the "dash to one." This time around it’s a fall toward, rather than rising to, what the legendary rock band Three Dog Night called the loneliest number. Around the world, government bond yields seem to be in an inexorable downward arc toward 1%, in some cases even below. Germany recently saw its 10-year "bund" yields briefly break below that incredibly low level. Even France, despite a financial profile that is beginning to resemble Greece, is only required to pay 1.3% to issue sovereign debt due in 2024. In fact, per David Rosenberg and the B of A Merrill data base, nearly half of the planet’s government bond yields are below 1% when taking into account shorter maturities.

Thanks to last year’s "taper tantrum," 10-year US treasuries are yielding 2.5%, after briefly breaking above 3% at the end of 2013. However, it’s doesn’t take clairvoyant powers to see them returning to under 1.5%, where they were a couple of years ago, or even lower, during the next recession and/or financial crisis.

As I’ve noted multiple times this year, this is exactly the opposite scenario envisioned by the majority of the investment community at the outset of 2014. Rates were supposed to rise, driven by an accelerating global economy—not erode toward nothingness. Obviously, this is a serious challenge for income-needy investors who have already been punished by essentially zero short-term interest rates for years.

Offsetting this pain, at least for Americans, has been the powerful surge of the US stock market. This has made most of us feel a lot richer, even though the recurring cash flows from our portfolios have continued to melt away. So, that leaves us with some crucial questions: What happens when stocks quit elevating, or, almost unthinkably, when they endure a bear market? Where in the world do investors migrate in that scenario in order to produce some kind of return a person can actually live on? (If you can get by on a 1% yield, you are rich indeed!)

Not to fret, however—I come bearing good news (don’t faint over that line)! There’s an asset class that offers the kind of cash flow and undervaluation that was available several years ago, before the Fed decided their new motto is "interest rates are evil and they must be eliminated." Even better, it’s close to home and is available in an underpriced currency with, in our view, far better intrinsic fundamentals than the US dollar .

Almost 50 years ago, young Americans headed north to Canada in droves to escape the draft. These days, boomers, either retired or soon to be, might need to repeat this exodus (at least with their cash) in order to avoid the threat of yield starvation.

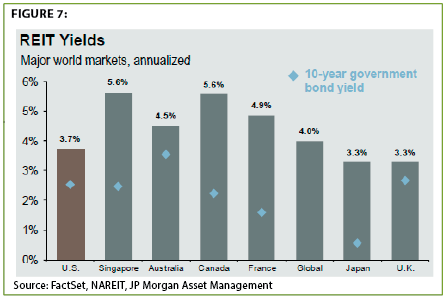

Long-time readers are aware that Evergreen has been negative on US REITs for several years with the qualification that, during the aforementioned taper tantrum, some smaller issues declined to attractive price points with yields in the 5% to 6% range. Other than that, however, the REIT pickings have been anorexic. The situation in Canada, though, is radically different. While blue chip US REITs yield around 3.5%, their Canadian counterparts pay distributions producing cash flow returns in the 5.5% range. In fact, Canadian REITs are among the "yield direct" in the developed world. (See Figure 7 above)

One of our favorites, which we have begun to buy for almost all of our clients, yields over 7%. In case you think this is because they are the REIT equivalent of a slum landlord, it’s not. In fact, this entity owns "Class A" properties, mostly of the high-rise office variety, heavily skewed toward extremely valuable metropolitan (CBD) locations. Below are photos of some of their key holdings.

In our view, what makes this opportunity even more alluring is that Canada’s currency, the Loonie, is trading at almost a 10% discount to the greenback. Frankly, our Canadian bond exposure has been one of our worst income performers over the last year and a half, strictly as a function of the Loonie’s swoon from around parity to the US dollar to 91 today. But rather than look at this as a negative, we see it as a wonderful chance to further diversify into a currency that has a much healthier long-term outlook—at least based on current US fiscal, monetary, and regulatory policies.

Partially as a result of the weaker Canadian dollar and partially due to a drop in REIT prices in Canada, the index up north for these real estate securities has fallen by nearly 20% from its peak. High-quality "Canuckian" REITs are trading at 15 times free cash flow (technically, adjusted funds from operations—AFFO), versus 22 times in the US. This is obviously the main reason these issues yield so much more than blue chip US REITs.

This is not to say it’s a layup, sure-winner investment opportunity. Should global equity markets sell off hard—say, caused by another flash crash in the US—Canadian REITs will almost certainly go down even further. Yet, that would make their yields all the more enticing, allowing us to increase our exposure. Moreover, the lower risk-free interest rates that would result from a market wind shear, likely driving the US 10-year treasury closer to 1%, would eventually be extremely supportive of safe yield instruments.

On the safety front, I should also note that during the global financial crisis—when nearly every US REIT either omitted or cut its distribution (or resorted to paying it in stock versus cash)—none of the leading Canadian REITs reduced or played games with their payout. And it’s doubtful that any downturn on the horizon will be as severe as 2008/2009 (or so we should emphatically pray). As such, it’s hard to visualize a future reduction in payouts from the Canadian REIT universe, other than perhaps a few isolated cases.

