“History doesn’t repeat, but it does rhyme.”

–Controversially attributed to Samuel Clemens, aka MARK TWAIN

“A bull market does not stay down long enough for you to buy, and a bear market is one that does not stay up long enough for you to sell.”

–MIKE O’ROURKE, Chief Market Strategist of Jones Trading

A Tale of Two Markets, Redux. It never ceases to amaze me how conditions can change almost instantaneously in the stock market. It was only a couple of months ago that the S&P 500 seemed invulnerable and on pace for a double-digit return year. However, as we approach the end of 2018, with countless investors praying for a Santa Claus rally, any gain would be appreciated.

Now, a flat year is not exactly a disaster but, as was the case in 2015, the superficial return number for the S&P doesn’t come close to telling the full story. As of the close of this week, the performance of the NYSE issue was -5.9% while the ValueLine Universe of 1700 stocks was -7.9% (be sure to note the minus signs!). Moreover, it’s a global market out there even though investors have increasingly clustered into the US because – as usual – that’s what’s been working in recent years. The MSCI World Index, excluding US stocks, was down -11.3% through 12/14/18.

Even in America, the still-stellar performance of a few monster-cap companies has propped up the S&P, as also happened in 2015, notwithstanding their recent de-rating (a fancy term for a market spanking). Almost all of these are tech or tech-related and several remain up 20% for the year.

As the above implies, if one drills down a bit there has been considerably more carnage. This damage has become severe and widespread enough to qualify for a “two-tier market” designation. Please allow me to elaborate with a trip down memory lane.

In the late spring of 2000, technology stocks (and a few mega-cap issues like, ironically, GE) had enormously out-performed the overall stock market over the prior two years. This is despite the fact that the great tech-wreck, which would lead to an eventual 78% obliteration of the NASDAQ, was already under way. In vivid contrast, most stocks, especially those of a value nature, had been in a below-the-radar bear market since the spring of 1998. During those 24 months or so of diverging performance, this author was constantly making the argument that it was a tale of two markets—i.e., a two-tier market—with a gaping chasm between the haves and have-nots. (Long-time EVA readers can easily imagine where my portfolios were most exposed in those days.)

The re-emergence of this condition is the reason for this Special Edition EVA. The déjà vu I’m presently experiencing occurs when I look at high-quality companies selling at single-digit P/Es vis-a-vis those of comparable stature (or lower) trading at 25 times earnings, if not substantially more. This is simply too dramatic for me not to do a shout-out about. (Sorry, I know sentences aren’t supposed to end with prepositions, but I like the rhyme.)

Consequently, it’s becoming hard to maintain a negative attitude toward the overall US stock market. It’s more accurate, I think, to say that large portions of it remain over-priced—in many cases, obscenely—while a growing share is looking downright appetizing. When foreign markets are included, the bargains are even more galore.

Looking at specific examples is always more helpful. Accordingly, one of our recent purchases is among the most venerable and respected life insurance companies in the country and the world. It is down about 35% from its January 2018, high. It sells at a skimpy 7 times this year’s essentially in-the-bag earnings and sports a 4.4% dividend yield. Another much smaller company—and heavily exposed to the far more cyclical property/casualty side of the insurance business—sells at 25 times earnings with a mere 2.7% yield.

This is far from an isolated instance. In fact, I’ll give you one more that is even more mystifying. Another recent purchase we made is a company that is in the IT category, though it has some financial sector characteristics. Its earning track record is simply one of the best I’ve ever seen. Profits even expanded by 15% during the Great Recession when most companies saw their sales fall by 20% to 25% and earnings were absolutely crushed (not to mention that a long list of actual financial institutions had near-death experiences). Over the past decade, this firm’s profits have swelled by 400% with nary a down year. Despite this remarkable performance, it is trading 40% below its peak in late 2015 and sells at a P/E of 8. That’s right—ocho.

The counter-example for this one isn’t as clean a “comp” as with the two insurance companies because this priced-beyond-perfection issue is in a different industry. In fact, they sell a mundane product that is in almost everyone’s home and/or garage. To give you a bigger hint, it comes in a blue and yellow can. For sure, it’s had a nice earnings history, but profits did dip in both 2008 and 2009. Over the past 10 years, profits per share have compounded at a solid, but unspectacular, clip of 7%. Yet—and this is another clue as to its name—it sells for 40 times earnings. Go figure. Maybe you can justify the disparities, but we can’t.

To further drive home this point, I’ve gone through the 47 companies that Evergreen holds for growth (vs income) purposes on behalf of its clients and 14 of them sell for single digit P/Es. Another 7 trade at between 10 and 12 times their estimated profits for this year. Moreover, they are scattered across most of the S&P sectors, so these alluring valuations are not just specific to one or two out-of-favor areas.

Even in the once uniformly white-hot tech sector, there are a number of stocks whose prices have been pounded down enough to qualify as genuine bargains. (By the way, Forrest Gump’s favorite “fruit company”, which not long ago briefly pierced the $1 trillion market value mark, just missed the cut at 12.7 times this year’s profits). Therefore, even in tech, a two-tiered market has emerged.