It’s possible, though far from certain, that we are going to be in an ultra-low yield world for many years to come. The cynical rationale being that "rich" governments realize the only way they can service their overwhelming debt loads is with rates near zero. Thus, it is in their best interest (pun intended) to keep growth sluggish, using regulatory tools (like forcing banks to buy government debt) to suppress yields. If so, being able to lock in 5%-7% income returns from Canadian REITs might be another fleeting yield opportunity--one that the not-so-shy, but definitely retiring, "me-generation" might not want to miss.

![]()

Say goodbye to your wallet. Earlier this week, Apple’s CEO Tim Cook took the stage in Cupertino, California to introduce the highly anticipated iPhone 6, as well as the long-rumored Apple Watch. Given the suspense build-up, this was certainly welcome news for consumers and shareholders alike. While the Watch and new iPhone are grabbing headlines, I think they’re overshadowing the bigger development from yesterday’s event: The iPhone 6’s new mobile wallet feature. Cook said that Apple wants to replace the traditional wallet with a more convenient and secure mobile solution. I’m going on record now: In five years, physical credit cards and billfolds will be as outdated as pay phones and the yellow pages.

Over two years ago, I wrote an article for the investing website Seeking Alpha (they must have been really desperate for content). In the article I argued that, while there are many ways the mobile payment landscape could unfold, unless Apple joined the fray, mass adoption was unlikely. (Click here to read the full article.)

Since the article was published, almost nothing has changed within the mobile payment space. Small advancements by companies like Google and PayPal have attempted to replace the traditional wallet, but widespread adoption wasn’t on the horizon—until Tuesday.

The key thing to remember about Apple is that they don’t invent, they perfect. When the iPod was introduced it was simply a competing technology with mp3 players. They were far from the first to market, but Apple made listening to music electronically simple and—more importantly—cool. The scroll wheel on the first iPod, coupled with its easy to use software, seamlessly integrated with iTunes, made for an elegant user experience. Even the smart phone was invented by IBM!

The mobile wallet functionality, called Apple Pay, will follow a similar blueprint. Their goal is simple: Deliver a convenient and secure way for consumers to pay for their goods without needing a wallet. Here’s how it will work: First, when setting up the new iPhone 6, existing Apple customers will have the option to link the current credit card on their existing iTunes account to their new phone. Users can also add additional cards they want stored for future use by simply uploading a photo. It’s important to note that the phone will not store the entire credit card number. This means if your phone is stolen, the thief won’t have access to your credit card info. Adding more convenience, at checkout, you simply wave your phone past the merchant’s machine, which detects your phone. Then, you simply provide a thumbprint to verify your identity.

Now, all of this sounds pretty cool, and I do believe that Apple will be successful where so many others have failed. But, there are some sizeable obstacles that must be overcome for widespread adoption to take place. For starters, initially there will be a limited number of retailers whose point-of-sale systems accept this form of payment. In a classic chicken and egg impasse, merchants have been very reluctant to invest in these more advanced payment systems until consumers could do so with a mobile device. Now, I believe that with Apple’s brand behind it, merchants will be willing to go out on a limb they previously avoided. Still, even if merchants upgrade their systems to allow for mobile payments, there’s yet another hurdle: Not all consumers have (or want) an iPhone. Therefore, there will need to be additional mobile payment solutions developed by companies like Google, Microsoft, and PayPal if the physical wallet is to be truly retired. Yet, even though it’s unclear how these companies will do it, I think Apple’s announcement will serve as the first shot fired in mobile wallet revolution.

From an investment standpoint, there are some direct and indirect implications worth considering. First, for Apple, their hefty clout allowed them to negotiate a portion of the processing fee, which traditionally went to banks. As more details emerge on their agreement, we will get better visibility as to how much of a profit driver this will be. In addition, Apple Pay further engrains customers in the Apple "ecosystem." I foresee Google, Microsoft, PayPal, Samsung, and more quickly rolling out other payment systems to provide consumers with an alternative. Failure to evolve could put all of them at a significant competitive disadvantage, allowing Apple to dominate yet another high-growth market.

Credit card companies like Visa, Mastercard, and American Express, are clear beneficiaries. The biometric signature, combined with the more secure storage of credit cards (the fact that entire credit card numbers aren’t stored), will greatly increase fraud protection. Payment solution providers, such as Verifone, stand to benefit from an upgrade cycle as merchants buy new systems to accept digital payments (assuming merchants believe consumers will adopt these digital payment methods).

As a society, it seems we’ve become numb to major innovation. In a way, this is a good thing. Technological advances are happening at such a rapid rate that we don’t even stop to notice. As we edge toward the age of the Jetson’s, consumers adopt anything that makes their life easier. Earlier, I mentioned that in order for mobile payments to really gain traction we would need Apple to lead the charge. Tuesday, I watched eagerly as Tim Cook laid the groundwork for digitizing the way consumers and merchants interact. It won’t take long to know if consumers take the leap to mobile payments, but my bet is they will. If so, celebrate, because this means one of the most terrifying phrases ever uttered will no longer be spoken: "I’ve lost my wallet." *

*The specific securities identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. ECM currently holds Apple and purchases it for client accounts if ECM believes that it is a suitable investment for the clients considering various factors, including investment objective and risk tolerance.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.