Admittedly, a number of the cheapest names we own are domiciled overseas. But, in most cases, they are world-class multinational enterprises. It’s no surprise that quite a few of them are energy-related and, once again, this sector has been taken out back and shot like a vicious dog. As you can see, the energy sector is trading at very close to 30-year lows relative to the overall stock market.

ENERGY SECTOR AS % OF S&P 500

Source: Bloomberg, Evergreen Gavekal as of 12/12/2018

What’s ironic is that oil and gas companies have been the main earnings overachievers for nearly three years now. Further, in the mid-stream energy sub-category (MLPs), I’ve never seen such a disconnect between robust--even spectacular--operating results and market prices that can only be called pathetic. It’s our belief that any meaningful near-term rally is likely to include a number of energy securities among its leaders.

Lest you think we’ve become raging bulls, please realize we have only committed a modest portion of the humongous cash reserves we hold for clients. Additionally, we’ve been doing very small buys which is fortunate since almost everything we’ve bought lately has continued to go down! (To be fair, over the course of this year we’ve done a lot of selling and most of those issues have been pummeled, as well.)

These are the kind of markets that I cut my teeth on over the years—and also those in which learned to cut—or at least control—my losses. They are the type where prices seem to almost melt away before your eyes. The human tendency is to freeze and not buy anything because of the immediate pain of doing so. But, in the long-term, that’s a big mistake. Making smaller buys and being prepared to add more on the likely further weakness has worked far better over my career.

We are further aware that cheap stocks can become much cheaper, particularly if we are truly entering a major bear market. In that regard, a recent Wall Street Journal article headline caught our eye—even though it was buried on page B6! It was titled, “Many US CFOs Predict Recession”. The article cited a Duke University survey stating that nearly half of Corporate America’s CFOs (chief financial officers) see a recession before the end of next year. And 80% think a downturn will hit no later than 2020.

These numbers are far higher than what the economic forecasting community is looking for in 2019 but, given the latter’s sorry prediction record, we’d much rather side with the CFOs. Basically, Evergreen agrees that the odds of a contraction in the US economy next year have risen materially in recent months. We’re not quite to the point where we are making an official recession call but we’re getting closer. (As a reminder, the last time we did so was in September of 2007 when we were one of the few who anticipated the 2008 downturn.)

So why buy any stocks right now, no matter how cheap they are? First, it’s still possible that the Fed can engineer a “soft-landing” for the economy, something it’s only been able to do a few times in its 100-plus year existence. Clearly, those are long odds against, and we wouldn’t bet on a gentle touch-down. But, second, bear market rallies can be extremely powerful. As noted above, we believe this is likely to be particularly true with energy. However, many of the recently slammed names, such as those described above, could also come roaring back…at least for a while.

We stick by our view expressed in prior EVAs that any big rallies are chances to reduce US stock exposure. Yet, we also concede we could see a replay of the March 2000 to June 2002 period when those issues that had been beaten-down over the prior two years actually rose in price even as the S&P fell around 30%, dragged down by its roughly 50% exposure to tech and telecom. (In July of 2002, a final 20% downside capitulation occurred and this took almost everything with it, including those stocks that had risen during the first two years of that bear market.)

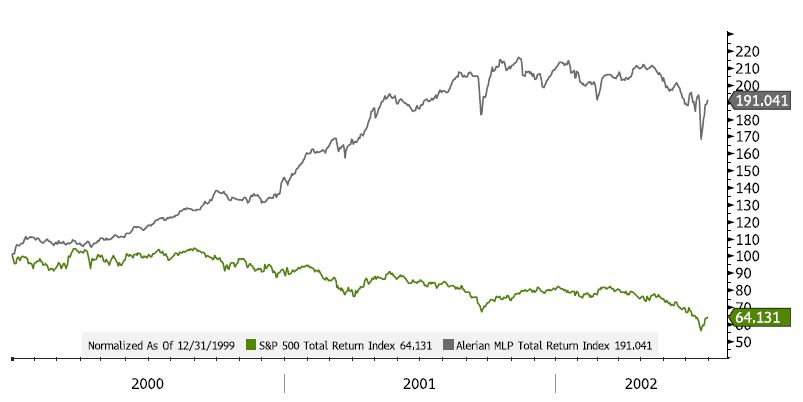

Regardless, if you are gradually accumulating fine companies at 7 to 12 times earnings, you should come out with decent, if not double-digit, long-term returns over the next five years—a timeframe when the S&P 500 may well lose money, even after dividends are included. Sound impossible? Take a look at the MLP index vs the S&P from January of 2000 (top of that bubble) to the summer of 2002 (close to the trough).

MLP INDEX VS. S&P 500 FROM JANUARY 2000 – JULY 2002

Source: Bloomberg, Evergreen Gavekal as of 12/12/2018

That’s what can happen when you truly have two-tier markets. Maybe, just maybe, to (possibly) paraphrase Mr. Twain, history is ready for rhyme-time.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE *

* Some EVA readers have questioned why Evergreen has as many ‘Likes’ as it does in light of our concerns about severe overvaluation in most US stocks and growing evidence that Bubble 3.0 is deflating. Consequently, it’s important to point out that Evergreen has most of its clients at about one-half of their equity target.

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.